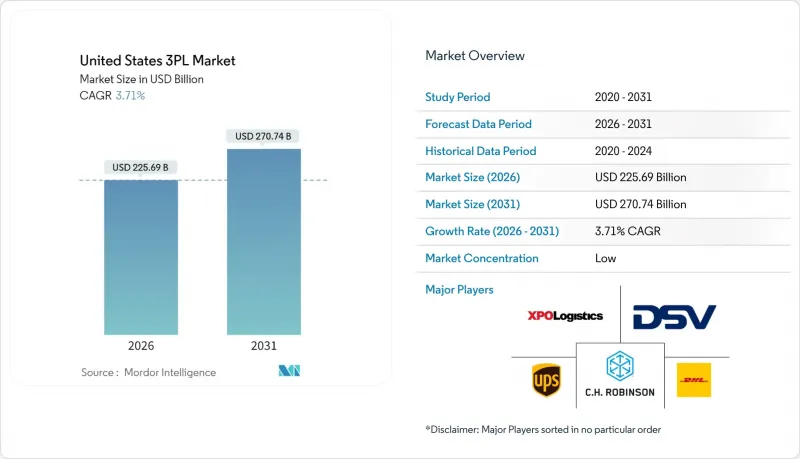

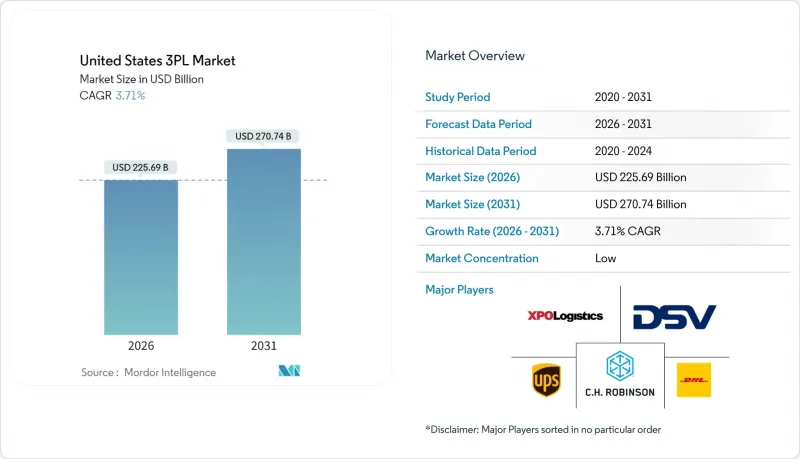

미국의 제3자 물류(3PL) 시장은 2025년 2,176억 2,000만 달러에서 2026년에는 2,256억 9,000만 달러로 성장하고, 2026년부터 2031년까지 CAGR 3.71%를 기록하며 2031년까지 2,707억 4,000만 달러에 달할 것으로 예측됩니다.

시장의 꾸준한 확대는 산업의 성숙, 지속적인 공급망 복잡화, 생산과 유통을 국내 소비자에게 더 가까이 가져다주는 니어쇼어링의 지속을 반영합니다. 제조업 고객은 여전히 핵심 부문이지만, 의료, E-Commerce, 기술 분야의 화주가 현재 가장 빠른 매출 증가의 원천이 되고 있습니다. 공급업체들은 노동력 부족과 연료 가격 변동에 대응하기 위해 자동화, 창고 로봇, 시각화 소프트웨어에 자본을 재분배하고 있습니다. 수십억 달러 규모의 인수합병으로 업계 재편이 가속화되는 가운데, 불확실한 화물 수요 사이클에서 하이브리드 자산 전략은 위험 분산을 위해 노력하고 있습니다. 화주와 제3자 물류(3PL) 사업자 간 파트너십 성공률이 83%까지 떨어졌다는 사실은 미국 3PL 시장의 경쟁과 성과에 대한 기대치가 높아졌음을 보여줍니다.

지속적인 온라인 지출(2024년 9.3% 증가)은 고밀도 전국 배송 네트워크에 대한 수요를 뒷받침하고, DHL 공급망이 IDS 풀필먼트(130만 평방피트 용량 증가)를 인수하는 계기가 되었습니다. 브랜드 기업들은 배송기간 단축을 위해 연안 지역의 거대 물류센터에서 지방 시장의 마이크로 풀필먼트 거점으로 유통망을 분산시키고 있습니다. 리버스 물류의 복잡성이 증가함에 따라 DHL이 인머 서플라이 체인 솔루션즈(Inmer Supply Chain Solutions)를 인수하여 북미 최대 규모의 반품 플랫폼이 탄생했습니다. 이를 통해 공급자는 순환형 상거래에서 이익을 얻을 수 있는 기회를 얻었습니다. 자동화 및 자율 배송의 시범 운영은 라스트 마일의 비용 구조를 지속적으로 변화시키고 있으며, 민첩한 전문 공급업체에게 더 많은 기회를 제공하고 있습니다. 이러한 추세와 함께 미국 제3자 물류 시장은 다년간 견고한 성장 기반을 유지하고 있습니다.

화주기업은 물류관리보다 제품개발에 집중하고, 실행위험을 규모 있는 3PL 사업자에게 이전하고 있습니다. C.H. 로빈슨의 매니지드 솔루션 플랫폼은 TMS, 3PL, 4PL 서비스를 통합하고 연간 3,500만 건의 운송 실적을 활용하여 비용 절감과 가시성 향상을 실현합니다. 운전자금 압박으로 인해 제조업체의 80%가 재고를 재조정해야 하는 상황이며, 이는 고부가가치 서비스(VAS) 창고에 대한 수요를 더욱 확대시키고 있습니다. 이러한 구조적 변화는 미국 제3자 물류 시장의 서비스 범위와 수익원을 확대하고 있습니다.

업계 단체는 향후 10년간 120만 명의 운전자 부족이 발생할 것이라고 경고하고 있으며, 이는 인건비 증가와 서비스 신뢰도 하락을 초래하고 있습니다. 창고 업계도 비슷한 인력 부족에 직면하고 있으며, 화주의 78%가 지속적인 채용난으로 인해 처리 능력이 저하되고 있다고 보고했습니다. XPO의 LTL 2.0 직원 참여 전략은 만족도 점수를 40% 향상시켰고, 정착률 향상을 위한 문화적 요인을 제시합니다. 또한, 공급업체들은 자동화 및 안전 규제 확대에 대응하기 위해 기술 향상 프로그램을 확장하고 있습니다. 자동화가 완전한 규모에 도달할 때까지 노동력 부족은 미국 제3자 물류 시장에서 가장 큰 걸림돌로 작용할 것입니다.

2025년 기준, 국내 운송 관리는 미국 제3자 물류 시장 점유율의 47.55%를 차지하여 화물 조정이 여전히 기본 서비스임을 보여줍니다. 예측 가격 책정 도구, 노선 밀도 분석, 멀티모달 최적화가 경쟁 우위를 형성하여 운송업체가 마진을 희생하지 않고 변동이 심한 현물 시장에서 살아남을 수 있도록 지원합니다. 한편, 부가가치형 창고 및 유통 서비스는 CAGR 7.55%로 확대되고 있으며, EC 판매자의 재고 이월, 키트화, 라벨링, 당일 마감 대응에 대한 수요 증가에 따라 전략적 중요성이 커지고 있습니다. C.H. 로빈슨의 '매니지드 솔루션' 제품군은 이러한 기능을 하나의 대시보드에 통합하여 미국 제3자 물류 시장을 특징짓는 서비스 아키텍처의 융합을 구현하고 있습니다.

창고 투자는 콜드체인 확장에도 연동되어 있습니다. DHL, UPS, AmeriCold는 2-8℃ 존과 GDP 인증 대응을 갖춘 FDA 준수 시설 건설에 박차를 가하고 있습니다. 의류 및 전자제품 반품 수요에 힘입어 리버스 물류 부문은 서비스 포트폴리오에 새로운 차원을 더하고 있습니다. 한편, 국제 운송 관리는 무역 정책 및 해상 화물 할증료에 따른 운송 능력의 변동에 직면하면서도 근해 공장에 원자재 공급을 담당하는 세계 공급망에서 그 중요성이 유지되었습니다. 종합적으로 볼 때, 번들형 서비스 모델은 미국 제3자 물류 업계 전반의 고객 유지율을 높이고 지속적인 수익률 다각화를 지원하고 있습니다.

The United States 3PL Market is expected to grow from USD 217.62 billion in 2025 to USD 225.69 billion in 2026 and is forecast to reach USD 270.74 billion by 2031 at 3.71% CAGR over 2026-2031.

The steady expansion of the market reflects the sector's maturation, persistent supply-chain complexity, and ongoing nearshoring that pulls production and distribution closer to domestic consumers. Manufacturing customers remain the anchor segment, yet healthcare, e-commerce, and tech shippers now supply the fastest incremental revenue streams. Providers continue reallocating capital toward automation, warehouse robotics, and visibility software to counter labor scarcity and fuel price volatility. Consolidation accelerates through billion-dollar acquisitions while hybrid asset strategies spread risk in an uncertain freight-demand cycle. Competitive intensity, measured by a declining 83% shipper-3PL partnership success rate, underscores rising performance expectations in the United States third-party logistics market.

Persistent online spending-up 9.3% in 2024-anchors demand for dense national fulfillment networks, prompting DHL Supply Chain's acquisition of IDS Fulfillment that added 1.3 million sq ft of capacity. Brands diversify distribution away from coastal mega-centers toward micro-fulfillment nodes in secondary markets to compress delivery windows. Reverse-logistics complexity rises; DHL's Inmar Supply Chain Solutions deal created the largest North American returns platform, positioning providers for margin capture in circular commerce. Automation and autonomous delivery pilots continue reshaping last-mile cost structures, expanding opportunity for nimble specialists. Collectively, these dynamics keep the United States third-party logistics market on a firm multiyear growth footing.

Shippers concentrate on product development rather than logistics administration, transferring execution risk to scaled 3PLs. C.H. Robinson's Managed Solutions platform unifies TMS, 3PL, and 4PL services, leveraging 35 million annual shipments to deliver cost and visibility gains. Working-capital pressures push 80% of manufacturers to rebalance inventory, which in turn amplifies demand for sophisticated VAS warehousing. These structural shifts widen the service scope-and revenue pool-inside the United States third-party logistics market.

Industry groups warn of a 1.2 million-driver deficit over the next decade, inflating wage bills and straining service reliability. Warehouses face similar scarcity, with 78% of shippers reporting persistent recruitment hurdles that cut into throughput. XPO's LTL 2.0 employee-engagement playbook lifted satisfaction scores 40%, hinting at cultural levers for retention. Providers also expand upskilling programs to meet growing automation and safety mandates. Until automation reaches full scale, labor scarcity remains the single largest drag on the United States third-party logistics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Domestic Transportation Management held 47.55% of the United States third-party logistics market share in 2025, showing that freight orchestration remains the bedrock service offering. Predictive pricing tools, lane-density analytics, and multimodal optimization now shape competitive positioning, enabling carriers to navigate volatile spot markets without surrendering margin. Conversely, Value-Added Warehousing & Distribution, advancing at 7.55% CAGR, is gaining strategic heft as e-commerce sellers demand inventory postponement, kitting, labeling, and same-day cutoffs. C.H. Robinson's Managed Solutions suite fuses these functions on a single dashboard, showcasing the converging service architecture that characterizes the United States third-party logistics market.

Warehouse investments also track cold-chain expansion: DHL, UPS, and Americold accelerated builds of FDA-compliant facilities with 2-8 °C zones and GDP-certified handling. Reverse-logistics units, fueled by apparel and electronics returns, added another dimension to service portfolios. Meanwhile, International Transportation Management battled capacity swings tied to trade policy and ocean-freight surcharges, yet retained relevance for global supply chains funneling inputs into nearshore plants. Altogether, bundled service models strengthen stickiness across the United States third-party logistics industry and support ongoing margin diversification.

The United States 3PL Market Report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End User (Automotive, Energy and Utilities, Manufacturing, and More), by Logistics Model (Asset-Light, Asset-Heavy, Hybrid), and by Region (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).