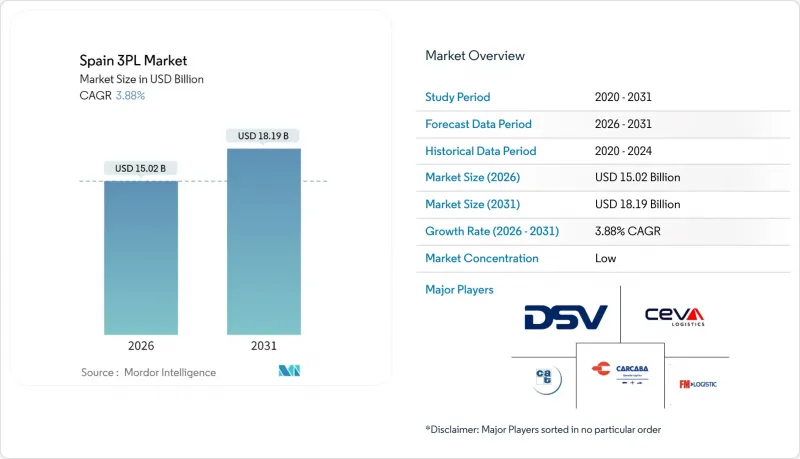

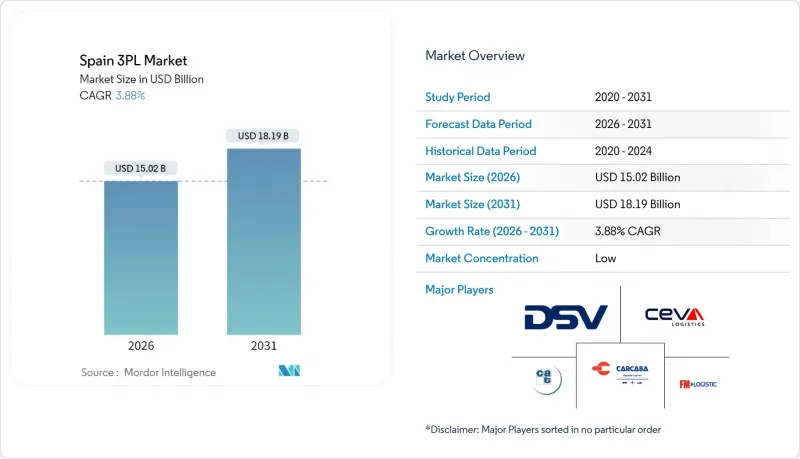

스페인의 제3자 물류(3PL) 시장은 2025년에 144억 6,000만 달러로 평가되었고, 2026년 150억 2,000만 달러에서 2031년까지 181억 9,000만 달러에 이를 것으로 예측됩니다.예측 기간(2026-2031년) CAGR은 3.88%로 전망됩니다.

유럽의 관문으로서 스페인의 역할, 아웃소싱을 통한 이행의 급속한 전환, 멀티모달 회랑의 업그레이드가 이러한 상승 추세를 뒷받침하고 있습니다. 마드리드와 바르셀로나를 넘어선 전자상거래의 지리적 확장, 북유럽의 견고한 니어쇼어링 유입, 정부 지원 철도 전기화 프로젝트가 결합되어 제3자 물류 서비스 제공업체의 잠재 고객 기반을 확대하고 있습니다. 디지털 세제 혜택으로 AI를 활용한 경로 최적화가 촉진되는 한편, 그린 모빌리티 정책이 전기차를 통한 도심 배송 수요를 자극하고 있습니다. 국내 및 다국적 운송업체 간 경쟁 심화는 가격 투명성을 가속화하고, 부가가치형 창고 관리, 실시간 가시화 플랫폼, 자본 위험을 완화하는 자산 라이트형 제휴의 보급을 촉진하고 있습니다.

스페인의 온라인 구매자 수는 2025년까지 4,000만 명에 달할 것으로 예상되며, 전국적인 계약 이행 파트너에 대한 의존도는 더욱 높아질 것으로 예측됩니다. 아마존이 아스투리아스 지방에 건설한 3억 2,700만 달러 규모의 물류센터는 48시간 배송 보장이 요구하는 인프라 규모의 대표적인 예입니다. 이에 반해 써드파티 업체들은 인구 밀집 지역과 가까운 곳에 재고를 배치하는 마이크로 풀필먼트 허브를 통해 대응하고 있습니다. 바르셀로나의 경우, 현재의 소포 처리량을 감당하기 위해 1,000개 이상의 도시형 거점이 필요하다는 조사 결과가 이러한 변화를 뒷받침하고 있습니다. 로봇 기술을 활용한 분류 라인과 AI 기반 슬로팅 솔루션은 성수기의 풀필먼트 사이클 시간을 더욱 단축할 수 있습니다. 그러나 배송 빈도가 증가함에 따라 3PL 사업자는 간선 경로를 재설계할 수밖에 없습니다. 이를 통해 대용량 트레일러가 야간에 도심지 창고에 보충을 함으로써 낮 시간대 교통체증 비용을 절감하고 있습니다.

백신 유통 확대, EU의 식품 안전 규제 강화, 소비자의 신선식품 선호도 변화 등이 맞물리면서 스페인의 콜드체인 이용이 확대되고 있습니다. 슈미츠카고가 스페인의 텔레매틱스 기업 아틀란티스 월드 시스템즈(Atlantis World Systems)를 인수한 사례는 트레일러 제조업체가 센서 네트워크를 통합하여 적재물 측정값을 엔드 투 엔드 검증할 수 있도록 하려는 노력을 보여줍니다. AI 수요 예측이 운송 용량 계획의 기반이 되어, 냉장 운송 용량을 고정 계약이 아닌 동적으로 할당할 수 있게 되었습니다. 이를 통해 에너지 가격 변동에도 불구하고 수익률을 유지하고 있습니다. 의약품 분야에서는 적정유통규범(GDP) 준수가 GDP 인증 보관구역의 프리미엄 요금을 견인하고 있으며, 치열한 경쟁 환경에서도 수익기반을 방어하고 있습니다. 새로운 통제된 대기실은 농산물 수출의 선택권을 넓히고, 지중해산 신선식품의 북쪽으로의 운송에 있어 보존 기간을 연장할 수 있습니다. 블록체인 시범 운영은 변조 불가능한 추적성을 추가하고, 스페인 규제 당국의 콜드체인 감사 강화에 따라 필수적인 기능이 되었습니다.

연료비는 도로화물 운송 총비용의 약 4분의 1을 차지하며, 2025년 가격 변동으로 인해 법정 할증 조항이 있더라도 수익률은 낮은 수준입니다. 마드리드-파리 간 계약 운임은 2024년 4분기 환율 환산 후 1,588달러로 3.5% 상승하여 회복 국면의 취약성을 보여주었습니다. 운송회사는 요금소, 교통상황, 주유소 등을 고려한 동적 경로를 채택하여 일률적인 요금 인상을 피하면서 서비스 수준 계약을 유지하고 있습니다. 차량 소유주들은 정부 보조금을 활용하여 에너지 의존도를 분산시키기 위해 고 수요 노선에서 LNG 트럭과 하이브리드 트럭을 시험 운행하고 있습니다. 그러나 지속적인 변동성으로 인해 화주들은 예산 계획의 예측 가능성을 위해 철도 운송에 대한 검토를 가속화하고 있으며, 이는 스페인의 제3자 물류 시장에서 장거리 트럭 운송 수요를 다소 억제하는 요인으로 작용하고 있습니다.

국내 운송 관리는 2025년 52.48%의 매출 점유율을 유지하며 스페인의 간선도로 중심의 화물 운송 패턴과 전국적인 밀크런(집배송) 스케줄의 지속적 필요성을 뒷받침하고 있습니다. 스페인의 부가가치 창고 및 유통 서비스 분야의 제3자 물류 시장 규모는 다른 서비스 라인보다 높은 CAGR 7.42%로 확대될 것으로 예측됩니다. 전자상거래 반품 처리, 커스터마이징, 키트화 업무가 증가함에 따라 창고 운영자는 자동 분류기, 음성 피킹 시스템, 카톤 적정 크기화 기계 도입을 추진하고 있습니다. 한편, 지중해 항구의 개보수를 통한 수송능력 강화를 배경으로 국제 운송관리가 가속화되고 있습니다. 이를 통해 마그레브 지역의 무역이 스페인 북부 물류 거점으로 유입되고 있습니다. CEVA 물류의 타라고나 시설(18,000m2)은 태양광 발전 지붕, LED 조명과 같은 지속가능성 부가가치가 계약 체결의 필수 조건이 되고 있는 현실을 보여줍니다.

주정부의 전기화 보조금에 힘입어 화물철도의 부활은 출발지와 도착지에서의 트럭 운송이 철도 중거리 운송을 끼고 있는 통합 서비스 패키지를 만들어내고 있습니다. 항공화물 취급량은 톤수 기준으로는 작지만, 2-8℃의 온도 관리 경로를 요구하는 생명과학 분야 화주에게 매력적인 수익률을 제공합니다. 벌크 상품은 연안 저속선이나 컨테이너 터미널을 통해 운송되지만, 옴니채널 소매업체들이 클릭 한 번으로 한 시간 이내에 방문 배송을 요구함에 따라 많은 제3자 물류(3PL) 업체들은 통관 및 무역 금융 서류 작성 서비스를 교차 판매하여 순수 톤당 가격보다 더 많은 수익을 창출하고 있습니다. 수수료 이상의 수익 향상을 도모하고 있습니다. 또한, 기존 DC(물류센터) 내에 마이크로 풀필먼트 기능을 추가하는 사례가 증가하고 있으며, 이는 스페인의 제3자 물류 시장 계약에서 재고의 근접성을 중시하는 경향을 뒷받침하고 있습니다.

The Spain 3PL Market was valued at USD 14.46 billion in 2025 and estimated to grow from USD 15.02 billion in 2026 to reach USD 18.19 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031).

Spain's role as a European gateway, the rapid shift toward outsourced fulfillment, and multimodal corridor upgrades underpin the upward trajectory. E-commerce's geographic spread beyond Madrid and Barcelona, resilient nearshoring inflows from Northern Europe, and government-backed rail electrification projects jointly widen the addressable base for third-party logistics service providers. Digital tax incentives now reward AI-enabled route optimization while green-mobility policies raise demand for electric urban fleets. Heightened competition among domestic and multinational carriers accelerates pricing transparency and forces broader adoption of value-added warehousing, real-time visibility platforms, and asset-light alliances that de-risk capital exposure.

Spain's online buyer base is expected to climb toward 40 million users in 2025, solidifying nationwide reliance on contracted fulfillment partners. Amazon's USD 327 million logistics center in Asturias typifies the infrastructure scale now demanded by 48-hour delivery guarantees. Third-party providers respond with micro-fulfillment hubs that position inventory nearer to dense consumer pockets, a shift illustrated by studies showing Barcelona needs more than 1,000 such urban sites to meet current parcel volumes. Robotics-enabled sortation lines and AI-driven slotting solutions further compress fulfillment cycle times during peak shopping seasons. Greater delivery frequency, however, compels 3PLs to redesign trunk routes so that high-capacity trailers replenish urban depots overnight, mitigating daytime congestion costs.

Heightened vaccine distribution, stricter EU food-safety rules, and a switch to fresh consumer habits combine to lift Spain's cold-chain utilization. Schmitz Cargobull's acquisition of Spanish telematics firm Atlantis Global System demonstrates how trailer makers are embedding sensor networks to keep payload readings verifiable end-to-end. AI demand forecasting now underpins capacity planning so that refrigerated slots are allocated dynamically rather than by static contracts, preserving margins despite energy-price volatility. On the pharmaceutical side, compliance with Good Distribution Practice drives premium tariffs for GDP-certified storage zones, offering revenue defense in an otherwise price-competitive landscape. Emerging controlled-atmosphere chambers broaden produce export options, extending shelf life for Mediterranean perishables shipped northward. Blockchain pilots add immutable traceability, an essential feature as Spanish regulators intensify random cold-chain audits.

Fuel accounts for about one-quarter of total road freight expense, and 2025 volatility keeps margins thin despite statutory surcharge clauses. Madrid-Paris contract rates climbed 3.5% in Q4 2024 to USD 1,588 after currency conversion, illustrating the fragile rebound phase. Carriers resort to dynamic routes that weigh tolls, traffic, and refueling points so service-level agreements remain intact without blanket price hikes. Fleet owners test LNG and hybrid trucks on high-volume corridors, leveraging government subsidies to diversify energy exposure. Persistent variability nevertheless prompts shippers to explore rail for predictable budget planning, moderately dampening Spain third-party logistics market demand for long-haul trucking.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Domestic Transportation Management retained a 52.48% revenue slice in 2025, underscoring Spain's highway-centric freight patterns and the enduring need for nationwide milk-run schedules. Spain third-party logistics market size for Value-Added Warehousing & Distribution is projected to expand at 7.42% CAGR, faster than any other service line. Rising e-commerce returns handling, customization, and kitting tasks push warehouse operators to embed automated sorters, pick-by-voice, and carton right-sizing machines. Meanwhile, International Transportation Management accelerates on the back of refurbished Mediterranean port capacity that funnels Maghreb trade into northern Spain depots. CEVA Logistics' 18,000 m2 Tarragona facility illustrates how sustainability add-ons-photovoltaic roofing and LED lighting-are now table stakes for contract awards.

The resurgence of freight rail, spurred by state electrification grants, sparks integrated service packages where truck drayage at origin and destination bookends a rail middle-haul. Air freight volumes, though minor by tonnage, yield attractive margins for life-science shippers demanding two-to-eight-degree routings. Bulk commodities funnel through coastal Ro-Ro and container terminals, yet many 3PLs cross-sell customs clearance and trade-finance documentation to lift yields above pure tonnage fees, as omnichannel retailers seek one-hour click-to-door delivery, micro-fulfillment add-ons inside legacy DCs proliferate, validating the premium placed on inventory proximity in Spain third-party logistics market contracts.

The Spain Third-Party Logistics (3PL) Market Report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End User (Automotive, Energy & Utilities, Manufacturing, Life Sciences & Healthcare, Technology & Electronics, E-Commerce, and More), and by Logistics Model (Asset-Light, Asset-Heavy, Hybrid). The Market Forecasts are Provided in Terms of Value (USD).