의료기기 수탁제조 시장 : 업계 동향과 세계 예측 - 용도별, 기기 클래스별, 대상 치료 영역별, 주요 지역별

Medical Device Contract Manufacturing Market: Industry Trends and Global Forecasts - Distribution by Application Area, Device Class, Target Therapeutic Area, Key Geographical Regions

상품코드:1762532

리서치사:Roots Analysis

발행일:2025년 07월

페이지 정보:영문 560 Pages

라이선스 & 가격 (부가세 별도)

한글목차

의료기기 수탁제조 시장 : 개요

세계의 의료기기 수탁제조 시장 규모는 올해 788억 달러에 달했습니다. 이 시장은 예측 기간 중 8.2%의 CAGR로 확대할 것으로 예측됩니다.

시장 세분화에서는 시장 규모 및 기회 분석을 다음과 같은 매개 변수로 구분합니다.

용도

치료용 의료기기

진단용 의료기기

약물전달 의료기기

기타 장비

장비 클래스

클래스 I

클래스 II

클래스 III

대상 치료 영역

심혈관 질환

중추신경계 질환

대사성 질환

종양학 질환

안과 질환

정형외과 질환

통증 장애

호흡기 질환

기타

주요 지역

북미(미국)

유럽(이탈리아, 독일, 프랑스, 스페인, 영국, 기타)

아시아태평양(중국, 일본, 인도)

기타 지역

의료기기 수탁제조 시장 : 성장과 동향

지난 50년 동안 의료기기 산업은 최소침습 수술기구의 도입과 심박조율기와 같은 이식형 기기의 등장 등 몇 가지 주목할 만한 발전을 이루었습니다. 또한 매년 수백만 명의 사람들이 수술이나 이식을 받고 있으므로 보철물과 같은 생체 의료기기의 사용도 시간이 지남에 따라 크게 증가하고 있습니다. 또한 심장 제세동기, 인공 고관절 및 인공 슬관절, 콘택트렌즈, 심장 페이스메이커 등은 가장 일반적으로 이식되는 의료기기 중 일부이며, 고정 장비 및 인공 관절은 전체 의료기기의 약 44%를 차지합니다. 이는 헬스케어 영역에서 의료기기 수요가 증가하고 있음을 보여줍니다. 그러나 대부분의 개발자들은 의료기기 및 관련 부품을 제조할 수 있는 충분한 자원과 필요한 전문 지식을 갖추고 있지 못합니다.

의료기기 CRO의 부상과 함께 의료기기에 정통한 CMO의 활약의 장도 꾸준히 확대되고 있으며, 2000년 이후 65개 이상의 CMO가 설립되었습니다는 점은 주목할 만합니다. 또한 세계보건기구(WHO)의 보고에 따르면 전 세계에서 약 200만 유형의 의료기기가 존재하며, 7,000개 이상의 범용기기 카테고리로 분류되어 있습니다. 주목할 만한 점은 CMO가 큰 비용적 이점, 정교한 최신 인프라에 대한 접근성, 대규모 생산 능력, 시장 출시 시간 단축을 제공하는 것으로 알려져 있다는 점입니다. 그 결과, 의료기기 수탁제조 서비스 프로바이더에 대한 기회는 꾸준히 확대되고 있습니다.

의료기기 수탁제조 시장 : 주요 인사이트

이 보고서는 의료기기 수탁제조 시장의 현황을 조사하고, 업계내 잠재적인 성장 기회를 파악합니다. 주요 조사 결과는 다음과 같습니다.

참신한 기술과 플랫폼이 많은 중소 의료기기 기업의 설립과 성공의 주요 요인 중 하나로 부상하고 있습니다.

규제 대응과 승인에 따른 복잡성, 제조 비용 증가, 다양한 기술로 인해 스폰서들은 장비의 전체 수명주기을 지원할 수 있는 제조 파트너를 찾고 있습니다.

전 세계 275개 이상의 기업이 치료 및 진단용 제품을 포함한 다양한 유형의 의료기기에 대한 제조 위탁 서비스를 제공하는 데 필요한 전문 지식과 인허가를 보유하고 있습니다.

시장 상황은 세분화되어 있으며, 기존 진입기업과 신규 진입기업이 모두 존재합니다. 현재 대부분의 의료기기 제조시설은 선진 지역에 위치하고 있습니다.

의료기기 CMO는 다양한 세계 및 지역 규제기관별 확립된 기준을 준수하기 위해 적극적으로 업무 조율에 힘쓰고 있습니다.

임플란트 분야는 비교적 활발한 인수 활동이 가장 두드러진 분야 중 하나로 부상하고 있습니다. 이러한 인수의 주요 가치 창출 요인으로는 역량 추가와 지역적 통합을 들 수 있습니다.

지난 6년간 다양한 의료기기를 평가하는 9,600건 이상의 임상시험이 다양한 유형의 스폰서에 의해 등록되었으며, 다양한 치료 분야를 망라하고 있습니다.

이 분야에 종사하는 기업은 각자의 서비스 포트폴리오를 강화하고 진화하는 업계 벤치마크를 준수하기 위해 꾸준히 역량을 확장하고 있습니다.

빠르게 확대되는 수요에 힘입어 의료기기 위탁 서비스 시장은 다양한 치료 분야와 지역의 완제품에 대해 연간 8.2% 이상 성장할 것으로 예측됩니다.

현재 기존 CMO가 큰 비중을 차지하고 있지만, 장기적으로는 다양한 유형의 기업, 장비 클래스, 용도에 기회가 분산될 것으로 예측됩니다.

의료기기 수탁제조 시장 : 주요 부문

시장은 용도별로 치료용 의료기기, 진단용 의료기기, 약물전달 의료기기, 기타 기기로 구분됩니다. 현재 전 세계 의료기기 수탁제조 시장에서는 인슐린 펌프, 주입 펌프 등 치료용 기기 수요가 증가함에 따라 치료용 의료기기 분야가 가장 큰 비중을 차지하고 있습니다. 또한 약물전달 기기 부문의 의료기기 수탁제조 시장은 예측 기간 중 가장 높은 시장 성장성을 보일 것으로 예측됩니다.

기기 등급별로 시장은 Class I, Class II, Class III로 구분됩니다. 현재 전 세계 의료기기 수탁제조 시장에서 가장 큰 점유율을 차지하고 있는 것은 Class II입니다. 또한 클래스 II 디바이스가 제공하는 다양한 장점(예: 사용자 정의의 용이성, 다양한 제품군 등)으로 인해 클래스 II 부문 시장은 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

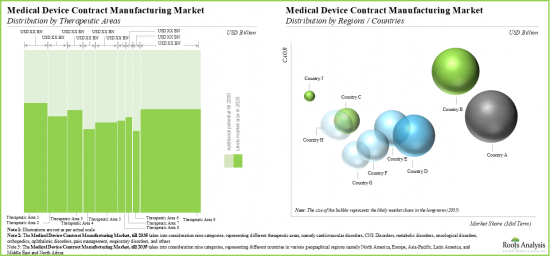

시장은 대상 치료 영역에 따라 심혈관질환, 중추신경계질환, 대사질환, 종양질환, 정형외과질환, 안과질환, 통증질환, 호흡기질환, 기타로 구분됩니다. 현재 정형외과 질환 분야가 세계 의료기기 수탁제조 시장에서 가장 높은 비중을 차지하고 있습니다. 그러나 비만, 인슐린 저항성, 1형 당뇨병, 고혈압과 같은 대사성 질환의 유병률 증가로 인해 대사성 질환 분야는 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

주요 지역별로 시장은 북미, 유럽, 아시아태평양, 기타 지역으로 구분됩니다. 현재 북미는 전 세계 의료기기 수탁제조 시장을 독점하고 있으며, 가장 큰 매출 점유율을 차지하고 있습니다. 또한 아시아태평양 시장은 향후 더 높은 CAGR로 성장할 가능성이 높습니다.

의료기기 수탁제조 시장의 참여 기업 예

Cirtec Medical

Creganna Medical

DynaFlex Technologies

Europlaz Technologies

I-Tek Medical Technologies

Interplex

Keystone Solutions Group

Modern Medical

Oscor

Riverside Medical Packaging

SMC

Synecco

Suzhou Jenitek

Stellartech Research

Trelleborg Sealing Solutions

목차

제1장 서문

제2장 개요

제3장 서론

챕터 개요

의료기기 : 개요

의료기기 제조

의료기기 CMO의 역사적 타임라인

의료기기 CMO가 제공하는 서비스

의료기기 CMO가 제공하는 이점

CMO에 대한 아웃소싱에 수반하는 리스크

주요 고려사항

결론

제4장 의료기기의 규제 상황

챕터 개요

의료기기에 관한 일반 규제 가이드라인

북미의 규제 상황

유럽의 규제 상황

아시아태평양의 규제 상황

지역 규제 환경의 비교

제5장 시장 개요 : 치료 기기

챕터 개요

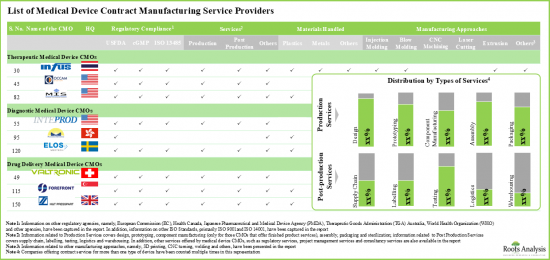

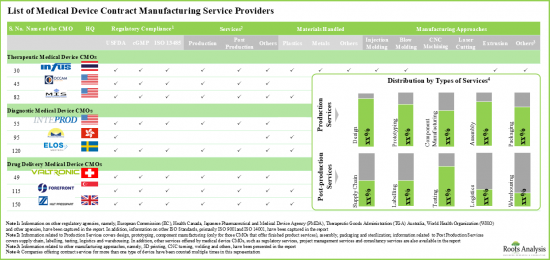

치료 기기용 서비스를 제공하는 의료기기 CMO

제6장 시장 개요 : 진단 기기

챕터 개요

진단 기기용 서비스를 제공하는 의료기기 CMO

제7장 시장 개요 : 전달 시스템과 기타

챕터 개요

카테터

약물전달 디바이스

기타 디바이스

제8장 벤치마크 분석

챕터 개요

벤치마크 분석 : 조사 방법

지역별 벤치마크 분석

결론

제9장 공급망 분석

챕터 개요

의료기기 공급망의 개요

의료기기 공급망에 영향을 미치는 요인

핵심성과지표

공급망 개선 전략

공급망 최적화 효과

비용 분석

제10장 기업 개요

챕터 개요

북미에 본사를 둔 CMO

Cirtec Medical

DynaFlex Technologies

I-Tek Medical Technologies

Keystone Solutions Group

Oscor

SMC

Stellartech Research

유럽에 본사를 둔 CMO

Creganna Medical

Europlaz Technologies

Riverside Medical Packaging

Synecco

Trelleborg Sealing Solutions

아시아에 본사를 둔 CMO

Interplex

Modern Medical

Providence Enterprise

Suzhou JenitekJenitek

제11장 임상시험 분석

챕터 개요

범위와 조사 방법

임상시험 분석 : 시험 타이틀의 워드 클라우드

임상시험의 분석

등록 피험자의 분석

중점 치료 영역의 분석

제12장 합병과 인수

제13장 사례 연구 : 의료기기 오프쇼어 제조 위탁

챕터 개요

신흥 시장 : 정의와 주요 지역

산업 제조에서 신흥 시장의 역할

신흥 시장에서의 의료기기 제조

신흥 시장에서 의료기기의 제조에 주력하는 다국적기업

신흥 시장에서 의료기기 제조의 비즈니스 모델

의료기기 업계에서 혁신에 관한 주요 과제

신흥 시장에 혁신 허브를 설립하는 이점

향후 전망

제14장 시장 예측

챕터 개요

예측 조사 방법과 주요 전제조건

2035년까지 의료기기 수탁제조 시장 전체

의료기기 계약 제조 시장 : 지역 분포(-2035년)

제15장 SWOT 분석

제16장 결론

제17장 조사/인터뷰 기록

제18장 부록 1 : 표형식 데이터

제19장 부록 2 : 기업·단체 리스트

KSA

영문 목차

영문목차

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: OVERVIEW

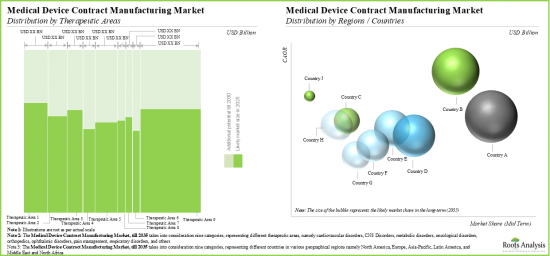

As per Roots Analysis, the global medical device contract manufacturing market valued at USD 78.8 billion in the current year is anticipated to grow at a CAGR of 8.2% during the forecast period.

The market sizing and opportunity analysis has been segmented across the following parameters:

Application Areas

Therapeutic Medical Devices

Diagnostic Medical Devices

Drug Delivery Medical Devices

Other Devices

Device Class

Class I

Class II

Class III

Target Therapeutic Area

Cardiovascular Disorders

CNS Disorders

Metabolic Disorders

Oncological Disorders

Ophthalmic Disorders

Orthopedic Disorders

Pain Disorders

Respiratory Disorders

Others

Key Geographical Regions

North America (US)

Europe (Italy, Germany, France, Spain, UK, Rest of the Europe)

Asia-Pacific (China, Japan, India)

Rest of the World

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: GROWTH AND TRENDS

Over the past 50 years, the medical device industry has seen several notable developments, such as the introduction of minimally invasive surgical instruments and the rise of implantable devices like pacemakers. Additionally, the use of biomedical devices like prostheses has increased substantially over time owing to the fact that each year, millions of individuals undergo surgeries and implantations. Further, cardioverter defibrillators, prosthetic hips and knees, contact lenses, and cardiac pacemakers are some of the most commonly implanted medical devices, while fixation devices and artificial joints account for about 44% of all medical devices. This is indicative of the growing demand for medical devices in the healthcare domain. However, most developers lack adequate resources and the necessary expertise to manufacture medical devices and related components.

Given the rise of medical device CROs, the opportunity for CMOs with expertise in medical devices is also steadily rising. It is worth highlighting that, since 2000, more than 65 CMOs have been established. Further, the World Health Organization reports approximately 2 million unique medical devices worldwide, classified into more than 7,000 generic device categories. Notably, CMOs are known to offer significant cost-benefits, access to sophisticated / up-to-date infrastructure, large production capacities and reduction in time-to-market. As a result, the opportunity for medical device contract manufacturing service providers is steadily increasing.

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: KEY INSIGHTS

The report delves into the current state of the medical device contract manufacturing market and identifies potential growth opportunities within industry. Some key findings from the report include:

Novel technologies and platforms have emerged as one of the primary factors responsible for the establishment and success of a number of small and mid-sized medical device companies.

Owing to complexities associated with regulatory compliance and approvals, increasing manufacturing costs and varying technologies, sponsors seek a manufacturing partner that can support the entire lifecycle of the device.

Over 275 companies worldwide have the necessary expertise and authorization to offer contract manufacturing services for various types of medical devices, including therapeutic and diagnostic products

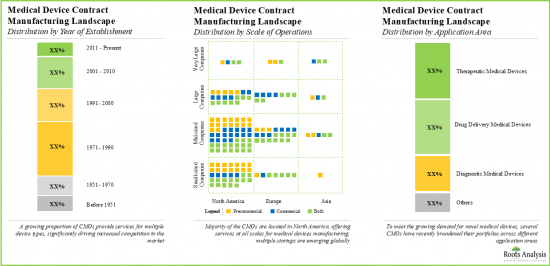

The market landscape is fragmented, featuring the presence of both established players and new entrants; presently, most medical device manufacturing facilities are located in the developed geographies.

Medical device CMOs are actively engaged in aligning their operations to comply with the standards established by various global and regional regulatory bodies.

Implants have emerged as one of the most prominent segments for which the acquisition activity is relatively higher; key value drivers behind such acquisitions include capability addition and geographical consolidation.

In the last six years, over 9,600 trials evaluating various medical devices have been registered by different types of sponsors covering a wide range of therapeutic areas.

Companies involved in this domain are steadily expanding their capabilities in order to enhance their respective service portfolios and comply with evolving industry benchmarks.

Driven by a rapidly growing demand, medical device contract services market is anticipated to grow at annualized rate of over 8.2% for a variety of therapeutic areas and geographies for finished products.

Established CMOs currently occupy a major share; in the long term, the opportunity is anticipated to be better distributed across different types of companies, device classes and application areas.

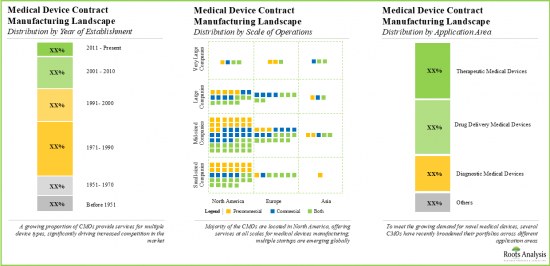

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: KEY SEGMENTS

Therapeutic Medical Devices Segment holds the Largest Share of the Medical Device Contract Manufacturing Market

Based on the application areas, the market is segmented into therapeutic medical devices, diagnostic medical devices, drug delivery medical devices and other devices. At present, the therapeutic medical devices segment holds the maximum share of the global medical device contract manufacturing market owing to the increasing demand for therapeutic devices such as insulin pumps and infusion pumps. Further, the medical device contract manufacturing market for drug delivery devices segment is expected to show the highest market growth potential during the forecast period.

By Device Class, Class II is the Fastest Growing Segment of the Global Medical Device Contract Manufacturing Market

Based on the device class, the market is segmented into Class I, Class II and Class III. At present, the class II segment holds the maximum share of the global medical device contract manufacturing market. Further, owing to the various benefits offered by class II devices, such as ease of customization and diverse product range, the market for class II segment is expected to grow at a higher CAGR during the forecast period.

By Target Therapeutic Area, Orthopedic Disorders Segment Accounts for the Largest Share of the Global Medical Device Contract Manufacturing Market

Based on the target therapeutic area, the market is segmented into cardiovascular disorders, CNS disorders, metabolic disorders, oncological disorders, orthopedic disorders, ophthalmic disorders, pain disorders, respiratory disorders, and others. Currently, the orthopedic disorders segment captures the highest proportion of the global medical device contract manufacturing market. However, the metabolic disorders segment is expected to grow at a higher CAGR during the forecast period owing to the growing prevalence of metabolic disorders such as obesity, insulin resistance, Type 1 diabetes and hypertension.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia-Pacific and Rest of the World. Currently, North America dominates the global medical device contract manufacturing market and accounts for the largest revenue share. Further, the market in Asia-Pacific is likely to grow at a higher CAGR in the coming future.

Example Players in the Medical Device Contract Manufacturing Market

Cirtec Medical

Creganna Medical

DynaFlex Technologies

Europlaz Technologies

I-Tek Medical Technologies

Interplex

Keystone Solutions Group

Modern Medical

Oscor

Riverside Medical Packaging

SMC

Synecco

Suzhou Jenitek

Stellartech Research

Trelleborg Sealing Solutions

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global medical device contract manufacturing market, focusing on key market segments, including [A] application areas, [B] device class, [C] target therapeutic area and [D] key geographical regions.

Market Landscape: A comprehensive evaluation of the medical device contract manufacturers, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] manufacturing facilities, [D] geographical location, [E] type of device manufactured, [F] the scale of operation and [G] types of services offered.

Regulatory Landscape for Medical Devices: A comprehensive discussion of the various guidelines established by major regulatory bodies for medical device approval across different countries. Additionally, the section includes a multi-dimensional bubble analysis, focusing on a comparison of the contemporary regulatory scenario in key geographies across the globe.

Benchmark Analysis: A comprehensive benchmark analysis emphasizing the primary focus areas of small, mid-sized, and large companies, comparing their current capabilities within and across peer groups, and offering stakeholders insights to achieve a competitive advantage in the industry.

Supply Chain Analysis: A detailed analysis of medical device supply chain, highlighting the role of CMOs engaged in the medical device contract manufacturing market and analysis based on services offered, such as [A] supply chain management services, [B] logistics services, [C] shipping services, and [D] warehousing services.

Company Profiles: In-depth profiles of key players that specialize in providing services for both pre-commercial and commercial scale manufacturing of medical devices, focusing on [A] overview of the company, [B] service portfolio, [C] manufacturing facilities and [D] recent developments and an informed future outlook.

Clinical Trial Analysis: An insightful analysis of clinical trials related to medical devices, based on several parameters, such as [A] number of registered trials, [B] current status of trials, [C] phase of development, [D] type of sponsor, [E] therapeutic area(s), [F] target disease indication(s), and [G] number of patients enrolled.

Mergers and Acquisitions: An in-depth analysis of mergers and acquisitions undertaken in the medical device contract manufacturing market highlighting the number of companies acquired in recent years. Further, in depth-analysis of the key value drivers for these mergers and acquisitions was performed. In addition, the analysis features an ownership change matrix, providing a summary of the involvement of private and public sector entities in the market.

SWOT Analysis: An analysis of industry affiliated trends, opportunities and challenges, which are likely to impact the evolution of antibody contract manufacturing market; it includes a Harvey ball analysis, assessing the relative impact of each SWOT parameter on industry dynamics.

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What factors are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary PPT Insights Packs

Complimentary Excel Data Packs for all Analytical Modules in the Report

15% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

1.1. Scope of the Report

1.2. Research Methodology

1.2.1. Research Assumptions

1.2.2. Project Methodology

1.2.3. Forecast Methodology

1.2.4. Robust Quality Control

1.2.5. Key Considerations

1.2.5.1. Demographics

1.2.5.2. Economic Factors

1.2.5.3. Government Regulations

1.2.5.4. Supply Chain

1.2.5.5. COVID Impact / Related Factors

1.2.5.6. Market Access

1.2.5.7. Healthcare Policies

1.2.5.8. Industry Consolidation

1.3 Key Questions Answered

1.4. Chapter Outlines

2. EXECUTIVE SUMMARY

3. INTRODUCTION

3.1. Chapter Overview

3.2. Medical Devices: An Overview

3.2.1. History of Medical Devices

3.2.2. Classification of Medical Devices

3.3. Medical Device Manufacturing

3.3.1. Challenges Associated with Medical Device Manufacturing

3.3.2. Role of CMOs in Medical Device Manufacturing

3.3.3. Role of Automation in Medical Device Manufacturing Process

3.4. Historical Timeline for Medical Device CMOs

3.5. Services Offered by Medical Device CMOs

3.6. Advantages Offered by Medical Device CMOs

3.7. Risks associated with Outsourcing to CMOs

3.8. Key Considerations

3.9. Concluding Remarks

4. REGULATORY LANDSCAPE FOR MEDICAL DEVICES

4.1. Chapter Overview

4.2. General Regulatory Guidelines for Medical Devices

4.3. Regulatory Landscape in North America

4.3.1. The US Scenario

4.3.1.1. Regulatory Authority

4.3.1.2. Review / Approval Process

4.3.2. The Canadian Scenario

4.3.2.1. Regulatory Authority

4.3.2.2. Review / Approval Process

4.4. Regulatory Landscape in Europe

4.4.1. Overall Scenario

4.4.1.1. Regulatory Authority

4.4.1.2. Review / Approval Process

4.4.2. Case Study: Brexit -The UK Scenario

4.5. Regulatory Landscape in Asia-Pacific

4.5.1. The Chinese Scenario

4.5.1.1. Regulatory Authority

4.5.1.2. Review / Approval Process

4.5.2. The Japanese Scenario

4.5.2.1. Regulatory Authority

4.5.2.2. Review / Approval Process

4.5.3. The Australian Scenario

4.5.3.1. Regulatory Authority

4.5.3.2. Review / Approval Process

4.6. Comparison of Regional Regulatory Environment

5. MARKET OVERVIEW: THERAPEUTIC DEVICES

5.1. Chapter Overview

5.2. Medical Device CMOs Offering Services for Therapeutic Devices

5.2.1. Analysis by Year of Establishment

5.2.2. Analysis by Size of Employee Base

5.2.3. Analysis by Location of Headquarters

5.2.4. Analysis by Location of Manufacturing Facility

5.2.5. Analysis by Regulatory Certifications / Accreditations

5.2.6. Analysis by Production Services Offered

5.2.7. Analysis by Post-production Services Offered

5.2.8. Analysis by Other Services Offered

5.2.9. Analysis by Device Class

5.2.10. Analysis by Type of Material(s) Handled

5.2.11. Analysis by Scale of Operation

5.2.12. Leading Players

6. MARKET OVERVIEW: DIAGNOSTIC DEVICES

6.1. Chapter Overview

6.2. Medical Device CMOs Offering Services for Diagnostic Devices

6.2.1. Analysis by Year of Establishment

6.2.2. Analysis by Size of Employee Base

6.2.3. Analysis by Location of Headquarters

6.2.4. Analysis by Location of Manufacturing Facility

6.2.5. Analysis by Regulatory Certifications / Accreditations

6.2.6. Analysis by Production Services Offered

6.2.7. Analysis by Post-Production Services Offered

6.2.8. Analysis by Other Services Offered

6.2.9. Analysis by Device Class

6.2.10. Analysis by Type of Material(s) Handled

6.2.11. Analysis by Scale of Operation

6.2.12. Leading Players

7. MARKET OVERVIEW: DELIVERY SYSTEMS AND OTHERS

7.1. Chapter Overview

7.2. Catheters

7.2.1. Medical Device CMOs Offering Services for Catheters

7.2.2. Analysis by Year of Establishment

7.2.3. Analysis by Size of Employee Base

7.2.4. Analysis by Location of Headquarters

7.2.5. Analysis by Location of Manufacturing Facility

7.2.6. Analysis by Regulatory Certifications / Accreditations

7.2.7. Analysis by Production Services Offered

7.2.8. Analysis by Post-Production Services Offered

7.2.9. Analysis by Other Services Offered

7.2.10. Analysis by Device Class

7.2.11. Analysis by Type of Material(s) Handled

7.2.12. Analysis by Scale of Operation

7.2.13. Leading Players

7.3. Drug Delivery Devices

7.3.1. Medical Device CMOs Offering Services for Drug Delivery Devices

7.3.2. Analysis by Year of Establishment

7.3.3. Analysis by Size of Employee Base

7.3.4. Analysis by Location of Headquarters

7.3.5. Analysis by Location of Manufacturing Facility

7.3.6. Analysis by Regulatory Certifications / Accreditations

7.3.7. Analysis by Production Services Offered

7.3.8. Analysis by Post-Production Services Offered

7.3.9. Analysis by Other Services Offered

7.3.10. Analysis by Device Class

7.3.11. Analysis by Type of Material(s) Handled

7.3.12. Analysis by Scale of Operation

7.3.13. Leading Players

7.4. Other Devices

7.4.1. Medical Device CMOs Offering Services for Other Medical Devices

7.4.2. Analysis by Year of Establishment

7.4.3. Analysis by Size of Employee Base

7.4.4. Analysis by Location of Headquarters

7.4.5. Analysis by Location of Manufacturing Facility

7.4.6. Analysis by Regulatory Certifications / Accreditations

7.4.7. Analysis by Production Services Offered

7.4.8. Analysis by Post-Production Services Offered

7.4.9. Analysis by Other Services Offered

7.4.10. Analysis by Device Class

7.4.11. Analysis by Type of Material(s) Handled

7.4.12. Analysis by Scale of Operation

8. BENCHMARK ANALYSIS

8.1. Chapter Overview

8.2. Benchmark Analysis: Methodology

8.3. Region-wise Benchmark Analysis

8.3.1. North America, Peer Group I

8.3.2. North America, Peer Group II

8.3.3. North America, Peer Group III

8.3.4. North America, Peer Group IV

8.3.5. North America, Peer Group V

8.3.6. North America, Peer Group VI

8.3.7. North America, Peer Group VII

8.3.8. Europe, Peer Group VIII

8.3.9. Europe, Peer Group IX

8.3.10. Europe, Peer Group X

8.3.11. Asia, Peer Group XI

8.3.12. Asia, Peer Group XII

8.4. Concluding Remarks

9. SUPPLY CHAIN ANALYSIS

9.1. Chapter Overview

9.2. Overview of the Medical Device Supply Chain

9.3. Factors Affecting the Medical Device Supply Chain

9.4. Key Performance Indicators

9.5. Supply Chain Improvement Strategies

9.5.1. Optimization of Supply Chain Capabilities

9.5.2. Visible Supply Chain and Related Advantages

9.5.2.1. Augmenting Supply Chain Visibility Through Digitalization

9.5.2.2. Benefits of Digital Supply Chain

9.6. Effects of Supply Chain Optimization

9.7. Cost Analysis

9.7.1. Production-related Costs

9.7.1.1. Labor Costs

9.7.1.2. Raw Materials Related Costs

9.7.1.3. Regulatory Compliance

9.7.1.4. Technology-related Costs

9.7.2. Supply Chain-related Costs

9.7.2.1. Local Presence

9.7.2.2. Geopolitical Risk

9.7.2.3. Logistics

10. COMPANY PROFILES

10.1. Chapter Overview

10.2. CMOs Headquartered in North America

10.2.1. Cirtec Medical

10.2.1.1. Company Overview

10.2.1.2. Service Portfolio

10.2.1.3. Manufacturing Capabilities and Facilities

10.2.1.3.1. Facilities located in North America

10.2.1.3.2. Facilities Located in Europe

10.2.1.4. Future Outlook

10.2.2. DynaFlex Technologies

10.2.2.1. Company Overview

10.2.2.2. Service Portfolio

10.2.2.3. Manufacturing Capabilities and Facilities

10.2.2.4. Future Outlook

10.2.3. I-Tek Medical Technologies

10.2.3.1. Company Overview

10.2.3.2. Service Portfolio

10.2.3.3. Manufacturing Capabilities and Facilities

10.2.3.4. Future Outlook

10.2.4. Keystone Solutions Group

10.2.4.1. Company Overview

10.2.4.2. Service portfolio

10.2.4.3. Manufacturing Facilities

10.2.4.4. Future Outlook

10.2.5. Oscor

10.2.5.1. Company Overview

10.2.5.2. Service Portfolio

10.2.5.3. Manufacturing Capabilities and facilities

10.2.5.4. Future Outlook

10.2.6. SMC

10.2.6.1. Company Overview

10.2.6.2. Service Portfolio

10.2.6.3. Manufacturing Capabilities and facilities

10.2.6.3.1. Facilities Located in North America

10.2.6.3.2. Facility Located in Central America

10.2.6.3.3. Facility Located in Europe

10.2.6.3.4. Facility Located in Asia

10.2.6.4. Future Outlook

10.2.7. Stellartech Research

10.2.7.1. Company Overview

10.2.7.2. Service Portfolio

10.2.7.3. Manufacturing Capabilities and facilities

10.2.7.4. Future Outlook

10.3. CMOs Headquartered in Europe

10.3.1. Creganna Medical

10.3.1.1. Company Overview

10.3.1.2. Service Portfolio

10.3.1.3. Manufacturing Facilities

10.3.1.3.1. Facilities Located in North America

10.3.1.3.2. Facilities Located in Central America

10.3.1.3.3. Facilities Located in Europe

10.3.1.3.4. Facilities Located in Asia

10.3.1.4. Future Outlook

10.3.2. Europlaz Technologies

10.3.2.1. Company Overview

10.3.2.2. Service Portfolio

10.3.2.3. Manufacturing facilities

10.3.2.4. Future Outlook

10.3.3. Riverside Medical Packaging

10.3.3.1. Company Overview

10.3.3.2. Service Portfolio

10.3.3.3. Manufacturing Facilities

10.3.3.4. Future Outlook

10.3.4. Synecco

10.3.4.1. Company Overview

10.3.4.2. Service Portfolio

10.3.4.3. Manufacturing Facilities

10.3.4.3.1. Facilities Located in Europe

10.3.4.3.2. Facilities Located in Asia

10.3.4.4. Future Outlook

10.3.5. Trelleborg Sealing Solutions

10.3.5.1. Company Overview

10.3.5.2. Service Portfolio

10.3.5.3. Manufacturing Facilities

10.3.5.3.1. Facilities Located in North America

10.3.5.3.2. Facilities Located in Europe

10.3.5.4. Future Outlook

10.4. CMOs Headquartered in Asia

10.4.1. Interplex

10.4.1.1. Company Overview

10.4.1.2. Service Portfolio

10.4.1.3. Manufacturing Facilities

10.4.1.3.1. Facilities Located in North America

10.4.1.3.2. Facilities Located in Europe

10.4.1.3.3. Facilities Located in Asia

10.4.1.4. Future Outlook

10.4.2. Modern Medical

10.4.2.1. Company Overview

10.4.2.2. Service Portfolio

10.4.2.3. Manufacturing facilities

10.4.2.4. Future Outlook

10.4.3. Providence Enterprise

10.4.3.1. Company Overview

10.4.3.2. Service Portfolio

10.4.3.3. Manufacturing Facilities

10.4.3.4. Future Outlook

10.4.4. Suzhou JenitekJenitek

10.4.4.1. Company overview

10.4.4.2. Service Portfolio

10.4.4.3. Manufacturing Facilities

10.4.4.4. Future Outlook

11. CLINICAL TRIAL ANALYSIS

11.1. Chapter Overview

11.2. Scope and Methodology

11.3. Clinical Trial Analysis: Word Cloud of Trial Titles

11.4. Analysis of Clinical Trials

11.4.1. Analysis by Trial Start Year

11.4.2. Analysis by Trial Status

11.4.3. Analysis by Phase of Development

11.4.4. Analysis by Target Indication

11.4.5. Analysis by Type of Sponsor

11.4.6. Analysis by Geography

11.4.7. Analysis by Trial Start Year and Geography

11.5. Analysis of Enrolled Patient Population

11.5.1. Analysis by Trial Status

11.5.2. Analysis by Phase of Development

11.5.3. Analysis by Geography

11.6. Analysis of Focus Therapeutic Areas

11.6.1. Analysis by Type of Sponsor

11.6.2. Analysis by Geography

11.6.2.1. North American Scenario

11.6.2.2. European Scenario

11.6.2.3. Asia Pacific Scenario

11.6.2.4. Rest of the World Scenario

11.6.3. Cardiovascular Disorders

11.6.3.1. Analysis by Trial Start Year

11.6.3.2. Analysis by Type of Sponsor

11.6.3.3. Analysis by Geography

11.6.4. Oncological Disorders

11.6.4.1. Analysis by Trial Start Year

11.6.4.2. Analysis by Type of Sponsor

11.6.4.3. Analysis by Geography

11.6.5. Central Nervous System (CNS) Disorders

11.6.5.1. Analysis by Trial Start Year

11.6.5.2. Analysis by Type of Sponsor

11.6.5.3. Analysis by Geography

11.6.6. Orthopedic Disorders

11.6.6.1. Analysis by Trial Start Year

11.6.6.2. Analysis by Type of Sponsor

11.6.6.3. Analysis by Geography

11.6.7. Respiratory Disorders

11.6.7.1. Analysis by Trial Start Year

11.6.7.2. Analysis by Type of Sponsor

11.6.7.3. Analysis by Geography

12. MERGERS AND ACQUISITIONS

12.1. Chapter Overview

12.2. Merger and Acquisition Models

12.3. Medical Device Contract Manufacturing: Mergers and Acquisitions

12.3.1. Analysis by Year of Mergers and Acquisitions

12.3.2. Analysis by Type of Acquisition

12.3.3. Most Active Acquirers: Analysis by Number of Acquisitions

12.3.4. Analysis by Key Value Drivers

12.3.4.1. Continent-wise distribution

12.3.4.2. Intercontinental and Intracontinental Deals

12.3.4.3. Country-wise distribution

12.3.5. Ownership Change Matrix

12.3.6. Acquisitions Made by Medical Device Companies

12.3.6.1. Acquisition of Entire Company

12.3.6.1.1. Analysis by Key Value Drivers

12.3.6.1.2. Analysis by Key Value Drivers and Year of Acquisition

12.3.6.1.3. Analysis by Type of Services Offered

12.3.6.1.4. Analysis by Type of Device

12.3.6.1.5. Analysis by Therapeutic Area

12.3.6.2. Acquisition of Company Assets

12.3.6.2.1. Analysis by Key Value Drivers

12.3.6.2.2. Analysis by Key Value Drivers and Year of Acquisition

12.3.7. Acquisition by Private Equity Firms

12.3.7.1. Analysis by Year of Acquisition

12.3.7.2. Analysis by Type of Acquisition

12.3.7.3. Analysis by Type of Device

12.3.7.4. Analysis by Therapeutic Area

12.4. Key Acquisitions: Deal Multiples

12.4.1. Analysis by Revenues

13. CASE STUDY: OFFSHORING MEDICAL DEVICE CONTRACT MANUFACTURING

13.1. Chapter Overview

13.2. Emerging Markets: Definitions and Key Regions

13.3. Role of Emerging Markets in Industrial Manufacturing

13.3.1. Contributions to the Automobile Industry

13.3.2. Contributions to the Aerospace and Defense Industries

13.4. Medical Devices Manufacturing in Emerging Markets

13.4.1. The US-Chinese Scenario

13.4.2. Partnership with Companies in Emerging Markets

13.5. Multinational Companies Focused on Manufacturing Medical Devices in Emerging Markets

13.6. Business Models for Medical Device Manufacturing in Emerging Markets

13.6.1. Case Studies

13.6.1.1. Study A: Overview

13.6.1.1.1. Value Proposition

13.6.1.1.2. Value Creation

13.6.1.2. Study B: Overview

13.6.1.2.1. Value Proposition

13.6.1.2.2. Value Creation

13.7. Key Challenges related to Innovation in the Medical Device Industry

13.7.1. Limitations of In-House Innovation

13.8. Advantages of Establishing Innovation Hubs in Emerging Markets

13.8.1. Challenges and Market Restraints

13.8.2. Strategies to Address Existing Challenges

13.9. Future Perspectives

14. MARKET FORECAST

14.1. Chapter Overview

14.2. Forecast Methodology and Key Assumptions

14.3. Overall Medical Device Contract Manufacturing Market, till 2035

14.3.1. Medical Device Contract Manufacturing Market: Distribution by Application Areas, till 2035

14.3.1.1. Medical Device Contract Manufacturing Market for Therapeutic Devices, till 2035

14.3.1.2. Medical Device Contract Manufacturing Market for Diagnostic Devices, till 2035

14.3.1.3. Medical Device Contract Manufacturing Market for Drug Delivery Devices, till 2035

14.3.1.4. Medical Device Contract Manufacturing Market for Other Devices, till 2035

14.3.2. Medical Device Contract Manufacturing Market: Distribution by Device Class, till 2035

14.3.2.1. Medical Device Contract Manufacturing Market: Class I Devices, till 2035

14.3.2.2. Medical Device Contract Manufacturing Market: Class II Devices, till 2035

14.3.2.3. Medical Device Contract Manufacturing Market: Class III Devices, till 2035

14.3.3. Medical Device Contract Manufacturing Market: Leading Players, till 2035

14.3.4. Medical Device Contract Manufacturing Market: Distribution by Therapeutic Areas, till 2035

14.3.4.1. Medical Device Contract Manufacturing Market for Cardiovascular Disorders, till 2035

14.3.4.2. Medical Device Contract Manufacturing Market for CNS Disorders, till 2035

14.3.4.3. Medical Device Contract Manufacturing Market for Metabolic Disorders, till 2035

14.3.4.4. Medical Device Contract Manufacturing Market for Oncological Disorders, till 2035

14.3.4.5. Medical Device Contract Manufacturing Market for Orthopedic Disorders, till 2035

14.3.4.6. Medical Device Contract Manufacturing Market for Ophthalmic Disorders, till 2035

14.3.4.7. Medical Device Contract Manufacturing Market for Pain Disorders, till 2035

14.3.4.8. Medical Device Contract Manufacturing Market for Respiratory Disorders, till 2035

14.3.4.9. Medical Device Contract Manufacturing Market for Other Therapeutic Areas, till 2035

14.4. Medical Device Contract Manufacturing Market: Distribution by Geography, till 2035

14.4.1. Medical Device Contract Manufacturing Market in North America, till 2035

14.4.1.1. Medical Device Contract Manufacturing Market in the US, till 2035

14.4.1.2. Medical Device Contract Manufacturing Market in Rest of North America, till 2035

14.4.1.3. Medical Device Contract Manufacturing Market in North America: Class I Devices, till 2035

14.4.1.4. Medical Device Contract Manufacturing Market in North America: Class II Devices, till 2035

14.4.1.5. Medical Device Contract Manufacturing Market in North America: Class III Devices, till 2035

14.4.1.6. Medical Device Contract Manufacturing Market in North America for Cardiovascular Disorders, till 2035

14.4.1.7. Medical Device Contract Manufacturing Market in North America for CNS Disorders, till 2035

14.4.1.8. Medical Device Contract Manufacturing Market in North America for Metabolic Disorders, till 2035

14.4.1.9. Medical Device Contract Manufacturing Market in North America for Oncological Disorders, till 2035

14.4.1.10. Medical Device Contract Manufacturing Market in North America for Orthopedic Disorders, till 2035

14.4.1.11. Medical Device Contract Manufacturing Market in North America for Ophthalmic Disorders, till 2035

14.4.1.12. Medical Device Contract Manufacturing Market in North America for Pain Disorders, till 2035

14.4.1.13. Medical Device Contract Manufacturing Market in North America for Respiratory Disorders, till 2035

14.4.1.14. Medical Device Contract Manufacturing Market for Other Therapeutic Areas in North America, till 2035

14.4.2. Medical Device Contract Manufacturing Market in Europe, till 2035

14.4.2.1. Medical Device Contract Manufacturing Market in Italy, till 2035

14.4.2.2. Medical Device Contract Manufacturing Market in Germany, till 2035

14.4.2.3. Medical Device Contract Manufacturing Market in France, till 2035

14.4.2.4. Medical Device Contract Manufacturing Market in Spain, till 2035

14.4.2.5. Medical Device Contract Manufacturing Market in the UK, till 2035

14.4.2.6. Medical Device Contract Manufacturing Market in Rest of Europe, till 2035

14.4.2.7. Medical Device Contract Manufacturing Market in Europe: Class I Devices, till 2035

14.4.2.8. Medical Device Contract Manufacturing Market in Europe: Class II Devices, till 2035

14.4.2.9. Medical Device Contract Manufacturing Market in Europe: Class III Devices, till 2035

14.4.2.10. Medical Device Contract Manufacturing Market in Europe for Cardiovascular Disorders, till 2035

14.4.2.11. Medical Device Contract Manufacturing Market in Europe for CNS Disorders, till 2035

14.4.2.12. Medical Device Contract Manufacturing Market in Europe for Metabolic Disorders, till 2035

14.4.2.13. Medical Device Contract Manufacturing Market in Europe for Oncological Disorders, till 2035

14.4.2.14. Medical Device Contract Manufacturing Market in Europe for Orthopedic Disorders, till 2035

14.4.2.15. Medical Device Contract Manufacturing Market in Europe for Ophthalmic Disorders, till 2035

14.4.2.16. Medical Device Contract Manufacturing Market in Europe for Pain Disorders, till 2035

14.4.2.17. Medical Device Contract Manufacturing Market in Europe for Respiratory Disorders, till 2035

14.4.2.18. Medical Device Contract Manufacturing Market in Europe for Other Therapeutic Areas, till 2035

14.4.3. Medical Device Contract Manufacturing Market in Asia Pacific, till 2035

14.4.3.1. Medical Device Contract Manufacturing Market in China, till 2035

14.4.3.2. Medical Device Contract Manufacturing Market in Japan, till 2035

14.4.3.3. Medical Device Contract Manufacturing Market in India, till 2035

14.4.3.4. Medical Device Contract Manufacturing Market in Rest of Asia Pacific, till 2035

14.4.3.5. Medical Device Contract Manufacturing Market in Asia Pacific: Class I Devices, till 2035

14.4.3.6. Medical Device Contract Manufacturing Market in Asia Pacific: Class II Devices, till 2035

14.4.3.7. Medical Device Contract Manufacturing Market in Asia Pacific: Class III Devices, till 2035

14.4.3.8. Medical Device Contract Manufacturing Market in Asia Pacific for Cardiovascular Disorders, till 2035

14.4.3.9. Medical Device Contract Manufacturing Market in Asia Pacific for CNS Disorders, till 2035

14.4.3.10. Medical Device Contract Manufacturing Market in Asia Pacific for Metabolic Disorders, till 2035

14.4.3.11. Medical Device Contract Manufacturing Market in Asia Pacific for Oncological Disorders, till 2035

14.4.3.12. Medical Device Contract Manufacturing Market in Asia Pacific for Orthopedic Disorders, till 2035

14.4.3.13. Medical Device Contract Manufacturing Market in Asia Pacific for Ophthalmic Disorders, till 2035

14.4.3.14. Medical Device Contract Manufacturing Market in Asia Pacific for Pain Disorders, till 2035

14.4.3.15. Medical Device Contract Manufacturing Market in Asia Pacific for Respiratory Disorders, till 2035

14.4.3.16. Medical Device Contract Manufacturing Market in Asia Pacific for Other Therapeutic Areas, till 2035

14.4.4. Medical Device Contract Manufacturing Market in Rest of the World, till 2035

14.4.4.1. Medical Device Contract Manufacturing Market in Rest of the World: Class I Devices, till 2035

14.4.4.2. Medical Device Contract Manufacturing Market in Rest of the World: Class II Devices, till 2035

14.4.4.3. Medical Device Contract Manufacturing Market in Rest of the World: Class III Devices, till 2035

14.4.4.4. Medical Device Contract Manufacturing Market in Rest of the World for Cardiovascular Disorders, till 2035

14.4.4.5. Medical Device Contract Manufacturing Market in Rest of the World for CNS Disorders, till 2035

14.4.4.6. Medical Device Contract Manufacturing Market in Rest of the World for Metabolic Disorders, till 2035

14.4.4.7. Medical Device Contract Manufacturing Market in Rest of the World for Oncological Disorders, till 2035

14.4.4.8. Medical Device Contract Manufacturing Market in Rest of the World for Orthopedic Disorders, till 2035

14.4.4.9. Medical Device Contract Manufacturing Market in Rest of the World for Ophthalmic Disorders, till 2035

14.4.4.10. Medical Device Contract Manufacturing Market in Rest of the World for Pain Disorders, till 2035

14.4.4.11. Medical Device Contract Manufacturing Market in Rest of the World for Respiratory Disorders, till 2035

14.4.4.12. Medical Device Contract Manufacturing Market in Rest of the World for Other Therapeutic Areas, till 2035

15. SWOT ANALYSIS

15.1. Chapter Overview

15.2. Strengths

15.3. Weaknesses

15.4. Opportunities

15.5. Threats

15.6. Concluding Remarks

16. CONCLUSION

16.1. Chapter Overview

16.2. Key Takeaways

17. SURVEY / INTERVIEW TRANSCRIPTS

18. APPENDIX 1: TABULATED DATA

19. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS