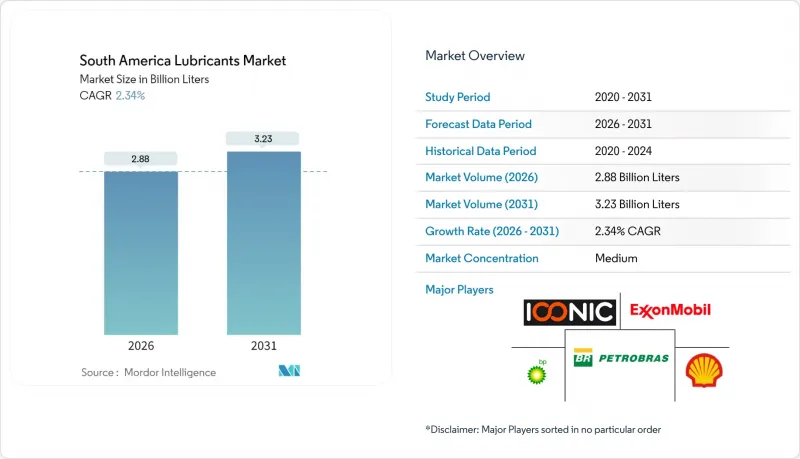

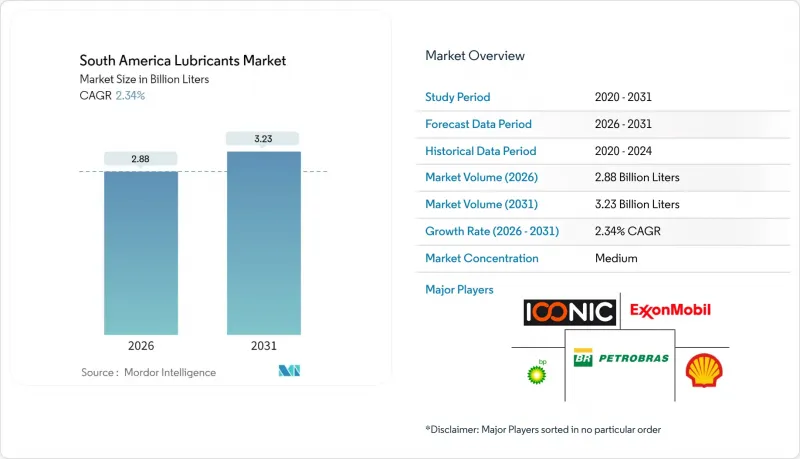

남미의 윤활유 시장 규모는 2026년에는 28억 8,000만 리터로 추정되고 있습니다.

이는 2025년 28억 1,000만 리터에서 성장한 수치이며, 2031년에는 32억 3,000만 리터에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 2.34%로 성장할 것으로 예상됩니다.

지역적 화물 운송 거리의 회복, 해양 석유 활동의 확대, 지속적인 산업 현대화가 수요를 뒷받침하고 있습니다. 한편, 환율 변동과 정책 전환이 국지적 리스크 요인으로 작용하고 있습니다. 브라질의 자동차 제조, 브라질과 가이아나의 심해 탐사, 칠레와 페루의 광업 자동화가 결합되어 광범위한 소비 기반을 확보하고 있습니다. 풍력 및 태양광을 중심으로 한 재생에너지의 증가는 터빈 오일과 유압유에 대한 새로운 수요를 창출하고 있으며, 배출 기준의 강화는 저SAPS 및 합성유로의 전환을 가속화하고 있습니다. 경쟁의 강도는 여전히 중간 수준이지만, 다국적 기업들이 현지 공급망을 강화하고 지역 기업들이 합병과 유통 제휴를 통해 규모를 확대함에 따라 경쟁의 강도가 높아지고 있습니다.

니어쇼어링의 발전과 E-Commerce의 확대로 브라질, 아르헨티나, 칠레의 장거리 트럭 운송이 활성화되어 화물 운송량은 팬데믹 이전 수준을 넘어섰습니다. 브라질의 트럭 운송 산업은 국내 화물의 60% 이상을 취급하고 있으며, 현재 배수 간격 연장 및 연비 향상을 위한 고품질 엔진 오일 및 변속기 오일에 대한 수요가 증가하고 있습니다. 콩, 옥수수, 구리 수확기는 물류 성수기에 윤활유 수요량을 더욱 끌어올려 단기적인 소비 급증세를 고정시켜 시장 성장의 기반을 유지했습니다.

브라질의 프리솔트 유전과 가이아나의 스타브로크 광구에서는 극한의 온도와 수심 2,000m를 견딜 수 있는 합성 시추 진흙탕, 해저 장비용 기어 오일, 유압작동유가 공동으로 요구되고 있습니다. 엑손모빌의 멀티 플랫폼 계획과 페트로브라스(Petrobras)의 해저 증압 계약은 프리미엄 가격을 실현하고 공급업체와 고객의 기술 협력을 강화하는 전문 서비스 모델의 좋은 예입니다.

보조금에 의한 저가 판매는 소비자들이 고효율 합성유에 대한 구매 의욕을 떨어뜨리고, 많은 운전자들이 짧은 간격으로 교체하는 광유에 묶여 승용차 엔진 오일의 부가가치 성장을 억제하고 있습니다. 보조금 제도는 기존에는 부가가치보다 판매량을 중시하는 경향이 있어, 장수명 프리미엄 제품보다는 재래식 미네랄 오일을 사용한 잦은 오일 교환을 장려해 왔습니다. 이러한 상황은 특히 승용차 부문에 영향을 미치고 있으며, 비용에 민감한 소비자들은 장기적인 엔진 보호 및 연비 개선 효과보다 즉각적인 비용 절감을 우선시하고 있습니다.

엔진 오일은 2025년 기준 남미 윤활유 시장 점유율의 39.72%를 차지하고 있으며, 광업, 농업, 재생에너지 분야의 자동화 발전에 따라 유압작동유는 2031년까지 CAGR 2.66%로 확대될 것으로 예상됩니다. 합성유 또는 바이오 기반 원료로 제조된 특수 유압작동유는 고압 시스템이 요구하는 산화 안정성과 내열성을 보장합니다. 변속기 오일과 기어 오일은 차량 현대화 프로그램의 혜택을 받는 반면, 그리스는 가혹한 해양 및 산업 환경에서 베어링을 보호하는 역할을 합니다.

배기가스 규제로 인해 엔진 오일은 그룹 III 오일이나 합성유 블렌드로의 업그레이드가 추진되고 있지만, 가격 측면의 고려로 인해 구식 차량에서는 여전히 광유 제품에 대한 수요가 있습니다. 재생에너지 확대에 따라 유압작동유의 수요가 증가하고 있으며, 환경 규제 대응을 위해 생분해성 배합이 선호되고 있습니다. 첨가제 화학 분야의 지속적인 연구개발을 통해 지역 블렌더 기업들은 남미 윤활유 시장에서 차별화된 제품을 개발할 수 있게 되었습니다.

남미 윤활유 보고서는 제품 유형별(엔진 오일, 변속기 및 기어오일, 유압유, 그리스 등), 기유별(광유, 합성유, 반합성유, 바이오기유), 최종사용자별(자동차, 중장비, 야금 및 금속가공, 발전, 선박 및 해양, 기타 산업), 지역별(아르헨티나, 브라질, 칠레, 콜롬비아, 페루, 기타 남미 국가), 지역별로 분류됩니다. 아르헨티나, 브라질, 칠레, 콜롬비아, 페루, 기타 남미 국가)로 분류되어 있습니다.

South America Lubricants Market size in 2026 is estimated at 2.88 Billion Liters, growing from 2025 value of 2.81 Billion Liters with 2031 projections showing 3.23 Billion Liters, growing at 2.34% CAGR over 2026-2031.

Recovering regional freight mileage, expanding offshore oil activity, and ongoing industrial modernization underpin demand, even as currency volatility and policy shifts create pockets of risk. Automotive manufacturing in Brazil, deep-water exploration in Brazil and Guyana, and mining automation in Chile and Peru together secure a broad consumption base. Renewable power additions, led by wind and solar, are introducing new needs for turbine and hydraulic fluids, while stricter emissions standards are accelerating migration toward low-SAPS and synthetic formulations. Competitive intensity remains moderate but rising as multinationals strengthen local supply chains and regional firms seek scale through mergers and distribution alliances.

Freight activity has surpassed pre-pandemic levels as near-shoring shifts and e-commerce intensify long-haul truck movements across Brazil, Argentina, and Chile. Brazil's trucking sector alone handles more than 60% of domestic cargo and now demands premium engine and transmission oils that enable extended drain intervals and fuel economy gains. Harvest cycles for soy, corn, and copper further lift lubricant volumes during peak logistics seasons, locking in a short-term consumption surge that sustains baseline market growth.

Brazil's pre-salt fields and Guyana's Stabroek Block collectively require synthetic drilling muds, subsea gear oils, and hydraulic fluids capable of withstanding extreme temperatures and 2,000 m water depths. ExxonMobil's multiplatform program and Petrobras subsea boosting contracts exemplify the specialized service models that command premium pricing and deepen supplier-client technical ties.

Subsidized pump prices reduce consumer motivation to purchase high-efficiency synthetics, locking many motorists into short-interval mineral oils and capping value growth in passenger-car motor oils. The subsidy system has historically favored volume over value, encouraging frequent oil changes with conventional mineral oils rather than extended-service premium products. This dynamic particularly affects the passenger vehicle segment, where cost-conscious consumers prioritize immediate savings over long-term engine protection and fuel economy benefits.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Engine oils retained 39.72% of the 2025 South America lubricants market share, but hydraulic fluids are poised for a 2.66% CAGR through 2031 as automation spreads in mining, agriculture, and renewables. Specialized hydraulics formulated from synthetic or bio-based stocks ensure oxidative stability and temperature resilience demanded by high-pressure systems. Transmission and gear oils gain from fleet modernization programs, whereas greases protect bearings in harsh marine and industrial environments.

Emissions mandates push engine oil upgrades toward Group III and synthetic blends, yet price sensitivity keeps mineral products relevant in older vehicles. Hydraulic-fluid demand benefits from renewable-energy build-outs, where biodegradable formulations are preferred for environmental compliance. Continuous research and development in additive chemistry allows regional blenders to position differentiated offerings in the South America lubricants market.

The South America Lubricants Report is Segmented by Product Type (Engine Oils, Transmission and Gear Oils, Hydraulic Fluids, Greases, and More), Base Oil (Mineral, Synthetic, Semi-Synthetic, and Bio-Based), End-User (Automotive, Heavy Equipment, Metallurgy and Metalworking, Power Generation, Marine and Offshore, and Other Industries), and Geography (Argentina, Brazil, Chile, Colombia, Peru, and Rest of South America).