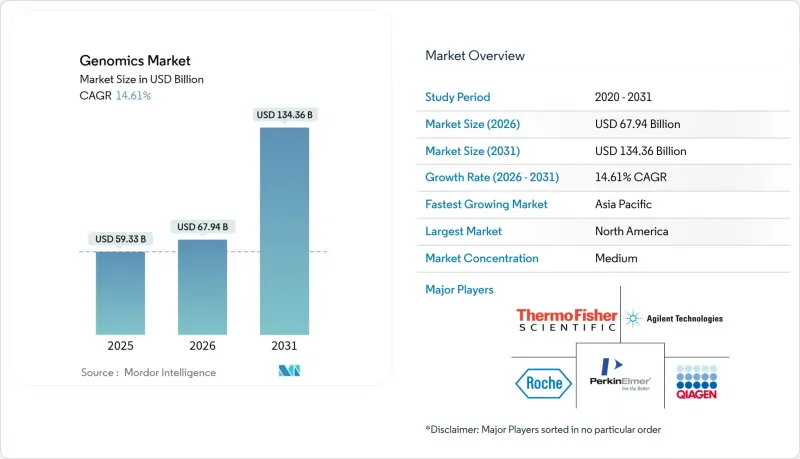

유전체학 시장은 2025년에 592억 8,000만 달러로 평가되었으며, 2026년 679억 4,000만 달러에서 2031년까지 1,343억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 14.62%로 예상됩니다.

시퀀싱 비용의 하락, 집단 시퀀싱, 인공지능의 급속한 보급은 유전체학 시장의 다년간의 성장을 견인하고 있습니다. 국가 주도의 시퀀싱 프로그램을 통해 유전체당 비용이 200-500달러대로 낮아졌고, 국내 플랫폼에 대한 국가적 투자는 공급망을 보호하고 데이터 주권을 지지하고 있습니다. 병원, 제약사, 정부는 현재 유전체학을 실험적 도구가 아닌 중요한 헬스케어 인프라로 인식하고 장비, 소모품, 클라우드 분석에 대한 지출을 촉진하고 있습니다. 경쟁 환경은 처리 시간 단축과 규제 준수를 지원하는 통합 하드웨어 및 소프트웨어 스택을 제공하는 기업에게 유리하게 작용하고 있습니다. 마지막으로, 완전한 인수가 아닌 파트너십을 기반으로 한 점진적인 통합이 진행됨에 따라 롱리드 화학, AI 해석, 클라우드 바이오인포매틱스에 집중하는 혁신적인 신규 진입기업을 위한 여지가 남아있습니다.

각국의 보건 시스템은 소아 의료를 사후 대응형에서 예측형으로 전환하기 위해 보편적 신생아 유전체 시퀀싱을 도입하고 있습니다. 영국 NHS는 전장유전체 스크리닝을 확대하고 있으며, 싱가포르의 프로그램은 가족성 고콜레스테롤혈증을 대상으로 하고 있습니다. 이러한 노력은 하이스루풋 시퀀서용 시약에 대한 장기적인 수요를 보장하고, 제약사들이 희귀질환 치료제 개발을 위해 라이선싱할 수 있는 데이터세트를 생성할 수 있도록 합니다. 애널리스트들은 후기 치료 회피로 인한 10배의 경제적 수익을 예측하고 있으며, 지속적인 공적 자금 투입을 촉구하고 있습니다. 유전 상담사 부족, 안전한 데이터 저장 등 도입상의 문제들이 병원을 클라우드 바이오인포매틱스 플랫폼으로 이끌고 있습니다.

인공지능은 유전체 분석 결과를 종단적 위험도 점수 및 치료 권장사항으로 변환합니다. 일루미나와 NVIDIA의 협력은 GPU 가속 알고리즘이 2차 분석 시간을 단축하고 변종 호출 정확도를 향상시키는 실례를 보여주고 있습니다. 미국 의료 시스템에서 AI 가이드형 약물유전학 도입 후 약물 부작용이 30% 감소했다고 보고되었으며, 제약사들은 멀티오믹스 AI를 통해 임상시험 대상 집단을 계층화 하고 있습니다. FDA 의료기기 규제와 신흥 AI 거버넌스 모두에 정통한 기업이 병원 계약을 따내고 있습니다. 프라이버시에 대한 기대치가 높아지면서 벤더들은 동형암호화 및 연합학습을 채택할 수밖에 없는 상황에 처해 있습니다.

유럽의 건강 데이터 공간(European Health Data Space)과 중국의 바이오 보안법은 유전체 정보 전송에 엄격한 규제를 부과하고 있으며, 다국적 기업들은 지역 데이터센터를 설립하고 컴플라이언스 대응 워크플로우를 구축해야 합니다. 이러한 병렬 인프라는 운영 비용을 증가시키고, 협업을 지연시키며, 국내 통합형 경쟁사에게 우위를 점하게 하는 결과를 초래하고 있습니다. 중소기업은 규제 대응 자원이 부족하고 철수 또는 인수합병의 위험에 직면하고 있으며, 전 세계적으로 사업하는 기업의 통합이 가속화되고 있습니다.

소모품은 2025년 매출의 43.05%를 차지해 일상적인 시퀀싱 워크플로우에서 소모품이 차지하는 중요한 역할을 뒷받침합니다. 배치 간 변동을 최소화하는 키트 표준화와 라이브러리 준비 속도를 높이는 자동화가 성장을 뒷받침하고 있습니다. 서비스형 시퀀싱과 바이오인포매틱스 위탁을 기반으로 한 서비스 분야는 연구소가 자본 지출을 운영 예산으로 전환하면서 17.94%의 CAGR로 성장하고 있습니다. 장비 수요는 중기 업그레이드와 롱리드 도입이 병원의 자본 제약을 상쇄하기 때문에 안정적으로 유지되고 있습니다. 소프트웨어 및 정보학은 과거에는 부수적인 것이었지만, 데이터 해석이 주요 병목현상이 되면서 현재는 프리미엄 지출을 끌어모으고 있습니다. 벤더는 시약의 정기 구매와 AI 기반 분석 도구 및 지원 계약을 결합하여 예측 가능한 수익과 높은 고객 유지율을 보장합니다.

소모품 구매는 더 이상 핵심 시약에 국한되지 않습니다. 연구소에서는 난시료용 특수 추출 키트, 기능 분석용 CRISPR 유전자 편집 소모품, 하이스루풋 연구를 위한 바코드 마이크로플레이트 등을 주문하고 있습니다. 서비스 제공업체는 CLIA 인증 검사, 보험 청구, 의사 대상 보고서를 제공하는 클라우드 포털을 통해 부가가치를 제공하고 있습니다. 병원들은 병원 내 바이오인포매틱스 인력을 증원하지 않고도 검사 결과를 빠르게 처리하기 위해 이러한 모델을 채택하는 경향이 있습니다. 유전체학 시장은 검사 건수의 증가가 소모품, 소프트웨어, 데이터 스토리지에 대한 수요를 견인하고 있기 때문에 수혜를 받고 있습니다.

PCR은 표적 진단 및 병원체 검출에 있어 신속성과 저비용을 실현하기 때문에 2025년 매출의 34.78%를 차지했습니다. 그러나 종합적인 유전체 프로파일링이 일상적인 진료에서 가능해짐에 따라, 시퀀싱 플랫폼은 CAGR 17.22%로 지속적으로 성장하고 있습니다. 롱리드 및 단일 분자 시스템은 구조적 돌연변이 및 메틸화 상태를 한 번의 처리로 검출할 수 있어 숏리드 방법으로는 보완할 수 없었던 임상적 문제를 해결합니다. 한편, 마이크로어레이는 점유율이 계속 낮아지고 있지만, 여전히 대량의 유전자형 분석에 유용합니다.

시퀀싱 업체들은 화학 기술의 다양화를 추진하고 있습니다. Oxford Nanopore는 대상 영역을 실시간으로 선택하는 적응형 샘플링 기술을 제공합니다. 로슈는 2026년까지 고속화 및 고정밀화를 실현할 수 있는 나노포어 기반 SBX 시스템을 준비 중입니다. 긴 리드의 정확도가 향상되고 시약 비용이 감소함에 따라 실험실은 여러 분석을 단일 워크플로우로 통합하여 수작업 시간과 총 지출을 줄일 수 있습니다. PCR은 기기의 견고성, 저비용, 고속이 요구되는 분산형, POC(Point-of-Care)(Point of Care) 애플리케이션에서 여전히 그 가치를 인정받고 있습니다.

북미는 2025년 전 세계 매출의 42.05%를 차지했으며, 선진적인 상환 제도, 대규모 바이오의약품 파이프라인, 성숙한 임상 유전체학 프로그램 등이 뒷받침되고 있습니다. 미국은 국가 코호트 프로젝트와 적극적인 병원 도입으로 대부분의 지출을 주도했습니다. 캐나다는 연방 정밀의료 보조금으로 유전체학을 지원하고, 멕시코는 진단 능력 현대화를 위해 국경을 초월한 협력을 추진하고 있습니다. 지역적 과제로는 복잡한 LDT 규제와 생물정보학자의 부족을 들 수 있으며, 이는 검사실 확장에 걸림돌이 되고 있습니다.

유럽은 정부 지원의 인구 기반 프로그램과 조화로운 규제 경로를 통해 탄탄한 기반을 유지하고 있습니다. 유럽 건강 데이터 공간(EHDS)은 데이터 보호 기준을 충족하면 국경을 초월한 연구를 용이하게 하고, 산학협력을 촉진합니다. 영국의 6억 5,000만 파운드 규모의 노력과 신생아 전장유전체 스크리닝의 보편화는 장기적인 수요를 확고히 하고 있습니다. 독일과 프랑스는 국민건강보험 적용을 통해 임상유전체학을 확대하고 있으며, 남유럽 국가들은 EU 보조금을 활용해 뒤처진 부분을 만회하고 있습니다.

아시아태평양은 2031년까지 CAGR 17.36%로 가장 빠르게 성장하는 지역입니다. 중국의 자급자족 전략, 일본의 정밀의료 보험 적용 코드, 한국의 AI 유전체 클러스터가 주도하고 있습니다. BGI Genomics는 국내 데이터 현지화 규정을 준수하는 결핵 시퀀싱 및 종양학 패널을 확장하고 있습니다. 인도는 확대되는 중산층을 대상으로 저비용 시퀀싱 서비스를 상용화하고, 호주는 연구 역량을 임상 적용으로 전환하고 있습니다. 데이터를 국내에 보관해야 한다는 정부의 의무는 현지 제조를 촉진하고 지역적 승자를 창출하고 있습니다.

라틴아메리카, 중동 및 아프리카는 규모는 작지만 점유율을 확대하고 있습니다. 브라질의 34억 달러 규모의 헬스케어 분야 M&A와 아프리카계 브라질인 집단을 대상으로 한 유전체 연구는 다양한 코호트 연구에 대한 관심을 보여주고 있습니다. 걸프 국가들은 국가 차원의 정밀의료 이니셔티브에 투자하고, 임상 도입을 가속화하기 위해 유럽 및 미국 기술 업체들과 협력하는 사례가 늘고 있습니다. 아프리카 국가들은 시퀀싱 거점 구축과 바이오인포매틱스 교육을 위한 컨소시엄 프로젝트에 참여하여 유전체학 시장이 궁극적으로 종합적인 시장이 될 수 있는 기반을 마련하고 있습니다.

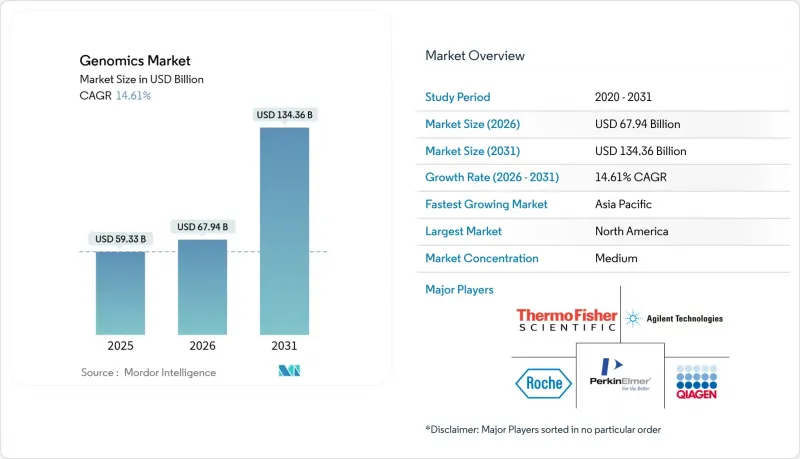

The genomics market was valued at USD 59.28 billion in 2025 and estimated to grow from USD 67.94 billion in 2026 to reach USD 134.36 billion by 2031, at a CAGR of 14.62% during the forecast period (2026-2031).

Declining sequencing costs, population-scale initiatives, and rapid adoption of artificial intelligence position the genomics market for multi-year growth. Sovereign sequencing programs lower per-genome costs toward the USD 200-500 range, while national investments in domestic platforms insulate supply chains and support data sovereignty. Hospitals, pharmaceutical companies, and governments now view genomics as critical healthcare infrastructure rather than an experimental tool, catalyzing spending on instruments, consumables, and cloud analytics. Competitive dynamics continue to tilt toward firms offering integrated hardware-software stacks that reduce turnaround time and support regulatory compliance. Finally, moderated consolidation, anchored by partnerships rather than complete acquisitions, preserves room for innovative entrants that focus on long-read chemistry, AI interpretation, and cloud bioinformatics.

National health systems are adopting universal newborn genome sequencing to shift pediatric care from reactive to predictive. The UK NHS is scaling whole-genome screening, while Singapore's program targets familial hypercholesterolemia. Such initiatives lock in long-term reagent demand for high-throughput sequencers and generate datasets that pharmaceutical companies license for orphan-drug discovery. Analysts project a 10-to-1 economic return from avoided late-stage treatments, reinforcing sustained public funding. Implementation challenges, such as genetic-counselor shortages and secure data storage, drive hospitals toward cloud bioinformatics platforms.

Artificial intelligence turns genomic outputs into longitudinal risk scores and treatment recommendations. Illumina's collaboration with NVIDIA demonstrates how GPU-accelerated algorithms cut secondary-analysis time and improve variant calling precision. US health systems report 30% fewer adverse drug reactions after adding AI-guided pharmacogenomics, while drug makers use multiomic AI to stratify trial populations.Firms fluent in both FDA device regulations and emerging AI governance are winning hospital contracts. Heightened privacy expectations are pushing vendors to adopt homomorphic encryption and federated learning.

The European Health Data Space and China's biosecurity legislation place strict controls on genomic transfers, forcing multinational providers to establish regional data centers and compliant workflows. These parallel infrastructures raise operating costs, slow collaboration, and favor domestically integrated competitors. Smaller firms lack regulatory bandwidth risk exit or acquisition, reinforcing consolidation among globally diversified players.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumables delivered 43.05% of 2025 revenue, underscoring their essential role in daily sequencing workflows. Growth is supported by kit standardization that minimizes batch variability and by automation that speeds library preparation. The services category, supported by sequencing-as-a-service and bioinformatics outsourcing, is expanding at a 17.94% CAGR as laboratories convert capital outlays into operating budgets. Instrument demand remains steady because mid-life upgrades and long-read adoption offset hospital capital constraints. Software & informatics, once an accessory, now attracts premium spend as data interpretation becomes the primary bottleneck. Vendors bundle reagent subscriptions with AI-powered analytics and support contracts, securing predictable revenue and higher customer retention.

Consumable purchasing is no longer limited to core reagents. Labs order specialized extraction kits for challenging samples, CRISPR gene-editing consumables for functional assays, and barcoded microplates for high-throughput studies. Service providers add value with CLIA-certified testing, insurance billing, and cloud portals that deliver physician-ready reports. Hospitals gravitate toward these models to accelerate turnaround time without expanding in-house bioinformatics staff. The genomics market benefits because every incremental test pulls through consumables, software, and data-storage needs.

PCR still accounts for 34.78% of 2025 revenue because it delivers speed and low cost in targeted diagnostics and pathogen detection. Yet, sequencing platforms are expanding at 17.22% CAGR as comprehensive genomic profiling becomes feasible in routine care. Long-read and single-molecule systems detect structural variants and methylation states in one pass, closing clinical gaps left by short-read methods. Meanwhile, microarrays continue to lose ground but remain useful for high-volume genotyping.

Sequencing vendors are diversifying chemistries. Oxford Nanopore offers adaptive sampling that selects regions of interest on the fly. Roche is preparing nanopore-based SBX systems that promise higher speed and accuracy by 2026. As long-read accuracy rises and reagent costs fall, laboratories can consolidate multiple assays into a single workflow, reducing hands-on time and overall spending. PCR retains value in decentralized and point-of-care applications where instruments must be rugged, cheap, and fast.

The Genomics Market is Segmented by Product & Services (Consumables {Reagents, Kits, and More}, Instruments & Systems {NGS Platforms, and More} and More), Technology (PCR, Sequencing, and More), Application (Diagnostics, Drug Discovery and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America held 42.05% of global revenue in 2025, supported by advanced reimbursement, large biopharma pipelines, and mature clinical genomics programs. The United States drives most spending through national cohort projects and aggressive hospital rollouts. Canada supports genomics with federal precision health grants, while Mexico collaborates cross-border to modernize diagnostic capacity. Regional headwinds include complex LDT regulations and shortages of bioinformaticians, which slow laboratory expansion.

Europe retains a strong installed base thanks to government-funded population programs and harmonized regulatory pathways. The European Health Data Space eases cross-border research once data-protection criteria are met, encouraging academic-industry partnerships. The United Kingdom's GBP 650 million commitment and universal newborn genome screening cement long-term demand. Germany and France scale clinical genomics through national insurance coverage, while Southern European countries leverage EU grants to catch up.

Asia Pacific is the fastest-growing region at a 17.36% CAGR to 2031, propelled by China's self-reliance strategy, Japan's precision medicine reimbursement codes, and South Korea's AI-genomics clusters. BGI Genomics expands tuberculosis sequencing and oncology panels that meet domestic data-localization rules. India commercializes low-cost sequencing services for its expanding middle class, and Australia translates research strength into clinical adoption. Government mandates that keep data inside national borders incentivize local manufacturing and create regional winners.

Latin America, the Middle East, and Africa contribute smaller but rising shares. Brazil's USD 3.4 billion in healthcare M&A and genomic studies on African-Brazilian populations underline interest in diverse cohort research. Gulf states are investing in national precision health initiatives, often partnering with Western technology vendors to fast-track clinical readiness. African nations participate in consortium projects that build sequencing hubs and bioinformatics training, ensuring the genomics market eventually becomes more inclusive.