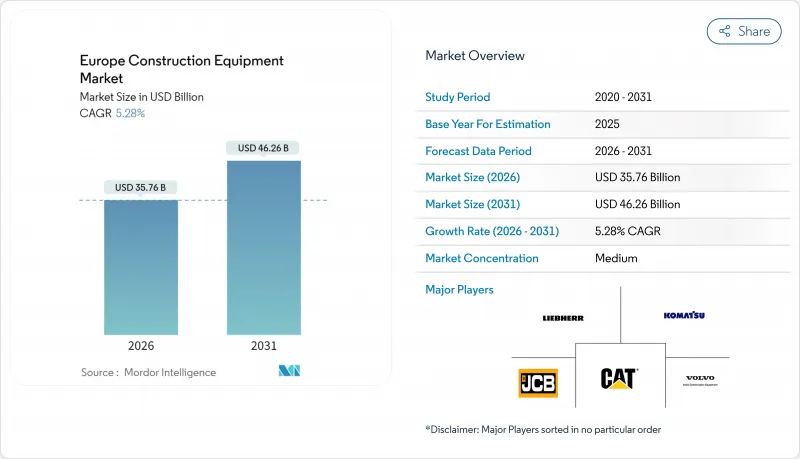

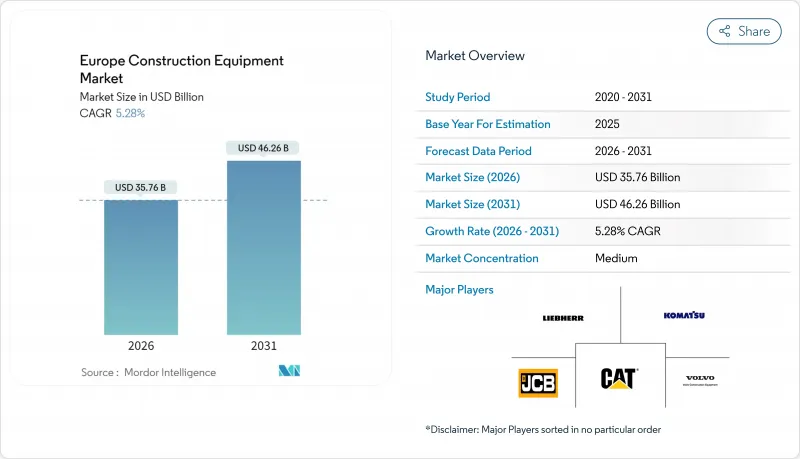

유럽의 건설기계 시장은 2025년 339억 7,000만 달러로 평가되었으며, 2026년 357억 6,000만 달러에서 2031년까지 462억 6,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 5.28%로 전망됩니다.

EU 그린딜과 관련된 유틸리티 지출 증가, 유럽 중앙 은행의 2025년 금리주기 및 현재 진행 중인 스테이지 V 배출 가스 규제의 도입이 수요를 형성하는 주요 요인이 되었습니다. 도시 프로젝트에서는 배터리 전기 모델에 대한 구매 추세가 강해지지만 중형 인프라 현장에서는 디젤 기계가 여전히 필수적입니다. 중국의 주문자 상표 부착 생산(OEM)에서는 직접 대출 및 현지 지원 센터를 활용하여 기존 서구 브랜드와의 경쟁 격차를 줄이고 있습니다. 동시에, 렌탈 플릿의 공급 과잉이 평균 판매 가격을 낮추고 서비스 중심의 수익 모델이나 구독형 텔레매틱스 번들로의 전환을 가속화하고 있습니다.

각 가맹국은 기후 변화에 강한 인프라에 역대 최대 규모의 자금을 투입하고 있으며, 조달 사이클은 18-24개월에서 최단 12개월로 단축되고 있습니다. 독일의 예산외기금은 2024년에 소폭 축소를 보인 뒤 2025년에는 건설 지출을 최소화하면서 증가할 전망입니다. 이 지출 확대는 재생에너지 설비 설치에 필요한 굴삭기, 모터 그레이더 및 소형 기계에 대한 수요를 뒷받침합니다. 건설업자는 그린딜 입찰 자격을 확보하기 위해 프리미엄 가격이 10% 이상 웃도는 경우에도 스테이지 V 적합 모델이나 전동 모델을 점점 선호하여 도입하고 있습니다. 따라서 공급업체는 가속화된 프로젝트 스케줄에 대응하므로 더 높은 재고 비축량을 유지해야 하는 압력에 직면하고 있습니다.

주택 투자는 2025년 1분기에 플러스로 돌아섰으며, 2022년 이후 첫 회복을 보였습니다. 주택 융자 승인 건수와 건설 대출 수요는 특히 고금리기에 주택 수요가 축적된 독일에서 강력하게 발생하고 있습니다. 도시 지역의 재개발 프로젝트가 신규 주택 건설의 대부분을 차지하기 때문에 소형 굴삭기, 미니 로더 및 텔레핸들러가 가장 혜택을 받고 있습니다. 또한 대출조건 완화로 소규모 계약업체가 설비 대출 시장으로 복귀하여 엔트리 레벨 전동기계 고객 기반이 확대되고 있습니다.

2021년부터 2022년까지의 적극적인 플릿 확대로 2024년의 렌탈 가동률은 불과 63.4%에 머물렀고, 렌탈 요금은 전년 대비 하락하였습니다. 렌탈 수요가 늘어나면서 각 회사는 플릿 투자를 최소화할 수밖에 없으며 6개월에서 9개월의 채널 재고가 과도하게 쌓여 있습니다. 제조업체는 렌탈 기간의 연장과 서비스 크레딧으로 대응하고 있지만, 이러한 조치는 이익률을 압박하고 혁신 예산의 축소를 초래합니다.

굴삭기는 2025년 유럽의 건설기계 시장에서 점유율 44.78%를 차지했으며, 2031년까지 연평균 복합 성장률(CAGR) 5.32%로 확대될 것으로 예상되어 유럽의 건설기계 시장 전체를 웃도는 성장률을 보일 전망입니다. 텔레스코픽 핸들러는 높은 곳에서 정밀한 배치를 필요로 하는 창고 자동화 프로젝트에 힘입어 성장률을 밀접하게 추종하고 있습니다. 크레인은 안정적인 판매량을 유지하면서 저가 수입품으로 인해 이익률의 압박을 받고 있으며 모터 그레이더는 운송 회랑에 대한 투자로부터 혜택을 받고 있습니다.

전동화는 각 하위 카테고리 내의 경쟁 구도를 재구성합니다. 립헬사의 L 507 E 휠 로더는 16시간의 가동 시간을 실현해 디젤기와 동등한 기능성을 나타내고 있습니다. 로더 및 백호 부문은 중국 제조업체와의 격렬한 가격 경쟁에 직면하는 반면, 특수 터널 굴삭기는 복잡한 안전 인증으로 높은 진입 장벽을 유지하고 있습니다. 건설업자는 굴삭기를 해체, 재활용, 정지 도구로 바꾸는 다기능 어태치먼트를 점점 선호하며 1대당 평균 판매 가격이 상승하여 구매자는 독자적인 유압 인터페이스에 구속되게 됩니다.

2025년에도 유럽의 건설기계 시장 규모의 80.66%를 내연기관이 차지하였지만, 배터리식 전기 유닛은 CAGR 5.39%로 가장 급속히 확대하고 있습니다. 충전 인프라가 정비되지 않은 지역에서는 하이브리드 구동 시스템이 제약을 보완하지만, 가동률이 높은 현장에서는 총 소유 비용의 우위성으로 인해 완전 전동기계가 유리합니다. 노르웨이와 네덜란드의 지방자치단체가 유틸리티에서 디젤기계 사용을 규제함으로써 공장의 리드타임을 웃도는 지역적인 전동기 수주 급증 현상이 발생하고 있습니다.

전기기계의 자본비용은 5분의 1 가량 높지만, 연간 1,500시간을 가동하는 건설업자는 연료비와 유지보수비 절감으로 4년 미만으로 추가비용을 회수할 수 있습니다. 수소 연료전지는 여전히 틈새 시장이지만, 립헬의 수소 굴삭기 파일럿 모델은 전력 공급이 불안정한 원격지 풍력 발전소에서의 사용에 관심을 불러 일으키고 있습니다. 제조업체는 현재 디젤과 전기라는 두 가지 제품 플랫폼을 관리해야 하며 이는 R&D 예산과 공급망 확대를 요구하고 있습니다. 리튬 및 희토류의 가격 변동으로 인해 배터리 조달이 복잡해지면서 부품 원가가 상승하고 있습니다. 이 제약으로 인해 유럽의 건설기계 시장의 예측 CAGR은 0.5포인트 하락했습니다.

The Europe Construction Equipment Market was valued at USD 33.97 billion in 2025 and estimated to grow from USD 35.76 billion in 2026 to reach USD 46.26 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031).

Rising public-works spending linked to the EU Green Deal, the European Central Bank's 2025 rate-cut cycle, and the ongoing rollout of Stage V emissions rules are the primary forces shaping demand. Equipment buyers are tilting toward battery-electric models for urban projects, while diesel machines remain essential on heavy infrastructure sites. Chinese original-equipment manufacturers (OEMs) are using direct financing and local support centers to narrow competitive gaps with incumbent Western brands. Simultaneously, rental-fleet oversupply is suppressing average selling prices, accelerating the pivot to service-centric revenue streams and subscription telematics bundles.

Member states are channeling unprecedented capital into climate-resilient infrastructure, compressing procurement cycles from 18-24 months to as few as 12 months. Germany's off-budget fund is already lifting real construction outlays by minimal in 2025 after a slight contraction in 2024. This spending wave boosts demand for excavators, motor graders, and compact machines needed for renewable-energy installations. Contractors increasingly favor Stage V-compliant or electric models, even when premiums exceed more than one-tenth, to secure eligibility for Green Deal tenders. Suppliers therefore face mounting pressure to maintain higher inventory buffers that match accelerated project timelines.

Housing investment turned positive slightly in Q1 2025, the first upturn since 2022. Mortgage approvals and construction loan demand have strengthened, especially in Germany, where pent-up housing needs accumulated during the high-rate period. Compact excavators, mini loaders, and telehandlers benefit the most because urban infill projects dominate new housing activity. Easier credit is also pulling small contractors back into the equipment-financing market, widening the customer base for entry-level electric machines.

Aggressive fleet expansion during 2021-2022 left rental utilization at only 63.4% in 2024, pushing rental rates down on year over year. Sluggish rental growth has forced companies to cut fleet spending by minimal, creating channel inventory bulges of six to nine months. Manufacturers respond with longer financing terms and service credits, but these steps erode margins and slow innovation budgets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Excavators captured 44.78% of the Europe construction equipment market share in 2025 and are projected to grow at a 5.32% CAGR to 2031, outpacing the overall Europe construction equipment market. Telescopic handlers follow closely in growth, fuelled by warehouse automation projects that demand precision placement at height. Cranes maintain steady volume but see margin pressure from lower-priced imports, while motor graders gain from transport-corridor spending.

Electrification reshapes competitive dynamics within each subcategory. Liebherr's L 507 E wheel loader delivers 16-hour run-time, showing functional parity with diesel units. Loader and backhoe segments face intense price competition from Chinese OEMs, whereas specialized tunneling equipment retains higher entry barriers thanks to complex safety certifications. Contractors increasingly prefer multi-functional attachments that turn excavators into demolition, recycling, or grading tools, boosting average selling price per unit and locking buyers into proprietary hydraulic interfaces.

Internal combustion engines still hold 80.66% of the Europe construction equipment market size in 2025, but battery-electric units are climbing fastest at a 5.39% CAGR. Hybrid drive-trains bridge constraints where charging infrastructure is lacking, yet total cost of ownership advantages favor full electrics on high-utilization sites. Provincial mandates in Norway and the Netherlands restrict diesel equipment on public projects, triggering regional spikes in electric orders that outstrip factory lead times.

Capital costs for electric machines are one-fifth higher, but contractors running 1,500 hours annually recoup premiums in under four years through fuel and maintenance savings. Hydrogen fuel cells remain niche, but Liebherr's pilot hydrogen excavator has sparked interest for use in remote wind farms where grid supply is thin. Manufacturers must now manage dual product platforms-diesel and electric-stretching R&D budgets and supply chains. Battery sourcing is complicated by lithium and rare-earth price swings that raise bills of material, a restraint subtracting 0.5 percentage points from Europe construction equipment market CAGR projections.

The Europe Construction Equipment Market Report is Segmented by Machinery Type (Cranes, Telescopic Handler, and More), Power Source (Internal-Combustion, Hybrid, and More), End-User Industry (Infrastructure & Construction, Mining & Quarrying, and More), Application (Earthmoving, Lifting & Material Handling, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).