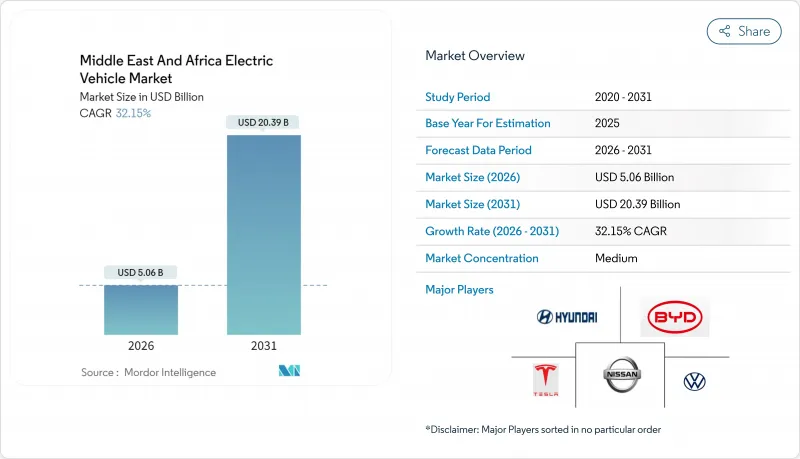

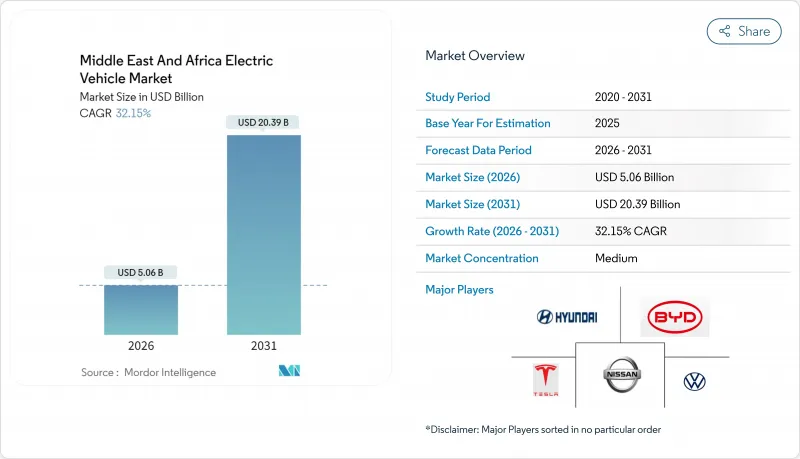

중동 및 아프리카의 전기자동차 시장은 2025년 38억 3,000만 달러로 평가되었으며, 2026년 50억 6,000만 달러, 2031년까지 203억 9,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026년-2031년) CAGR은 32.15%를 나타낼 전망입니다.

정부 펀드는 수십억 달러 규모의 자금을 국내 생산 생태계에 투입하고 있으며, 석유 수출국은 풍부한 태양광 자원을 활용하여 충전 비용을 줄이고 세계 OEM을 유치하고 있습니다. 구속력 있는 탈탄소화 의무, 전지 비용의 저하, 공공 급속 충전 회랑의 정비가 수요의 기세를 뒷받침하는 한편, 중고 내연 기관차(ICE)의 수입이 단기적인 역풍 요인이 되고 있습니다. 승용차는 여전히 최대의 설치 대수를 유지하고 있지만, 석유 및 가스 사업자가 일괄전화 입찰을 실시함에 따라 상용차 플릿이 증가분의 대부분을 차지하게 되고 있습니다. 에너지 대기업과 자동차 제조업체와의 전략적 제휴 및 고온 환경용 배터리의 열 관리 기술 혁신에 의해 이 지역은 극한 고온 하에서의 EV 성능의 기술적 시험장으로서의 지위를 확립하고 있습니다.

걸프 협력 회의(GCC) 회원국은 국가 개발 아젠다에 전기자동차의 도입 할당을 통합하여 OEM 투자 판단의 기초가 되는 수요의 최저 라인을 설정하고 있습니다. 사우디아라비아의 '비전 2030'에서는 2030년까지 리야드 자동차의 30%를 전기자동차로 하는 것을 의무화하고 있으며 UAE의 연방 전략에서는 2050년까지 전기자동차 비율을 50%로 하는 것을 목표로 하고 있습니다. 이 지침은 공공 부문의 조달을 제로 방출 모델로 유도하고, 민간 부문의 차량 전환을 촉진하고, 걸프 표준화기구(GSO)의 규칙에 따라 인증을 표준화하고, 국경을 넘은 거래를 용이하게 합니다. 모로코는 2026년까지 2,500개소의 충전 포인트의 설치를 의무화하고 있으며, 확고한 정책이 인프라의 규모 확대를 가속화시키는 방법을 보여주고 있습니다. 법적 구속력이 있는 목표는 COP28의 약속과 연동하여 투자자들에게 장기적인 전망을 제공함으로써 초기 수요 변동을 보충합니다.

도시 간 고속 충전 회랑은 EV를 도시 지역의 단거리 이동 수단에서 지역 횡단 이동 수단으로 전환합니다. 리야드-카심 고속도로에 설치된 EVIQ사의 주력 150kW 사이트는 간선도로에서의 실용성을 실증하는 것과 동시에, 동왕국에서 가장 교통량이 많은 10개의 간선도로망에의 전개를 예고하고 있습니다. 병행하여 UAE는 2030년까지 아부다비 전역에 7만기의 공공 충전기를 설치할 계획이며, 두바이는 2025년까지 1,000개소의 설치를 목표로 하고 있으며, 수장 국내의 항속 거리 불안을 효과적으로 해소합니다. 모로코에서는 카사블랑카, 라바트, 탄지르를 연결할 계획이 진행되어, 재생에너지로 가동하는 직류 충전 유닛에 의해 30분 미만의 충전을 가능하게 합니다. 나이지리아에서는 2025년 서아프리카 최대급의 충전 허브가 가동 개시되어 신흥 시장에 대한 인프라망이 확대됩니다. 회랑의 충전 밀도 향상은 상용차의 가동 시간을 실질적으로 증가시켜, 제벨 알리 항 등 항만을 거점으로 하는 화물 사업자에 있어서의 전동화를 촉진합니다.

배터리 가격이 하락했음에도 불구하고 구매 가격이 높아 저소득층에서 대중 시장으로의 보급을 막고 있습니다. 이집트에서는 할부 플랜의 한계와 환율 변동 위험을 수반하는 외화 지출 때문에 신차 판매에 차지하는 EV의 비율은 불과 0.1%에 그치고 있습니다. 중고 수입차의 증권화에 익숙한 전통적인 금융기관은 전기자동차 시장용 대출에 잔존가치의 벤치마크가 부족하여 금리 스프레드를 확대하고 있습니다. 서브 사하라 아프리카에서는 마이크로 파이낸싱 메커니즘이 사륜차 구매가 아닌 이륜 택시를 대상으로 하기 때문에 OEM 제조업체에서 규모의 경제 실현이 더욱 늦어지고 있습니다.

2025년 시점에서 배터리형 전기자동차(BEV)가 전기자동차 시장 점유율의 78.64%를 차지했습니다. 이 지역은 완전 전기 구동 시스템을 선호하는 경향을 뒷받침하며 플러그인 하이브리드 자동차의 연료세 관련 복잡성을 피하는 선택입니다. BEV의 매력은 유지 보수의 간편함과 쇼핑몰, 공항, 산업 단지 등에 목적지 충전기의 설치 확대로 인한 것입니다. 이 부문의 견고한 이익률 구조는 테슬라, BYD, 요시리(지리) 등의 제조업체를 끌어들이고, 기존의 딜러망을 우회하는 소비자용 직접 판매 포털 사이트의 시작을 촉진하고 있습니다.

플릿 사업자는 야간 충전에 의한 디포 충전을 채택해, 낮의 업무 중단을 경감하고 있습니다. 연료전지 전기자동차(FCEV)는 사우디아라비아가 산업 회랑 주변에 그린 수소 급유 거점을 확대하는 가운데 2031년까지 연평균 복합 성장률(CAGR) 35.90%를 기록해 장거리 수송 가능성을 부각하고 있습니다. 한편, 플러그인 하이브리드 자동차는 전력망의 신뢰성이 낮은 지역에서 항속 거리의 안전성을 제공하는 과도한 존재로 계속되고 있습니다. 따라서, 구동방식의 구성비는 인프라의 성숙도를 반영하고 있으며, 도시의 걸프 지역에서는 BEV가 우세한 반면, 사막의 화물 수송 루트를 따라 연료전지차가 대두하고 있습니다.

승용차는 2025년 수익의 64.05%를 차지했지만, 중형 및 대형 상용차는 2031년까지 연평균 복합 성장률(CAGR)35.05%로 성장이 가속될 것으로 예측되어 기업 조달 채널에서 전기자동차 시장 규모를 확대시킵니다. 유전 서비스용 트럭과 마지막 마일 배송 밴은 일일 주행 거리가 길기 때문에 연료비 절감과 탄소 감사상의 이점이 현저합니다. 제다 자유무역지역의 물류기업은 항만 당국의 배출규제에 대응하기 위해 입찰로 전기모델을 지정하게 되었습니다. 카이로와 케이프 타운의 버스 전동화의 파일럿 사업은 대중 교통 수요 증가를 나타내고 있으며, 라이드 셰어링 사업자는 도심부의 클린 에어 규제 대응을 위해 소형 해치백 EV를 도입하고 있습니다. OEM 각사는 지역 특화형의 적재량 규격, 강화된 캐빈 공조 시스템, 비포장로 대응의 강화 서스펜션으로 대응하고 있습니다. 상용차 판매량이 증가함에 따라 트럭 바디, 배터리 케이스, 텔레매틱스 서비스가 국내 조달 가능해지기 때문에 공급망의 현지화가 심화되고 있습니다.

The electric vehicle market in the Middle East and Africa was valued at USD 3.83 billion in 2025 and estimated to grow from USD 5.06 billion in 2026 to reach USD 20.39 billion by 2031, at a CAGR of 32.15% during the forecast period (2026-2031).

Sovereign wealth funds are directing multibillion-dollar allocations toward domestic production ecosystems, and oil-exporting nations are leveraging abundant solar resources to lower charging costs and attract global original-equipment manufacturers (OEMs). Binding decarbonization mandates, falling battery costs, and the rollout of public fast-charging corridors reinforce demand momentum even as used internal-combustion-engine (ICE) imports remain a short-term headwind. Passenger cars retain the most extensive installed base, yet commercial fleets increasingly dominate incremental volume as oil-and-gas operators issue bulk electrification tenders. Strategic partnerships between energy majors and automakers and hot-climate battery-thermal innovations are positioning the region as a technical test bed for extreme-heat EV performance.

Gulf Cooperation Council (GCC) members have embedded electric-mobility quotas into national development agendas, creating demand floors that anchor OEM investment decisions. Saudi Arabia's Vision 2030 compels 30% of Riyadh's vehicles to be electric by 2030, while the UAE's federal strategy targets a 50% electric-vehicle mix by 2050. These directives funnel public-sector procurement toward zero-emission models, catalyze private-sector fleet conversions, and standardize certification under Gulf Standardization Organization (GSO) rules, which ease cross-border trade. Morocco's mandates 2,500 charging points by 2026, illustrating how firm policy anchors accelerate infrastructure scale-up. Binding targets dovetail with COP28 commitments, giving investors long-cycle visibility, compensating for initial demand volatility.

Intercity fast-charging corridors convert EVs from urban runabouts into region-wide mobility options. EVIQ's flagship 150 kW site on the Riyadh-Qassim motorway demonstrates highway viability and signals forthcoming coverage of the kingdom's 10 busiest arterial routes. In parallel, the UAE plans 70,000 public chargers across Abu Dhabi by 2030, while Dubai targets 1,000 sites by 2025, effectively eliminating intra-emirate range anxiety. Morocco's plan links Casablanca, Rabat, and Tangier with green-energy-powered DC units that supply sub-30-minute stops. Nigeria's 2025 inauguration of West Africa's largest assembled charging hub widens the infrastructure map to frontier markets. Corridor density materially lifts commercial-vehicle uptime, unlocking electrification for freight operators serving ports such as Jebel Ali.

Purchase-price premiums continue to deter mass-market adoption in lower-income segments even as batteries cheapen. Egypt's EV share remains just 0.1% of new-car sales due to limited installment plans and hard-currency outlays that expose buyers to exchange-rate swings. Traditional lenders, accustomed to securitizing used imports, lack residual-value benchmarks for electric vehicle market loans, inflating interest spreads. In Sub-Saharan Africa, microfinance mechanisms target two-wheeler taxis rather than four-wheeler purchases, further stalling scale economics for OEMs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Battery-electric vehicles (BEVs) commanded 78.64% of the electric vehicle market share in 2025, validating the region's preference for fully electric drivetrains and sidestepping the fuel-duty complexity of plug-in hybrids. BEV appeal stems from simpler maintenance and the rollout of destination chargers at malls, airports, and industrial parks. The segment's robust margin structure has enticed Tesla, BYD, and Geely to launch direct-to-consumer sales portals that bypass traditional dealerships.

Fleet operators adopt BEVs for depot-night charging, reducing daytime operational disruptions. Fuel-cell electric vehicles post a 35.90% CAGR through 2031 as Saudi Arabia scales green-hydrogen refueling nodes around its industrial corridors, underscoring their long-haul potential. Meanwhile, plug-in hybrids remain transitional, offering range security where grid reliability lags. The drive-type mix therefore mirrors infrastructure maturity, with BEVs prevailing in the urban Gulf and fuel-cells rising along desert freight links.

Passenger cars controlled 64.05% of 2025 revenue, yet medium and heavy commercial vehicles are forecast to outpace with a 35.05% CAGR to 2031, expanding the electric vehicle market size in corporate procurement channels. Oil-field service trucks and last-mile delivery vans accrue higher daily mileage, magnifying fuel savings and carbon audit benefits. Logistics firms in the Jeddah free zone now specify electric models in tenders to comply with port authority emissions limits. Bus electrification pilots in Cairo and Cape Town indicate growing public-transport appetite, while ride-hailing operators deploy small hatchback EVs to meet city-center clean-air mandates. OEMs are responding with region-tuned payload ratings, enhanced cabin HVAC, and reinforced suspensions for unpaved routes. As commercial volumes climb, supply-chain localization deepens because truck bodies, battery enclosures, and telematics services can all be sourced domestically.

The Middle East and Africa Electric Vehicle Market Report is Segmented by Drive Type (Battery-Electric, Plug-In Hybrid, and Fuel-Cell Electric), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, and Others), Charging Level (AC Below 7 KW, and More), and by Country. Market Forecasts are Provided in Terms of Value (USD).