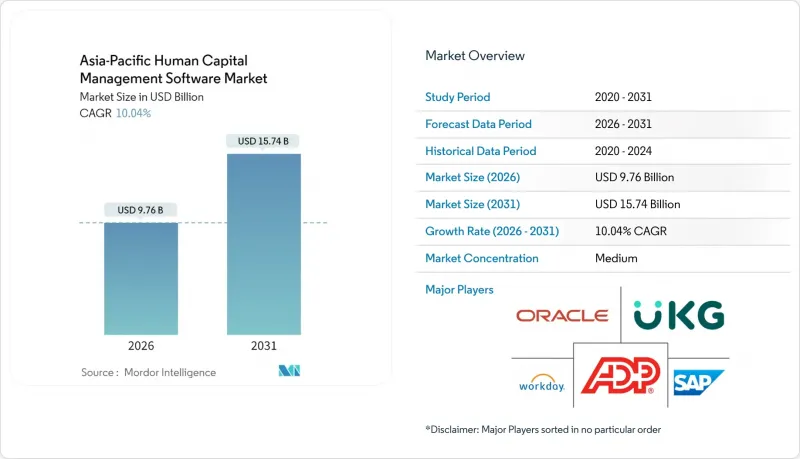

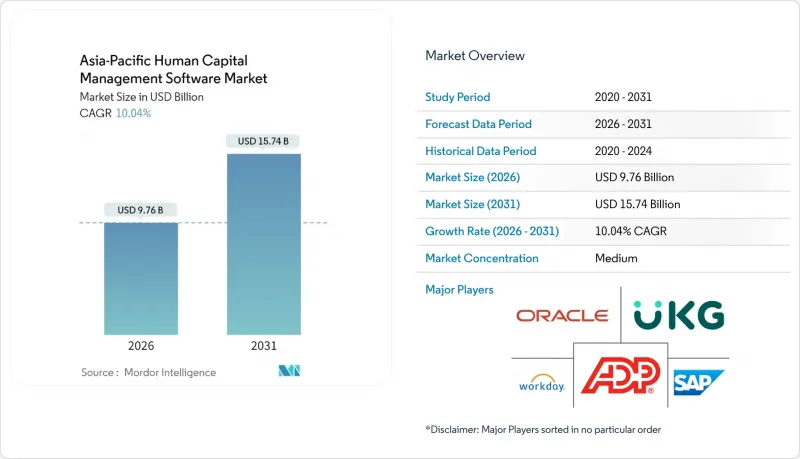

아시아태평양의 인적 자본 관리 소프트웨어 시장은 2025년 88억 7,000만 달러에서 2026년에는 97억 6,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 10.04%를 기록하며 2031년까지 157억 4,000만 달러에 달할 것으로 예측됩니다.

이러한 급격한 성장은 이 지역 기업들이 기존의 수작업 중심의 HR 툴을 수작업을 줄이고 컴플라이언스 리스크를 줄이며, 모바일 우선의 직원 니즈를 충족하는 통합 클라우드 네이티브 플랫폼으로 대체하고 있는 현 상황을 반영합니다. 다양한 언어와 규제 규칙에 대응하면서 채용, 분석, 급여 계산을 효율화하는 AI 기반 자동화로의 빠른 전환이 수요를 촉진하고 있습니다. 심층적인 현지화와 확장 가능한 클라우드 아키텍처를 모두 갖춘 벤더가 우위를 점하고 있으며, 조직은 현대적 HCM을 주변적인 추가 기능이 아닌 핵심 시스템으로 인식하고 있습니다. 건전한 경쟁이 존재하는 반면, 전환 비용과 규제의 복잡성으로 인해 과격한 가격 경쟁은 억제되고 있으며, 기존 사업자에게는 신제품 출시와 인수를 통한 확장을 위한 자금 조달의 여지가 생기고 있습니다.

스마트폰의 보급으로 인해 많은 직원들이 데스크톱 HR 포털에 로그인하지 않는 상황이 발생하고 있습니다. 이 때문에 기업들은 작은 화면에 맞게 워크플로우를 재설계하고 있습니다. 네이티브 모바일 앱은 셀프서비스 도입을 촉진하고, HR 티켓의 양을 줄이며, 데이터를 최신 상태로 유지합니다. BYOD(개인 소유 단말기 반입) 규칙이 주류가 되어 보안 업데이트가 필요하지만, 언제든 접속할 수 있는 편의성을 강화하고 있습니다. 급여명세서, 휴가 승인, 마이크로러닝을 단말기에 전달할 수 있는 벤더는 직원들의 몰입도를 유지할 수 있어 갱신율을 높일 수 있습니다. 인도와 인도네시아에서는 통신사 및 소매업체들이 소비자 앱을 통해 HCM 기능을 일상적으로 배포하고 있으며, 이러한 변화가 두드러지게 나타나고 있습니다.

예산 담당자들은 온프레미스 HR 스위트를 규제 변화에 뒤처지기 쉬운 업그레이드 주기를 수반하는 경직되고 비용이 많이 드는 시스템으로 간주하는 경향이 있습니다. 구독형 클라우드로 전환하면 총소유비용을 최대 절반으로 줄이면서 실시간 기능 출시를 실현할 수 있습니다. SAP 등 세계 기업들은 스킬 추론 AI를 접목한 2024년 버전 업데이트를 발표하며, 클라우드 환경에서만 구현 가능한 기능성을 보여주고 있습니다. 인도와 같은 시장의 강력한 광대역 환경, 스토리지 가격 하락, SaaS 친화적인 규제 등으로 인해 대기업과 중소기업의 기능 격차가 줄어들고 있습니다. 기업이 국경을 넘어 사업을 확장하는 가운데, 중앙 집중식 클라우드 HR 시스템은 여러 관할권에서 급여 계산과 컴플라이언스의 정합성을 용이하게 해줍니다.

많은 국가들이 국경 간 데이터 유통을 제한하고 있기 때문에 SaaS 업체들은 지역 내 데이터센터와 엄격한 암호화를 도입해야 합니다. 모바일 도입으로 인해 새로운 공격 경로가 생겨나고 있으며, 디바이스 관리 및 제로 트러스트 액세스에 대한 투자가 확대되고 있습니다. 전담 보안팀이 없는 기업에서는 통제 감사 과정에서 프로젝트가 지연되는 경우가 종종 발생합니다. ISO 27001 인증을 획득하고 싱가포르 개인정보보호법을 준수하는 벤더는 계약 체결이 용이합니다.

2025년 기준, 클라우드 기반 솔루션은 아시아태평양 인적 자본 관리 소프트웨어 시장 점유율의 78.05%를 차지하며 CAGR 10.98%로 성장할 것으로 예상됩니다. 조직들은 기능 제공의 신속성과 컴플라이언스 업데이트의 중앙 집중식 관리를 주요 장점으로 꼽고 있습니다. 온프레미스 도입은 호주의 특정 공공부문 환경이나 일본의 금융회사 등 규제 당국이 로컬 서버를 요구하는 경우에만 계속하고 있습니다. 비용 모델에서는 전환 후 5년 동안 하드웨어 및 유지보수 비용이 40-60% 절감되는 것으로 나타났습니다. Workday와 같은 공급자들은 데이터 거주지에 대한 구매자의 우려를 해소하기 위해 지역 데이터센터를 확장하고 있습니다.

컴포저블 HR 아키텍처로의 전환은 클라우드 보급을 더욱 가속화하고 있습니다. 고객은 대규모 업그레이드 주기 없이 학습 관리, 성과 평가 등의 새로운 모듈을 도입할 수 있습니다. 생태계 통합업체가 세무, 근태 관리, 협업 앱용 커넥터를 사전 패키지화하여 배포를 가속화할 수 있습니다. 그 결과, 아시아태평양 인재관리 소프트웨어 시장에서는 온프레미스로의 전환보다 SaaS를 통한 신규 도입이 더 많이 이루어지고 있습니다.

핵심 인사관리 시스템은 핵심 기록 시스템으로서 2025년 29.74%의 매출을 유지했지만, 성과 관리 및 인재관리는 CAGR 11.68%로 빠르게 성장하고 있습니다. AI는 개인별 목표 생성, 360도 피드백 집계, 이직 위험이 높은 직원 식별을 실현합니다. 급여 계산은 특히 법정 공제가 분기별로 변경되기 때문에 그 중요성은 유지되고 있지만, 차별화 요소는 총 지급액에서 수취액으로 계산하는 것이 아니라 분석 대시보드로 이동하고 있습니다. 하이브리드 근무를 도입하는 업계에서는 인력 관리가 다시금 주목받고 있습니다.

학습 및 채용 모듈은 AI 기반 스킬 매칭의 혜택을 받고 있습니다. 코너스톤의 2025년 릴리스에서는 생성형 AI를 활용하여 후보자의 이력서를 사내 역량 프레임워크에 매핑하는 기능을 추가했습니다. 거버넌스 리스크 컴플라이언스(GRC) 애드온은 ISO 및 SOC 보고를 위한 감사 추적을 기록합니다. 보상 엔진은 국경을 초월한 팀에 필수적인 지역별 임금 체계를 고려합니다. 이러한 고급 모듈은 종합적으로 고객당 지갑 점유율을 확대하여 애드온 판매로 인한 아시아태평양의 인적 자본 관리 소프트웨어 시장 규모를 증가시키고 있습니다.

The Asia-Pacific Human Capital Management Software market is expected to grow from USD 8.87 billion in 2025 to USD 9.76 billion in 2026 and is forecast to reach USD 15.74 billion by 2031 at 10.04% CAGR over 2026-2031.

This rapid climb reflects how enterprises across the region are replacing patchwork HR tools with unified, cloud-native platforms that cut manual effort, lower compliance risk, and meet mobile-first employee expectations. Demand is reinforced by a sharp pivot toward AI-enabled automation that streamlines recruiting, analytics, and payroll while supporting diverse languages and regulatory rules. Vendors able to pair deep localization with scalable cloud architecture are gaining ground as organizations view modern HCM as a core system, not a peripheral add-on. Competition is healthy, yet switching costs and regulatory complexity temper aggressive price wars, giving established providers room to fund new product releases and acquisition-driven expansion.

Widespread smartphone use means many employees never log into a desktop HR portal, so companies are redesigning workflows for smaller screens. Native mobile apps lift self-service adoption, which slashes HR ticket volumes and keeps data current. Bring-your-own-device rules are now mainstream, compelling security updates but reinforcing the convenience of anytime access. Vendors that can push payslips, leave approvals, and micro-learning to handsets are earning higher renewal rates because employees stay engaged. India and Indonesia showcase this shift, as telecom operators and retailers routinely roll out HCM functions through consumer-grade apps.

Budget holders increasingly view on-premise HR suites as rigid and costly, with upgrade cycles that lag regulatory change. Moving to a subscription-based cloud can drop total ownership costs by up to half while adding real-time feature releases. Global players such as SAP released 2024 updates that embed skills-inference AI, illustrating functionality only practical in the cloud. Strong broadband, falling storage prices, and SaaS-friendly regulations in markets like India are shrinking the gap between enterprise and SME capabilities. As firms expand across borders, centralized cloud HR systems ease payroll and compliance alignment in multiple jurisdictions.

Many countries restrict cross-border data flows, so SaaS vendors must deploy in-region data centers and rigorous encryption. Mobile adoption introduces additional attack vectors, prompting higher spend on device management and zero-trust access. Firms without dedicated security teams often face project delays while controls are audited. Vendors that certify to ISO 27001 and align with Singapore's Personal Data Protection Act find it easier to close deals.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud options captured 78.05% of the Asia-Pacific Human Capital Management Software market share in 2025 and are growing at an 10.98% CAGR. Organizations cite faster feature delivery and centralized compliance updates as top benefits. On-premise deployments persist only where regulators require local servers, such as certain public-sector environments in Australia and financial firms in Japan. Cost modeling shows a 40-60% reduction in hardware and maintenance spend over five years after migration. Providers like Workday extend regional data centers to reassure buyers about data residency.

A shift toward composable HR architecture further boosts the cloud. Customers can turn on new modules, such as learning or performance, without a major upgrade cycle. Ecosystem integrators pre-package connectors for tax, time clocks, and collaboration apps, speeding rollout. As a result, the Asia-Pacific Human Capital Management Software market registers more first-time buyers entering directly via SaaS than through on-premise conversions.

Core HR retained 29.74% revenue in 2025 as the anchor record system, yet performance and talent management are accelerating at 11.68% CAGR. AI generates personalized goals, collates 360-degree feedback, and flags flight-risk employees. Payroll remains mission-critical, especially as statutory deductions change quarterly, but differentiation now centers on analytics dashboards rather than gross-to-net calculations. Workforce management enjoys renewed attention in industries adopting hybrid shifts.

Learning and recruiting modules benefit from AI-based skill matching. Cornerstone's 2025 release employed generative AI to map candidate resumes to internal competency frameworks. Governance, risk, and compliance add-ons record audit trails for ISO and SOC reporting. Compensation engines factor location-based pay scales, vital for cross-border teams. Collectively, these advanced modules expand wallet share per customer, raising the Asia-Pacific Human Capital Management Software market size, attributed to add-on sales.

The Asia-Pacific Human Capital Management Software Market Report is Segmented by Deployment (Cloud-Based and On-Premise), Application (Core HR, Payroll Management, and More), Organization Size (Small and Medium-Sized Enterprises and Large Enterprises), Offering (Software and Services), End-User Industry (BFSI, IT and Telecom, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).