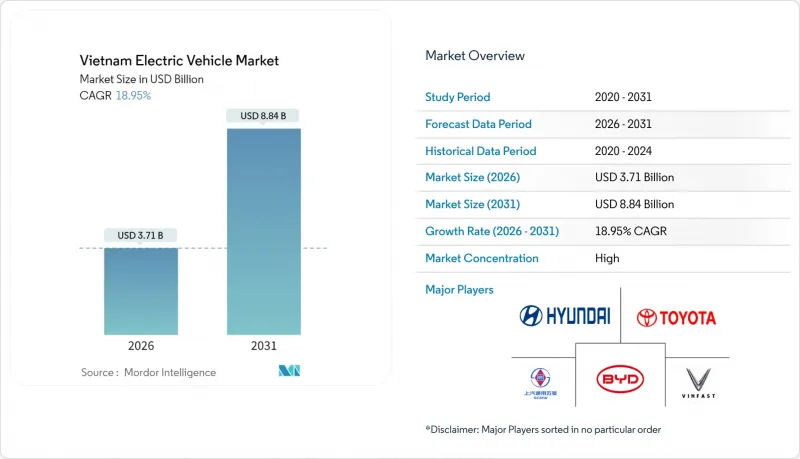

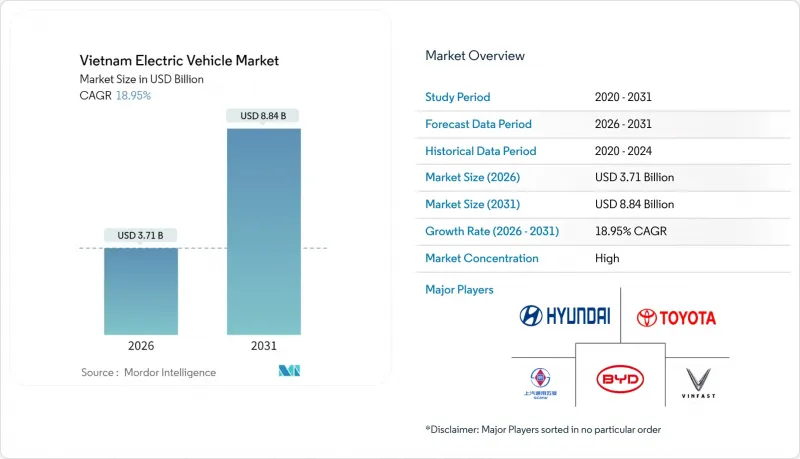

2026년 베트남 전기자동차 시장 규모는 37억 1,000만 달러로 추정되며, 2025년 31억 2,000만 달러에서 성장이 전망됩니다. 2031년까지 예측에서는 88억 4,000만 달러에 달하고, 2026년부터 2031년까지 CAGR 18.95%로 확대될 전망입니다.

수요는 2030년까지 도시지역에서 전기자동차 보급률 50% 달성, 2050년까지 순배출량 제로화라는 정부의 확고한 목표에 의해 촉진되고 있습니다. VinFast의 현지화 추진, 외국 OEM 업체의 공장 설치 계획, 우대 전력 요금이 결합되어 총 소유 비용을 절감하고 보급을 가속화하고 있습니다. 이륜차의 급속한 전동화로 소비자의 인지도가 높아지면서 공유 충전 인프라가 이륜차 시장에도 파급되고 있습니다. 한편, 배터리 팩 가격의 하락으로 인해 LFP 기술은 비용 중심 부문에서 주류가 되고 있습니다. VinFast의 지배적 지위가 가격 경쟁을 억제하고 있기 때문에 경쟁은 여전히 완만하지만, 중국 브랜드와 세계 대중시장용 OEM 업체들이 가격 경쟁력을 갖춘 모델로 진입하고 있어 생태계는 모델 다양화와 가격 하락의 흐름으로 가고 있습니다.

VinFast는 2026년까지 국내 조달률 80%를 목표로 2027년까지 50만대, 2030년까지 연간 100만대 생산을 목표로 하고 있습니다. 이러한 규모 확대로 부품 비용이 압축되고, 환리스크도 감소합니다. Chery와 Geely의 보완적인 노력은 베트남이 지역 조립 기지로서의 입지를 강화하는 반면, 고급 전자제품과 배터리 관리 시스템은 여전히 수입에 의존하고 있습니다. VinFast의 보장된 판매 계약은 현지 공급업체에게 수요 전망을 제공하고, 새로운 자본 투자를 촉진하며, 현지화를 가속화하고 있습니다.

특혜 조치 패키지는 2027년 2월까지 전기자동차 등록비가 면제되고, 아세안 역내에서 생산된 차량에 대한 수입 관세가 0으로 유지되어 대당 1억VND 이상의 구매 가격 인하를 실현할 수 있습니다. 우대 충전 요금(2,204 VND/kWh)은 전기자동차의 총 소유 비용을 더욱 유리하게 만듭니다. 호치민시가 제안한 40만 대 규모의 오토바이 전환 프로그램을 위한 면세 조치와 저금리 대출 등 지방정부의 추가 정책은 다층적인 정책 연계를 강조하고 있습니다. 2027년 이후 지속 여부는 비용 패리티 달성에 달려있기 때문에 시장은 재정정책의 지속 위험에 노출되어 있습니다.

주요 도시에서는 종합적인 반면, 지방에서는 밀도가 빠르게 감소하고 있으며, 도시 간 이동 및 200km 미만 모델의 성장을 제한하고 있습니다.V-Green은 4억 4천만 달러를 추가 스테이션 설치에 투입할 방침이지만, 리드타임으로 인해 단기적으로 병목현상이 지속될 것입니다. 수요가 많은 달에는 전력망에 부하가 발생하여 정부는 전력 공급의 내결함성을 우선시하라는 지시를 내리고 있습니다.

2025년 승용차 시장 규모는 전체의 67.65%를 차지했으며, 버스 부문은 33.11%의 CAGR로 가장 빠르게 성장했습니다. 베트남의 버스용 전기자동차 시장 규모는 지방정부의 도입 의무화로 인해 대규모 입찰이 발생하고 있어 2025년부터 2028년까지 두 배로 증가할 것으로 예상됩니다. 현재 보유 대수의 대부분은 개인 구매자가 보유하고 있지만, 성장 곡선을 주도하는 것은 상업용 차량입니다. 호치민시의 37개 노선에 대한 전기버스 도입 계획과 하노이 중심부의 100% 버스 전동화 계획은 예측 가능한 대량 수요를 창출하고 있습니다.

차량 사용 빈도가 높을수록 총 소유 비용의 이점이 커지기 때문에 상업용 구매자는 차세대 배터리 화학 기술 및 급속 충전 솔루션의 조기 도입자가 될 수 있습니다. 한편, 이륜차는 도시와 지방을 연결하는 출퇴근 수요를 통해 활력을 유지하고, 간접적으로 충전 거점의 경제성을 강화하여 이륜차 보급을 촉진합니다. 예측 기간 동안 버스와 밴이 대중교통 및 라스트 마일 물류 분야에서 정책적으로 주도적으로 점유율을 확대함에 따라 승용차 점유율은 판매량 증가에도 불구하고 완만하게 하락할 것으로 예상됩니다.

2025년 기준 베트남 전기자동차 시장 점유율의 70.82%는 배터리 전기자동차(BEV)가 차지하며 하이브리드 및 플러그인 하이브리드 자동차를 앞질렀습니다. 정부가 과도기적 파워트레인을 뛰어넘는 전략을 추진한 결과, BEV 판매량은 CAGR 27.85%로 증가하며 그 우위는 더욱 강화되고 있습니다. 하이브리드 차량은 주행거리의 유연성을 필요로 하는 교외 통근자를 위한 틈새 수요가 있지만, BEV와의 세제상의 불평등이 성장을 저해하고 있습니다. 연료전지 자동차는 인프라 부족으로 인해 아직 실험 단계에 머물러 있습니다.

VinFast의 헌신적인 BEV 제품 전략은 소비자의 인식을 형성하고, 전국적인 충전 보조금은 순수 전기자동차의 이야기를 강화하고 있습니다. 외국 업체들은 주행거리 불안감을 완화하기 위해 플러그인 하이브리드 차량을 도입할 가능성이 있지만, 정책 방향은 BEV를 주류 노선으로 유지하고 있습니다. 동시에 배터리의 발전으로 충전 시간이 단축되고, 과거 하이브리드 자동차의 프리미엄 가격을 정당화했던 실용적인 제약이 해소되고 있습니다. 종합적으로 볼 때, 베트남의 전기자동차 산업은 선진국 시장에서 볼 수 있는 단계적 하이브리드 자동차로의 전환을 피하고, BEV로 가는 직접적인 경로를 고수하고 있습니다.

The Vietnam electric vehicle market size in 2026 is estimated at USD 3.71 billion, growing from 2025 value of USD 3.12 billion with 2031 projections showing USD 8.84 billion, growing at 18.95% CAGR over 2026-2031.

Demand is propelled by firm government targets that mandate 50% EV penetration in urban areas by 2030 and net-zero emissions by 2050. VinFast's localization drive, foreign OEM factory commitments, and preferential electricity tariffs collectively reduce the total cost of ownership, amplifying adoption. Rapid two-wheeler electrification creates consumer familiarity and shared charging infrastructure that spills over to four-wheelers, while falling battery pack prices allow LFP technology to dominate value-conscious segments. Competition remains moderate because VinFast's dominance deters price wars, yet Chinese brands and global mass-market OEMs are entering with cost-competitive models, nudging the ecosystem toward wider model variety and lower pricing.

VinFast aims for 80% domestic content by 2026, with a goal to produce 500,000 vehicles by 2027 and reach 1 million vehicles annually by 2030, a scale that compresses component costs and mitigates exchange-rate exposure. Complementary commitments from Chery and Geely reinforce Vietnam's standing as a regional assembly hub, yet sophisticated electronics and battery management systems remain import-reliant. Guaranteed offtake contracts from VinFast give local suppliers demand visibility, prompting new capital investment that accelerates localisation.

The incentive package waives registration fees for EVs until February 2027 and keeps import duties at zero on ASEAN-built cars, trimming purchase prices by more than VND 100 million per unit. Preferential charging tariffs of 2,204 VND/kWh further tilt the total cost of ownership in favor of electric models. Provincial add-ons, such as Ho Chi Minh City's proposed tax holidays and soft loans for its 400,000-unit motorcycle conversion program, underscore multi-tier policy coordination. Continuity beyond 2027 depends on reaching cost parity, exposing the market to fiscal-policy rollover risk.

Although dense in tier-one cities, the network thins rapidly in rural corridors, restricting inter-city travel and segment growth beyond sub-200 km models. V-Green has earmarked USD 404 million to deploy additional stations, yet lead times mean near-term bottlenecks persist. Grid stress surfaces during high-demand months, prompting government directives that prioritize power supply resilience.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passenger cars contributed 67.65% of overall revenue in 2025, while buses registered the quickest expansion at a 33.11% CAGR. The Vietnam electric vehicle market size for buses is projected to double between 2025 and 2028 as provincial mandates trigger large tender volumes. Private car buyers account for much of today's stock, yet commercial fleets tip the growth curve; Ho Chi Minh City's 37-route electric bus roll-out and Hanoi's 100% core-area bus electrification agenda inject predictable bulk demand.

Intense fleet utilisation magnifies total-cost benefits, making commercial buyers early adopters of newer battery chemistries and fast-charging solutions. Conversely, two-wheelers retain vitality through rural-urban commuter demand, indirectly bolstering charging-hub economics that benefit four-wheeler deployment. Over the forecast horizon, passenger-car share will erode modestly even as volumes rise, because buses and vans gain policy-driven ground in public transit and last-mile logistics.

Battery electric vehicles captured 70.82% of the Vietnam electric vehicle market share in 2025, eclipsing hybrid and plug-in alternatives. That dominance deepens as BEV volumes compound at 27.85% CAGR, propelled by a government strategy that leapfrogs transitional powertrains. Hybrids hold niche appeal for peri-urban commuters needing range flexibility, but a lack of tax parity with BEVs caps growth. Fuel-cell vehicles remain experimental due to infrastructure voids.

VinFast's single-minded BEV product map shapes consumer perception, while nationwide charging subsidies reinforce the pure-electric narrative. Foreign OEMs may inject plug-in variants to hedge range anxiety, yet policy signals keep BEVs on the mainstream trajectory. In tandem, battery advancements shorten charging times, shaving practical limitations that once justified hybrid premiums. Altogether, the Vietnam electric vehicle industry stays on a direct-to-BEV path, avoiding the incremental hybrid detour seen in developed markets.

The Vietnamese Electric Vehicle Market Report is Segmented by Vehicle Type (Passenger Cars, Commercial Vehicles, and More), Propulsion (Battery Electric Vehicles, Plug-In Hybrid Electric Vehicles, and More), Driving Range (Below 200 Km, 200 To 400 Km, and More), Battery Type (Private Ownership, and More), and Region (Northern Vietnam, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).