플라스미드 DNA 제조 시장 : 사업 규모별, 플라스미드 DNA 등급별, 응용 분야별, 치료 분야별, 최종사용자별, 지역별 - 업계 동향과 세계 예측(- 2035년)

Plasmid DNA Manufacturing Market by Scale of Operation, Application Area, Therapeutic Area, and Geography : Industry Trends and Global Forecasts, Till 2035

상품코드:1682711

리서치사:Roots Analysis

발행일:2025년 03월

페이지 정보:영문 255 Pages

라이선스 & 가격 (부가세 별도)

한글목차

세계의 플라스미드 DNA 제조 시장 규모는 2035년까지 예측 기간 동안 14.85%의 연평균 복합 성장률(CAGR)로 확대되어 현재 1억 달러에서 2035년까지 5억 3,000만 달러로 성장할 것으로 예상됩니다.

첨단 치료제(ATMP) 연구개발 이니셔티브가 증가함에 따라 플라스미드 DNA 제조 분야는 크게 성장하고 있습니다. 플라스미드 DNA의 개발은 기존의 문제점을 극복하고 세포 및 유전자 치료제 개발, 핵산 백신 개발, 바이러스 벡터 제조 등 다양한 분야에서 플라스미드 DNA의 용도를 더욱 확대하는 것을 목표로 하고 있습니다. 그러나 플라스미드 DNA의 제조 공정에는 장비 및 시설의 유지보수, 고급 전문 지식의 필요성 등 여러 가지 비용이 많이 드는 문제점이 있기 때문에 제약업계의 일부 기업들은 플라스미드 DNA의 제조 업무를 유능한 전문 서비스 제공업체에 아웃소싱하고 있습니다. 아웃소싱하고 있습니다. 이러한 아웃소싱 추세에 따라 플라스미드 DNA 제조 역량을 제공하는 서비스 제공업체가 다수 등장하고 있습니다. 또한, 경쟁이 치열해짐에 따라 최첨단 공정 최적화 도구와 기술을 이용할 수 있는 것이 차별화 요소로 부상하고 있습니다. 이에 따라 많은 서비스 제공업체들이 전략적 인수를 통해 서비스 포트폴리오를 적극적으로 확장하고 있습니다. 시간이 지남에 따라 일부 플라스미드 DNA 서비스 제공업체들은 플라스미드 설계 및 엔지니어링에서 프로세스 개발 및 최적화에 이르기까지 엔드 투 엔드 서비스 역량을 개발했다고 주장하고 있습니다. 앞서 언급한 요인들을 고려할 때, 플라스미드 DNA 제조 시장은 향후 몇 년동안 급성장할 것으로 예상됩니다.

현재 70개 이상의 기업이 다양한 응용 분야에서 플라스미드 DNA에 대한 광범위한 서비스를 제공하고 있다고 주장하고 있습니다.

이해관계자의 50% 이상이 세포 및 유전자 치료제 개발자에게 GMP 등급의 플라스미드 DNA 제조 서비스를 제공합니다. 최근 파트너십의 움직임이 상당히 활발해졌으며, 올해 체결된 대부분의 거래는 플라스미드 DNA 개발 및 제조에 초점을 맞춘 것으로 나타났습니다. 이 분야에 대한 관심 증가는 지난 몇 년동안 보고된 인수 건수에도 반영되어 있습니다. 이러한 노력의 50% 이상이 포트폴리오를 추가하는 데 초점을 맞추었습니다. 전 세계 플라스미드 DNA 생산 설비는 다양한 지역에 분포되어 있지만, 그 중 45% 이상이 미국 제조 공장에 설치되어 있습니다. 세포치료제 및 유전자치료제 파이프라인의 확장, 핵산 도메인에 대한 투자 증가로 인해 플라스미드 DNA 제조 시장은 당분간 큰 성장을 이룰 것으로 예상됩니다.

세계의 플라스미드 DNA 제조 시장에 대해 조사했으며, 시장 개요와 함께 사업 규모별/플라스미드 DNA 등급별/응용 분야별/치료 분야별/최종사용자별/지역별 동향, 시장 진출기업 프로파일 등의 정보를 전해드립니다.

목차

제1장 서문

제2장 조사 방법

제3장 경제 및 기타 프로젝트 특유의 고려사항

제4장 주요 요약

제5장 서론

제6장 시장 구도

제7장 주요 인사이트

제8장 파트너십 및 협업

제9장 인수

제10장 용량 분석

제11장 기업 경쟁력 분석

제12장 기업 개요

제13장 수요 분석

제14장 시장에 대한 영향 분석 : 성장 촉진요인 및 억제요인, 기회, 과제

제15장 세계의 플라스미드 DNA 제조 시장

제16장 플라스미드 DNA 제조 시장, 사업 규모별

제17장 플라스미드 DNA 제조 시장, 플라스미드 DNA 등급별

제18장 플라스미드 DNA 제조 시장, 응용 분야별

제19장 플라스미드 DNA 제조 시장, 치료 분야별

제20장 플라스미드 DNA 제조 시장, 최종사용자별

제21장 플라스미드 DNA 제조 시장, 지역별

제22장 결론

제23장 주요 인사이트

제24장 부록 I : 표 형식 데이터

제25장 부록 II : 기업 및 단체 리스트

LSH

영문 목차

영문목차

PLASMID DNA MANUFACTURING MARKET: OVERVIEW

As per Roots Analysis, the global plasmid DNA manufacturing market is estimated to grow from USD 0.1 billion in the current year to USD 0.53 billion by 2035, at a CAGR of 14.85% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Scale of Operation

Commercial

Clinical

Preclinical

Application Area

Cell Therapy Manufacturing

Gene Therapy Manufacturing

DNA / RNA Vaccine Development

Viral Vector Manufacturing

Other Application Areas

Therapeutic Area

Metabolic Disorders

Neurological Disorders

Oncological Disorders

Rare Disorders

Other Disorders

Key Geographical Regions

North America

Europe

Asia

Latin America

Middle East and North Africa

Rest of the World

PLASMID DNA MANUFACTURING MARKET: GROWTH AND TRENDS

Owing to the increasing research and development initiatives for advanced therapeutics medicinal products (ATMPs), the field of plasmid DNA manufacturing is experiencing extensive growth. Ongoing efforts for plasmid DNA aim to overcome existing challenges and further expand the applications of plasmid DNA in various fields, including cell and gene therapy development, nucleic acid vaccine development and viral vector manufacturing. However, due to various challenges associated with plasmid DNA manufacturing process, including the high cost of instruments, equipment maintenance and the requirement of high-end expertise, several players in the pharmaceutical industry are outsourcing their plasmid DNA manufacturing operations to capable, specialty service providers. This outsourcing trend has resulted in the emergence of several service providers offering plasmid DNA manufacturing capabilities. Further, amidst the growing competition, the availability of cutting-edge process optimization tools and technologies has emerged as a differentiating factor. This has led many service providers to actively expand their service portfolios through strategic acquisitions. Over time, several plasmid DNA service providers claim to have developed end-to-end service capabilities, ranging from plasmid design and engineering to process development and optimization. Considering the aforementioned factors, it is anticipated that the plasmid DNA manufacturing market is likely to witness rapid growth over the next few years.

PLASMID DNA MANUFACTURING MARKET: KEY INSIGHTS

The report delves into the current state of the plasmid DNA manufacturing market and identifies potential growth opportunities within the industry. Some key findings from the report include:

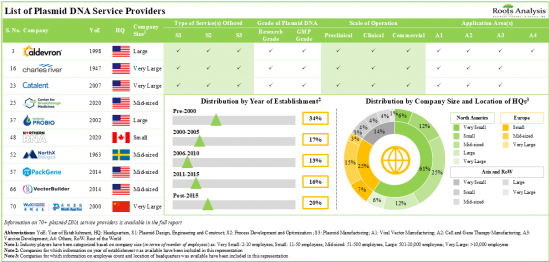

1. Presently, over 70 players claim to offer a wide range of services for plasmid DNA across various application areas; majority of such firms are headquartered in North America.

2. More than 50% of the stakeholders provide GMP grade plasmid DNA manufacturing services to cell and gene therapy developers.

3. A considerable increase in partnership activity has been observed in recent years; majority of the deals inked in the current year were focused on plasmid DNA development and manufacturing.

4. The rising interest in this domain is reflected by the number of acquisitions reported in the last few years; more than 50% of such initiatives were focused on portfolio addition.

5. The global installed plasmid DNA manufacturing capacity is spread across various geographies; over 45% of this capacity is installed in the production plants located in the US.

6. Driven by the expanding pipeline of cell and gene therapies, and increasing investments in nucleic acid domain, the market for plasmid DNA manufacturing is poised to witness significant growth in the foreseeable future.

7. The plasmid DNA manufacturing market is likely to grow at a CAGR of ~15% over the next 12 years, primarily driven by the revenues generated from plasmid DNA-based therapeutics intended for oncological disorders.

PLASMID DNA MANUFACTURING MARKET: KEY SEGMENTS

Clinical Operations Occupy the Largest Share of the Plasmid DNA Manufacturing Market

Based on the scale of operation, the market is segmented into preclinical, clinical and commercial scale. Whilst at present, the clinical scale holds the maximum share of the overall market, it is worth highlighting that the plasmid DNA manufacturing market at commercial scale is likely to grow at a relatively higher CAGR.

GMP Grade Plasmid DNA is Likely to Dominate the Plasmid DNA Manufacturing Market

Based on the grade of plasmid DNA, the market is segmented into GMP grade plasmid DNA, research grade plasmid DNA and high quality plasmid DNA. At present, GMP grade plasmid DNA captures the highest share of the plasmid DNA manufacturing market. This trend is unlikely to change in the near future.

DNA Vaccine Development is the Fastest Growing Segment of the Plasmid DNA Manufacturing Market During the Forecast Period

Based on the application area, the market is segmented into cell therapy manufacturing, gene therapy manufacturing, DNA / RNA vaccine development, viral vector manufacturing, and other application areas. It is worth highlighting that, at present, gene therapy manufacturing holds a larger share of the plasmid DNA manufacturing market. However, the plasmid DNA manufacturing market for DNA vaccine development is likely to grow at a relatively higher CAGR.

Oncological Disorders Occupy the Largest Share of the Plasmid DNA Manufacturing Market

Based on the therapeutic areas, the market is segmented into metabolic disorders, neurological disorders, oncological disorders, rare disorders, and other disorders. It is worth highlighting that the majority of the current plasmid DNA manufacturing market is captured by oncological disorders. This can be attributed to the growing incidence of oncological disorders, globally, which necessitate the development and production of effective treatments, including cell and gene therapies, and plasmid DNA based vaccines.

Pharma and Biotech Companies are Likely to Dominate the Plasmid DNA Manufacturing Market During the Forecast Period

Based on the end-users, the market is segmented into pharma and biotech companies, academic and research institutes, and other end users. At present, pharma and biotech companies hold the maximum share of the plasmid DNA manufacturing market. This trend is unlikely to change in the near future.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the Rest of the World. The majority of the share is expected to be captured by players based in North America. This is likely to remain the same in the forthcoming years.

Example Players in the Plasmid DNA Manufacturing Market

AGC Biologics

Aldevron

Biomay

Catalent Pharma Solutions

Charles River

Cytovance Biologics

Forge Biologics

GenScript ProBio

Thermo Fisher Scientific

VGXI

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

Chief Executive Officer and Co-Founder, Small Company, Slovenia

Senior Director, Large Company, USA

Business Development Manager, Mid-sized Company, Spain

Client Engagement Manager, Mid-sized Company, US

PLASMID DNA MANUFACTURING MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the plasmid DNA manufacturing market, focusing on key market segments, including [A] scale of operation, [B] grade of plasmid DNA, [C] application area, [D] therapeutic area, [E] end user and [F] key geographical regions.

Market Landscape: A comprehensive evaluation of plasmid DNA manufacturing service providers, considering various parameters, such as [A] year of establishment, [B] company size (in terms of the number of employees), [C] location of headquarters, [D] type of company, [E] type of venture, [F] type of service(s) offered, [G] location of manufacturing facility, [H] key offerings, [I] grade of plasmid DNA, [J] scale of operation and [K] application area(s).

Key Insights: An insightful analysis, highlighting the contemporary market trends in the plasmid DNA manufacturing market through different representations, based on relevant parameters, such as [A] company size and location of headquarters; [B] company size and type of venture; [C] key offerings and location of headquarters; [D] scale of operation and company size; [E] grade of plasmid DNA and application area(s); [F] scale of operation, application area(s) and location of manufacturing facility.

Company Competitiveness Analysis: A comprehensive competitive analysis of pDNA manufacturing service providers, examining factors, such as supplier strength, their respective capabilities and partnership activity.

Company Profiles: In-depth profiles of key industry players offering plasmid manufacturing services, focusing on [A] company overviews, [B] financial information (if available), [C] recent developments and [D] an informed future outlook.

Partnerships and Collaborations: An analysis of partnerships established in this sector, covering manufacturing and supply agreements, product development and manufacturing agreements, technology utilization agreements, service alliances, and product development agreements.

Acquisitions: An analysis of acquisitions reported in this sector, since 2015, based on multiple parameters, such as [A] year of acquisition, [B] type of acquisition, [C] geographical location, [D] company size and ownership of the companies involved, [E] key value drivers, and [F] acquisition deal multiples (based on revenues).

Capacity Analysis: Estimation of global pDNA manufacturing capacity, derived from data provided by various stakeholders in the public domain. This analysis emphasizes the distribution of the available capacity on the basis of [A] company size (very small, small, mid-sized, large and very large), [B] grade of plasmid DNA (research grade plasmid DNA, and GMP grade plasmid DNA), [C] scale of operation (pre-commercial and commercial), and [D] location of manufacturing facility (North America, Europe, Asia and rest of the world).

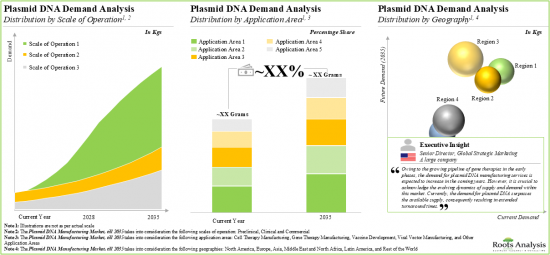

Demand Analysis: Informed estimates of the annual demand for plasmid DNA based on several relevant parameters, such as [A] scale of operation, [B] application area, and [C] geography. This analysis includes target patient population, dosing frequency and dose strength.

Market Impact Analysis: The report analyzes various factors such as drivers, restraints, opportunities, and challenges affecting the market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What kind of partnership models are commonly adopted by industry stakeholders?

What is the current annual demand for plasmid DNA?

What are the factors that are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary PPT Insights Packs

Complimentary Excel Data Packs for all Analytical Modules in the Report

10% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

1.1. Introduction

1.2. Project Objectives

1.3. Scope of the Report

1.4. Inclusions and Exclusions

1.5. Key Questions Answered

1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

2.1. Chapter Overview

2.2. Research Assumptions

2.3. Project Methodology

2.4. Forecast Methodology

2.5. Robust Quality Control

2.6. Key Considerations

2.6.1. Demographics

2.6.2. Economic Factors

2.6.3. Government Regulations

2.6.4. Supply Chain

2.6.5. COVID Impact / Related Factors

2.6.6. Market Access

2.6.7. Healthcare Policies

2.6.8. Industry Consolidation

2.7. Key Market Segmentations

3.ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

3.1. Chapter Overview

3.2. Market Dynamics

3.2.1. Time Period

3.2.1.1. Historical Trends

3.2.1.2. Current and Forecasted Estimates

3.2.2. Currency Coverage

3.2.2.1. Major Currencies Affecting the Market

3.2.2.2. Impact of Currency Fluctuations on the Industry

3.2.3. Foreign Exchange Impact

3.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

3.2.3.2. Strategies for Mitigating Foreign Exchange Risk

3.2.4. Recession

3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

3.2.5. Inflation

3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

3.2.5.2. Potential Impact of Inflation on the Market Evolution

4. EXECUTIVE SUMMARY

4.1. Chapter Overview

5. INTRODUCTION

5.1. Chapter Overview

5.2. Overview of Plasmids

5.2.1. Structure of a Plasmid DNA

5.3. Types of Plasmids (By Function)

5.3.1. Fertility Plasmids

5.3.2. Resistance Plasmids

5.3.3. Virulence Plasmids

5.3.4. Degradative Plasmids

5.3.5. Col Plasmids

5.4. Plasmid DNA Manufacturing

5.4.1. Steps Involved in Plasmid DNA Manufacturing

5.5. Applications of Plasmid DNA in Pharmaceutical Industry

5.5.1. Cell and Gene Therapy Manufacturing

5.5.2. Viral Vector Manufacturing

5.5.3. Vaccine Development

5.5.4. Other Research Applications

5.6. Challenges Associated with Plasmid DNA Manufacturing

5.7. Need for Outsourcing Plasmid DNA Manufacturing

5.8. Future Perspectives

6. OVERALL MARKET LANDSCAPE

6.1. Chapter Overview

6.2. Plasmid DNA Service Providers: Overall Market Landscape

6.2.1. Analysis by Year of Establishment

6.2.2. Analysis by Company Size

6.2.3. Analysis by Location of Headquarters

6.2.4. Analysis by Type of Company

6.2.5. Analysis by Type of Venture

6.2.6. Analysis by Type of Service(s) Offered

6.2.7. Analysis by Location of Manufacturing Facility

6.2.8. Analysis by Key Offerings

6.2.9. Analysis by Grade of Plasmid DNA

6.2.10. Analysis by Scale of Operation

6.2.11. Analysis by Application Area(s)

7. KEY INSIGHTS

7.1. Chapter Overview

7.2. Plasmid DNA Service Providers: Key Insights

7.2.1. Analysis by Company Size and Location of Headquarters

7.2.2. Analysis by Year of Establishment and Type of Venture

7.2.3. Analysis by Key Offerings and Location of Headquarters

7.2.4. Analysis by Scale of Operation and Company Size

7.2.5. Analysis by Grade of Plasmid DNA and Application Area(s)

7.2.6. Analysis by Scale of Operation, Application Area(s) and Location of Manufacturing Facility

8. PARTNERSHIPS AND COLLABORATIONS

8.1. Chapter Overview

8.2. Partnership Models

8.3. Plasmid DNA Services: Partnerships and Collaborations

8.3.1. Analysis by Year of Partnership

8.3.2. Analysis by Type of Partnership

8.3.3. Analysis by Year and Type of Partnership

8.3.4. Analysis by Type of Partner

8.3.5. Analysis by Type of Partnership and Type of Partner

8.3.6. Analysis by Grade of Plasmid DNA

8.3.7. Analysis by Scale of Operation

8.3.8. Analysis by Geography

8.3.8.1. Local and International Agreements

8.3.8.2. Intercontinental and Intracontinental Agreements

8.3.9. Most Active Players: Analysis by Number of Partnerships

9. ACQUISITIONS

9.1. Chapter Overview

9.2. Acquisitions Models

9.3. Plasmid DNA Services Providers: Acquisitions

9.3.1. Analysis by Year of Acquisition

9.3.2. Analysis by Type of Acquisition

9.3.3. Analysis by Geography

9.3.3.1. Local and International Acquisitions

9.3.3.2. Intercontinental and Intracontinental Acquisitions