단백질 공학 분야 실험실 자동화 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Lab Automation in Protein Engineering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640326

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

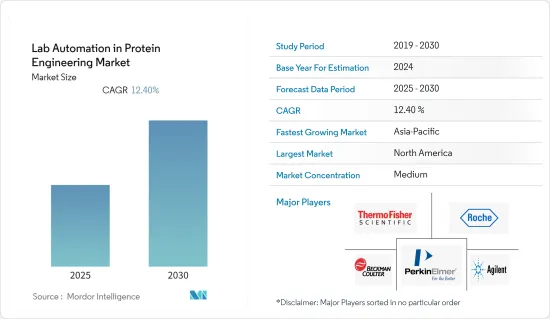

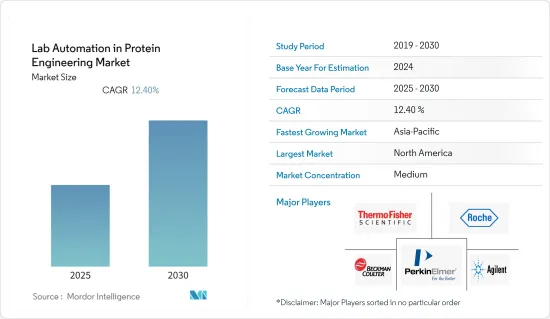

단백질 공학 분야 실험실 자동화 시장은 예측 기간 동안 CAGR 12.4%를 기록할 전망입니다.

주요 하이라이트

단백질 에너지 영양 실조(PEM)는 신흥국의 농촌 지역에서 증가하고 있으며 콰시오르코르, 마라스무스, 마라스무스-콰시오르코르 전환기를 포함한 질병 전체를 말합니다. 콰시오르코르의 발병률은 지역에 따라 다르며 미국에서는 꽤 드문 질병으로 중남미, 동남아시아, 콩고, 자메이카, 푸에르토리코, 남아프리카가 영향을 받고 있습니다. 그 결과, 단백질 결핍증의 빈도가 높아지고 있으며, 이는 시장 전체 수요를 밀어 올리고 있습니다.

헬스케어 사업은 단백질 공학 연구개발과 의식 향상 프로그램 스폰서 등 정부 이니셔티브 증가에 영향을 받고 있습니다. 정부는 몇 가지 연구 이니셔티브에 자금을 제공하고 있는데 예를 들어, Protein Technologies(PTL)는 획기적인 단백질 공학 연구를 위해 영국 정부의 기술 전략위원회(현재 혁신 UK)로부터 자금을 얻고 있습니다.

단백질 공학은 보다 우수한 기능을 가진 효소를 만들어 작물의 수율을 향상시키고 바이오연료의 생산을 용이하게 할 수 있기 때문에 농약 사업에서도 큰 가능성을 가지고 있습니다. 또한 미래의 요구를 충족시키는 데 필요한 농업 성과를 높이기 위한 기술로도 중요한 역할을 할 것으로 예상됩니다.

COVID-19가 발생한 이래, 연구소는 부지와 자원을 COVID-19 검사 시설로 바꾸어 자동화 장비의 사용을 늘리고 있습니다. 워싱턴 대학의 연구실이 그 첫 번째 예로 브로드 연구소가 임상 처리 실험실을 대규모 COVID-19 검사 시설로 전환한다고 발표한 후 전환되었습니다.

단백질 공학 분야 실험실 자동화 시장 동향

자동 액체 처리기 장비가 최대 시장 점유율을 차지

액체 핸들러는 일반적으로 생화학 및 화학 연구소에서 채택됩니다. 자동 액체 취급 로봇은 실험실에서 샘플 및 기타 액체를 분배하는 데 도움이 됩니다. 자동 액체 처리기는 운전 시간을 최소화하고 정확도를 극대화합니다. 또한, 액체 핸들러는 나노리터를 포함한 광범위한 용량 내에서 작동할 수 있으므로 분주 작업에 유용성이 입증되었습니다.

주요 기업은 자동 액체 핸들러 개발 벤치마크를 설정하고 생산성을 효과적으로 향상시키기 위한 프리미엄 제품 개발에 끊임없이 투자하고 있습니다. 미량의 액체를 처리할 수 있는 액체 핸들러의 진화는 시장에서 모듈식 실험실 자동화 시스템의 신속한 개척에 기여하고 있습니다.

Robotic Industries Association에 따르면 생명 과학 분야에서는 자동 액체 핸들러, 자동 플레이트 핸들러, 로봇 암 등 산업용 로봇에 대한 수요가 세 번째로 높은 성장을 보이고 있습니다.

Parker에 따르면, 생명 과학 로봇 동향 중 하나는 로봇 분석 장치에서 유체공학을 더 쉽게 이해할 수 있다는 점입니다. 이 동향은 임상 실험실이나 병원이 중요한 샘플을 다룰 때 장치가 멈추지 않는다는 점에 의해 발생합니다. 이전에는 분배 장치 끝에 바늘 50개가 장착되고 다수의 튜브를 사용했던 몇몇 로봇 시스템은 튜브를 필요로 하지 않고 고장 가능성을 줄이는 특수 밸브 매니폴드를 사용하게 되었습니다. 매니폴드는 누설 가능성을 최소화합니다.

북미가 가장 큰 시장 점유율을 차지

북미는 수년간 임상 연구의 선구자 자리를 지켜왔습니다. 이 지역에는 화이자, 노바티스, 글락소스미스클라인, J&J 등 주요 제약 회사가 있습니다. 또한 이 지역에는 개발업무 수탁기관(CRO)이 가장 집중되어 있습니다. 주요 CRO로는 Laboratory Corp. of America Holdings, IQVIA, Syneos Health, Parexel International Corp. 등이 있습니다. 업계 선도적인 회사의 존재와 FDA의 엄격한 규제로 인해 이 지역 시장 경쟁은 치열합니다. 경쟁사보다 우위를 차지하기 위해 이 지역의 유전체학 연구 기관은 실험실에 로봇 공학과 자동화를 채택하는 경향을 강화하고 있습니다.

유전체 산업은 특히 미국에서도 계속 성장하고 있으며 앞으로 수년 간 더 확대될 것으로 예상됩니다. 새로운 유전체 시퀀싱 기술의 가용성, 이미 확립된 건강 관리 인프라 및 노인 인구 증가가 수익 확대의 주요 요인이 되었습니다. 미국에서는 성장에 대한 대응과 효율화의 필요성으로 혈액센터가 전자동 워크웨이 시스템을 도입하여 혈액형 검사, 스크리닝, 감염증 검사를 실시하고 있습니다.

많은 기업들이 광범위한 R&D 능력을 통해 기술 혁신에 참여하고 있습니다. 자동화의 개별 영역은 정제, 단백질 공학, 화합물 합성, 생물학적 시험 및 마그나 모션 트랙을 갖춘 실험실 내 분석을 포함할 수 있습니다.

단백질 공학의 실험실 자동화 산업 개요

단백질 공학에서 실험실 자동화 시장은 다양한 크고 작은 기업이 많은 국가에 제품을 수출하고 있기 때문에 경쟁은 중간 정도입니다. 대기업이 채택하는 주요 전략은 개발 기술 진보, 파트너십, M&A입니다. 이 시장의 주요 기업으로는 Thermofisher Scientific, F. Hofman La Roche, Siemens Health Inners, Danaher, Parkin Elmer 등이 있습니다. 최근 시장 동향은 다음과 같습니다.

2023년 1월 - 선도적인 의료 기술 제공업체인 BD(벡턴 디킨슨 앤드 컴퍼니)는 BD 키에스트라 미생물 실험실 솔루션을 위한 새로운 로봇식 트럭 시스템을 전 세계적으로 발표했습니다. 이 시스템은 실험실 표본의 처리를 자동화하고 수작업을 줄일 수 있습니다. 새로운 BD 키에스트라 3세대 컴플리트 랩 자동화 시스템은 실험실의 특정 요구에 맞게 확장 가능하며, 유연하고 사용자 정의된 전체 실험실 자동화 구성으로 여러 BD 키에스트라 모듈을 연결할 수 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

밸류체인/서플라이체인 분석

업계의 매력도 - Porter's Five Forces 분석

신규 참가업체의 위협

구매자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

COVID-19의 업계에 대한 영향 평가

제5장 시장 역학

촉진요인

IoT에 의한 실험실의 디지털 전환의 동향 고조

방대한 데이터의 효율적 관리

억제요인

고액의 초기 설정 비용

제6장 시장 세분화

기기별

자동 액체 핸들러

자동 플레이트 핸들러

로봇 암

자동 보관 및 검색 시스템(AS/RS)

기타 기기

지역별

북미

유럽

아시아태평양

세계 기타 지역

제7장 경쟁 구도

기업 프로파일

Thermo Fisher Scientific Inc.

Danaher Corporation/Beckman Coulter

Hudson Robotics Inc.

Becton, Dickinson and Company

Synchron Lab Automation

Agilent Technologies Inc.

Siemens Healthineers AG

Tecan Group Ltd

Perkinelmer Inc.

Eli Lilly and Company

F. Hoffmann-La Roche Ltd

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

CSM

영문 목차

영문목차

The Lab Automation in Protein Engineering Market is expected to register a CAGR of 12.4% during the forecast period.

Key Highlights

Protein-energy malnutrition (PEM) is rising in emerging economies' rural communities. It refers to a collection of illnesses that includes kwashiorkor, marasmus, and marasmus-kwashiorkor transitional phases. As a result, the incidence of kwashiorkor varies by region. It is pretty uncommon in the United States. Central America, Southeast Asia, Congo, Jamaica, Puerto Rico, and South Africa are impacted. As a result, the rising frequency of protein-deficiency illnesses boosts total market demand.

The healthcare business has been affected by a growing number of government efforts, such as sponsoring R&D for protein engineering and awareness programs. As a result, the government is funding several research initiatives ahead of time. For example, Protein Technologies Ltd (PTL) obtained money from the UK government's Technology Strategy Board (now Innovate UK) for their ground-breaking protein engineering research.

Protein engineering also has great potential in the agrochemical business because it can lead to better-functioning enzymes, boost crop yields, or make biofuel production easier. It is also anticipated to play a vital role as a technique for achieving the higher agricultural outcomes required to satisfy future needs.

Since the outbreak of COVID-19, labs have been turning their premises and resources into COVID-19 testing facilities, increasing automation equipment use. The University of Washington's laboratories were the first to do so. The statement came after the Broad Institute announced that its clinical processing lab would be converted into a large-scale COVID-19 testing facility.

Lab Automation in Protein Engineering Market Trends

Automated Liquid Handler Equipment Accounted for the Largest Market Share

Liquid handlers are usually employed in biochemical and chemical laboratories. Automated liquid handling robots help in dispensing samples and other fluids in laboratories. Automated liquid handlers minimize run times and maximize accuracy. Moreover, liquid handlers can operate across a wide range of volumes, extending into nanolitres, thus proving their usefulness in dispensing operations.

Leading companies have set the benchmark for the development of automated liquid handlers and are constantly investing in developing premium products to increase productivity effectively. The evolution of liquid handlers, capable of handling minute volumes of liquids, has contributed to the rapid development of modular lab automation systems in the market.

According to the Robotic Industries Association, the life science sector has the third-highest growth in industrial robots, in terms of automated liquid handlers, automated plate handlers, robotic arms, and others, to meet the demand.

According to Parker, one of the trends in life science robotics is fluidics getting more straightforward in robotic analyzers. This trend arose because clinical laboratories and hospitals cannot afford an instrument to go down when critical samples are involved. Specific robotic systems that used to have 50 needles on the end of a dispensing unit and lots of tubing increasingly use special valve manifolds that eliminate the need for tubing and result in less chance of failure. The manifolds minimize the possibility of leakage.

North America Occupied the Largest Market Share

North America has been a pioneer in clinical research for years. This region is home to major pharmaceutical companies, like Pfizer, Novartis, GlaxoSmithKline, J&J, and Novartis. The part also has the highest concentration of contract research organizations (CROs). Some significant CROs are Laboratory Corp. of America Holdings, IQVIA, Syneos Health, and Parexel International Corp. Owing to the presence of all the major players in the industry and stringent FDA regulations; the market is very competitive in the region. To gain an advantage over competitors, the genomics research organizations in the area are increasingly adopting robotics and automation in labs.

The genomic industry, especially in the United States, is still growing and is expected to increase over the coming years. The availability of new genome sequencing technologies, well-established healthcare infrastructure, and the increasing geriatric population are significant contributing factors to revenue growth. In the United States, the need to accommodate growth and the drive to boost efficiency are priming blood centers to acquire fully automated walkaway systems to perform types and screens or test specimens for infectious diseases.

Many companies are involved in innovation due to their extensive R&D capabilities. Individual areas of automation can encompass purification, protein engineering, compound synthesis, biological testing, and analysis in the lab equipped with a Magnamotion track.

Lab Automation in Protein Engineering Industry Overview

The lab automation in protein engineering market is moderately competitive, owing to many small and big players exporting products to many countries. The key strategies adopted by the major players are technological advancement in development, partnerships, and merger and acquisition. Some of the major players in the market are Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, Siemens Healthineers, Danaher Corporation, and PerkinElmer. Some of the recent developments in the market are:

January 2023 - BD (Becton, Dickinson and Company), a leading medical technology provider, unveiled a new robotic track system for the BD Kiestra microbiology laboratory solution worldwide. This system automates the processing of lab specimens, which could help to cut down on manual labor. The new BD Kiestra 3rd Generation Complete Lab Automation System is expandable to fit the specific demands of labs and allows them to connect several BD Kiestra modules in a flexible and customized total lab automation configuration.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Value Chain/Supply Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of the COVID-19 Impact on the Industry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Trend of Digital Transformation for Laboratories with IoT

5.1.2 Effective Management of the Huge Amount of Data Generated

5.2 Market Restraints

5.2.1 Expensive Initial Setup

6 MARKET SEGMENTATION

6.1 By Equipment

6.1.1 Automated Liquid Handlers

6.1.2 Automated Plate Handlers

6.1.3 Robotic Arms

6.1.4 Automated Storage and Retrieval Systems (AS/RS)