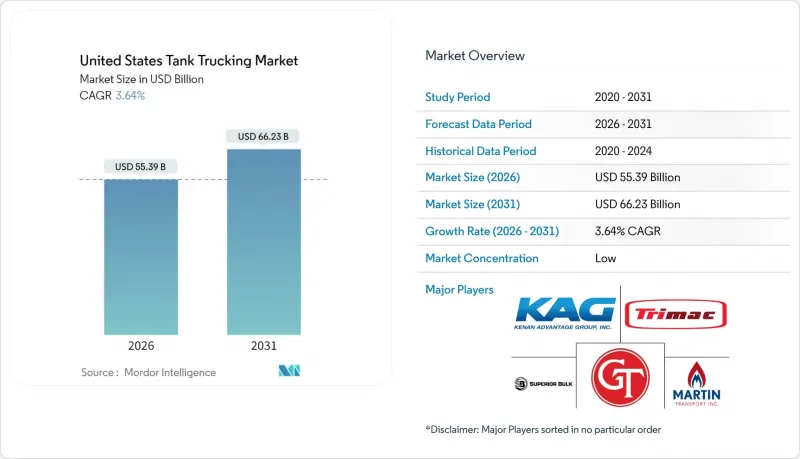

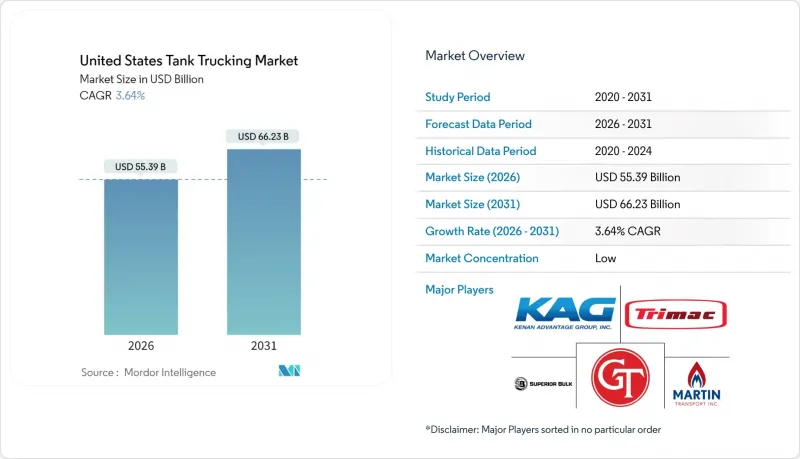

미국의 탱크 트럭 운송 시장 규모는 2026년에 553억 9,000만 달러로 추정되며, 2025년 534억 5,000만 달러에서 성장이 전망됩니다.

2031년에는 662억 3,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 3.64%로 성장할 것으로 전망됩니다.

이러한 지속적인 확장은 변화하는 에너지 믹스, 강화되는 안전 규제, 변동하는 투입 비용에 대한 적응력을 반영하고 있습니다. 재생 디젤, 특수 화학제품, 온도관리 식품원료의 운송량 증가로 화물 기반이 확대되는 한편, 디지털 배차 도구와 경량 탱크 사양이 자산 생산성 향상을 촉진하고 있습니다. 한편, 운전자 부족, 위험물 규제 위반 처벌, 자율주행 트럭의 시범 도입 등의 과제는 운영 경제성을 압박하고 있으며, 운송 사업자에게 노선 설계, 차량 구성, 자본 계획의 재검토를 요구하고 있습니다. 이러한 어려움에도 불구하고, 미국 탱크 트럭 운송 시장은 계속해서 사모펀드 자본을 유치하고 있으며, 컴플라이언스 기반 확대와 틈새 고수익 화물에 대한 접근성을 확대하기 위한 인수합병이 진행 중입니다.

바이오연료 생산의 모멘텀은 플랜트가 신뢰할 수 있는 원료의 퍼스트 마일 배송과 완성된 연료의 라스트 마일 유통을 필요로 하기 때문에 석유 물류 경로를 재구축하고 있습니다. 미국의 바이오연료 생산량은 2035년까지 하루 130만 배럴에 달할 것으로 예상되며, 이러한 추세는 특수 유조선의 수요를 직접적으로 증가시킬 것입니다. 멕시코만 연안의 정제업체와 서해안의 재생 디젤 생산업체들은 인화점이 높은 연료에 대응하는 인증된 탱크에 의존하고 있으며, 자체 중량을 줄이고 처리 시간을 단축하기 위해 차량 업그레이드를 추진하고 있습니다. 캘리포니아주 저탄소 연료 기준 개정에 따라 2046년까지 운송 사업자는 저탄소 연료 취급 범위 확대를 의무화함에 따라 단열 사양의 전용 설비에 대한 수요가 증가하고 있습니다. 고부가가치 특수 제품은 프리미엄 가격이 적용되기 때문에 장거리 운송에 따른 비용 증가를 상쇄할 수 있고, 전국적인 디젤 소비량 감소 추세 속에서도 수익을 확보할 수 있습니다.

2024년 단기적인 수축을 거쳐 2025년 말까지 화학제품 생산량은 1.9% 증가했습니다. 이는 산업 수요 개선과 유리한 에탄 원료 갭으로 인한 가동률 향상에 기인합니다. 에틸렌, 프로필렌, 특수 배터리 소재가 미국 걸프 지역 및 중서부 공장에서 출하됨에 따라 수출용 컨테이너에 적기 적재 시 철도 운송보다 탱크로리 운송을 우선시하는 출발지 및 목적지 재조정이 진행됩니다. 석유화학업체들은 오염 위험을 최소화하고 연안 터미널에서 수출 프리미엄을 얻기 위해 전용 운송업체에 의존하고 있습니다. 반도체 등급 화학 플랜트 투자는 화물 구성의 다양화를 촉진하고, 계절적 정유소 변동성을 완화하는 안정적인 계약 물동량을 창출할 것입니다.

FMCSA(연방 자동차 안전국)의 민사 벌금이 급증하여 위험물 위반 시 1건당 최대 10만 2,348달러의 벌금이 부과됩니다. PHMSA(미국 석유가스안전국)의 소형 운송업체 등록비가 50% 인상되고, 화물탱크 검사 불합격 시 8,000달러의 벌금이 부과될 수 있습니다. 전자기록장치에 의한 디지털 감사로 인해 기존에는 일상적이었던 스케줄 조정이 노출되어 가동률이 저하됨. 법규 준수를 위해 추가 인력이 필요합니다. 컴플라이언스 담당자를 배치할 수 없는 중소 사업자는 철수 또는 매각을 강요당하고, 업계 구조조정이 가속화되는 한편, 가용 운송 능력은 감소하는 추세입니다.

석유 제품은 2025년 매출의 46.30%를 차지하며 미국 탱크 트럭 운송 시장 규모를 뒷받침하고 있습니다. 이는 견조한 정유소 처리량과 확대되는 재생 디젤 혼합 연료 풀에 기인합니다. 재생 연료 생산자들은 제품의 품질 보존을 위해 전용 스테인리스 또는 알루미늄 드럼을 선호하고 있으며, 장기 계약 수요를 강화하고 있습니다. 식음료 부문은 유제품 현대화 및 음료 SKU 증가로 인한 운송 거리 연장에 힘입어 2026년부터 2031년까지 4.24%의 가장 빠른 CAGR을 기록할 것으로 예상됩니다. 화학 부문은 미국 걸프 지역 확장 및 중서부 지역의 비료 생산량 증가로 인해 두 번째 수익원으로서의 지위를 유지하고 있습니다. 비료 운송량은 작물 수확기에 최고조에 달해 현물 운임이 급등하고, 운송업체들은 이를 활용해 지역 간 운송 흐름을 조정하고 있습니다.

저탄소 연료 기준(LCFS)의 강화로 재생 원료 물류에 대한 투자가 촉진되고, 바이오 유래 액체 연료의 미래 성장이 강조되고 있습니다. 석유 부문의 점유율은 2027년 이후 재생 가능 연료의 확대에 따라 감소할 수 있지만, 총 수송 배럴 수는 계속 증가하여 미국 탱크 트럭 운송 시장에서 연료 물류의 지속적인 중요성을 보여줍니다. 한편, FDA의 식품 안전 규제는 전문 운송업체에게 가격 결정권을 부여하여 세척 시설 비용 상승에도 불구하고 수익률을 보장하고 있습니다. 이러한 추세와 함께 단일 상품 라인의 주기적 변동을 완화하는 다양한 화물 기반이 구축되고 있습니다.

대형 트럭은 2025년 매출의 51.85%를 차지했으며, 적재율 향상으로 1회당 운송량이 증가하여 고정비 분산이 이루어지고 있습니다. DOT-412 표준으로의 개조로 적재량 범위가 더욱 확대되어 장거리 석유화학 운송 노선에서 대형 차량의 중요성이 강화되고 있습니다. 소형 트럭 부문은 규모는 작지만, 도시 지역 내 구역 규제로 인한 대형 트레일러 진입 제한과 E-Commerce용 연료 스테이션의 단주기, 고빈도 충전 수요로 인해 2026년부터 2031년까지 3.72%의 가장 높은 CAGR을 기록할 것으로 예상됩니다. 중형 트럭 자산은 중량 제한이 있는 교량을 우회하는 경로 선택이 적재량보다 우선시되는 위험물 운송의 틈새 시장을 담당하고 있습니다.

전동화 시범사업은 경차급에 초점을 맞추고 있습니다. 배터리 항속거리가 도시 지역의 일상적인 루프 운행에 충분하고, 무게 감소가 적재량 감소를 상쇄할 수 있기 때문입니다. 한편, 수소나 LNG(액화천연가스) 옵션은 적재량을 희생하지 않고 항속거리를 연장하고자 하는 대형 트랙터에게 매력적입니다. 이러한 기술 분화를 통해 모든 용량 등급이 명확한 성장 경로를 유지하여 장비 제조업체와 운송 사업자 모두를 지원할 수 있습니다.

United States Tank Trucking Market size in 2026 is estimated at USD 55.39 billion, growing from 2025 value of USD 53.45 billion with 2031 projections showing USD 66.23 billion, growing at 3.64% CAGR over 2026-2031.

The sustained expansion reflects the market's capacity to adapt to shifting energy mixes, stricter safety rules, and volatile input costs. Rising movements of renewable diesel, specialty chemicals, and temperature-controlled food ingredients are expanding the freight base, while digital dispatch tools and lighter tank specifications are pushing asset productivity higher. In parallel, driver shortages, hazmat compliance penalties, and disruptive pilot programs for autonomous trucks are pressuring operating economics and forcing carriers to re-evaluate route design, fleet mix, and capital plans. Despite these challenges, the United States tank trucking market continues to attract private equity capital, with acquisitions aimed at scaling compliance infrastructure and expanding access to niche, higher-margin cargoes.

Biofuel manufacturing momentum is redrawing petroleum logistics corridors as plants require dependable first-mile feedstock deliveries and last-mile finished fuel distribution. United States biofuel output is projected to reach 1.3 million barrels of oil equivalent per day by 2035, a trend that directly increases specialized tank requirements. Gulf Coast refiners and West Coast renewable diesel producers rely on tanks certified for elevated flash-point fuels, driving fleet upgrades that cut tare weight and speed turnarounds. California's updated Low-Carbon Fuel Standard compels carriers to handle a widening slate of low-carbon fuels through 2046, reinforcing demand for insulated, dedicated equipment. Higher-value specialty products pay premiums that offset longer haul distances, securing revenues even as total diesel consumption gradually declines nationwide.

After the brief 2024 contraction, chemical output is set to advance 1.9% by the end of 2025 as improved industrial demand and a favorable ethane feedstock gap lift utilization rates. Ethylene, propylene, and specialty battery materials moving from Gulf Coast and Midwest plants spur origin-destination realignment that favors tank trucks over rail for just-in-time export container stuffing. Petrochemical producers lean on dedicated carriers to minimize contamination risks and capture higher export premiums at coastal terminals. Investments in semiconductor-grade chemical plants further diversify the freight mix, creating steady contract carriage volumes that smooth seasonal refinery swings.

FMCSA civil penalties have surged, with hazmat violations now costing up to USD 102,348 per count. PHMSA registration fees for small carriers rose 50%, while cargo-tank inspection failures can trigger USD 8,000 fines. Digital audits from electronic logging devices expose once-routine schedule adjustments, cutting utilization and requiring additional headcount to keep fleets legal. Smaller operators lacking compliance personnel are either exiting or selling, accelerating consolidation but trimming available capacity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Petroleum products supplied 46.30% of 2025 revenue, underpinning the United States tank trucking market size with resilient refinery throughput and a growing renewable diesel blend pool. Renewable-fuel producers favor dedicated stainless or aluminum barrels to safeguard product integrity, reinforcing long-term contract demand. Food and beverages register the fastest 4.24% CAGR (2026-2031), supported by dairy modernization and beverage SKU proliferation that lengthen haul distances. Chemicals remain the second-largest revenue pillar, lifted by Gulf Coast expansion and Midwest fertilizer output. Fertilizer shipments peak around planting seasons yet drive pronounced spot-rate spikes that carriers exploit to balance regional flows.

Intensifying LCFS requirements steer investment toward renewable feedstock logistics, weighting future growth toward bio-derived liquids. The petroleum segment's share may ease post-2027 as renewable volumes scale, yet absolute barrels shipped continue to rise, underscoring the enduring role of fuels logistics in the United States tank trucking market. Meanwhile, FDA food-safety mandates grant specialized carriers pricing power, securing margins amid climbing wash-bay costs. Together, these trends cement a diverse cargo base that tempers cyclical swings in any single commodity line.

Heavy trucks generated 51.85% of 2025 revenue, benefitting from larger load factors that spread fixed costs over more gallons per trip. DOT-412 retrofits further expand payload windows, reinforcing the heavy-duty fleet's central role in long-haul petrochemical corridors. The light-duty bracket, though smaller, produces the strongest 3.72% CAGR (2026-2031) as urban zoning curbs large trailer access and e-commerce fuel stations demand shorter, more frequent replenishment cycles. Medium-duty assets fill hazmat niches where routing around weight-restricted bridges trumps load size.

Electrification pilots focus on the light-duty class because battery range suffices for daily metro loops, and weight savings offset cargo penalties. Conversely, hydrogen and LNG options appeal to heavy tractors seeking extended range without payload sacrifice. These technology splits assure all capacity classes retain defined growth paths, supporting equipment manufacturers as well as carriers.

The United States Tank Trucking Market Report is Segmented by Product Category (Crude Petroleum, Petroleum Products, Chemicals, Food and Beverages, Fertilizers, and Others), Capacity (Light Duty, Medium Duty, and Heavy Duty), Destination (Domestic and International), Distance (Long Haul and Short Haul), Application (Residential, Commercial, and Industrial). The Market Forecasts are Provided in Terms of Value (USD).