부분 가수분해 구아검 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Partially Hydrolyzed Guar Gum Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1755257

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 263 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

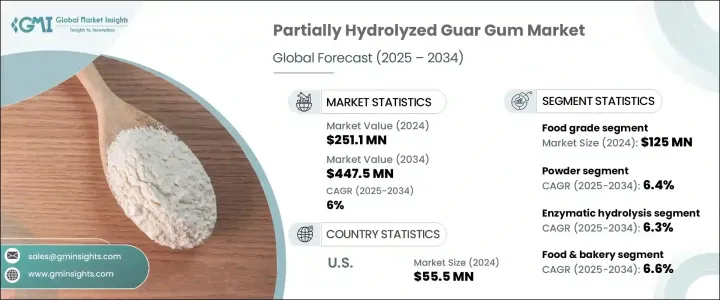

세계의 부분 가수분해 구아검 시장은 2024년에 2억 5,110만 달러로 평가되었고 소화기계 건강 제품, 클린 라벨 영양, 프리바이오틱스 강화 식품에 대한 세계 수요의 급증에 견인되어 2034년까지는 4억 4,750만 달러에 달할것으로 예측되며, CAGR6%로 성장할 전망입니다.

PHGG는 효소적 가수분해를 거쳐 저점도, 수용성 식이섬유로, 다양한 응용 분야에 적합합니다. pH 수준과 온도 변화에 걸쳐 안정성을 유지하며, 기능성 식품, 음료, 식이 보조제 등 다양한 식품 시스템과 호환됩니다. 식물성, 알레르기 유발 성분 없는 원료로의 전환 추세는 PHGG를 건강 중심 소비자 제품 개발의 선호 성분으로 자리매김시켰습니다.

소화기 건강 개선을 원하는 소비자들의 수요가 영양 기능성 제품에서 PHGG의 수요를 촉진하고 있습니다. PHGG의 프리바이오틱스 효과는 장내 미생물 균형을 지원하고 소화기 질환 증상을 완화합니다. 이 성분은 제과 제품, 식물성 대체품, 강화 스낵, 치료용 제형 등에 널리 사용되고 있습니다. 이는 제품에 쉽게 첨가할 수 있고 기능적 다양성을 갖추었기 때문입니다. PHGG는 클린 라벨 매력, 우수한 용해성, 부드러운 맛을 제공하여 건강을 중시하는 소비자들이 텍스처나 맛을 희생하지 않고 일일 식이섬유 섭취를 늘리려는 수요에 부응합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

2억 5,110만 달러

예측 금액

4억 4,750만 달러

CAGR

6%

식품 등급 부문은 2024년에 1억 2,500만 달러의 매출을 올렸습니다. 이 부문은 PHGG의 용해성과 건강 증진 효과로 인해 일상 식품에 널리 사용되어 혜택을 보고 있습니다. PHGG는 맛이나 식감을 저하시키지 않고 기능성 섬유를 공급할 수 있는 특성으로 섬유질이 풍부한 음료, 시리얼, 식사 바에 통합되는 것을 촉진했습니다. 포만감과 소화 편안함을 촉진하는 역할로 클린 라벨, 웰빙 지향적인 제품을 찾는 소비자에게 이상적입니다.

제약 부문은 2024년에 7,090만 달러를 창출했으며, 2034년에는 1억 1,640만 달러에 달할 것으로 예상됩니다. PHGG는 IBS(과민성 대장 증후군)와 변비와 같은 소화기 질환 관리 분야에서 임상 영양학에서 널리 인정받고 있습니다. 낮은 점도와 연령대에 걸친 내약성은 장기적인 식이 지원에 적합합니다. 임상 데이터가 그 효능을 점점 더 입증함에 따라 PHGG는 전 세계 노인층과 건강 의식 높은 인구층을 대상으로 한 대장 건강 보조제 및 치료용 식이섬유 기반 개입에 널리 적용되고 있습니다.

미국의 부분 가수분해 구아검 시장은 2024년에 5,550만 달러를 달성하며 식품 및 제약 부문의 상당한 관심을 받았습니다. 사용 사례는 치료용 식이요법, 의료 영양, 심지어 애완동물 및 개인 위생 용품 부문으로 빠르게 확대되고 있으며, 특히 고령층에서 수요가 증가하고 있습니다. 이 성분은 소화기 건강을 지원하고, 혈당 반응을 관리하며, 체중 조절을 돕는 기능으로 건강에 초점을 맞춘 제품 개발에 필수적인 기능성 성분으로 자리매김하고 있습니다. 제형 개발자들은 보충제, 임상 영양 제제 및 노인 식단 요구 사항과의 호환성을 위해 PHGG를 연구하고 있습니다.

부분 가수분해 구아검 시장의 주요 시장 기업으로는 BASF SE, Ingredion Incorporated(및 그 자회사 Tic Gums, Inc), CP Kelco US, Ashland Global Holdings Inc., Cargill, Incorporated 등이 있습니다. 이 기업들은 시장 혁신과 확장에 적극적으로 기여하고 있습니다. 부분적으로 가수분해된 구아검 분야를 선도하는 기업들은 제약, 기능성 식품, 클린 라벨 응용 분야에 맞춤형 PHGG 변종을 개발하기 위해 연구 개발에 대규모 투자를 진행 중입니다. 많은 업체들이 특히 북미와 아시아에서 증가하는 전 세계 수요를 충족하기 위해 생산 능력을 확대하고 있습니다. 식품 및 기능성 식품 제조업체와의 전략적 협력은 기업들이 유통망을 확대하는 데 도움이 되고 있습니다. 규제 당국의 승인 및 임상 검증도 시장 진출과 신뢰성 확보에 중요한 요소로, 기업들은 과학적 연구 및 안전 인증에 우선순위를 두고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

시장 소개

업계 밸류체인 분석

제품 개요

Phgg: 정의와 구성

제조 공정과 효소 가수분해

물리화학적 특성

영양 성분과 건강 효과

프리바이오틱스의 특성과 장의 건강에 대한 영향

천연 구아검과의 비교

다른 식이섬유와의 비교

시장 역학

시장 성장 촉진요인

소화 건강 및 프리바이오틱스에 대한 수요 증가

기능성 식품과 영양 보조 식품의 성장

클린 라벨 및 식물성 원료 선호도

시장 성장 억제요인

높은 생산 및 가공 비용

신흥 시장에서 소비자의 낮은 인지도

지역간 규제의 복잡성

시장 기회

장 건강 기능성 원료에 대한 수요 증가

영양 보조 식품과 식품 분야에서의 응용 확대

저 FODMAP 식이 섬유에 대한 관심 증가

업계에 미치는 영향요인

성장 가능성 분석

업계의 잠재적 리스크 및 과제

규제 프레임워크과 기준

식품첨가물 규제

식이섬유의 정의

건강 강조 표시 규제

품질과 안전 기준

유기농 및 비유전자 재조합 인증

제조 공정 분석

구아검 추출

효소 가수분해 공정

정제 기술

건조와 분쇄

품질 관리 절차

원재료 분석 및 조달 전략

가격 분석

지속가능성과 환경영향 평가

PESTEL 분석

Porter's Five Forces 분석

무역 분석 : 수출입 시나리오

트럼프 정권의 관세 분석

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

무역 통계(HS코드)

주요 수출국(2021-2024년)

미국

일본

한국

주요 수입국(2021-2024년)

인도

러시아

미국

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

제4장 경쟁 구도

시장 점유율 분석

전략 틀

합병과 인수

합작투자와 콜라보레이션

신제품 개발

확대 전략

경쟁 벤치마킹

벤더 상황

경쟁 포지셔닝 매트릭스

전략적 대시보드

특허 분석과 혁신평가

신규 참가자 시장 진출 전략

배전망 분석

제5장 시장 추계 및 예측 : 등급별(2021-2034년)

주요 동향

식품 등급

표준

프리미엄

의약품

산업

기타

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

주요 동향

분말

세립

조립

과립

기타

제7장 시장 추계 및 예측 : 제조 방법별(2021-2034년)

주요 동향

효소 가수분해

배치

연속

화학적 가수분해

기타 생산

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

식품 및 베이커리

베이커리 및 과자류

유제품 및 냉동 디저트

음료

조식용 시리얼 바

소스, 드레싱, 조미료

고기 및 닭고기 제품

기타 식품 용도

영양보조식품

식이섬유 보충제

체중 관리 보충제

소화기계의 건강 보충제

기타 보충제 유형

의약품

고형 제형

액체 제형

기타 의약품 용도

퍼스널케어 및 화장품

동물사료

기타 용도

제9장 시장 추계 및 예측 : 기능별(2021-2034년)

주요 동향

식이섬유 강화

프리바이오틱스 효과

식감 개선

안정

증점

지방 치환

기타 기능

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

식품 및 음료 업계

주요 식품 제조업체

중형 및 소형 푸드 프로세서

전문 식품 제조업체

영양보조식품업계

제약업계

주요 제약 회사

제네릭 의약품 제조업체

계약 제조 조직(CMOS)

퍼스널케어 업계

동물사료 산업

기타 최종 이용 산업

제11장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

주요 동향

직접 판매

리셀러 및 도매업체

온라인 채널

기타

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

러시아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제13장 기업 프로파일

Altrafine Gums

Ashland Global Holdings Inc.

BASF SE

Cargill, Incorporated

CP Kelco US, Inc.

Dabur India Ltd.

Deosen Biochemical Ltd.

DuPont de Nemours, Inc.

Fufeng Group

Guangrao Liuhe Chemical Co., Ltd.

Hindustan Gum &Chemicals Ltd.

Ingredion Incorporated

Jingkun Chemistry Company

Kerry Group plc

Lonza Group AG

Lotus Gums &Chemicals

Lucid Colloids Ltd.

Meihua Holdings Group Co., Ltd.

Neelkanth Polymers

Nexira

Polygal AG

Rama Industries

Shandong Yuansheng Chemical Co., Ltd.

Shree Ram Gum Chemicals

Sunita Hydrocolloids Pvt. Ltd.

Taiyo International, Inc.

Tic Gums, Inc.(Ingredion)

Vikas WSP Limited

Wuxi Jinxin Science &Technology Co., Ltd.

HBR

영문 목차

영문목차

The Global Partially Hydrolyzed Guar Gum Market was valued at USD 251.1 million in 2024 and is estimated to grow at a CAGR of 6% to reach USD 447.5 million by 2034, driven by the global surge in demand for digestive health products, clean-label nutrition, and prebiotic-enriched foods. PHGG undergoes enzymatic hydrolysis, making it a low-viscosity, water-soluble fiber ideal for several applications. It maintains stability across varying pH levels and temperatures, offering compatibility with diverse food systems including functional foods, beverages, and dietary supplements. The increasing shift toward plant-based, allergen-free ingredients has also positioned PHGG as a preferred component in formulating health-focused consumer products.

Consumers seeking digestive relief are fueling the demand for PHGG in nutraceuticals, where its prebiotic benefits support gut microbiota balance and alleviate symptoms of gastrointestinal disorders. The ingredients are increasingly found in bakery goods, plant-based alternatives, fortified snacks, and therapeutic formulations due to ease of incorporation and functional versatility. It offers clean-label appeal, excellent solubility, and a mild taste, making it ideal for health-conscious consumers looking to boost daily fiber intake without compromising texture or flavor.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$251.1 Million

Forecast Value

$447.5 Million

CAGR

6%

The food-grade segment generated USD 125 million in 2024. This segment benefits from the broad usage of PHGG in everyday food items due to its solubility and health-promoting qualities. PHGG's ability to deliver functional fiber without compromising flavor or texture has driven its integration into fiber-enriched beverages, cereals, and meal bars. Its role in promoting satiety and digestive comfort makes it ideal for consumers seeking clean-label, wellness-oriented products.

The pharmaceutical segment generated USD 70.9 million in 2024 and is projected to reach USD 116.4 million by 2034. PHGG is well-recognized in clinical nutrition for managing digestive ailments such as IBS and constipation. Its low viscosity and tolerance across age groups make it suitable for long-term dietary support. As clinical data increasingly affirms its efficacy, PHGG is finding wider use in colon health supplements and therapeutic fiber-based interventions, especially in geriatric and health-conscious populations worldwide.

United States Partially Hydrolyzed Guar Gum Market generated USD 55.5 million in 2024 witnessing substantial traction from the food and pharma sectors. Use cases are expanding rapidly across therapeutic dietary applications, medical nutrition, and even pet and personal care categories, with demand rising especially among aging populations. The ingredient's ability to support digestive health, manage glycemic response, and aid in weight control positions are a functional staple in health-focused product development. Formulators are also exploring PHGG for its compatibility with supplements, clinical nutrition formulas, and geriatric dietary needs.

Key market players in the Partially Hydrolyzed Guar Gum Market include BASF SE, Ingredion Incorporated (and its subsidiary Tic Gums, Inc.), CP Kelco U.S., Inc., Ashland Global Holdings Inc., and Cargill, Incorporated. These companies are actively contributing to market innovation and expansion. Strategic focus, leading companies in the partially hydrolyzed guar gum space are investing heavily in R&D to develop specialized PHGG variants tailored for pharmaceutical, functional food, and clean-label applications. Many players are expanding their production capacities to meet growing global demand, especially in North America and Asia. Strategic collaborations with food and nutraceutical manufacturers are helping firms broaden their distribution networks. Regulatory approvals and clinical validation are also key to market entry and credibility, prompting companies to prioritize scientific studies and safety certifications.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Research methodology

1.2 Research scope & assumptions

1.3 List of data sources

1.4 Market estimation technique

1.5 Market segmentation & breakdown

1.6 Research limitations

Chapter 2 Executive Summary

2.1 Market snapshot

2.2 Segment highlights

2.3 Competitive landscape snapshot

2.4 Regional market outlook

2.5 Key market trends

2.6 Future market outlook

Chapter 3 Industry Insights

3.1 Market introduction

3.2 Industry value chain analysis

3.3 Product overview

3.3.1 Phgg: definition & composition

3.3.2 Production process & enzymatic hydrolysis

3.3.3 Physicochemical properties

3.3.4 Nutritional profile & health benefits

3.3.5 Prebiotic properties & gut health effects

3.3.6 Comparison with native guar gum

3.3.7 Comparison with other dietary fibers

3.4 Market dynamics

3.4.1 Market drivers

3.4.1.1 Rising demand for digestive health and prebiotics

3.4.1.2 Growth in functional foods and nutraceuticals

3.4.1.3 Clean-label and plant-based ingredient preferences

3.5 Market restraints

3.5.1.1 High production and processing costs

3.5.1.2 Limited consumer awareness in emerging markets

3.5.1.3 Regulatory complexity across regions

3.6 Market opportunities

3.6.1.1 Rising demand for gut health functional ingredients

3.6.1.2 Expanding applications in nutraceutical and food sectors

3.6.1.3 Growing interest in low-fodmap dietary fibers

3.7 Industry impact forces

3.7.1 Growth potential analysis

3.7.2 Industry pitfalls & challenges

3.8 Regulatory framework & standards

3.8.1 Food additive regulations

3.8.2 Dietary fiber definitions

3.8.3 Health claim regulations

3.8.4 Quality & safety standards

3.8.5 Organic & non-gmo certifications

3.9 Manufacturing process analysis

3.9.1 Guar gum extraction

3.9.2 Enzymatic hydrolysis process

3.9.3 Purification techniques

3.9.4 Drying & milling

3.9.5 Quality control procedures

3.10 Raw material analysis & procurement strategies