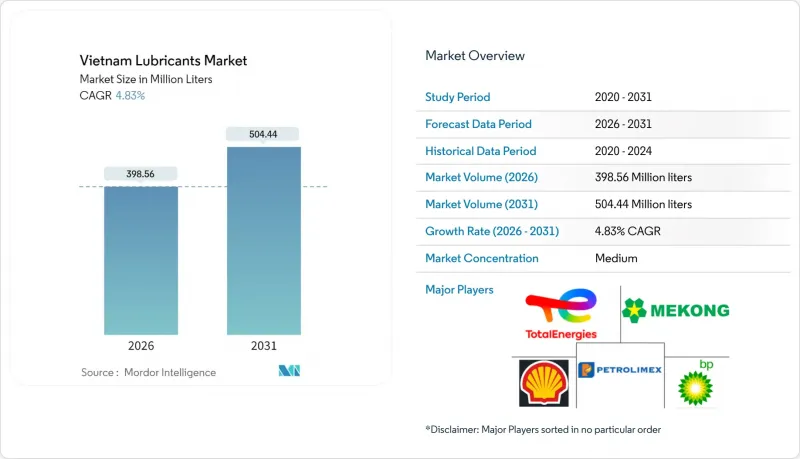

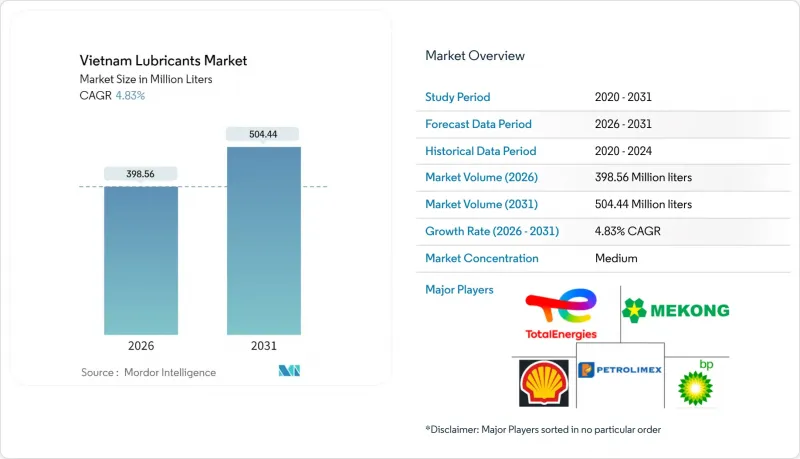

베트남의 윤활유 시장 규모는 2026년에 3억 9,856만 리터에 달할 것으로 예측됩니다.

이는 2025년 3억 8,020만 리터에서 성장한 수치이며, 2031년에는 5억 4,440만 리터에 달할 것으로 예상됩니다. 2026년부터 2031년까지 연평균 4.83%의 성장세를 이어갈 것으로 예상됩니다.

이러한 성장은 전동화가 진행되는 가운데에도 지속될 것으로 예상됩니다. 그 배경에는 이륜차가 여전히 이동수단의 주류로 자리 잡고 있고, 새로운 제조 투자가 산업 활동을 계속 촉진하고 있다는 점이 있습니다. 증가하는 차량 보유량이 성장 모멘텀을 뒷받침하고, 고성능화로의 수요 전환, 그리고 산업단지 전체에서 기계 수요를 촉진하는 안정적인 외국인 직접투자가 기여하고 있습니다. 시장 진입 기업들은 기유 가격 변동에 대한 마진 보호를 위해 프리미엄 배수 간격 제품, 광범위한 유통망, 현지 배합에 중점을 두고 있습니다. 동시에, 다가오는 환경세와 확대된 생산자책임재활용(EPR) 규제로 인해, 생산자들은 고가이면서도 라이프사이클 배출량을 줄일 수 있는 합성유와 바이오 기반 제품군으로 전환하고 있습니다. 이러한 교차하는 추세는 전기자동차(EV)가 기존 엔진 오일의 수요를 점차 잠식하는 가운데 베트남 윤활유 시장의 단기적인 견조한 전망을 형성하고 있습니다.

베트남의 산업정책은 2030년까지 연간 승용차 및 이륜차 판매량을 약 100-110만대까지 늘리겠다는 목표를 세우고 있습니다. 이륜차는 여전히 전체 차량의 대부분을 차지하고 있으며, 잦은 오일 교환을 필요로 하는 내연기관의 기반이 유지되고 있습니다. 2024년에는 전기 오토바이가 신규 등록 오토바이의 대부분을 차지했지만, 도시 외 지역에서의 항속 거리에 대한 불안감으로 인해 광유 및 반합성 제품에 대한 지속적인 수요가 지속되고 있습니다. 오토바이에 따른 정기적인 유지보수 주기와 가처분 소득의 증가가 결합되어 엔진 오일 및 변속기 오일 판매량 증가의 기반이 되고 있습니다.

2024년 상반기 제조업에 대한 외국인직접투자액은 152억 달러에 달했으며, 가공 및 전자제품 공장이 유입액의 3분의 2 이상을 차지했습니다. 이러한 자본 투입은 수명 연장과 다운타임 감소를 목적으로 하는 유압유, 기어유, 금속가공유를 필요로 하는 기계 설비의 도입으로 이어집니다. 하이퐁, 박닌, 동나이의 산업단지에서는 세계 공급망 감사 기준을 준수하는 OEM 인증 윤활유를 요구하고 있습니다. 이로 인해 발생하는 합성유 및 바이오 기반 윤활유에 대한 수요는 예측 기간 동안 프리미엄 제품의 시장 침투율 향상에 기여할 것입니다.

베트남은 기유 수요의 대부분을 수입에 의존하고 있기 때문에 현지 블렌딩 업체들은 세계 원유 가격 변동에 영향을 받기 쉽습니다. 2024년 그룹 II 기유 현물 가격의 급등은 마진을 압박하여 대부분의 점도 등급에서 소매 가격 상승을 초래했습니다. 재고 신용이 제한된 독립 블렌더는 비용 전가에 어려움을 겪고 있으며, 대규모 프로모션을 진행하는 국제 브랜드에 판매량을 빼앗길 위험에 직면해 있습니다. 그 결과, 일부 판매업체는 지방의 재고 수준을 줄이고, 공급 계약이 정상화될 때까지 지방 도시에서 간헐적인 품귀현상이 발생했습니다.

2025년 현재 자동차 엔진 오일이 시장 점유율의 37.90%를 차지하고 있으며, 이는 베트남의 교통 상황이 오토바이에 크게 편중되어 있는 현실을 보여줍니다. 이곳에서는 2행정 및 4행정 엔진 오일이 등록대수 7,700만대라는 어마어마한 오토바이 시장에 대응하고 있습니다. 산업용 엔진 오일은 가장 빠르게 성장하는 제품군으로, 신규 가스화력 및 재생에너지 발전 프로젝트를 배경으로 2031년까지 CAGR 5.22%로 성장할 것으로 예상됩니다. 수요는 유지보수 주기를 연장할 수 있는 저회분 배합에 대한 OEM의 요구에 의해 주도되고 있습니다. 변속기 오일은 승용차의 AT(자동변속기) 보급률 증가에 따른 수혜가 예상되며, 기어오일 수요는 경상용차 및 물류차량 확대와 연동하여 증가할 것으로 예상됩니다.

금속가공유는 삼성과 폭스콘의 정밀 가공 투자 확대에 따라 수요가 증가하고 있으며, 마스터유체솔루션즈의 현지 유통망이 이러한 추세를 뒷받침하고 있습니다. 베트남의 전력 개발 계획이 2030년까지 재생에너지 비율 29%를 목표로 하고 있는 가운데, 터빈 오일과 변압기 오일은 꾸준히 성장하고 있으며, 매력적인 수익률을 제공하는 특수 유체 분야의 기회를 창출하고 있습니다. 전반적으로 제품 구성은 현대 설비의 고부하 및 고온 운전 조건에 대응하는 고성능 합성유로 전환되고 있습니다.

베트남 윤활유 시장 보고서는 제품 유형(자동차 엔진 오일, 산업용 엔진 오일, 변속기 오일, 기어오일, 브레이크 오일, 유압유, 그리스 등), 최종사용자 산업(자동차, 선박, 항공우주, 중장비, 산업), 기유 유형(광물성, 합성, 반합성, 바이오 기반)으로 분류됩니다. 베이스, 합성, 반합성, 바이오 기반) 별로 분류되어 있습니다. 시장 예측은 리터 단위로 제공됩니다.

Vietnam Lubricants Market size in 2026 is estimated at 398.56 million liters, growing from 2025 value of 380.20 million liters with 2031 projections showing 504.44 million liters, growing at 4.83% CAGR over 2026-2031.

This growth persists even as electrification advances, because two-wheelers continue to dominate mobility, and new manufacturing investments keep industrial activity rising. An expanding vehicle parc sustains momentum, a shift toward higher-performance formulations, and steady foreign direct investment that lifts machinery demand across industrial zones. Market participants emphasize premium drain-interval products, broad distribution, and localized blending to protect margins against base-oil cost fluctuations. At the same time, looming environmental taxes and Extended Producer Responsibility (EPR) rules are steering producers toward synthetic and bio-based lines that command higher price points yet trim lifecycle emissions. These intersecting trends frame a resilient near-term outlook for the Vietnam lubricants market even as electric vehicles (EVs) gradually erode conventional engine oil volumes.

Vietnam's industrial policy aims to achieve annual passenger-car and two-wheeler sales of approximately 1.0-1.1 million units by 2030. Two-wheelers still account for the majority of the vehicle fleet, preserving a large base of internal-combustion engines that require frequent oil changes. Although electric motorcycles accounted for a significant portion of new two-wheeler registrations in 2024, range anxiety outside urban cores continues to underpin sustained demand for mineral oil and semi-synthetic products. Regular maintenance cycles associated with motorcycles, combined with rising disposable incomes, continue to anchor volume growth for engine oils and transmission fluids.

Manufacturing FDI reached USD 15.2 billion in the first six months of 2024, with processing and electronics plants accounting for more than two-thirds of the inflows. These capital injections translate into machinery installations that demand hydraulic, gear, and metalworking fluids engineered for longer drain intervals and lower downtime. Industrial parks in Hai Phong, Bac Ninh, and Dong Nai require OEM-approved lubricants that comply with global supply-chain audit standards. The resulting pull for synthetic and bio-based lubricants helps lift overall premium-product penetration through the forecast window.

Vietnam imports the majority of its base-oil requirement, exposing local blenders to global crude swings. A spike in Group II base-oil spot prices in 2024 compressed margins and led to retail price hikes across most viscosity grades. Independent blenders with limited inventory credit struggled to pass on costs, risking volume losses to heavily promoted international brands. As a result, some distributors trimmed rural stock levels, causing sporadic shortages in tier-3 cities until supply contracts normalized.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2025, automotive engine oil commands a 37.90% share of the market, underscoring Vietnam's transportation landscape, which is heavily skewed towards motorcycles. Here, both 2-stroke and 4-stroke engine oils cater to a staggering 77 million registered two-wheelers. Industrial engine oil is the fastest-growing product category, expanding at a 5.22% CAGR through 2031, driven by new gas-fired and renewable power projects. The demand is driven by OEM requirements for low-ash formulations that enable longer maintenance intervals. Transmission fluids are expected to benefit from increased automatic-transmission penetration in passenger cars, while gear oil demand is expected to align with the expansion of light-commercial and logistics fleets.

Metalworking fluids escalate in tandem with precision-machining investments by Samsung and Foxconn suppliers, and Master Fluid Solutions' localized distribution underscores this trend. Turbine and transformer oils are experiencing steady growth as Vietnam's Power Development Plan targets a 29% renewable capacity by 2030, creating specialty-fluid opportunities that offer attractive margins. Overall, the product mix is tilting toward higher-performance synthetics that accommodate high-load, high-temperature operating conditions in modern equipment.

The Vietnam Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Transmission Fluids, Gear Oil, Brake Fluids, Hydraulic Fluids, Greases, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), and Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based). The Market Forecasts are Provided in Terms of Volume (Litres).