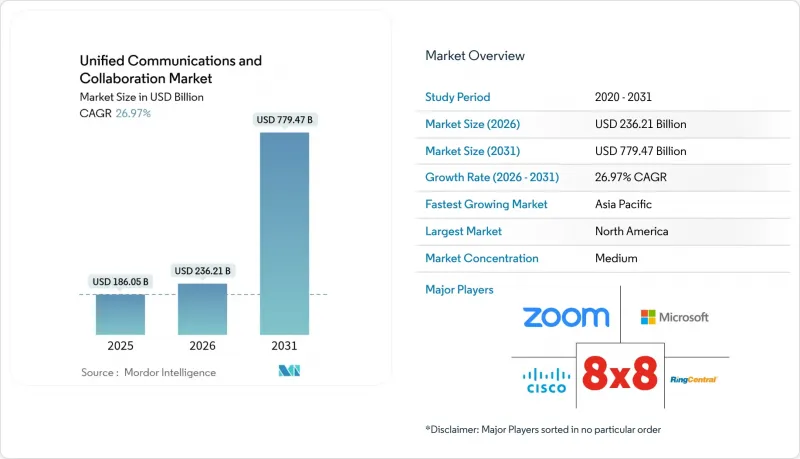

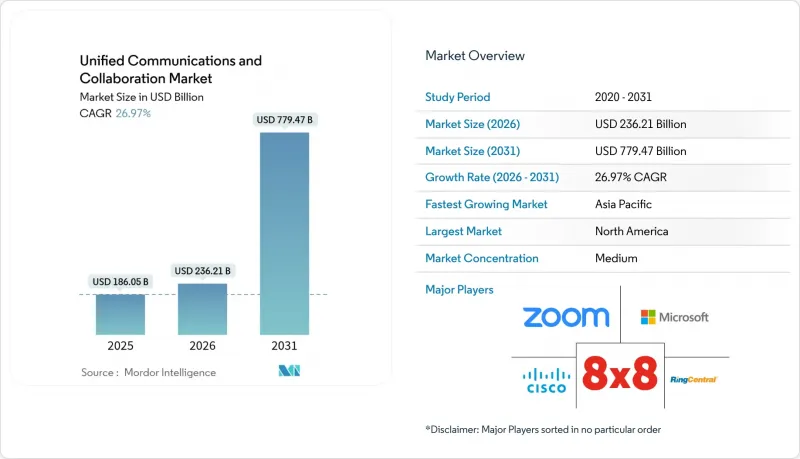

통합 커뮤니케이션 및 협업(UC&C) 시장은 2025년 1,860억 5,000만 달러에서 2026년에는 2,362억 1,000만 달러로 성장하며, 2026-2031년에 CAGR 26.97%로 추이하며, 2031년까지 7,794억 7,000만 달러에 달할 것으로 예측됩니다.

이러한 성장의 원동력은 하이브리드 업무 프로그램의 확대, AI를 통한 생산성 향상 기능, 분산된 음성, 영상, 메시징, 워크플로우 용도를 단일 클라우드 환경으로 통합할 필요성에 기인합니다. 기업은 디지털 전환 예산을 분산된 팀 전체에 걸쳐 직원들의 참여를 높이는 커뮤니케이션 툴로 재분배하고 있습니다. 마이크로소프트, 시스코, 링센트럴 등 기존 기업은 플랫폼의 횡적 깊이로 점유율을 지키고 있는 반면, AI 퍼스트의 도전자들은 틈새 워크플로우의 틈새를 공략하고 있습니다. 전략적 합병(링센트럴의 마이텔 6억 5,000만 달러 인수, 에릭슨의 보나지 62억 달러 인수)은 벤더들이 통합 커뮤니케이션을 컨택센터 기능 및 API 역량과 결합하여 대상 시장을 확대하는 방법을 보여주고 있습니다.

레거시 PBX 시스템을 교체한 기업은 Microsoft Teams Phone으로 워크로드를 전환한 후 유지보수 비용 절감과 가동 시간 향상을 보고하고 있으며, 플로리다 크리스탈스(Florida Crystals)의 경우 통신 비용을 78% 절감했습니다. 캐나다 중견기업의 채용률 증가도 비슷한 궤적을 보이고 있으며, 지역적으로 분산된 직원들에게 클라우드 UC가 효과적이라는 것을 입증하고 있습니다. 음성, 영상, 채팅, 워크플로우 앱을 단일 라이선스로 묶어 제공하는 업체들은 포인트 솔루션을 대체하여 고객 유지율을 높이고 있습니다. 이러한 전환은 클라우드 규모가 부족한 기존 전화 벤더들을 압박하고, 전 세계 배포를 빠르게 실행할 수 있는 UCaaS 전문 업체들의 매출을 증가시키고 있습니다. 북미의 대규모 도입 기반은 이 지역이 새로운 기능 도입의 지표적 역할을 유지하고 있다는 것을 의미합니다.

마이크로소프트의 AI 사업은 팀즈(Teams) 회의, 통화, 메시지에 내장된 코파일럿 서비스를 통해 2025년 2분기 연간 130억 달러의 매출을 달성했습니다. 링센트럴도 마찬가지로 AI 접수 기능을 수익화하여 연간 5,000만 달러 이상의 반복 매출과 1,000개 이상의 고객사를 돌파했습니다. 실시간 전사, 다국어 번역, 자동 회의 요약 기능을 통해 통합 커뮤니케이션은 수동적인 연결에서 능동적인 의사결정 지원으로 진화하고 있습니다. AI를 통한 전화 진료 기능을 도입한 의료기관에서는 예약 불이동률 감소와 대응 시간 단축이 보고되는 등 구체적인 임상적 성과가 입증되고 있습니다. 경쟁의 초점은 기능의 수보다는 추론의 정확성과 원활한 워크플로우 통합으로 옮겨가고 있습니다.

의료 분야의 HIPAA, 결제 분야의 PCI-DSS, 유럽 사용자 데이터의 GDPR(EU 개인정보보호규정)과 같은 규제는 암호화, 감사, 현지화의 추가 계층을 요구하고 도입 기간을 연장시킵니다. 스매쉬는 2025년 2월 콜캐비닛을 인수하여 AI 기반 통화 녹음 및 분석 기능을 아카이브 플랫폼에 통합하여 컴플라이언스 체제를 강화했습니다. 금융 기업은 MiFID II를 준수하기 위해 음성, 영상, 채팅 등 모든 형태의 통신 기록이 의무화되면서 엄격한 벤더 실사 및 전문 컴플라이언스 스택에 대한 요구가 증가하고 있습니다. 엔드투엔드 인증이 없는 공급자는 규제 대상 입찰에서 제외될 위험이 있으며, 매출 기회가 제한될 수 있습니다.

2025년 지출에서 클라우드 서비스는 66.18%를 차지하며 28.55%의 연평균 복합 성장률(CAGR)로 가장 높은 성장 궤도를 유지하며 통합 커뮤니케이션 및 협업(UC&C) 시장의 핵심이 될 것으로 보입니다. 기업이 상각이 완료된 PBX 하드웨어를 단계적으로 폐기함에 따라 클라우드 배포에 있으며, 통합 커뮤니케이션 및 협업(UC&C) 시장 규모가 급성장할 것으로 예측됩니다. 각 벤더들은 고급 암호화 기술, 주권 클라우드 옵션, 업계 템플릿 인증을 지속적으로 추진하고 있으며, 규제 대상 기업조차도 순수한 SaaS 환경을 채택하도록 장려하고 있습니다. 한편, 에어갭 환경이 필수적인 영역에서는 On-Premise형과 호스팅형 모델이 존속하고 있지만, 이들의 총매출 기여도는 매년 감소하는 추세입니다. 하이브리드 아키텍처는 중요한 통화 제어 기능을 온사이트에 유지하면서 탄력적인 워크로드를 클라우드로 확장하여 위험 회피 지향적인 기업에게 전환 기간을 제공함으로써 지지를 받고 있습니다. 향후 5년간 통합 마이그레이션 툴, 제로 터치 디바이스 프로비저닝, 사용자 단위 구독 옵션은 On-Premise 점유율을 더욱 감소시킬 것으로 예측됩니다.

음성/IP 전화는 2025년에도 34.88%의 매출 점유율을 유지하며 영업, 서비스, 사고 대응에 있으며, 실시간 대화에 대한 의존도가 지속되고 있음을 반영하고 있습니다. 그러나 협업/컨텐츠 공유는 27.20%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 채팅, 공동 편집, 화이트보드, 작업 추적을 통합한 멀티 툴 워크스페이스로의 전환이 두드러지게 나타나고 있습니다. 통합 커뮤니케이션 및 협업(UC&C) 시장에서 음성의 점유율은 조직이 비즈니스 용도과 통합된 비동기식 미디어를 선호함에 따라 점차 감소할 것입니다. 통합 커뮤니케이션 및 협업(UC&C) 시장 내에서는 각 벤더들이 문서 공동 편집, 디지털 화이트보드, 상시 연결 채팅을 화상회의에 통합하여 구성 요소의 경계를 모호하게 만들고 있습니다.

북미는 2025년 매출의 25.12%를 차지하며, 통합 커뮤니케이션 플랫폼의 주요 R&D 거점이자 초기 도입 지역으로서의 역할을 강조하고 있습니다. 미국 기업은 클라우드 전환을 가속화하고 있으며, 마이크로소프트의 상용 클라우드 매출은 2025년 3분기 전년 동기 대비 20% 증가한 424억 달러를 넘어섰습니다. 캐나다 중견기업 시장에서는 4분의 3 이상의 중견기업이 도입을 추진하고 있으며, 이는 높은 브로드밴드 보급률과 분산된 근무형태를 반영하고 있습니다. 멕시코의 근해 제조 붐은 국경을 초월한 협업 수요를 증가시키고, UC 스위트내 스페인어 및 영어 지원 서비스를 촉진하고 있습니다.

아시아태평양은 18.05%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국의 클라우드 통신 업체들은 국가 주도의 5G 구축과 기업의 디지털화 추진의 혜택을 누리고 있지만, 데이터 주권 규제로 인해 국내 호스팅 파트너가 우대받고 있습니다. 일본의 5G 투자 로드맵은 2026년까지 4조 3,620억 엔(310억 달러)의 통신 장비 판매를 목표로 하고 있으며, 몰입형 협업 인프라에 대한 지속적인 지출을 예고하고 있습니다. 인도의 Bharat 6G 얼라이언스는 미국 등과의 정부 간 양해각서(MOU)에 힘입어 고 대역폭 용도 대응을 비약적으로 발전시켜 UC 벤더의 장기적인 전체 시장 규모(TAM) 확대를 목표로 하고 있습니다.

The unified communications and collaboration market is expected to grow from USD 186.05 billion in 2025 to USD 236.21 billion in 2026 and is forecast to reach USD 779.47 billion by 2031 at 26.97% CAGR over 2026-2031.

Expanding hybrid-work programs, AI-augmented productivity features, and the need to collapse disparate voice, video, messaging, and workflow applications into a single cloud environment drive this momentum. Enterprises continue reallocating digital-transformation budgets toward communication tools that raise employee engagement across distributed teams. Incumbents such as Microsoft, Cisco, and RingCentral defend share through horizontal platform depth, while AI-first challengers target niche workflow gaps. Strategic mergers-RingCentral's USD 650 million purchase of Mitel and Ericsson's USD 6.2 billion acquisition of Vonage-illustrate how vendors bundle unified communications with contact-center and API capabilities to widen addressable markets.

Enterprises replacing legacy PBX systems report lower maintenance costs and improved uptime after moving workloads into Microsoft Teams Phone, achieving a 78% telecom-expense reduction at Florida Crystals Corporation. Rising adoption rates among Canadian mid-market firms show the same trajectory, validating cloud UC for geographically dispersed staff. Providers that bundle voice, video, chat, and workflow apps on one license displace point solutions and deepen customer stickiness. The shift squeezes traditional telephony vendors that lack cloud scale, bolstering revenue for UCaaS specialists able to execute global roll-outs quickly. Larger install bases in North America mean the region remains the bellwether for new functionality introductions.

Microsoft's AI business exited Q2 2025 at a USD 13 billion annual run rate, driven by Copilot services embedded in Teams meetings, calls, and messages. RingCentral likewise monetizes AI Receptionist capabilities, crossing 1,000 customers with over USD 50 million in annual recurring revenue. Real-time transcription, multilingual translation, and automated meeting summaries move unified communications from passive connectivity to active decision support. Healthcare providers using AI call-triage features report lower no-show rates and faster response times, demonstrating tangible clinical outcomes. Competitive focus now centers on inference quality and seamless workflow integration rather than raw feature counts.

HIPAA for healthcare, PCI-DSS for payments, and GDPR for European user data add encryption, audit, and localization layers that lengthen deployment timelines. Smarsh reinforced its compliance position by acquiring CallCabinet in February 2025, bundling AI-driven call recording and analytics into its archive platform. Financial firms must capture every modality-voice, video, chat-for MiFID II, prompting rigorous vendor due-diligence and driving demand for specialty compliance stacks. Providers without end-to-end certifications risk exclusion from regulated tenders, limiting addressable revenue.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud services represented 66.18% of spending in 2025 and maintain the highest trajectory at 28.55% CAGR, making the segment the nucleus of the unified communications and collaboration market. The unified communications and collaboration market size for cloud deployments is forecast to widen sharply as companies phase out depreciated PBX hardware. Vendors continue to certify advanced encryption, sovereign-cloud options, and industry templates, convincing even regulated firms to adopt pure SaaS footprints. Conversely, on-premises and hosted models persist where air-gapped environments are mandatory, though their collective revenue contribution declines each year. Hybrid architectures gain traction by retaining critical call control on-site while bursting elastic workloads into the cloud, giving risk-averse enterprises a transition runway. Over the next five years, bundled migration tooling, zero-touch device provisioning, and per-user subscription options will further compress the on-premises share.

Voice/IP telephony retained 34.88% revenue share in 2025, reflecting continued reliance on live conversations for sales, service, and incident response. Yet collaboration/content sharing climbs fastest at 27.20% CAGR, underscoring moves toward multitool workspaces that combine chat, co-editing, whiteboarding, and task tracking. The unified communications and collaboration market share for voice will gradually compress as organizations favor asynchronous media that integrates with business applications. Inside the unified communications and collaboration market, vendors embed document co-authoring, digital whiteboards, and persistent chat into video meetings, blurring component boundaries.

The Unified Communications and Collaboration Market is Segmented by Deployment Model (On-premises/Hosted, Cloud), Component (Voice/IP Telephony, Video Conferencing, Messaging and Presence and More), Organization Size (SMEs, Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

North America contributed 25.12% of 2025 revenue, underscoring its role as the primary R&D and early-adopter region for unified communications platforms. U.S. enterprises accelerated cloud migrations as Microsoft's commercial cloud sales surpassed USD 42.4 billion in Q3 2025, up 20% year over year. Canadian mid-market adoption tops three quarters of medium-sized firms, reflecting favorable broadband penetration and distributed workforce patterns. Mexico's near-shoring manufacturing boom increases cross-border collaboration demand, encouraging Spanish-English language services within UC suites.

Asia-Pacific is the fastest-growing territory at an 18.05% CAGR. China's cloud-communications vendors benefit from state-backed 5G roll-outs and enterprise digitization drives, although data-sovereignty rules favor domestic hosting partners. Japan's 5G investment roadmap, targeting JPY 4.362 trillion (USD 0.031 trillion) in telecom equipment sales by FY 2026, signals sustained spending on immersive collaboration infrastructure. India's Bharat 6G alliance, supported by government memoranda of understanding with the United States and others, aims to leapfrog high-bandwidth application readiness, enhancing long-term TAM for UC vendors.