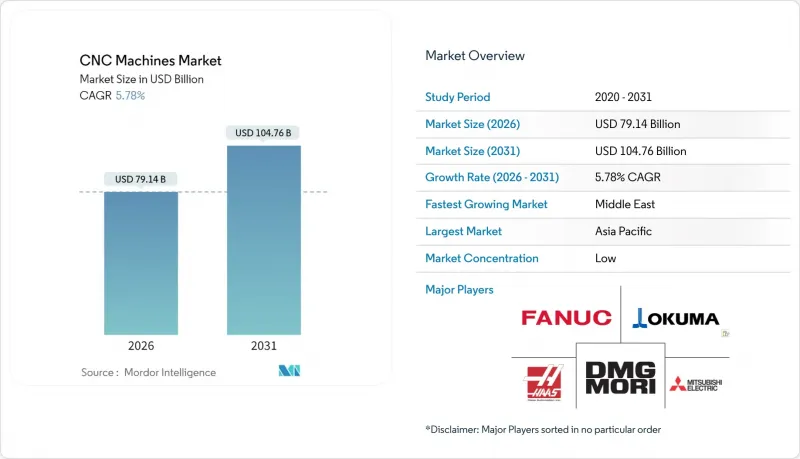

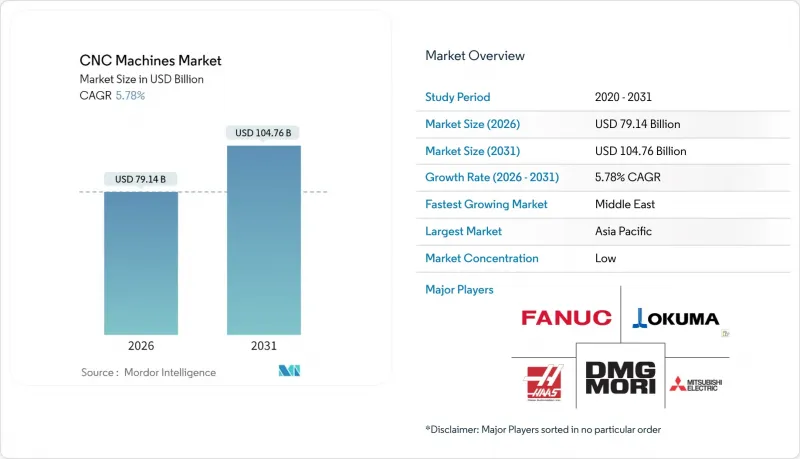

2026년 CNC 공작기계 시장 규모는 791억 4,000만 달러로 추정되며, 2025년 748억 2,000만 달러에서 성장하며, 2031년에는 1,047억 6,000만 달러에 달할 것으로 예측됩니다.

2026-2031년에는 CAGR 5.78%로 확대할 전망입니다.

디지털화 생산에 대한 수요 증가, 전기자동차 및 항공우주 프로그램의 엄격한 공차 요구 사항, 공장 현대화에 대한 재정적 인센티브 등이 이러한 확장을 종합적으로 지원하고 있습니다. 벤더들은 하드웨어, 소프트웨어, 예측 서비스를 통합하는 사례가 증가하고 있으며, 이를 통해 고객은 생산 능력을 확장하고 자산 활용도를 높이며 신규 장비 구매를 미룰 수 있습니다. 현재 조달 전략은 산업용 5G 및 엣지 컴퓨팅 플랫폼과의 상호운용성을 우선순위에 두고 있으며, 이를 통해 폐기율을 최대 30%까지 줄이고 예비 부품의 리드타임을 10% 단축할 수 있습니다. 지정학적 공급망에 대한 우려로 인해 OEM(Original Equipment Manufacturer)가 중요한 가공 작업을 국내로 되돌리면서 북미 및 유럽 연합의 국내 설치에 대한 수요가 강화되고 있습니다.

제조업체들은 고립된 공작기계에서 완전히 네트워크로 연결된 셀로 전환하고 있습니다. IoT 센서가 실시간 가동 상황을 엣지 서버로 전송하여 불량품을 30% 줄이고, 예비 부품 재고를 10% 절감하고 있습니다. 5세대 무선 기술은 기존의 지연 문제를 해결하고, 운영자에게 안정적인 연결성을 제공하여 프로그램 중단을 방지합니다. 디지털 트윈 기술을 통해 절삭을 시작하기 전에 열 드리프트와 주축의 동적 특성을 시뮬레이션할 수 있으며, 가동 시간을 40% 단축할 수 있습니다. AI 지원 툴패스 에이전트는 프로그래밍 작업량을 50% 감소시키면서 표면가공의 재현성을 향상시킵니다. 이러한 업그레이드를 통해 CNC 장비는 단독 설비 자산에서 자율 생산 루프의 노드로서의 위치가 전환되고 있습니다.

전기자동차 배터리 하우징, 인버터 플레이트, 모터 고정자에는 기존에는 항공우주 구조물에 한정되었던 공차 범위가 요구되어 자동차 공장에서의 5축 가공의 보급을 촉진하고 있습니다. 항공우주 분야의 회복은 제2의 정밀 가공 수요를 창출하고, 티타늄 및 탄소섬유 부품은 기존 매개 변수를 넘어서는 안정적인 공구 접촉을 요구합니다. 하이브리드 적층 및 절삭 복합 가공 공정은 복잡한 항공우주용 브래킷의 사이클 시간을 35% 단축시키면서 치수 정확도를 유지합니다. 규제에 따른 추적성 요구사항으로 인해 마이크론 단위의 정확성을 증명하는 디지털 가공 로그 기록이 더욱 요구되고 있습니다. 이 두 분야 수요 증가로 인해 고정밀 CNC 가공 능력은 프리미엄 옵션이 아닌 기본 요건으로 자리 잡고 있습니다.

5축 가공 센터는 고정밀 회전축, 선형 모터, 열 보상 시스템을 통합하여 구매 가격을 50만 달러를 훨씬 초과하는 수준으로 끌어올렸습니다. 이는 소규모 공장의 장벽이 될 수 있습니다. 오쿠마의 추정에 따르면 수명주기 비용의 15%는 구매 시점에만 발생하며, 85%는 유지보수, 에너지, 예기치 않은 정전에 따른 비용으로 발생합니다. 디지털 트윈 라이선스나 AI 모듈은 기업 자원 계획에 추가 비용을 쌓이게 합니다. 연구에 따르면 하이브리드 적층 및 절삭 가공 셀은 특히 분말이 고가인 경우 투자 회수가 현실화되기 전에 철저한 로트 크기 분석이 필요합니다. 따라서 높은 소유 부담으로 인해 소량 생산 업체로의 보급을 제한하고 있습니다.

CNC 선반은 2025년 매출의 26.95%를 차지하여 샤프트, 부싱 등 여러 밸류체인에서 회전 부품 제조의 필수적인 역할을 지원합니다. 간편한 프로그래밍과 견고한 공구를 통해 신속한 셋업이 가능하며, 자동차 및 유압 장비의 Tier 1 공급업체에서 주력 장비로 사용되고 있습니다. 밀링 머신은 다면 정밀도가 요구되는 직육면체 형상 가공에 있어서는 차선책입니다. 한편, 레이저 커터는 강철, 알루미늄, 복합재 적층을 최소의 왜곡으로 절단하는 파이버 레이저 소스로 인해 8.55%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다.

프리마파워의 'Laser Next 2130'은 지멘스의 'SINUMERIK ONE' 제어장치와 결합하여 자동차 BIW(Body In White) 라인의 동적 반응성을 20%, 생산성을 13% 향상시켰습니다. 이는 복잡한 패널에서 레이저 가공이 프레스 가공을 대체하고 있는 이유를 보여줍니다. 방전가공과 연삭가공은 금형 제조업체와 베어링 제조업체에서 틈새 시장 우위를 유지하고 있습니다. 하이브리드 적층 및 절삭 가공기는 니켈 초합금의 니어넷 형상 증착을 가능하게 하고, 동일한 테이블에서 마무리 가공을 함으로써 항공우주 주요 제조업체의 물류 공정을 대폭 절감할 수 있습니다. 이에 따라 CNC 공작기계 시장은 성숙한 선반 수요와 급속한 레이저 기술 혁신의 균형을 유지하고 있습니다.

2025년 아시아태평양은 전 세계 매출의 46.10%를 차지했습니다. 중국, 일본, 인도가 수입 위험을 줄이고 국내 수요를 충족시키기 위해 국내 생산 능력을 확대했기 때문입니다. 중국 퍼스트레보자동화은 국산 하이엔드 제어장치 개발을 위해 1억 위안(1,390만 달러)을 조달하여 전략 공작기계 기술의 국산화를 위한 정부의 의지를 보여주었습니다. 일본은 지속적인 제어장치 업그레이드를 통해 고급 부문을 지키고 있습니다. 오쿠마의 OSP-P500은 적응형 가공과 사이버 보안 대응 클라우드 연계를 결합하여 기존의 전문 지식이 데이터베이스 서비스로 진화하는 실례를 보여주고 있습니다.

북미는 리쇼어링 보조금, 항공우주산업 통합, 방산 수요를 배경으로 2위 자리를 유지. 오크리지 국립연구소와 MSC 산업 서플라이가 공동으로 탭 테스트 소프트웨어를 개발하여 허용 절삭 속도를 향상시키고, 민관 협력을 통해 생산성을 향상시켰습니다. 캐나다는 온타리오주의 자동차 산업 클러스터를 활용하고, 멕시코의 바히오 회랑은 전자기기 및 백색가전 가공을 흡수하여 미국 수요에 대응.

유럽은 독일, 이탈리아, 북유럽의 전문 업체들이 고정밀 셀을 전 세계에 수출하며 기술적 우위를 유지하고 있습니다. 그러나 중동은 산유국들이 다각화를 추진하면서 2031년까지 8.85%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 킹살만 에너지 파크에 위치한 에머슨의 13,000평방미터 규모의 공장과 담맘에 위치한 첨단 프레시젼 산업 서비스(Advanced Precision Industrial Services)의 5만 4,000평방미터 규모의 확장은 에너지, 항공우주 및 석유화학 분야의 중장비 가공을 지역에 제공할 것입니다. 제공합니다. 이러한 투자는 수입 의존도를 낮추고, 현지 부품 수리의 다운스트림 분야에서 기회를 창출할 수 있습니다.

CNC Machines Market size in 2026 is estimated at USD 79.14 billion, growing from 2025 value of USD 74.82 billion with 2031 projections showing USD 104.76 billion, growing at 5.78% CAGR over 2026-2031.

Rising demand for digitally enabled production, tighter tolerance requirements in electric-vehicle and aerospace programs, and fiscal incentives for factory modernization collectively underpin this expansion. Vendors increasingly bundle hardware, software, and predictive services, allowing customers to raise asset utilization and defer new-equipment purchases while still expanding productive capacity. Procurement strategies now prioritize interoperability with industrial 5G and edge-computing platforms that reduce scrap rates by up to 30% and shorten spare-parts lead times by 10%. Geopolitical supply-chain concerns are also encouraging OEMs to reshore critical machining work, strengthening demand for domestic installations in North America and the European Union.

Manufacturers are migrating from isolated machine tools to fully networked cells where IoT sensors stream real-time conditions to edge servers, cutting scrap by 30% and trimming spare-parts inventories by 10%. Fifth-generation wireless closes previous latency gaps, giving operators steady connectivity that prevents program interruptions. Digital twins now model thermal drift and spindle dynamics before a single chip is cut, trimming ramp-up times by 40%. AI-assisted toolpath agents lower programming workloads by 50% while improving surface finish repeatability. Collectively, these upgrades reposition CNC equipment as nodes within autonomous production loops rather than stand-alone capital assets.

Electric-vehicle battery housings, inverter plates, and motor stators impose tolerance bands once limited to aerospace structures, prompting wider 5-axis adoption in automotive shops. Aerospace recovery adds a second precision stream, with titanium and carbon-fiber components requiring stable tool engagement beyond conventional parameters. Hybrid additive-subtractive processes can shave 35% off cycle times for intricate aerospace brackets while preserving dimensional integrity. Regulatory traceability rules further compel digital machining logs that prove micron-level accuracy. This dual-sector pull cements high-precision CNC capability as a baseline requirement rather than a premium option.

Five-axis centers integrate high-precision rotary axes, linear motors, and thermal-compensation systems, lifting purchase tickets well above USD 500,000, a hurdle for small shops. Okuma estimates only 15% of lifetime spending happens at acquisition, with 85% tied to maintenance, energy, and unplanned outages. Digital twin licenses and AI modules pile extra costs onto enterprise resource plans. Studies show hybrid additive-subtractive cells demand thorough batch-size analyses before payback is viable, especially when powders carry premium prices. High ownership burden, therefore, limits penetration among low-volume manufacturers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

CNC lathes captured 26.95% of 2025 revenue, underscoring their indispensable role in shafts, bushings, and other rotational parts across multiple value chains. Their straightforward programming and rigid tooling allow quick changeovers, making them staples for Tier 1 automotive and hydraulic suppliers. Milling machines follow, serving prismatic geometries where multi-surface accuracy matters. Laser cutters, however, are climbing fastest at an 8.55% CAGR thanks to fiber-laser sources that pierce steel, aluminum, and composite stacks with minimal distortion.

Prima Power's Laser Next 2130, paired with Siemens' SINUMERIK ONE control, boosted dynamic response by 20% and productivity by 13% in automotive body-in-white lines, illustrating why lasers are displacing stamping on complex panels. Electro-discharge machining and grinding sustain niche dominance in die-makers and bearing producers. Hybrid additive-subtractive units enable near-net deposition of nickel superalloys, then finishing on the same table, saving aerospace primes multiple logistics steps. The CNC machines market thus balances mature turning demand with rapid laser innovation.

The CNC Machines Market Report is Segmented by Machine Type (CNC Lathes, CNC Milling Machines, and More), by Axis Type (3-Axis, 4-Axis, and More), by End-User Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific secured 46.10% of global revenue in 2025 as China, Japan, and India expanded domestic capacity to mitigate import risk and satisfy internal demand. China's First Automation raised RMB 100 million (USD 13.9 million) to develop native high-end controllers, signaling official intent to localize strategic machine-tool technology. Japan protects its premium segment through continual control upgrades; Okuma's OSP-P500 pairs adaptive machining with cyber-secure cloud links, demonstrating how legacy expertise evolves into data-driven services.

North America ranks second, combining reshoring subsidies, aerospace consolidation, and defense imperatives. Oak Ridge National Laboratory and MSC Industrial Supply co-developed tap-testing software that raises permissible material-removal rates, showing public-private collaboration on productivity. Canada leverages automotive clusters in Ontario, whereas Mexico's Bajio corridor absorbs electronics and white-goods machining to serve the United States' demand.

Europe retains technical leadership through German, Italian, and Nordic specialists who export high-tolerance cells worldwide. The Middle East, though, will post the strongest 8.85% CAGR to 2031 as oil-rich nations diversify. Emerson's 13,000 m2 plant at King Salman Energy Park and Advanced Precision Industrial Services' 54,000 m2 expansion in Dammam equip the region with heavy-duty machining for energy, aerospace, and petrochemical needs. These investments reduce import reliance and open downstream opportunities for localized component repair.