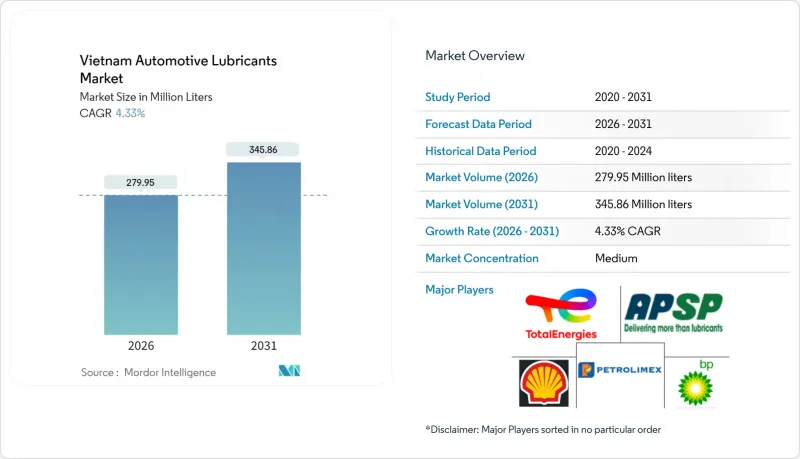

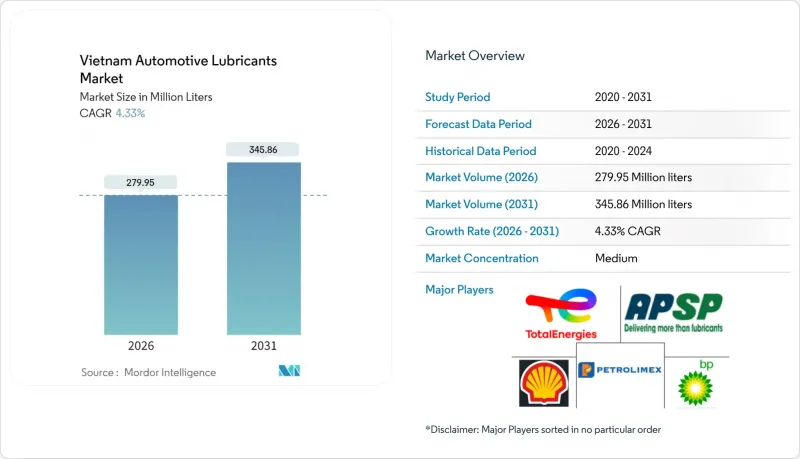

베트남 자동차 윤활유 시장은 2025년에 2억 6,834만 리터로 평가되었으며, 2026년 2억 7,995만 리터에서 2031년까지 3억 4,586만 리터에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.33%로 예상됩니다.

견조한 화물 운송 활동, 노후화된 차량 보유량, 확대되는 E-Commerce용 차량군이 성장을 뒷받침하고 있습니다. 한편, 전동화 정책은 장기적인 수요 구조를 바꾸고 있습니다. 페트로리멕스의 유통망 우위와 쉘, BP/카스트롤, 모투르의 현지 배합 투자가 결합되어 공급의 탄력성을 유지하면서 경쟁적 차별화를 도모하고 있습니다. 프리미엄 합성유의 급속한 보급, OEM 제조업체의 교체 주기 연장 요청, 위조품에 대한 엄격한 단속 강화로 평균 판매가격이 상승하여 이익률 확대를 촉진하고 있습니다. 한편, 하노이시가 순환도로 1호선 내 화석연료 이륜차 금지를 앞두고 있고, 호치민시가 저공해 구역을 도입하려는 움직임은 기존 이륜차 수요에 대한 규제 압력을 시사하고 있습니다.

국내 자동차 등록대수는 지속적으로 증가하고 있습니다. 7년 이상 경과한 모델의 비율이 증가하고 있으며, 노후화 및 블로우 바이로 인한 오일 교환 빈도의 증가가 필요합니다. 트럭 운송은 여전히 분산화되어 있으며, 대부분의 상용차는 5톤 미만이며, 업체당 평균 보유 대수는 5대에 불과하여 서비스 사고 발생 빈도가 높아지고 있습니다. 이러한 요인들이 결합되어 전동화 추세로 인한 역풍에도 불구하고 베트남 자동차 윤활유 시장은 수량 기준으로 상승 추세를 유지하고 있습니다.

베트남은 2025년 세계 2위의 전기이륜차 시장이 될 것이며, 혼다는 같은 해에 220만 대의 내연기관(ICE) 오토바이를 판매할 것으로 예상하고 있습니다. 도처에 있는 갓길 세차장에서 이루어지는 정기적인 오일 서비스는 윤활유 소비의 높은 빈도를 만들어 내고 있습니다. 하노이시가 2026년 순환도로 1호선 내 화석연료 오토바이의 운행을 금지하는 등 법규에 의한 금지 조치로 인해 도시 지역의 수요가 줄어들기 시작했지만, 다른 지역에서는 여전히 많은 차량이 운행되고 있기 때문에 베트남의 자동차 윤활유 시장은 2030년까지 오토바이 수요로 인한 판매량을 뒷받침할 수 있을 것으로 예상됩니다. 유지될 것으로 예상됩니다.

VinFast는 2024년 9만 7,399대의 배터리 전기자동차를 출하하고, 2025년에는 15만 700대를 목표로 하고 있습니다. BEV는 엔진오일 사용이 불필요하고 변속기 오일의 수요도 감소하기 때문에 베트남의 자동차 윤활유 시장은 구조적인 수요 감소에 직면해 있습니다. 특히 도시 지역의 자동차 차량에서 두드러지게 나타납니다. 그러나 열관리용 냉각수 및 특수 e-그리스가 새로운 고부가가치 분야를 개척하고 있습니다.

2025년 기준, 자동차 엔진 오일은 베트남 자동차 윤활유 시장 점유율의 52.88%를 차지했습니다. 승용차, 오토바이, 트럭에 내장되어 수량 면에서 주도권을 확보하고 있습니다. 그러나 자동변속기 오일(ATF)은 4.52%의 CAGR로 가장 가파른 성장세를 보이고 있으며, 승용차의 자동변속기 보급률 증가와 부품 보증 대응 강화가 기여하고 있습니다. 수동 변속기 오일은 여전히 소형 트럭 분야에서 점유율을 유지하고 있으며, 브레이크 오일은 안정적이고 중간 정도의 한 자릿수 기여도를 유지하고 있습니다.

위조품의 만연으로 인해 브랜드 제조사들은 프리미엄 제품에 가시적, 비가시적 보안 마커를 내장해야 하는 상황에 직면해 있으며, 비용 증가에도 불구하고 브랜드 가치를 유지하기 위해 노력하고 있습니다. 또한, 블렌딩 제조업체는 API SP 및 유로 6 표준을 준수하기 위해 그룹 III 기유와 고성능 첨가제를 배합합니다. 모투르 베트남 공장은 재생 기유 블렌드의 상업적 테스트를 시작했으며, 신규 그룹 II 기유에 비해 탄소발자국을 줄일 수 있을 것으로 기대됩니다. 이러한 기술 혁신은 경쟁 우위를 강화하고 베트남 자동차 윤활유 산업에서 OEM 파트너십의 발전과 조화를 이룹니다.

베트남 자동차 윤활유 시장 보고서는 제품 유형별(자동차 엔진오일(0W-XX, 5W-XX, 5W-XX, 10W-XX, 15W-XX, 단일점도 오일, 기타 등급), 수동변속기 오일, 자동변속기 오일, 브레이크 오일, 자동차용 그리스, 기타 제품 유형) 및 차량 유형(승용차, 상용차, 이륜차)별로 분류되어 있습니다. 시장 예측은 리터 단위로 제공됩니다.

The Vietnam Automotive Lubricants Market was valued at 268.34 million liters in 2025 and estimated to grow from 279.95 million liters in 2026 to reach 345.86 million liters by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Robust freight activity, an aging vehicle parc, and expanding e-commerce fleets underpin this growth, even as electrification policies begin to reshape long-term demand. Distribution dominance by Petrolimex, combined with localized blending investments from Shell, BP/Castrol, and Motul, sustains supply resiliency while intensifying competitive differentiation. The rapid adoption of premium synthetics, longer drain intervals mandated by OEMs, and stricter crackdowns on counterfeit products are increasing average selling prices and encouraging margin expansion. At the same time, Hanoi's impending ban on fossil-fuel motorcycles inside Ring Road 1 and Ho Chi Minh City's Low Emission Zone signal regulatory pressure on legacy two-wheeler demand.

National vehicle registrations continue to rise. A growing proportion of models are seven years or older, requiring more frequent oil replacements due to degradation and blow-by. Trucking remains fragmented; the majority of commercial vehicles are under 5 tons and average just five trucks per firm, which magnifies service incidents. These factors collectively sustain the Vietnam automotive lubricants market on an upward volume trajectory, despite the headwinds from the electrification trend.

Although Vietnam became the world's second-largest electric two-wheeler market in 2025, Honda still projects selling 2.2 million ICE motorcycles that year. Routine oil services conducted at ubiquitous roadside washes yield high-frequency lubricant turnover. Legislated bans, such as Hanoi's 2026 exclusion of fossil-fuel motorcycles inside Ring Road 1, begin to narrow urban demand yet leave a vast in-use fleet elsewhere, allowing the Vietnam automotive lubricants market to retain two-wheeler volume support into 2030.

VinFast shipped 97,399 battery EVs in 2024 and targets 150,700 units in 2025. Because BEVs eliminate engine oil usage and reduce transmission-fluid needs, the Vietnam automotive lubricants market faces structural demand erosion, especially in urban car fleets. Yet thermal-management coolants and specialized e-greases open new high-value niches.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Automotive engine oil accounted for 52.88% of the Vietnam automotive lubricants market share in 2025. Embedded usage across cars, motorcycles, and trucks ensures volume leadership. However, automatic transmission fluid (ATF) displays the steepest growth trajectory at a 4.52% CAGR, benefiting from rising passenger-car automatic transmission penetration and intensified parts-warranty compliance. Manual transmission fluid still holds a share in light-duty trucks, whereas brake fluids maintain steady mid-single-digit contributions.

Persistent counterfeit activity forces branded suppliers to embed overt and covert security markers on premium SKUs, adding costs but preserving brand equity. Blenders also incorporate Group III base oils and high-performance additive chemistries to comply with API SP and Euro 6 requirements. Motul's Vietnamese plant has begun commercial trials of Re-Refined Base Oil blends, promising a reduction in carbon footprint compared to virgin Group II stocks. These innovations reinforce competitive positioning and align with evolving OEM partnerships inside the Vietnam automotive lubricants industry.

The Vietnam Automotive Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil (0W-XX, 5W-XX, 10W-XX, 15W-XX, Monogrades, and Other Grades), Manual Transmission Fluids, Automatic Transmission Fluids, Brake Fluids, Automotive Greases, and Other Product Types), and Vehicle Type (Passenger Vehicles, Commercial Vehicles, and Two-Wheelers). The Market Forecasts are Provided in Terms of Volume (Litres).