실험실 자동화 시장 : 업계 동향과 세계 예측 - 자동화 단계별, 기기 유형별, 용도별, 최종사용자별, 주요 지역별

Lab Automation Market: Industry Trends and Global Forecasts - Distribution by Stage of Automation, Type of Instrument, Application, End-user and Key Geographical Regions

상품코드:1762524

리서치사:Roots Analysis

발행일:2025년 07월

페이지 정보:영문 231 Pages

라이선스 & 가격 (부가세 별도)

한글목차

실험실 자동화 시장 : 개요

세계의 실험실 자동화 시장 규모는 2035년까지의 예측 기간 중 9.4%의 CAGR로 확대하며, 현재 65억 달러에서 2035년까지 160억 달러로 성장할 것으로 예측됩니다.

시장 세분화에서는 시장 규모와 시장 기회를 다음과 같은 매개 변수로 구분합니다.

자동화 단계

분석 전 단계

분석 단계

사후 분석 단계

전체 실험실 자동화

장비 유형

자동 액체 처리 시스템

자동 마이크로플레이트 리더기

자동 샘플링 시스템

분석 장비

자동 저장 및 검색 시스템(ASRS)

기타

용도

진단

유전체 솔루션

미생물학

신약개발

단백질체학 솔루션

기타

최종사용자

제약-바이오 기업

연구-진단 실험실

기타

주요 지역

북미

유럽

아시아태평양

중동 및 북아프리카

라틴아메리카

실험실 자동화 시장 : 성장과 동향

실험실 자동화는 최근 수년간 진단 검사 과학에서 가장 중요한 동향 중 하나이며, 1950년대에 시작된 실험실 자동화의 목적은 실험실 검사의 인적 오류와 처리 시간을 줄이는 것입니다. 모든 실험실 프로세스 중 인적 오류는 분석 전 오류의 약 30%에서 86%를 차지한다는 점은 주목할 가치가 있습니다. 따라서 인간 대신 로봇을 도입하면 이 상당한 양의 부정확성을 효과적이고 즉각적으로 제거할 수 있습니다. 수년 동안 실험실 자동화는 연구자뿐만 아니라 업계 관계자들로부터 큰 관심을 받아왔습니다. 모든 연구 및 기술 분야에서 기계가 수작업을 대체할 수 있기 때문입니다. 자동화는 프로세스의 품질을 향상시키고, 인적 오류와 변수를 제거하여 궁극적으로 운영을 보다 비용 효율적이고, 효율적이며, 신속하게 처리할 수 있기 때문입니다.

또한 지난 10년간 실험실 자동화 개념이 발전한 속도를 감안할 때, 이 분야의 새로운 기술은 매우 큰 잠재력을 보여주고 있습니다. 실제로 많은 실험실 관리자들은 반복적인 작업을 간소화하고 효율성을 높이기 위한 수단으로 이동 로봇 분야를 모색하고 있습니다. 많은 과학자들이 연구실 내에서 재료를 독립적으로 운반하고 취급할 수 있는 로봇 실험실 도우미를 구상하고 있습니다. 자동 액체 처리 시스템과 같은 실험실 자동화 장비는 일관된 높은 정확도를 유지하면서 시료 전처리를 간소화하고, 실험실에서 수작업을 없애고, 반복성을 유지하면서 더 많은 시료를 처리할 수 있다는 장점이 있습니다. 또한 자동 보관 및 검색 시스템(ASRS)은 피킹, 보관, 조립, 재고 보충과 같은 작업에서 수작업이 필요 없기 때문에 업무의 변동 비용을 낮출 수 있습니다. 그 결과, 연구 노력 증가, 첨단 장비의 개발, 다양한 이해관계자들의 노력으로 이 분야의 산업은 향후 주목할 만한 성장을 보일 가능성이 높습니다.

실험실 자동화 시장 : 주요 인사이트

이 보고서는 실험실 자동화 시장의 현황을 조사하고 업계내 잠재적인 성장 기회를 파악합니다. 이 보고서의 주요 조사 결과는 다음과 같습니다.

실험실 자동화 시스템 제조업체의 90% 이상이 분석 전 단계 기반 기기에 집중하고 있습니다. 이 중 ALHS와 AAS는 제약회사 및 바이오테크놀러지 회사에서 널리 채택하고 있습니다.

경쟁 우위를 확보하기 위해 각 회사는 기존 역량을 적극적으로 강화하고, 제품 포트폴리오를 강화하며, 진화하는 업계 벤치마크를 준수하기 위해 노력하고 있습니다.

파트너십 활동은 약 25%의 연평균 복합 성장률(CAGR)로 증가하고 있습니다. 실제로 실험실 자동화 관련 가장 큰 거래는 지난 3년 동안 체결된 것으로 나타났습니다.

최근 6,200건 이상의 실험실 자동화 관련 특허가 출원/취득되었으며, 이는 확장 가능하고 구성 가능한 실험실 자동화 시스템에 대한 이해관계자들의 관심이 증가하고 있음을 강조합니다.

대부분의 실험실 자동화 소프트웨어 공급업체는 북미에 본사를 두고 있으며, 시장의 55% 이상은 소규모 업체가 차지하고 있습니다.

헬스케어 산업에서 실험실 자동화 도입이 증가함에 따라 실험실 자동화 소프트웨어 공급업체에게 수익성 있는 비즈니스 기회가 창출될 것으로 예측됩니다.

이 시장은 연간 9.4%의 성장률을 보일 것으로 예상되며, 기회는 다양한 유형의 장비, 지역, 자동화 단계, 최종사용자에 잘 분산될 것으로 보입니다.

실험실 자동화 시장 : 주요 부문

자동화 단계별로 시장은 분석 전 단계, 분석 단계, 분석 후 단계, 종합 실험실 자동화로 구분됩니다. 현재, 분석 전 단계 부문은 전 세계 실험실 자동화 시장에서 가장 큰 점유율을 차지하고 있습니다. 그러나 종합 실험실 자동화 부문은 예측 기간 중 가장 높은 시장 성장성을 보일 것으로 예측됩니다.

장비 유형별로 시장은 자동 액체 처리 시스템, 자동 마이크로플레이트 판독기, 자동 샘플링 시스템, 분석 장비, 자동 저장 및 검색 시스템(ASRS), 기타 장비로 구분됩니다. 현재 자동 액체 처리 시스템 부문은 전 세계 실험실 자동화 시장에서 가장 큰 점유율을 차지하고 있습니다. 또한 분석 장비 부문은 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

용도별로 시장은 진단, 유전체 솔루션, 미생물학, 신약개발, 단백질체학 솔루션, 기타 용도로 구분됩니다. 현재 진단 분야는 전 세계 실험실 자동화 시장에서 가장 높은 비중을 차지하고 있습니다. 또한 신약 개발 부문은 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

시장은 최종사용자별로 바이오 및 제약 산업, 연구 및 학술기관, 기타 최종사용자로 구분됩니다. 현재, 생명공학 및 제약 산업 부문은 세계 실험실 자동화 시장에서 가장 큰 점유율을 차지하고 있습니다. 그러나 기타 최종사용자 부문 시장은 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

주요 지역별로 시장은 북미, 유럽, 아시아태평양, 중동 및 북아프리카, 라틴아메리카로 구분됩니다. 현재 북미는 전 세계 실험실 자동화 시장에서 가장 큰 매출 점유율을 차지하고 있습니다. 또한 아시아태평양 시장은 향후 더 높은 CAGR로 성장할 가능성이 높습니다.

실험실 자동화 시장의 참여 기업 예

Abbott

Anton Paar

BD

Beckman Coulter

ERWEKA

Leuze

Ortho Clinical Diagnostics

Pall Corporation

PerkinElmer

Roche Diagnostics

Siemens Healthineers

SYSTAG

목차

제1장 서문

제2장 개요

제3장 서론

실험실 자동화의 개요

실험실 자동화의 역사적 진화

실험실 자동화의 단계

실험실 자동화의 프로세스

실험실 자동화가 수작업보다 우수한 점

실험실 자동화에 수반하는 과제

향후 전망

제4장 시장 구도

실험실 자동화 시스템 제조업체 : 시장 구도

제5장 기업 경쟁력 분석

제6장 기업 개요

Abbott

Anton Paar

BD

Beckman Coulter

ERWEKA

Leuze

Ortho Clinical Diagnostics

Pall Corporation

PerkinElmer

Roche Diagnostics

Siemens Healthineers

SYSTAG

제7장 사례 연구 : 실험실 자동화 소프트웨어

실험실 자동화 소프트웨어 프로바이더 : 시장 구도

제8장 파트너십과 협업

파트너십 모델

실험실 자동화 : 파트너십과 협업 리스트

제9장 특허 분석

제10장 시장 예측과 기회 분석

조사 방법과 주요 전제

2035년까지의 세계 실험실 자동화 시장

제11장 이그제큐티브 인사이트

제12장 부록 I : 표형식 데이터

제13장 부록 II : 기업 및 조직 리스트

KSA

영문 목차

영문목차

LAB AUTOMATION MARKET: OVERVIEW

As per Roots Analysis, the global lab automation market is estimated to grow from USD 6.5 billion in the current year to USD 16 billion by 2035, at a CAGR of 9.4% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Stage of Automation

Pre-Analytical Stage

Analytical Stage

Post-Analytical Stage

Total Lab Automation

Type of Instrument

Automated Liquid Handling Systems

Automated Microplate Readers

Automated Sampling Systems

Analyzers

Automated Storage and Retrieval Systems (ASRS)

Other Instruments

Application

Diagnostics

Genomic Solutions

Microbiology

Drug Discovery

Proteomic Solutions

Other Applications

End-user

Pharmaceutical and Biotechnology Companies

Research and Diagnostic Laboratories

Other End-users

Key Geographical Regions

North America

Europe

Asia-Pacific

Middle East and North Africa

Latin America

LAB AUTOMATION MARKET: GROWTH AND TRENDS

Laboratory automation has been one of the most significant developments in diagnostic laboratory sciences in recent years. The purpose of laboratory automation, which began in the 1950s, is to reduce human error and turnaround time for laboratory testing. It is worth highlighting that human error accounts for approximately 30% to 86% of all pre-analytical mistakes among all laboratory processes. As a result, the implementation of robots in place of humans can effectively and immediately eliminate this significant amount of inaccuracy. Over the years, lab automation has garnered significant interest from researchers as well as from industry players, owing to the potential of machines to replace manual operations in every field of research and technology. This is because automation enhances process quality, eliminates human error and variability, and eventually makes operations more cost-effective, efficient, and quick.

Further, given the rate at which the concept of lab automation has evolved over the last decade, new technologies in this domain have demonstrated enormous potential. In fact, many lab managers are exploring the field of mobile robots as a means to streamline repetitive tasks and enhance efficiency. A robotic lab assistant that can independently transport and handle materials in the lab has been conceptualized by many scientists. Lab automation devices, such as automated liquid handling systems, have several advantages, including the ability to simplify sample preparation while maintaining consistent high accuracy and allowing labs to free up manual labor and run more samples along with maintaining reproducibility. In addition, automated storage and retrieval systems (ASRS) lower down the variable cost of operations by eliminating the need for manual labor for tasks such as picking, storing, assembly and inventory replenishment. Consequently, owing to the growing research efforts, development of advanced instrumentations, and efforts of various stakeholders, this segment of industry is likely to witness noteworthy growth in the foreseen future.

LAB AUTOMATION MARKET: KEY INSIGHTS

The report delves into the current state of the lab automation market and identifies potential growth opportunities within industry. Some key findings from the report include:

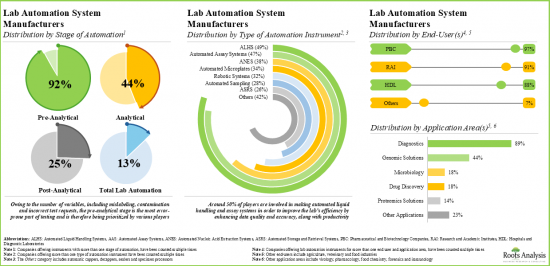

More than 90% of the lab automation system manufacturers are focusing on pre-analytical stage-based instruments; of these, ALHS and AAS have been more widely adopted by pharma and biotech companies.

In pursuit of gaining a competitive edge, companies are actively enhancing their existing capabilities to strengthen their respective product portfolios and drive compliance to evolving industry benchmarks.

The partnership activity has increased at a CAGR of around 25%; in fact, the maximum deals related to lab automation have been inked in the last three years.

More than 6,200 patents related to lab automation have been filed / granted recently, highlighting the growing interest of stakeholders in scalable and configurable lab automation systems.

Majority of the lab automation software providers are headquartered in North America; more than 55% of the market is captured by small players.

The increasing adoption of lab automation in the healthcare industry is anticipated to create profitable business opportunities for lab automation software providers.

The market is estimated to grow at an annualized rate of 9.4%; the opportunity is likely to be well distributed across various types of instruments, geographical regions, stages of automation and end-users.

LAB AUTOMATION MARKET: KEY SEGMENTS

Pre-analytical Stage Segment holds the Largest Share of the Lab Automation Market

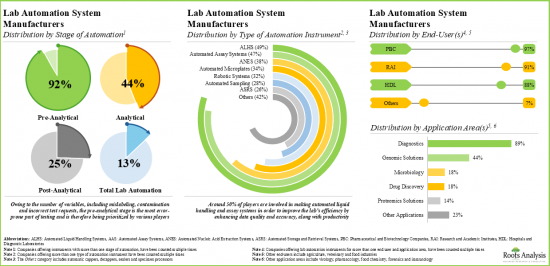

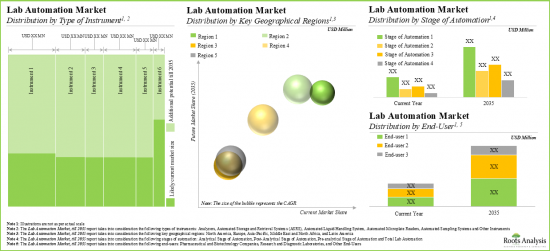

Based on the stage of automation, the market is segmented into pre-analytical stage, analytical stage, post-analytical stage and total lab automation. At present, the pre-analytical stage segment holds the maximum share of the global lab automation market. However, the total lab automation segment is expected to show the highest market growth potential during the forecast period.

By Type of Instrument, Analyzers is the Fastest Growing Segment of the Global Lab Automation Market

Based on the type of instrument, the market is segmented into automated liquid handling systems, automated microplate readers, automated sampling systems, analyzers, automated storage and retrieval systems (ASRS), and other instruments. At present, the automated liquid handling systems segment holds the maximum share of the global lab automation market. Further, the market for analyzers segment is expected to grow at a higher CAGR during the forecast period.

By Application, Diagnostics Segment Accounts for the Largest Share of the Global Lab Automation Market

Based on the application, the market is segmented into diagnostics, genomic solutions, microbiology, drug discovery, proteomic solutions and other applications. Currently, the diagnostics segment captures the highest proportion of the global lab automation market. Further, the drug discovery segment is expected to grow at a higher CAGR during the forecast period.

By End-user, Other End-users is the Fastest Growing Segment of the Global Lab Automation Market

Based on the end-user, the market is segmented into biotechnology and pharmaceutical industries, research and academic institutes and other end users. At present, the biotechnology and pharmaceutical industries segment holds the maximum share of the global lab automation market. However, the market for the other end-user segment is expected to grow at a higher CAGR during the forecast period.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia-Pacific, Middle East and North Africa, and Latin America. Currently, North America dominates the global lab automation market and accounts for the largest revenue share. Further, the market Asia-Pacific is likely to grow at a higher CAGR in the coming future.

Example Players in the Lab Automation Market

Abbott

Anton Paar

BD

Beckman Coulter

ERWEKA

Leuze

Ortho Clinical Diagnostics

Pall Corporation

PerkinElmer

Roche Diagnostics

Siemens Healthineers

SYSTAG

LYOPHILIZATION SERVICES MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global lyophilization services market, focusing on key market segments, including [A] stage of automation, [B] type of instrument, [C] application, [D] end-user and [E] key geographical regions.

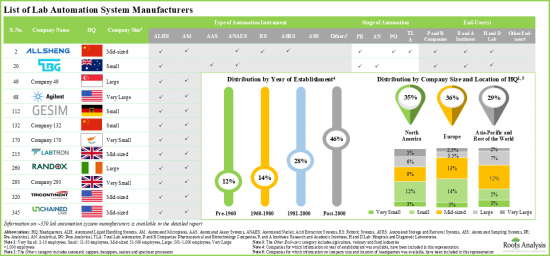

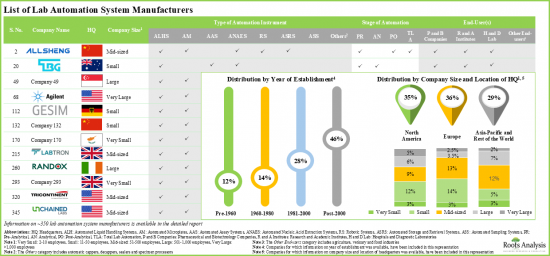

Market Landscape: A comprehensive evaluation of around 350 lab automation system manufacturers, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] types of lab automation system(s), [E] stage(s) of automation, [F] application area(s) and [G] end-user(s).

Company Competitiveness Analysis: A comprehensive competitive analysis of lab automation system manufacturers, examining factors, such as [A] company strength, [B] product diversity and [BC] portfolio strength.

Company Profiles: In-depth profiles of key players that are currently engaged in the development of lab automation systems across North America, Europe and Asia-Pacific and Rest of the World, focusing on [A] overview of the company, [B] financial information (if available), [C] product portfolio and [D] recent developments and an informed future outlook.

Partnerships and Collaborations: An insightful analysis of the deals inked by stakeholders in this domain, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D] type of automation instrument(s), [E] most active players (in terms of number of partnerships) and [F] regional distribution of partnership activity.

Patent Analysis: An in-depth analysis of patents filed / granted till date related to lab automation, based on various relevant parameters, such as [A] patent publication year, [B] type of patent, [C] patent jurisdiction, [D] CPC symbols, [E] type of applicant, [F] emerging focus areas and [G] leading players (in terms of number of patents filled / granted), [H] leading individual assignees, [I] benchmarking analysis and [J] patent valuation.

Case Study: A detailed discussion on the lab automation software providers, based on various parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] type of software, [E] mode(s) of deployment and [F] end-user(s).

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What factors are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary Excel Data Packs for all Analytical Modules in the Report

15% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

1.1. Scope of the Report

1.2. Research Methodology

1.2.1. Research Assumptions

1.2.2. Project Methodology

1.2.3. Forecast Methodology

1.2.4. Robust Quality Control

1.2.5. Key Considerations

1.2.5.1. Demographics

1.2.5.2. Economic Factors

1.2.5.3. Government Regulations

1.2.5.4. Supply Chain

1.2.5.5. COVID Impact / Related Factors

1.2.5.6. Market Access

1.2.5.7. Healthcare Policies

1.2.5.8. Industry Consolidation

1.3 Key Questions Answered

1.4. Chapter Outlines

2. EXECUTIVE SUMMARY

3. INTRODUCTION

3.1. Overview of Lab Automation

3.2. Historical Evolution of Lab Automation

3.3. Stages of Lab Automation

3.4. Process of Lab Automation

3.5. Advantages of Lab Automation Over Manual Handling

3.6. Challenges associated with Lab Automation

3.7. Future Perspectives

4. MARKET LANDSCAPE

4.1. Lab Automation System Manufacturers: Overall Market Landscape

4.1.1. Analysis by Year of Establishment

4.1.2. Analysis by Company Size

4.1.3. Analysis by Location of Headquarters

4.1.4. Analysis by Company Size and Location of Headquarters

4.1.5. Analysis by Type of Lab Automation System(s)

4.1.6. Analysis by Type of Automated Liquid Handler(s)

4.1.7. Analysis by Type of Automated Microplate(s)

4.1.8. Analysis by Stage(s) of Automation

4.1.9. Analysis by Application Area(s)

4.1.10. Analysis by Type of Lab Automation System(s) and Application Area(s)

4.1.11. Analysis by End-user(s)

4.1.12. Analysis by Stage(s) of Automation and End-user(s)

5. COMPANY COMPETITIVENESS ANALYSIS

5.1. Assumptions and Key Parameters

5.2. Methodology

5.3. Competitiveness Analysis: Very Small Companies based in North America (Peer Group I)

5.4. Competitiveness Analysis: Small Companies based in North America (Peer Group II)

5.5 Competitiveness Analysis: Mid-sized Players based in North America (Peer Group III)

5.6. Competitiveness Analysis: Large Companies based in North America (Peer Group IV)

5.7. Competitiveness Analysis: Very Large Companies based in North America (Peer Group V)

5.8 Competitiveness Analysis: Very Small Companies based in Europe (Peer Group VI)

5.9. Competitiveness Analysis: Small Companies based in Europe (Peer Group VII)

5.10. Competitiveness Analysis: Mid-sized Companies based in Europe (Peer Group VII)

5.11. Competitiveness Analysis: Large Companies based in Europe (Peer Group IX)

5.12. Competitiveness Analysis: Very Large Companies based in Europe (Peer Group X)

5.13. Competitiveness Analysis: Very Small Companies based in Asia-Pacific and Rest of the World (Peer Group XI)

5.14. Competitiveness Analysis: Small Companies based in Asia-Pacific and Rest of the World (Peer Group XII)

5.15. Competitiveness Analysis: Mid-sized Companies based in Asia-Pacific and Rest of the World (Peer Group XIII)

5.16. Competitiveness Analysis: Large Companies based in Asia-Pacific and Rest of the World (Peer Group XIV)

5.17. Competitiveness Analysis: Very Large Companies based in Asia-Pacific and Rest of the World (Peer Group XV)