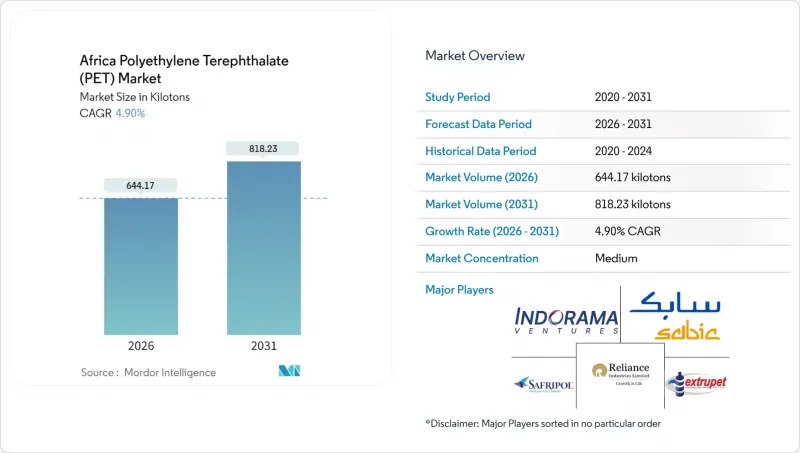

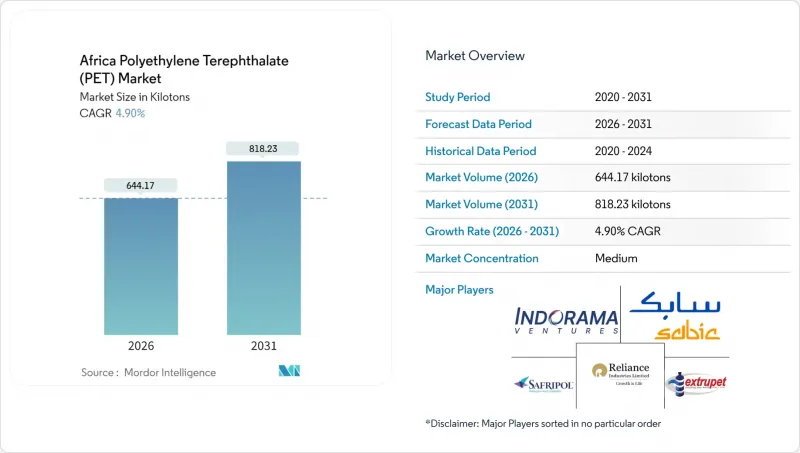

아프리카의 폴리에틸렌 테레프탈레이트(PET) 시장 규모는 2026년에 644.17 킬로톤으로 추정되고 있습니다.

이는 2025년 614.08 킬로톤으로부터 성장하며, 2031년에는 818.23 킬로톤에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 4.9%로 성장할 전망입니다.

지속적인 중산층 성장, 아프리카 대륙자유무역지대(AfCFTA)의 관세 조화, 현지 보틀링 능력의 확대가 수요를 견인하는 주요 요인입니다. 브랜드 소유주들은 투명성, 강도 대 중량비, 기존 충진 라인과의 친화성 때문에 PET를 선호하고 있으며, 생산자책임규제가 강화됨에 따라 재생등급에 대한 수요도 확대되고 있습니다. 다국적 소비재 제조업체(FMCG)는 현지 생산 거점을 지속적으로 구축하여 공급 균형을 수입 의존에서 지역 수지 공장 중심으로 전환하고 있습니다. 공공 부문 대출은 순환경제 목표에 따라 대규모 블루론과 그린본드를 통합 회수 및 재활용 인프라로 유도하고 있습니다. 그러나 원유 연동 원재료 가격 변동과 바이오 대체품에 대한 소비자의 관심은 전략적 불확실성을 야기하고 있으며, 민첩한 조달 전략과 제품 혁신을 요구하고 있습니다.

도시 지역의 급격한 소득 증가가 탄산음료, 생수, 기능성 음료 수요를 견인하고 있습니다. 코카콜라 HBC는 나이지리아에 10억 달러를 투자해 생산능력을 확충하고, 코카콜라 비버리지스 아프리카는 2024년 나미비아에 5,000만 달러 규모의 보틀링 라인을 개설할 예정입니다. 생산량 증가는 프리폼과 캡의 대형 오프 테이크 계약으로 이어져 버진 수지의 안정적인 수요를 보장합니다. 소비 확대에 따라 미비한 폐기물 처리 시스템에 부하가 걸리면서 라고스, 아크라 등의 도시에서는 생산자 부담금에 의한 보증금 반환 제도의 시범 도입이 진행되고 있습니다. 음료 제조업체는 캡 성형, 스트레치 블로우 성형, 충진 라인의 집적화를 통해 운송 비용 절감과 리드타임 단축을 도모하고 있습니다. 충진량 증가로 단위당 포장비용이 압축되어 PET는 유리나 알루미늄에 비해 가격 경쟁력을 유지하고 있습니다.

케냐의 2024년 확대 생산자 책임(EPR) 규정은 수입품 1개당 150 케냐 실링의 과징금을 부과하고, 브랜드 등록을 의무화함으로써 재활용 소재 사용에 대한 명확한 인센티브를 제공합니다. 남아공의 EPR 프레임워크(2021년 시행)는 회수 및 처리량에 대한 연례 보고를 요구하고 있습니다. 나이지리아 규제 당국도 유사한 규정을 마련 중이며, 인프라가 마련되는 대로 최소 재생재 함량 비율을 단계적으로 도입할 예정입니다. 펩시콜라 아프리카는 현재 전체 음료 라인에서 재생 폴리에스테르(rPET)를 20% 함유하는 것을 목표로 하고 있으며, 지역적 조달 계약의 토대를 마련하고 있습니다. 높은 rPET 비율을 인증받은 기업은 새로운 에코라벨 제도에 따라 매장에서의 가시성 향상이라는 이점을 얻을 수 있습니다. 그러나 효과적인 시행을 위해서는 비공식 수집업자의 정규화와 세척 및 고체상 중축합(SSP) 장치를 식품 등급 표준으로 업그레이드하는 것이 필수적입니다.

바이오 포장을 채택한 세계 식품 및 음료 신제품은 2019-2024년 연간 60% 증가했습니다. 유럽연합(EU) 규정은 특정 생분해성 폴리머를 재활용할 수 있는 것으로 인정하고 있으며, 이는 아프리카 정책 입안자들이 모방할 수 있는 규제 선례가 될 수 있습니다. 각 브랜드는 퇴비화 가능한 커피 캡슐과 전분 기반 냄비를 시험적으로 도입하여 틈새 분야에서 PET 사용량에 대한 압력을 가하고 있습니다. 재생 PET는 일반적으로 버진 소재보다 톤당 150달러 더 비싸게 거래되므로 장기적으로 비용 균형을 달성할 수 있다면 바이오 솔루션의 시범 도입에 대한 의지가 높아질 수 있습니다. 그러나 원료 물류, 특수 압출 설비, 산업용 퇴비화 시설의 부족으로 인해 아프리카에서 바이오폴리머 공급 확대는 여전히 복잡한 과제입니다.

2025년, 버진 PET는 아프리카 폴리에틸렌 테레프탈레이트(PET) 시장 점유율의 82.78%를 차지했습니다. 이는 컨버터가 안정적인 고유 점도와 광범위한 식품 등급 인증을 중시하기 때문입니다. 이 부문은 성숙한 수입 경로, 원자재에 대한 관세 우대, 풍부한 프리폼 변환 능력의 혜택을 누리고 있습니다. 병에서 병으로 재생 PET(rPET)는 고품질 플레이크 생산을 위해 특수한 고온 세척 라인과 SSP 라인이 필요하며, 현재 이를 가동하고 있는 공장이 극소수이기 때문에 공급에 제약이 있습니다.

재활용 PET는 EPR 규제와 음료 대기업의 자발적 서약(경영진 보상을 순환형 포장 달성 목표에 연동)에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 7.85%로 확대될 것으로 예측됩니다. 국제금융공사(IFC)의 융자 지원으로 새로운 세척 라인과 SSP의 병목현상 해소를 지원하는 한편, 사슬 연장 첨가제를 통해 투명성을 손상시키지 않고 고유점도를 회복할 수 있게 되었습니다. 이러한 투자 확대에 따라 아프리카의 재생 폴리에틸렌 테레프탈레이트(PET) 시장 규모는 2020년대 말까지 두 자릿수 점유율을 기록할 것으로 예측됩니다. 그러나 베일 공급, 규제 일관성, 신용 시장이 마련되고 대규모 재생 PET(rPET) 통합의 리스크가 줄어들기 전까지는 버진 수지가 주류가 될 것입니다.

아프리카 폴리에틸렌 테레프탈레이트(PET) 시장 보고서는 원료 유형별(버진 PET, 재생 PET), 최종사용자 산업별(자동차, 건축/건설, 전기/전자, 산업/기계, 포장, 기타 최종사용자 산업), 지역별(나이지리아, 남아프리카, 기타 아프리카 국가) 등으로 분류됩니다. )로 분류되어 있습니다. 시장 예측은 톤과 금액(USD)으로 제공됩니다.

Africa Polyethylene Terephthalate (PET) market size in 2026 is estimated at 644.17 kilotons, growing from 2025 value of 614.08 kilotons with 2031 projections showing 818.23 kilotons, growing at 4.9% CAGR over 2026-2031.

Sustained middle-class growth, tariff harmonization under the African Continental Free Trade Area (AfCFTA), and expanding local bottling capacity are the primary forces lifting demand. Brand owners favor PET for its clarity, strength-to-weight ratio, and familiarity in existing filling lines, while recycled grades gain momentum as producer responsibility rules tighten. Multinational fast-moving consumer goods (FMCG) players continue to build localized production hubs, shifting the supply balance away from imports and toward regional resin plants. Public-sector lending taps into circular economy objectives, directing large-scale blue-loans and green-bonds toward integrated collection and recycling infrastructure. Nonetheless, oil-linked feedstock swings and consumer interest in bio-based alternatives create strategic uncertainty that requires agile sourcing strategies and product innovation.

Rapid income gains across urban hubs propel demand for carbonated drinks, bottled water, and functional beverages. Coca-Cola HBC has earmarked USD 1 billion for Nigerian capacity additions, while Coca-Cola Beverages Africa opened a USD 50 million bottling line in Namibia in 2024. Higher throughput translates into larger off-take contracts for preforms and caps, locking in steady offtake for virgin resin. Growing consumption stresses underdeveloped waste systems, prompting cities such as Lagos and Accra to pilot deposit-return schemes funded by producer levies. Beverage converters respond by co-locating closure injection, stretch-blow, and filling lines, reducing freight cost and cutting lead times. Rising fill volumes compress per-unit packaging costs, preserving PET's price competitiveness against glass and aluminum.

Kenya's 2024 Extended Producer Responsibility (EPR) regulations impose KES 150 per imported item and require brand registration, creating explicit incentives for recycled content. South Africa's EPR framework, live since 2021, demands annual reporting on collected and processed volumes. Nigeria's regulator is drafting similar rules that will phase in minimum recycled content thresholds once infrastructure matures. PepsiCo Sub-Saharan Africa now targets 20% rPET inclusion across its beverage lines, setting an anchor for regional offtake contracts. Firms that certify higher rPET ratios gain shelf visibility advantages under emerging eco-labeling schemes. Effective enforcement, however, hinges on formalizing informal collectors and upgrading washing and solid-state polycondensation (SSP) units to food-grade standards.

Global food and beverage launches featuring bio-based packaging rose 60% annually between 2019 and 2024. European Union rules recognize certain biodegradable polymers as recyclable, creating a regulatory precedent that African policymakers may emulate. Brands test compostable coffee-capsules and starch-based pots, pressuring PET volumes in niche segments. Recycled PET often trades USD 150 per tonne above virgin, widening the motivation to test bio-based solutions if long-run cost parity can be achieved. Scaling biopolymer supply in Africa remains complex because feedstock logistics, specialized extrusion equipment, and industrial composting sites are still limited.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Virgin PET secured 82.78% of the Africa Polyethylene Terephthalate (PET) market share in 2025 because converters prize its consistent intrinsic viscosity and broad food-grade approvals. The segment benefits from mature import corridors, duty concessions on raw materials, and plentiful preform conversion capacity. Bottle-to-bottle rPET remains supply-constrained as high-grade flake requires specialized hot-wash and SSP lines that only a handful of plants operate today.

Recycled PET is advancing at an 7.85% CAGR to 2031, propelled by EPR regulations and voluntary pledges from beverage majors that link executive remuneration to circular-packaging milestones. International Finance Corporation loans underwrite new wash lines and SSP debottlenecking, while chain-extension additives now restore intrinsic viscosity without compromising clarity. As these investments scale, the Africa Polyethylene Terephthalate (PET) market size for recycled grades could reach meaningful double-digit share by the end of the decade. Still, virgin resin will dominate until bale supply, regulatory coherence, and credit markets align to de-risk full-scale rPET integration.

The Africa Polyethylene Terephthalate (PET) Market Report is Segmented by Source Type (Virgin PET, Recycled PET), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, Other End-User Industries), and Geography (Nigeria, South Africa, Rest of Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).