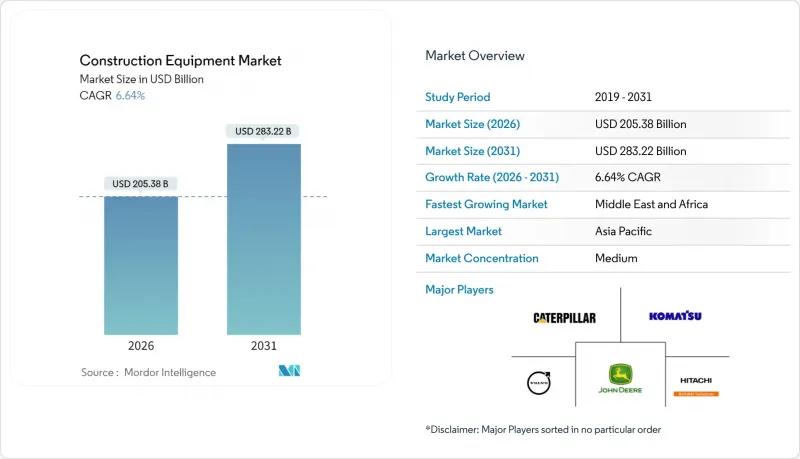

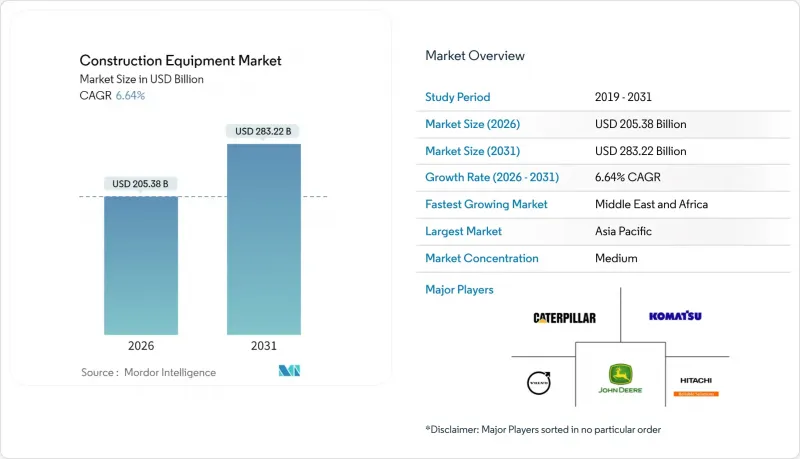

건설기계 시장은 2026년에 2,053억 8,000만 달러 규모이며, 2031년까지 2,832억 2,000만 달러까지 확대할 것으로 예측됩니다. 이 기간에 CAGR은 6.64%를 기록하며, 시장 규모와 이익 기반 꾸준한 확대를 보이고 있습니다.

도로, 철도, 전력망, 반도체 제조 공장 등에 대한 정부의 견고한 지출이 토목 기계, 자재관리 기계, 콘크리트 기계에 대한 수요를 지원하고 있습니다. 아시아의 대형 프로젝트 계획, 유럽과 북미의 전기화 추진, 업계 전반의 임대 차량으로의 전환이 결합되어 견고한 성장 전망을 지원하고 있습니다. 중국 업체들이 해외 시장에서 점유율을 확대하는 반면, 유럽과 미국의 주요 업체들은 서비스 중심의 제안과 자율기술로 중심을 옮기는 등 경쟁이 심화되고 있습니다. 건설기계 시장은 Stage V 및 EPA 3단계 규제로 인해 차량 갱신 주기가 가속화되면서 제품 및 디지털 서비스 출시 간격이 짧아지고 있습니다.

3조 7,000억 달러가 넘는 확정된 프로젝트가 배분 우선순위를 바꾸고, 대형 불도저, 45톤급 굴착기, 대용량 콘크리트 펌프가 다른 지역보다 먼저 아시아 창고에 집결하고 있습니다. 사우디는 2024년에만 550억 달러 규모의 프로젝트를 발주(전년 대비 57% 증가), UAE는 200% 증가한 340억 달러 규모에 달할 전망입니다. OEM 업체들은 고출력, 롱리치 붐 모델의 판매 구성을 최적화하고, 고가 계약과 애프터마켓 계약을 통해 매출 기반을 강화하고 있습니다.

반도체 공장, 전기자동차 공장, 전력망 업그레이드에 대한 연방 정부의 특혜로 인해 선벨트 지역 전체에서 250-500마력의 불도저와 유압식 굴착기에 대한 구조적 수요가 발생하고 있습니다. 미국 토목학회는 2035년까지 3조 7,000억 달러의 인프라 갭을 예측하고 있으며, OEM의 수주 잔고는 지속적인 전망이 확보되어 있습니다. 인력 부족에 직면한 건설업체들은 프로젝트 일정을 단축하고 시간당 운영 예산을 절감할 수 있는 대형 유닛을 선택하는 경향이 있습니다.

중요 유압 밸브 및 펌프의 납기가 42주를 초과하는 상황으로 인해 건설업체는 프로젝트 공정을 조정할 수밖에 없습니다. 시장 선도 기업은 공급을 확보하기 위해 수직계열화를 가속화하고 있으며, 캐터필러가 자체 부품 가공을 확대한 것도 이에 따른 것입니다. 공급 병목현상이 지속될 경우, 재고가 정상화될 때까지 건설기계 시장의 단기적인 모멘텀이 둔화되고, 갱신 주기가 지연될 것으로 우려됩니다.

2025년 건설기계 시장 점유율은 굴착기가 51.24%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 7.15%를 나타낼 것으로 예측됩니다. 유압 효율, 퀵 어태치먼트 툴, 텔레매틱스 통합으로 도로 건설, 유틸리티, 철거 분야에서 지속적인 수요를 창출하고 있습니다. 로더는 판매량 2위를 유지하고 있으며, 포장 작업에는 휠로더, 연약지반에는 트랙로더가 선호되고 있습니다. 크레인 수요는 고층 빌딩과 교량 건설 일정에 연동되며, 그레이더와 롤러는 mm 단위의 정밀도로 도로 표면을 유지합니다.

불도저는 경사면 안정성을 위해 높은 견인력이 요구되는 광산 벤치 작업에 활용되며, 덤프트럭은 500미터 이상의 운반을 담당합니다. 콘크리트 펌프, 트렌처 등 특수기계는 건설기계 시장 규모에서 중요한 비중을 차지하고 있습니다. 코마츠의 수소 동력 프로토타입은 향후 연료의 다양화를 시사하고 있지만, 보급을 위해서는 연료 보급 인프라의 확충이 필요합니다.

2025년 출하량에서 내연기관 차량이 90.12%를 차지했으나, 규제 강화에 따라 하이브리드 및 배터리 전기 모델은 CAGR 22.16%로 증가할 것으로 예측됩니다. 하이브리드 시스템은 소형 디젤 엔진과 배터리를 결합하여 연료 소비를 25-35% 절감합니다. 공회전 및 실내 작업 시에는 정숙한 무배기 운전을 실현합니다. 캐터필러의 323형 전기 굴착기는 전력망 연결형 재개발 현장에서 낮은 운영비용을 실현하여 2025년 말까지 다수의 수주를 확보했습니다.

세계에서 수소연료전지 굴착기는 일본, 독일, 한국 등지에서 주로 파일럿 프로그램을 통해 제한적으로 운영되고 있습니다. JCB는 연료전지 관련 비용을 피하고 2027년까지 수소 연소 엔진 상용화를 목표로 하고 있습니다. 무공해 건설기계 시장은 전력망 용량과 충전 인프라에 밀접하게 의존하고 있습니다. 이 때문에 신뢰할 수 있는 전원이 널리 보급되기 전까지는 디젤 엔진을 백업으로 하는 하이브리드 기계를 선호하는 구매자도 있습니다.

2025년 건설기계 시장에서는 아시아태평양이 45.80%의 점유율로 1위를 차지했습니다. 이는 중국의 일대일로(一帶一路) 구상과 인도의 국가 인프라 구축 계획에 힘입은 것입니다. 중국의 크롤러 굴착기 생산량은 2027년까지 15만 대를 넘어 2023년 생산량의 2배 이상에 달하고, 공급업체들의 규모의 경제를 강화할 것으로 예측됩니다. 이 업체는 고출력 디젤을 동남아시아 및 GCC 지역 현장에 공급하는 한편, 소형 전기 로더를 일본과 한국 도시에 수출하고 있습니다.

중동 및 아프리카은 2031년까지 연평균 복합 성장률(CAGR) 9.12%로 가장 높은 성장세를 보이고 있으며, 사우디아라비아의 '비전 2030'과 아랍에미리트(UAE)의 '두바이 도시 마스터플랜'에 따라 주택, 관광, 물류 분야에 수십억 달러가 투입되고 있습니다. 2024년 프로젝트 수주가 크게 증가하고 지역내 설비 공급이 부족해짐에 따라 OEM 업체들은 제벨알리 항구에 임시 수입 야드를 설치했습니다. 건설기계 시장에서 걸프 지역의 차별화 요소는 내열성 배터리 화학 성분과 밀폐형 캐빈용 필터 시스템입니다.

북미 시장은 IRA(인플레이션 억제법) 및 CHIPS 법안에 힘입은 산업 회귀와 인프라 개혁으로 인해 견고한 전망을 유지하고 있습니다. 2027년형부터 시행되는 EPA 3단계 기준은 도시 유틸리티용 소형 장비의 하이브리드 및 전기식 전환을 촉진하고 있습니다. 렌탈 대기업은 규모 확대를 위해 통합을 추진하고 있으며, 수십억 달러 규모의 인수로 인해 딜러 네트워크가 축소되고 액세스 요금이 상승하고 있습니다.

The construction equipment market stands at USD 205.38 billion in 2026 and is forecast to climb to USD 283.22 billion by 2031, registering a 6.64% CAGR during the period, underscoring steady gains in market size and profit pools.

Robust government spending on roads, rail, power transmission, and semiconductor fabs underpins demand across earthmoving, material-handling, and concrete machinery. Asia's mega-project pipeline, the electrification push in Europe and North America, and the industry-wide tilt toward rental fleets jointly reinforce a resilient growth outlook. Competitive intensity is sharpening as Chinese OEMs capture share abroad while Western leaders pivot to service-centric offerings and autonomous technologies. The construction equipment market is also shaped by quicker fleet renewal cycles driven by Stage V and EPA Phase 3 regulations, tightening the gap between product and digital service launches.

A committed project pipeline exceeding USD 3.7 trillion is transforming allocation priorities, pulling large dozers, 45-ton excavators, and high-capacity concrete pumps into Asian depots ahead of other regions. Saudi Arabia alone awarded USD 55 billion in projects in 2024, a 57% jump year-on-year, while the UAE lifted awards by 200% to USD 34 billion. OEMs are tailoring sales mixes toward higher horsepower and longer-reach booms, anchoring revenue in the construction equipment market through larger ticket sizes and aftermarket contracts.

Federal incentives for semiconductor fabs, EV plants, and grid upgrades have created a structural pull for 250-500 HP dozers and excavators across the Sun Belt. The American Society of Civil Engineers identifies a USD 3.7 trillion infrastructure gap by 2035, ensuring sustained visibility for OEM order books. Contractors, faced with labor constraints, are leaning toward larger units that compress project schedules and ease per-hour operating budgets.

Delivery windows stretch beyond 42 weeks for critical hydraulic valves and pumps, forcing contractors to adjust project phasing. Market leaders increasingly vertically integrate to secure supply, echoing Caterpillar's expanded in-house component machining. Persistent bottlenecks threaten to defer replacement cycles and dampen near-term construction equipment market momentum until inventories normalize.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Excavators commanded 51.24% construction equipment market share in 2025 and are projected to register a 7.15% CAGR to 2031. Hydraulic efficiency, quick-attach tooling, and telematics integration sustain demand across road-building, utilities, and demolition. Loaders remain second in volume, with wheel loaders favored for paved operations and track loaders for soft terrain. Crane demand follows high-rise and bridge timelines, while graders and rollers maintain road surfaces to millimeter tolerances.

Bulldozers thrive in mining benches where slope stability requires significant drawbar pull, and dump trucks handle hauls beyond 500 meters. Specialty machines, including concrete pumps and trenchers, together hold a significant share of construction equipment market size. Komatsu's hydrogen-powered prototype signals future fuel diversification, though widespread adoption awaits refueling infrastructure expansion .

Internal combustion units accounted for 90.12% of 2025 shipments, yet hybrids battery electric models will rise at 22.16% CAGR as regulations tighten. Hybrid systems pair smaller diesel engines with batteries, cutting fuel by 25-35% and enabling quiet, zero-tailpipe operation for idling and indoor work. Caterpillar's 323 electric excavator delivered lower operating costs on grid-connected redevelopment jobs and logged significant orders by end-2025 .

Globally, hydrogen fuel-cell rigs are operational in limited numbers, primarily in pilot programs across Japan, Germany, and South Korea. JCB is sidestepping the costs associated with fuel cells, aiming to commercialize its hydrogen combustion engine by 2027. The market for zero-emission construction equipment is closely tied to grid capacity and charging infrastructure. As a result, some buyers are leaning towards hybrids, which offer a diesel fallback until a reliable power source is widely available.

The Construction Equipment Market Report is Segmented by Equipment Type (Excavator, Loader, and More), Propulsion Type (Internal Combustion, Hybrid Battery Electric, and More), Equipment Size (Heavy (Above 11 Tons), Medium (6-11 Tons), and More), Power Output (Up To 250 HP, 250 - 500 HP, and More), Application, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia Pacific led with 45.80% of the construction equipment market in 2025, underpinned by China's Belt and Road Initiative and India's National Infrastructure Pipeline. Chinese crawler excavator volumes are set to exceed 150,000 units by 2027, more than doubling 2023 output and reinforcing supplier economies of scale. Manufacturers route high-power diesel inventory to Southeast Asia and GCC job sites while shipping compact electric loaders to Japanese and Korean cities.

The Middle East and Africa posts the fastest trajectory at 9.12% CAGR through 2031 as Saudi Arabia's Vision 2030 and the UAE's Dubai Urban Master Plan funnel billions into housing, tourism, and logistics. Project awards jumped significantly in 2024, tightening regional equipment supply and prompting OEMs to stage temporary import yards at Jebel Ali Port. Heat-tolerant battery chemistries and sealed cabin filtration systems are differentiators in the Gulf slice of the construction equipment market.

North America maintains a solid outlook propelled by industrial reshoring and infrastructure revamps backed by the IRA and CHIPS legislation. EPA Phase 3 standards, effective model year 2027, are nudging fleets toward hybrid and electric compact equipment for urban utility work. Rental giants consolidate to secure scale, evidenced by multi-billion-dollar acquisitions that compress dealer networks and elevate access fees.