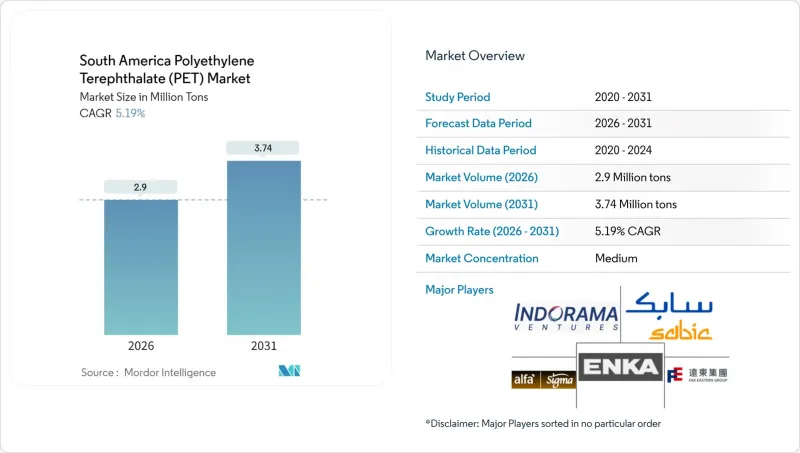

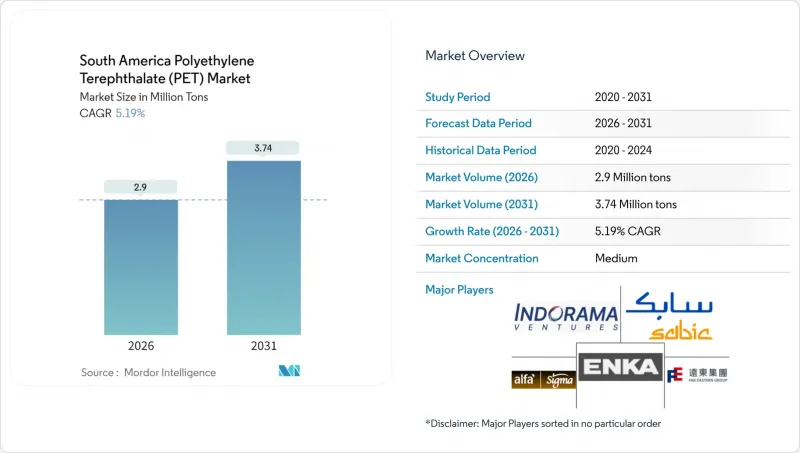

남미의 폴리에틸렌 테레프탈레이트(PET) 시장 규모는 2026년에 290만 톤에 달할 것으로 예측되고 있습니다.

이는 2025년 276만 톤으로부터 성장한 수치이며, 2031년에는 374만 톤에 달할 것으로 전망되고 있습니다. 2026-2031년의 연평균 성장률(CAGR)은 5.19%에 달할 전망입니다.

이러한 성장 곡선은 브라질의 수입 대체로의 결정적인 전환, 재활용 소재 사용 의무화 규제, 소비재 대기업의 니어쇼어링(near-shoring) 움직임이 결합되어 이 지역의 PET 수요를 지원하고 있다는 것을 보여줍니다. 산토스항과 파라나과항의 항만 혼잡은 단기적으로 수입 물류의 발목을 잡는 한편, 컨버터 업체들이 빠른 납기를 보장할 수 있는 현지 수지 공급업체를 우선적으로 선택하도록 유도하고 있으며, 이로 인해 국내 투자 모멘텀이 강화되고 있습니다. 코카콜라의 70억 헤알 규모의 14개 라인 증설 등 적극적인 생산능력 확대와 재활용 분야의 민관 협력으로 공급 옵션이 확대되어 원유 연동 원재료 가격 변동 리스크가 완화되고 있습니다. 경쟁의 강도는 여전히 중간 정도이며, 기존 다국적 기업은 수직적 통합을 활용하는 반면, 신생 재활용 기업은 회수 네트워크의 확대와 기술 라이선스 제공을 통해 점유율을 확보하고 있습니다.

국가 고형 폐기물 정책에 따라 2026년부터 폐쇄형 재활용이 법적으로 의무화되며, 음료 충전업체는 모든 병의 회수 및 재가공을 증명해야 합니다. 브라질은 2024년 41만 톤의 PET를 재활용하여 2022년 대비 14% 증가했으나, 여전히 규제 준수에 필요한 양에는 미치지 못했습니다. 메르코수르 지역내 통일된 식품용 재생 PET(rPET) 표준을 통해 생산자는 원료를 국경을 넘어 이동할 수 있으며, 운송 비용 절감과 등급 균일성 향상을 도모할 수 있습니다. 공급망에서는 폐기물을 전략적 자산으로 인식하고, 수거 경로를 대도시권에서 병입 청량음료의 보급이 활발한 농업 지역으로 확대하고 있습니다. 광학 선별기 및 고점도 압출 시스템에 대한 투자가 빠르게 확대되고 있으며, 여러 시설에서 이미 미국 FDA의 동등성 감사에 따라 식품 접촉 승인을 획득했습니다. 역물류 보고 의무화에 따라 현지 사업자들은 베일 가격 협상력이 높아질 것으로 예상하고 있으며, 유가 변동시 원료비 안정화가 기대됩니다.

라틴아메리카의 팬데믹 이후 레저 수요 증가로 레스토랑, 경기장, 이벤트 장소의 고객이 회복되고 있습니다. 0.31L-0.51L 사이즈의 프리미엄 PET병 수요가 증가하고 있습니다. 코카콜라는 70억 헤알을 투자해 14개의 새로운 라인을 가동했습니다. 대부분 내구성과 경량화를 겸비한 리턴형 PET 전용 라인입니다. 펩시콜라의 우루과이내 1억 달러 규모의 저장시설은 24개 수출 시장을 위한 주내 보충이 가능하며, 자유무역지대의 특혜를 활용하여 재고 보유 일수를 최소화하고 있습니다. 크라프트 맥주 양조장과 지역 와이너리들은 야외 행사장에서 유리병에서 PET 용기로 전환하고 있으며, 무게 감소로 인해 팔레트 당 최대 35%까지 운송비를 절감할 수 있습니다. 병 디자인의 색상, 촉감 마감, 스마트 캡의 차별화는 수지 원가 상승분을 흡수하는 고가대 판매를 지원합니다. 고캐비티 블로우 성형기 제조업체들은 2026년 말까지 수주 잔고를 보고하고 있으며, 거시경제 성장 둔화에도 불구하고 수요가 지속될 것임을 시사하고 있습니다.

PET 마진은 나프타 및 파라크실렌 가격 변동에 연동되며, 이는 원유 지표 가격의 변화를 따라갑니다. 페트로브라스는 2028년까지 167억 달러 규모의 정유소 업그레이드를 계획하고 있지만, 새로운 파라크실렌 또는 PTA 공급원은 아직 확정되지 않았으며, 컨버터는 아시아 지표 가격 변동 위험에 노출되어 있습니다. 환율 변동이 또 다른 요인으로 작용합니다. 원자재 수입은 달러화로, 국내 판매는 헤알화나 페소화로 정산되기 때문입니다. 대형 통합기업은 스왑계약이나 다양한 크래커 설비군으로 리스크 헤지를 하지만, 중소형 컨버터는 주로 현물 거래로 운영되어 최근 비용 급등을 흡수할 수 밖에 없습니다. 원재료 가격의 재평가가 빈번하게 이루어지기 때문에 장기 프로젝트 평가가 복잡해지고 신규 PET 플랜트 및 프리폼 플랜트 건설이 지연되고 있습니다. 이러한 변동성 리스크는 차입 신용프리미엄을 확대시켜 고체반응기를 도입하려는 중견 재활용 기업의 자금조달 비용을 상승시키고 있습니다.

포장 용도는 2025년 생산량의 98.58%를 차지하여 남미 폴리에틸렌 테레프탈레이트 시장이 포장 중심의 생태계임을 입증했습니다. 이 부문의 구조적 우위는 확립된 음료 라인, PET의 배리어 특성에 대한 이해, 그리고 광범위한 연신 블로우 성형 기술에 대한 지식에 기인합니다. 전기 및 전자 분야는 규모는 작지만 CAGR 7.15%로 성장하고 있으며, PET의 유전체 특성을 활용한 가전제품 어셈블리 및 저전압 커넥터 하우징이 주도하고 있습니다. 자동차 분야에서는 연료탱크 라이너와 후드 아래 액체 탱크가 중심이 되어 경량화가 자동차 제조업체의 연비 기준 달성에 기여하고 있습니다. 건축 및 건설 분야에서는 채광-단열용 PET 시트가, 산업-기계 분야에서는 정밀 가이드 및 펌프 부품에 PET가 사용되고 있습니다. 코카콜라의 100% 재생 PET 프리폼 시험 생산은 포장 분야의 지속가능성 분야에서 선구적인 노력을 보여주고 있습니다. 한편, 사이델의 슈퍼 콤비라인은 컨버터가 병 모양을 빠르게 전환할 수 있으며, 라인 가동률 유지에 기여합니다.

향후 수년간 리터너블 용기의 순환 시스템 확대와 뚜껑 고정 규제 강화로 포장용기의 점유율이 더욱 확대될 것으로 예측됩니다. 한편, 고수익성 전기기기 용도의 경우, 라틴아메리카의 가전제품 생산량 증가에 따라 수지 수요 증가가 예상됩니다. 난연성 등급에 대한 상호 학습은 PET의 전자 분야에서의 존재감을 확대할 수 있으며, 자동차 경량화 목표는 연료전지 스택 및 배터리 부품에 대한 틈새 수요를 예고하고 있습니다. 2026-2031년 포장 분야가 계속해서 핵심 분야가 될 것이며, 다양한 최종 용도에서의 채택은 음료 수요의 주기적 하락을 완화하는 데 도움이 될 것입니다.

남미 폴리에틸렌 테레프탈레이트(PET) 시장 보고서는 최종사용자 산업별(자동차, 건축/건설, 전기/전자, 산업/기계, 포장, 기타 최종사용자 산업), 원료 유형별(버진 PET와 재생 PET), 지역별(아르헨티나, 브라질, 기타 남미)로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 톤과 금액(USD)으로 제공됩니다.

The South America Polyethylene Terephthalate Market size in 2026 is estimated at 2.9 million tons, growing from 2025 value of 2.76 million tons with 2031 projections showing 3.74 million tons, growing at 5.19% CAGR over 2026-2031.

The growth curve highlights Brazil's decisive shift toward import substitution, mandatory recycled-content rules, and near-shoring moves by fast-moving consumer-goods majors that collectively anchor regional PET demand. Port congestion at Santos and Paranagua, while a short-term drag on inbound logistics, is nudging converters to favor local resin suppliers that can guarantee shorter lead times, thereby reinforcing domestic investment momentum. Active capacity expansion-such as Coca-Cola's BRL 7 billion, 14-line build-out-and public-private alliances in recycling are broadening supply options and cushioning volatility in crude-linked feedstock prices. Competitive intensity remains moderate; established multinationals leverage vertical integration, while emerging recyclers win share through collection-network outreach and technology licenses.

The National Solid Waste Policy makes closed-loop recycling legally binding as of 2026, requiring beverage fillers to demonstrate that every bottle is collected and reprocessed. Brazil recycled 410,000 tons of PET in 2024, a 14% increase from 2022, yet volumes still fall short of compliance needs. Harmonized MERCOSUR food-grade rPET specifications enable producers to shuttle feedstock across borders, thereby trimming transport costs and enhancing grade uniformity. Supply chains now treat waste as a strategic asset, extending pickup routes from megacities to farming belts where bottled soft drink penetration is climbing. Investments in optical sorters and high-viscosity extrusion systems are scaling rapidly, with several facilities already boasting food-contact clearance under U.S. FDA equivalency audits. As reverse logistics reporting becomes enforceable, local players anticipate stronger bargaining power over bale pricing, thereby stabilizing input costs during crude price swings.

Latin America's post-pandemic leisure boom revives restaurant, stadium, and event traffic, lifting demand for premium PET bottles in the 0.31 L-0.51 L range. Coca-Cola has allocated BRL 7 billion to 14 new lines, many of which are dedicated to returnable PET, blending durability with lightweighting. PepsiCo's USD 100 million storage park in Uruguay enables same-week replenishment for 24 export markets, leveraging free-zone perks to minimize inventory holding days. Craft brewers and regional wineries are switching from glass to PET for open-air venues because weight reductions cut freight bills by up to 35% per pallet. Bottle-design differentiation-in colors, tactile finishes, and smart closures-supports higher shelf prices that absorb resin cost escalations. Equipment makers selling high-cavity blow-molders report order backlogs through late 2026, signaling sustained demand even if macroeconomic growth cools.

PET margins fluctuate with shifts in naphtha and paraxylene prices, which follow changes in crude benchmarks. Petrobras plans USD 16.7 billion in refining upgrades through 2028, but fresh paraxylene or PTA streams remain unconfirmed, leaving converters exposed to Asian benchmark swings. Currency fluctuations add another layer because feedstock imports are clear in USD, while domestic sales settle in reals or pesos. Large integrated players hedge their exposures via swap arrangements and diversified cracker fleets, whereas small converters operate largely on a spot basis, absorbing immediate cost spikes. Frequent feedstock repricing complicates long-horizon project appraisals, thereby delaying the construction of green-field PET or preform plants. The volatility risk amplifies borrower-credit premiums, increasing finance costs for mid-tier recyclers seeking to incorporate solid-state reactors.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Packaging applications accounted for 98.58% of the 2025 volume, confirming the South America Polyethylene Terephthalate market as a packaging-centric ecosystem. The segment's structural lead reflects entrenched beverage lines, familiarity with PET's barrier properties, and widespread stretch-blow expertise. Electrical and electronics, although small, are pacing at a 7.15% CAGR and benefit from consumer electronics assemblies and low-voltage connector housings that tap PET's dielectric performance. Automotive uptake centers on fuel-tank liners and under-hood fluid reservoirs, where weight saving helps manufacturers meet efficiency norms. Building and construction uses PET sheets for daylighting and insulation, while industrial and machinery firms select PET for precision guides and pump components. Coca-Cola's 100% rPET preform pilot at Jundiai showcases packaging's sustainability vanguard, whereas Sidel's Super Combi lines enable converters to quickly switch between bottle formats, thereby protecting line uptime.

In the years ahead, additional returnable loops and tethered-cap regulations will likely consolidate packaging's share, while higher-margin electrical applications may pull incremental resin volumes as Latin American appliance output increases. Cross-learning on flame-retardant grades could broaden PET's electronics footprint, while automotive lightweighting targets foreshadow niche demand in fuel-cell stacks and battery components. Over the 2026-2031 period, packaging remains the anchor, but diversified end-use adoption helps buffer cyclical dips in beverage demand.

The South America Polyethylene Terephthalate (PET) Market Report is Segmented by End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-User Industries), Source Type (Virgin PET and Recycled PET), and Geography (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).