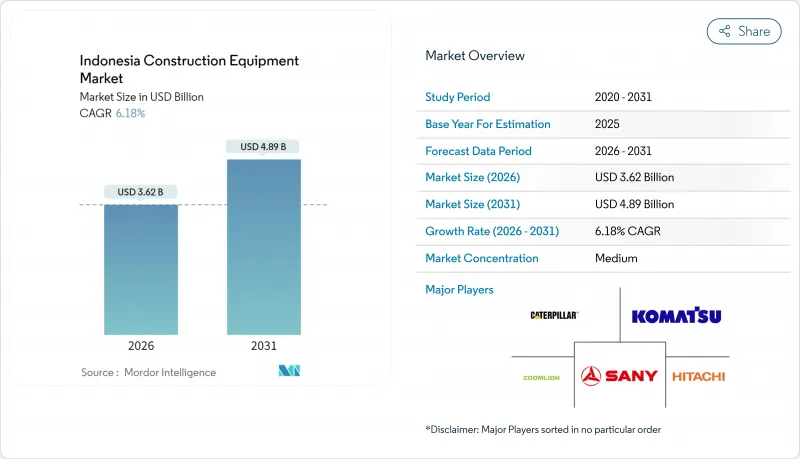

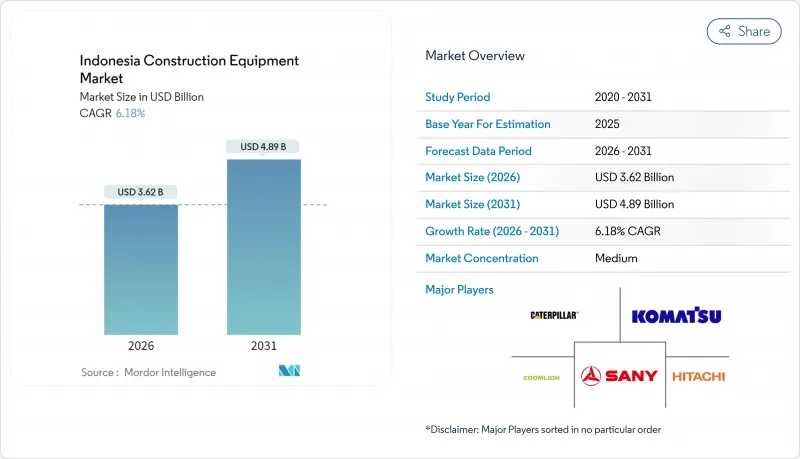

인도네시아의 건설 장비 시장은 2025년 34억 1,000만 달러로 평가되었고, 2026년 36억 2,000만 달러에서 2031년까지 48억 9,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 6.18%를 나타낼 것으로 예상됩니다.

국가전략사업(PSN) 파이프라인의 지속적 추진, 350억 달러 규모의 신수도(IKN) 프로그램, 그리고 탄력적인 광업 투자가 토목 장비, 자재 취급 장비, 특수 장비 부문 전반에 걸쳐 수요를 견인하고 있습니다. 현지 조립, 유연한 금융 지원, 텔레매틱스 서비스를 결합한 공급업체들이 자카르타 중심의 차량 군에서 활용률을 극대화할 수 있는 최적의 위치에 있습니다.

인도네시아의 41개 최종 단계 PSN 사업은 유료 도로, 댐, 항만, 산업 단지에 걸쳐 중단 없는 장비 배치가 필요합니다. 인프라에 지출된 1루피아당 1.9루피아의 경제적 가치를 창출하여 계약업체와 임대 업체의 조달 예산을 강화하고 있습니다. 이 배율은 경제 특구 및 전력 프로젝트에서 가장 강력하게 나타나, 역사적으로 자바에 집중되던 수요가 전국적으로 고점을 형성하게 합니다. 북수마트라와 남술라웨시가 가장 가파른 생산량 증가를 기록하며 각 주를 지역별 임대 수요 중심지로 변모시켰습니다. 장기 프로젝트 파이프라인은 공급업체가 5-7년 유지보수 계약을 구성할 수 있게 하여 장비 수명 주기 전반에 걸쳐 부품 및 서비스 수익을 확보합니다.

2024년 완공된 치망기스-치비퉁 고속도로는 굴삭기와 덤프트럭의 대규모 투입으로 토공 작업 강도가 매우 높은 사례다. 카랑조앙-카리앙가우 3A 구간의 현장 디지털 모니터링은 장비 가동률 향상과 동시에 유휴 시간을 크게 줄여 텔레매틱스 통합의 중요성을 부각시켰습니다. 정밀 유도 시스템을 도입한 건설사들은 연비 효율과 작업 속도에서 눈에 띄는 개선 효과를 보고 있습니다. 이러한 관행은 현재 지방 당국에 의해 북수마트라 파라팟 같은 인프라 회랑으로 확대되고 있어, 기술 주도형 업그레이드가 자바 섬을 넘어 확장되고 있음을 시사합니다. 노후화된 Tier 2 장비에 대한 배출 규제가 강화되면서 건설사들은 점점 더 청정하고 사용 시간이 적은 Tier 3 및 하이브리드 장비로 전환하고 있습니다.

자본재 수입은 인도네시아 무역 바스켓에서 상당한 비중을 차지하여, 건설사들이 외환 변동에 노출되게 함으로써 구매 예산을 몇 주 만에 0.25% 포인트씩 잠식하고 있습니다. 신용장은 비용 완충 역할을 하지만, 현지 조달 의무는 세계의 브랜드의 사양 선택을 복잡하게 만듭니다. 무역부 장관령 제8/2024호는 항만 통관을 간소화했으나 통화 리스크는 지속되어 장비 금융사들이 중소기업 대상 담보비율(LTV)을 강화하고 있습니다. 딜러들은 달러 연동 부품 계약과 루피아 표시 장비 대출을 묶어 제공하는 경우가 늘어나 불일치는 줄었지만 서류 작업 부담은 증가했습니다. 바탐과 치카랑에서의 현지 조립은 노출을 완화하지만, Tier 4F 엔진 수입은 여전히 달러로 가격 책정됩니다.

2025년 인도네시아의 건설 장비 시장에서 토목장비는 10억 달러를 넘는 매출을 창출해 PSN(공공서비스 네트워크) 및 광업기반 정비의 급증에 따라 48.12%의 점유율을 차지했습니다. 모터 그레이더, 크롤러 굴삭기, 굴절식 덤프 트럭은 유료 도로 및 댐 패키지의 핵심을 이루며, 배칭 플랜트와 분쇄 장치는 대규모 EPC 범위를 완성합니다. 첨단 텔레매틱스 기술은 이제 공회전 연료 소모와 차대 마모를 추적하여, 배출 규제가 시행되기 전에 건설사들이 구형 Tier 2 모델을 업그레이드하도록 유도하고 있습니다.

자자재 취급 장비는 상당한 점유율을 차지했으며, 창고 자동화와 항만 현대화에 힘입어 7.32%의 연평균 성장률(CAGR)로 확장 중입니다. 리튬이온 배터리 팩을 장착한 지게차는 배터리 교체 없이 3교대 운영이 가능해 가동 중단 시간을 25% 단축합니다. 탄중프리옥 항에서는 원격 조종 부두 크레인이 선석 생산성을 향상시켜 탄중페락과 키징 항에서 후속 주문이 이어지고 있습니다.

유압 플랫폼은 비용 대비 성능 균형과 인도네시아 운영자들의 친숙도로 뒷받침되어 2025년 매출의 84.55%를 차지했습니다. 공급업체들은 작업 습관을 바꾸지 않고도 연료 소비를 8% 절감하기 위해 스풀 밸브 조정 및 에너지 회수 회로를 개선하고 있습니다. 원격 시추 프로젝트는 전기적 복잡성보다 유압적 견고성을 중시하여 반경 100km 이상 광산에서 교체 수요를 유지합니다.

전기식 및 하이브리드식은 현재 임대 대수가 4,200대에 불과하지만, 탄소 크레딧 인센티브와 현지 조달 전기차에 대한 10% 부가가치세 감면으로 6.45%의 연평균 성장률(CAGR)을 기록합니다. 20톤 굴삭기 대상 시범 개조 결과, 1㎥당 운영 비용이 30베이시스 포인트 감소했습니다. 하이브리드 채택 업체는 탄소 포집·활용·저장(CCS/CCUS) 규정 준수 공공 입찰에서 우대 점수를 확보하는 경우가 많습니다. 금융 패키지에는 그린 라벨 자산담보부증권이 포함되어 기존 대출 대비 쿠폰 스프레드를 축소하며, 2027년 이후 주류 입찰 시장으로의 확산을 촉진하고 있습니다.

The Indonesia Construction Equipment Market was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 4.89 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

Continued implementation of the Proyek Strategis Nasional (PSN) pipeline, the USD 35 billion New Capital City (IKN) program, and resilient mining investment jointly anchors demand across earth-moving, material-handling, and specialized machinery categories. Suppliers that blend local assembly, flexible financing, and telematics services are best positioned to capitalize on utilization rates in Jakarta-centric fleets.

Indonesia's 41 final-stage PSN schemes require uninterrupted equipment deployment across toll roads, dams, ports, and industrial parks. Every rupiah spent on infrastructure has generated 1.9 rupiah in economic value, reinforcing procurement budgets for contractors and rental houses. The multiplier appears strongest in economic zones and power projects, prompting nationwide demand peaks rather than the historical Java concentration. North Sumatra and South Sulawesi have posted the sharpest output lifts, turning each province into a regional rental hotspot. Longer project pipelines permit suppliers to structure five- to seven-year maintenance contracts, locking in parts and service revenue throughout machine life cycles.

Completed in 2024, the Cimanggis-Cibitung Toll Road exemplifies high earth-moving intensity, with significant deployment of excavators and dump trucks during peak construction. On-site digital monitoring at the Karangjoang-Kariangau Section 3A helped reduce equipment idle time significantly while improving utilization rates-highlighting the growing importance of telematics integration. Contractors adopting precision guidance systems are seeing notable gains in fuel efficiency and operational speed. These practices are now being extended by provincial authorities to infrastructure corridors like Parapat in North Sumatra, indicating that technology-driven upgrades are expanding beyond Java. With stricter emission norms tightening around aging Tier 2 equipment, contractors are increasingly turning to cleaner, low-hour Tier 3 and hybrid machines.

Capital-goods imports form a significant share of Indonesia's trade basket, exposing contractors to foreign-exchange swings that erode purchasing budgets by quarter-points in weeks. Letters of credit add cost buffers, while local content mandates complicate specification choices for global brands. Trade Ministerial Regulation No. 8/2024 streamlines port clearance, yet currency risk persists, prompting equipment financiers to tighten loan-to-value ratios for smaller firms. Dealers increasingly bundle dollar-indexed parts contracts with rupiah-denominated machine loans, reducing mismatch but raising documentation overheads. Local assembly in Batam and Cikarang mitigates exposure, though Tier 4F engine imports remain priced in USD.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Earth-moving machinery generated more than a billion USD within the Indonesian construction equipment market in 2025, translating into a 48.12% share amid a surge of PSN and mining groundwork. Motor graders, crawler excavators, and articulated haulers form the backbone of toll-road and dam packages, while batching plants and crushing units round out larger EPC scopes. Advanced telematics now track idle fuel-burn and undercarriage wear, nudging contractors to upgrade older Tier 2 models ahead of emission mandates.

Material-handling equipment contributed significant share and is expanding at a 7.32% CAGR, propelled by warehouse automation and port modernization. Forklifts with lithium-ion packs enable triple-shift operations without battery swaps, cutting downtime by 25%. At Tanjung Priok, remote-operated quay cranes improve berth productivity, driving follow-on orders from Tanjung Perak and Kijing.

Hydraulic platforms captured 84.55% revenue in 2025, underpinned by cost-performance equilibrium and familiarity among Indonesian operators. Suppliers refine spool-valve tuning and energy-recovery circuits to cut fuel consumption by 8% without shifting working habits. Remote drilling projects value hydraulic robustness over electrical complexity, sustaining replacement demand in 100 km-plus radius mines.

Electric and hybrid variants, although only 4,200 units on rent today, post a 6.45% CAGR backed by carbon-credit incentives and 10% VAT discounts on locally contented EVs. Pilot retrofits on 20-tonne excavators show operating-cost drops of 30 basis points per cubic meter moved. Contractors adopting hybrids often secure preferential scoring in public tenders aligned with CCS/CCUS compliance. Financing bundles include green-label asset-backed securities, trimming coupon spreads versus conventional loans, and nudging adoption into mainstream bids for 2027 onward.

The Indonesia Construction Equipment Market Report is Segmented by Equipment Type (Earth-Moving Equipment, Road Construction Equipment, and More), Drive Type (Hydraulic and Electric/Hybrid), Power Output (Less Than 100 KW and More), End-User (Infrastructure & Real-Estate Contractors and More), Application (Residential Construction and More), and Region. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).