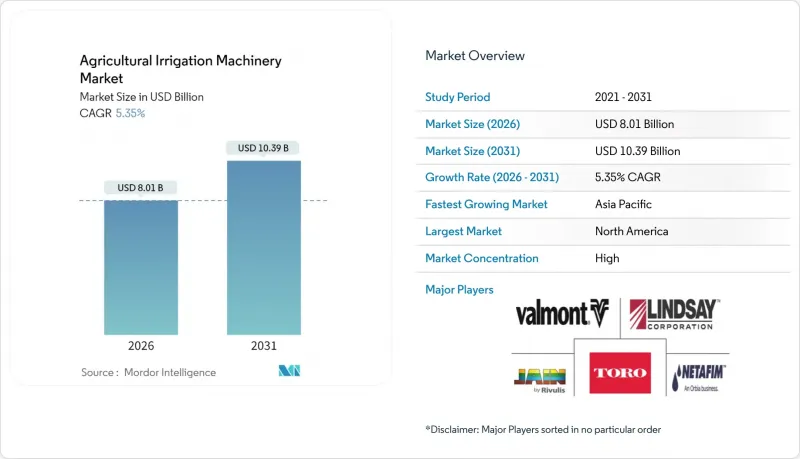

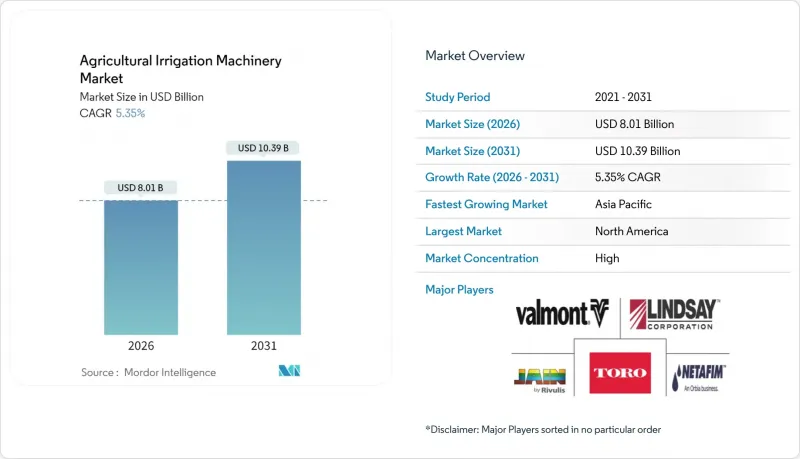

농업용 관개 기계 시장은 2025년에 76억 달러로 평가되며, 2026년 80억 1,000만 달러에서 2031년까지 103억 9,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 5.35%로 전망됩니다.

물 부족의 심화, 정밀농업의 도입, 그리고 보조금 제도가 강화되면서 농업용 관개기계 시장을 촉진하고 있으며, 기술을 활용한 서비스 모델이 새로운 매출 기회를 제공합니다. 경쟁의 치열함은 센서 및 자동화 분야의 제품 혁신과 일회성 장비 판매에서 장기적인 데이터 서비스로의 전환을 통해 형성되고 있습니다. ESG 관련 펀드를 통한 자본 확보는 마이크로 관개 도입에 박차를 가하고 있지만, 개발도상국의 토지 소유권 세분화가 전체 성장을 저해하고 있습니다. 애프터서비스 지원의 현지화 및 플라스틱 폐기물 문제에 대응하는 제조업체는 농업용 관개기계 시장 수요 증가를 포착할 수 있는 입지를 구축했습니다.

연방정부의 보전기금 확충으로 중규모 생산자들의 초기 비용 부담을 경감시켜주고 있습니다. 미국 농무부(USDA)의 환경 품질 인센티브 프로그램(EQIP)은 2024 회계연도에 시스템 비용의 최대 75%를 보조하여 효율성 향상에 19억 달러를 배정했습니다. 인플레이션 억제법에 따른 다년 보증은 제조업체의 생산 능력 확대를 촉진하고, 성과 기반 지표는 벤더의 제품 제공을 정책 목표에 맞게 조정합니다. 이러한 자금 조달의 확실성을 통해 장비 제조업체는 생산 능력과 공급망 인프라에 대한 확신을 가지고 투자할 수 있습니다. 이 프로그램이 측정 가능한 물 절약 성과를 중시하는 점은 제조업체의 정밀농업 기술과 일치하여 기술 통합형 솔루션의 경쟁 우위를 창출하고 있습니다.

주요 농업 지역의 물 스트레스 지표는 홍수 관개에서 정밀 공급 시스템으로의 전환을 가속화하고 있습니다. 유엔의 최신 물 개발 보고서에 따르면 20억 명의 인구가 물 부족 국가에 거주하고 있으며, 2050년까지 농업용수 수요가 35% 증가할 것으로 예측했습니다. 이러한 경제적 요구는 물 비용을 넘어 규제 준수에 대한 필요성으로까지 확장됩니다. 관할권에서 물 사용량 보고 요건이 점점 더 엄격해지고 있기 때문입니다. 정밀 관개 시스템이 상세한 소비 분석을 제공할 수 있는 능력은 단순한 효율성 향상을 위한 옵션이 아닌 필수적인 컴플라이언스 툴로 자리매김하고 있습니다.

센터 피봇 관개 시스템의 자본 집약성은 경제성과 자금 조달 수단의 개선에도 불구하고 여전히 도입의 큰 장벽으로 작용하고 있습니다. 피벗 시스템의 전체 설치 비용은 지형과 기술 사양에 따라 1에이커당 1,200-2,000달러로 다양하며, 중규모 농업 경영체에게는 많은 자본이 투입되어야 합니다. 물 비용이 중간 정도인 지역에서는 투자 회수 기간이 7-10년에 달하며, 가격 변동에 직면한 상품 생산자에게는 현금 흐름 관리의 어려움이 있습니다. 설비 융자 조건은 보통 20-30%의 계약금이 필요하며, 여러 개의 밭을 동시에 현대화하려는 사업자에게는 유동성 제약이 발생합니다. 제조업체들은 모듈식 설치 방식이나 리스 구매 프로그램을 통해 대응하고 있지만, 초기 자본 요구 사항으로 인해 여전히 도입에 제약이 있습니다.

점적 관개 시스템은 우수한 물 이용 효율과 시비 관개 정확도로 인해 2025년 농업용 관개 기계 시장 점유율 46.08%를 유지했습니다. 이러한 우위는 기후 스트레스가 증가함에 따라 견고한 부문 전망을 지원하고 있습니다. 스프링클러 장비는 가장 빠르게 성장하는 하위 부문으로, 광활한 곡물 재배 지역의 기계화 촉진에 힘입어 2031년까지 연평균 8.05%의 성장률을 보일 것으로 예측됩니다. 피벗 솔루션은 의사결정 주기를 단축하는 센서 통합을 통해 더 많은 성장의 여지를 열어줍니다. 밸리 아이리게이션의 AgSense 365는 통합 제어 대시보드로의 전환을 구현하여 평생 서비스 가치를 높이고 있습니다.

주요 농업 지역의 물 비용 상승과 노동력 확보의 어려움으로 인해 경제성이 개선되면서 이 부문의 성장이 가속화되고 있습니다. 물 부족이 심화되고 규제 프레임워크가 효율성 중심의 기술로 전환됨에 따라 지표관개와 홍수식 관개 등 다른 관개 방식은 채택이 감소하는 추세입니다. 세분화 추세는 데이터베이스 농업 관리 방식을 지원하는 정밀 공급 시스템으로의 구조적 전환을 시사하고 있습니다.

북미는 2025년 매출의 32.12%를 차지할 것으로 예상되며, 이는 풍부한 비용 분담 프로그램과 성숙한 유통망을 기반으로 하고 있습니다. 2031년까지 예산의 확실성은 시장 포화로 인해 수량 성장이 억제되는 상황에서도 업데이트 및 업그레이드 주기가 유지될 수 있도록 합니다. 캐나다의 기후 변화에 강한 농업 우선 정책과 멕시코의 수출 지향적 원예는 지역 농업 관개 기계 시장에 추가적인 추진력을 더하고 있습니다.

아시아태평양은 중국의 물 스트레스 대책 의무화와 인도의 '프라단 만트리 크리시 신차이 요자나(Pradhan Mantri Krishi Singh Chai Yojana)'에 따른 급속한 마이크로 관개 도입에 힘입어 8.06%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역으로 자리매김하고 있습니다. 일본에서는 고령화되는 농업 종사자층이 자동화 투자를 가속화하고 있으며, 동남아시아의 온실 클러스터에서는 센서가 풍부한 점적관개 시스템이 요구되고 있습니다. 이러한 요인들이 복합적으로 작용하여 2031년까지 아시아태평양의 농업용 관개 기계 시장 규모가 크게 성장할 것으로 예측됩니다.

유럽에서는 정밀관개를 녹색금융 대상의 지속가능한 활동으로 자리매김하는 공동농업정책(CAP)의 환경적 기둥 아래 정밀관개가 꾸준히 확대될 것으로 예측됩니다. 지중해 지역의 가뭄으로 인해 지하 관개시설의 도입이 가속화되고 있는 반면, 네덜란드와 독일에서는 폐쇄형 온실 관개가 강조되고 있습니다. 중동 및 아프리카에서는 국가 지원 대규모 농장과 기후 변화 대응형 농업 회랑이 수요를 견인할 것입니다. 남미의 주요 콩 생산지에서는 강우량 변동성을 완화하기 위해 피벗식 관개시설에 대한 투자가 진행되어, 농업용 관개기계 시장에서 지역적으로 분산된 매출 기반을 강화하고 있습니다.

The agricultural irrigation machinery market was valued at USD 7.60 billion in 2025 and estimated to grow from USD 8.01 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031).

Rising water scarcity, the adoption of precision agriculture, and robust subsidy pipelines are combining to propel the agricultural irrigation machinery market, while technology-enabled service models offer fresh revenue opportunities. Competitive intensity is shaped by product innovations in sensors and automation, as well as the shift from one-off equipment sales to long-term data services. Capital availability through ESG-linked funding accelerates the deployment of micro-irrigation, yet fragmented landholdings in developing regions temper overall growth. Manufacturers that localize after-sales support and address plastic-waste concerns position themselves to capture incremental demand in the agricultural irrigation machinery market.

Expanded federal conservation funding makes upfront costs more accessible for medium-scale growers. The United States Department of Agriculture (USDA) Environmental Quality Incentives Program covered up to 75% of system outlays in fiscal 2024, allocating USD 1.9 billion to efficiency upgrades. Multi-year guarantees from the Inflation Reduction Act encourage manufacturers to boost production capacity, while outcome-based metrics align vendor offerings with policy targets. This funding certainty enables equipment manufacturers to invest in production capacity and supply chain infrastructure with confidence. The program's emphasis on measurable water savings outcomes aligns with manufacturers' precision agriculture capabilities, creating competitive advantages for technology-integrated solutions.

Water stress indicators across major agricultural regions are accelerating the transition from flood irrigation to precision delivery systems. The United Nations' latest water development report identifies 2 billion people living in water-stressed countries, with agricultural water demand projected to increase 35% by 2050. The economic imperative extends beyond water costs to include regulatory compliance, as jurisdictions implement increasingly stringent water-use reporting requirements. Precision irrigation systems' ability to provide detailed consumption analytics positions them as essential compliance tools rather than optional efficiency upgrades.

The capital intensity of center-pivot irrigation systems remains a significant barrier to adoption, despite improving economics and financing options. Complete pivot installations range from USD 1,200 to USD 2,000 per acre, depending on terrain and technology specifications, representing substantial capital commitments for mid-sized operations. The payback period extends to 7-10 years in regions with moderate water costs, posing a challenge to cash flow management for commodity producers facing price volatility. Equipment financing terms typically require down payments of 20-30%, creating liquidity constraints for operators seeking to modernize multiple fields simultaneously. Manufacturers are responding with modular installation approaches and lease-to-own programs, but adoption remains constrained by initial capital requirements.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Drip systems retained 46.08% of the agricultural irrigation machinery market share in 2025 on superior water-use efficiency and fertigation precision. This dominance underpins a robust segment outlook as climate stresses intensify. Sprinkler equipment is the fastest-growing sub-segment, projected to post an 8.05% CAGR through 2031 as labor shortages spur mechanization across broad-acre grains. Pivot solutions unlock additional upside through sensor integration that shortens decision cycles. Valley Irrigation's AgSense 365 exemplifies the shift to unified control dashboards, lifting lifetime service value.

The segment's growth acceleration reflects improved economics as water costs rise and labor availability declines across major agricultural regions. Other irrigation types, including surface and flood systems, face declining adoption as water scarcity intensifies and regulatory frameworks increasingly favor efficiency-oriented technologies. The segmentation dynamics indicate a structural shift toward precision delivery systems capable of supporting data-driven agricultural management practices.

The Agricultural Irrigation Machinery Market Report is Segmented by Irrigation Type (Sprinkler Irrigation, Drip Irrigation, Pivot Irrigation, and Other Irrigation Types), by Application Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Other Applications), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 32.12% of 2025 revenue, anchored by generous cost-share programs and mature distribution networks. Budget certainty through 2031 sustains replacement and upgrade cycles, even as market saturation moderates volume growth. Canada's climate-resilient farming priorities and Mexico's export-oriented horticulture add incremental momentum to the regional agricultural irrigation machinery market.

Asia-Pacific is positioned as the fastest-growing region at an 8.06% CAGR, boosted by water-stress mandates in China and rapid micro-irrigation rollouts under India's Pradhan Mantri Krishi Sinchayee Yojana. Japan's aging farmer demographic accelerates automation spending, while Southeast Asian greenhouse clusters seek sensor-rich drip systems. This confluence drives outsized gains in the agricultural irrigation machinery market size within Asia-Pacific through 2031.

Europe delivers steady expansion under the Common Agricultural Policy's environmental pillar, which labels precision irrigation as a sustainable activity eligible for green finance. Mediterranean drought episodes hasten subsurface installations, whereas the Netherlands and Germany emphasize closed-loop greenhouse watering. In the Middle East and Africa, state-backed megafarms and climate-smart corridors dominate demand. South America's soybean heartland invests in pivots to smooth rainfall variability, reinforcing a diversified geographic revenue stream across the agricultural irrigation machinery market.