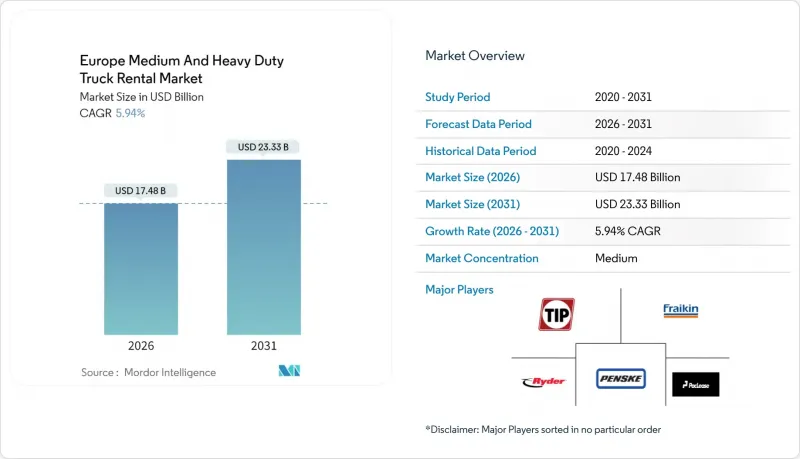

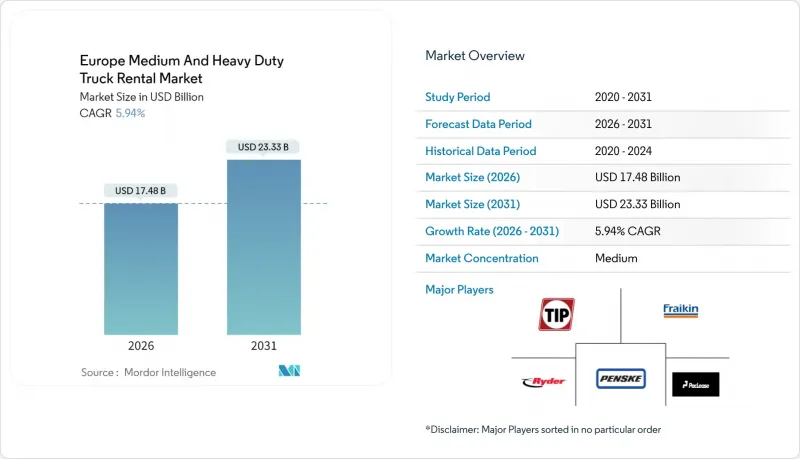

유럽의 중형 및 대형 트럭 렌탈 시장 규모는 2026년에 174억 8,000만 달러에 달할 것으로 예측되고 있습니다.

이는 2025년 165억 달러에서 성장한 수치이며, 2031년에는 233억 3,000만 달러에 달할 것으로 전망되고 있습니다. 2026-2031년의 연평균 성장률(CAGR)은 5.94%로 예측되고 있습니다.

이러한 성장 가속화는 E-Commerce 물동량 증가, 외주 차량에 유리한 엄격한 배기가스 규제, 고금리 환경 하에서 운영비용을 중시하는 추세에 힘입은 바 큽니다. 거래 시간을 단축하고 고객층을 확대하는 디지털 예약 플랫폼의 보급과 최종사용자의 기술적 위험 장벽을 낮추는 전동화 파일럿 사업으로 성장이 더욱 가속화되고 있습니다. 유럽 주요 회랑에서 적재 경제성을 극대화하기 위해 대형 차량이 수요의 대부분을 차지하지만, 도시 지역의 무공해 구역이 확대됨에 따라 중형 차량과 전기자동차 옵션에 대한 관심이 높아지고 있습니다.

온라인 소매업의 강화로 TIMOCOM 현물시장의 화물 수요는 전년 대비 92% 증가하여 2024년 대부분 기간 중 화물 수요 대 운송능력 비율이 70%를 초과했습니다. 운송업체와 3PL 사업자들은 영구적인 자산을 추가하지 않고 성수기 수요 급증에 대응하기 위해 단기 임대에 의존하고 있습니다. 우편 및 소포 부문만 보더라도 눈에 띄는 CAGR로 성장하고 있으며, 이러한 속도는 유럽 중형 및 대형 트럭 렌탈 시장의 각 사업자들에게 가동률 압박을 초래하고 있습니다. 소매업체들도 자본 투입 전 신규 지역 허브의 시험 운영에 렌탈을 활용하고 있으며, 이는 구조적으로 높은 차량 유연성의 기반을 지원하고 있습니다. 2025년 부활절이 4월로 넘어가면서 새로운 임시 수요의 물결이 단기 임 대 수요의 모멘텀을 더욱 강화할 것으로 예측됩니다.

유럽중앙은행의 통화 긴축으로 인해 2025년 초 기업 트럭 융자 비용이 4%를 넘어섰지만, 연초에는 3.61%까지 완화되었습니다. 그럼에도 불구하고 2022년 이전 수준을 상회하고 있습니다. 따라서 소규모 차량은 자산 감가상각에 대한 방어적 운용비용으로 렌탈을 활용하고 있습니다. 2024년 4분기에는 전년 동기 대비 현물 운송 가격이 상승했고, 연료비 및 탄소세 할증료로 인한 상승은 변동비 모델을 더욱 정당화했습니다. 중형 트럭 사용자의 경우, 잔존가치의 불확실성이 자금조달 위험을 증폭시키기 때문에 가장 두드러진 변화를 볼 수 있습니다. 변동 기간 계약과 마켓플레이스 가격 설정은 현재 많은 개인 브랜드 유통 네트워크를 지원하고 있으며, 유럽 중형 및 대형 트럭 렌탈 시장 공급자의 잠재 고객층을 확대하고 있습니다.

중고 대형 트럭 가격은 2025년 중반까지 2023년형과 2021년형 모델에서 하락하여 다가오는 배출가스 규제에 따른 감가상각 위험을 부각시켰습니다. 중고 시장에 의존하여 차량을 갱신하는 렌탈 기업은 디젤 차량의 가치가 예정된 차량 갱신 주기보다 빠르게 하락할 경우, 이익률 압박에 직면하게 됩니다. 사업자들은 보유 기간 단축과 다양한 추진 시스템 구성을 통한 헤지를 채택하고 있지만, 완전한 갱신은 여전히 자본 집약적일 수밖에 없습니다. 가속화된 감가상각은 전통적 소유 형태를 더욱 억제하고 간접적으로 임 대 수요를 확대할 것입니다. 그러나 동시에 대량의 디젤 차량 재고를 보유하고 있는 렌탈 사업자에게는 매출의 원천이 좁아지는 결과를 초래할 수 있습니다.

2025년에도 유럽 중형 및 대형 트럭 렌탈 시장 점유율의 72.48%는 오프라인 채널이 차지할 것으로 예측됩니다. 이는 장기리스에서 여전히 관계 기반 계약이 주류를 이루고 있기 때문입니다. 그러나 고객이 24시간 365일 셀프 서비스 대시보드, 투명한 요금 체계, 즉각적인 차량 배차를 선호하는 추세로 인해 온라인 포털은 CAGR 7.77%로 빠르게 성장하고 있습니다. 렌탈 사업자는 통합 API를 도입하여 재고 정보를 화주의 운송 관리 시스템과 동기화하여 수동 견적 주기를 몇 시간에서 몇 분으로 단축하고 있습니다. 구독형 요금 체계, 디지털 문서 서명, 내장된 보험 옵션은 플랫폼의 편의성을 더욱 강화합니다.

온라인 예약의 성장은 경쟁의 경계를 명확히 하고 있습니다. 디지털 네이티브 플랫폼은 낮은 거래비용을 활용하여 기존에는 지역 대리점이 담당하던 소규모 운송업체까지 도달할 가능성이 있습니다. 한편, 기존 기업은 옴니채널 전략에 대응하고 있으며, 표준 차량에는 셀프 서비스 주문을, 복잡한 프로젝트에는 인적 계정 관리를 결합하고 있습니다. 그 결과, 유럽의 중형 및 대형 트럭 렌탈 시장에서는 단기적인 대량 수요가 온라인으로 이동하는 반면, 주문형 계약은 오프라인으로 존속하는 두 가지 흐름이 공존하는 모델이 생겨났습니다. 예측 기간 중 디지털화를 통한 가시성 향상으로 차량 가동률이 상승하여 자산을 비례적으로 늘리지 않고도 잉여 용량을 창출할 수 있을 것으로 예측됩니다.

2025년 기준 유럽 중형 및 대형 트럭 렌탈 시장의 61.72%를 차지하는 장기 임대는 규모의 경제를 실현하고 예측 가능한 경로를 가진 화주에게 낮은 일일 비용을 제공합니다. 한편, CAGR 8.49%로 확대되는 단기 계약은 계절적 수요 피크, 프로젝트 기반 업무 또는 급격한 EC 수요 증가가 특징인 산업에서 번창하고 있습니다. 유연성에 대한 프리미엄은 동등한 장기 일당 요금에 비해 15-20%에 달하지만, 화주는 유휴 차량 위험을 피하기 위해 이 가격 차이를 기꺼이 받아들일 수 있습니다.

유로7 규제 대응 비용 증가가 예상되는 가운데, 차세대 차량에 대한 시운전 기간을 선택하는 사업자가 증가하고 있으며, 이러한 움직임은 단기 리스 파이프라인을 확대하고 있습니다. 렌탈 업체는 휴일이나 수확기 수요 급증시 한정된 용량의 매출을 극대화하기 위해 동적 가격 책정 알고리즘을 채택하여 단위당 매출을 확대하고 있습니다. 한편, 장기계약은 안정적인 현금흐름을 가져와 선대 확대를 위한 설비투자를 지원하고 있습니다. 이러한 수입원의 균형을 맞추기 위해서는 강력한 수요 예측과 자산 재분배 전략이 필요하며, 유럽 중형 및 대형 트럭 렌탈 시장 전체에서 분석 능력은 경쟁 차별화 요소로 자리매김하고 있습니다.

Europe Medium & Heavy-Duty Truck Rental market size in 2026 is estimated at USD 17.48 billion, growing from 2025 value of USD 16.50 billion with 2031 projections showing USD 23.33 billion, growing at 5.94% CAGR over 2026-2031.

This acceleration rests on rising e-commerce freight volumes, stringent emissions policy that favors outsourced fleets, and a preference for operating-expense models during an elevated interest-rate climate. Growth is further amplified by digital booking platforms that compress transaction times and broaden customer reach, while electrification pilots reduce technology-risk barriers for end users. Heavy-duty vehicles dominate demand because they maximize payload economics on core European corridors, yet medium-duty and electric options are gaining attention as cities expand zero-emission zones.

Intensified online retail has lifted freight offers on the TIMOCOM spot marketplace by 92% year-over-year, pushing the freight-to-capacity ratio past 70% for most of 2024 . Carriers and 3PLs lean on short-term rentals to absorb peak season spikes without adding permanent assets. The postal and parcel segment alone is expanding at a notable CAGR, a pace that tightens utilization for every Europe Medium & Heavy-Duty Truck Rental market operator. Retailers also use rentals to pilot new regional hubs before committing capital, supporting a structurally higher baseline for fleet flexibility. As Easter shifts to April in 2025, a fresh swell of ad-hoc demand is expected to reinforce short-term leasing's momentum.

European Central Bank tightening pushed corporate truck loan costs above 4% in early 2025 before easing to 3.61% mid-year, levels that still exceed pre-2022 norms . Smaller fleets, therefore, treat rentals as a defensive operating expense hedge against asset depreciation. Spot transport prices climbed year-over-year in Q4 2024, an uptick driven by fuel and carbon surcharges that further validate variable-cost models. Medium-duty users exhibit the sharpest shift as residual-value uncertainty compounds financing risk. Variable-term contracts and marketplace pricing now underpin many private-label distribution networks, broadening the addressable pool for Europe's Medium & Heavy-Duty Truck Rental market providers.

Used heavy-duty truck prices slid in 2023 model-year units and 2021 models by mid-2025, underscoring the depreciation risk tied to looming emissions regulations. Rental companies that rely on resale markets to refresh fleets face compressed margins when diesel values sag faster than scheduled de-fleet cycles allow. Operators adopt shorter holding periods and hedge with diversified propulsion mixes, yet outright replacement remains capital-intensive. Accelerated depreciation further deters traditional ownership, indirectly expanding rental demand; however, it simultaneously tightens profit pools for rental providers that maintain large diesel inventories.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Offline channels still controlled 72.48% of the European Medium & Heavy-Duty Truck Rental market share in 2025, as relationship-based contracts remain the norm for long-term leasing. Nevertheless, online portals are scaling quickly at a 7.77% CAGR as customers prefer 24/7 self-service dashboards, transparent rates, and instantaneous vehicle availability. Rental operators deploy integrated APIs that sync inventory with shipper transportation-management systems, reducing manual quote cycles from hours to minutes. Subscription-style pricing, digital document signatures, and embedded insurance options further reinforce platform convenience.

The growth of online booking also sharpens competitive boundaries: digital-native platforms leverage lower transaction costs to reach small haulers historically served by local agencies. Legacy firms counter with omnichannel strategies that blend self-service ordering for standardized units and human account management for complex projects. As a result, the European Medium & Heavy-Duty Truck Rental market witnesses a twin-track model in which high-volume short-term demand migrates online while bespoke contracts persist offline. Over the forecast window, digital engagement is expected to raise fleet utilization through better visibility, thereby unlocking capacity without proportional asset growth.

Long-term leasing controlled 61.72% of the European Medium & Heavy-Duty Truck Rental market share in 2025 and enjoys economies of scale that keep daily costs low for shippers with predictable routes. Yet short-term contracts, expanding at 8.49% CAGR, flourish in industries characterized by seasonal peaks, project-based work, or rapid e-commerce surges. The flexibility premium can reach 15-20% over equivalent long-term day rates, but shippers willingly absorb that markup to sidestep idle-fleet risk.

As Euro 7 compliance costs loom, more operators opt for trial periods with next-generation vehicles, a dynamic that feeds short-term leasing pipelines. Rental companies employ dynamic pricing algorithms to maximize yield on scarce capacity during holiday or harvest surges, widening revenue per unit. Conversely, long-term deals contribute stable cash flows, underpinning fleet-expansion capex. Balancing these streams requires robust demand forecasting and asset re-allocation strategies, cementing analytics as a competitive differentiator across the European Medium & Heavy-Duty Truck Rental market.

The Europe Medium & Heavy-Duty Truck Rental Market Report is Segmented by Booking Type (Offline Booking and Online Booking), Rental Type (Short-Term Leasing and Long-Term Leasing), Truck Class (Medium-Duty (7. 5-16t) and Heavy-Duty (Above 16t)), End-User Industry (General Freight and 3PL, Construction and Infrastructure, and More), Propulsion Type, and Country. The Market Forecasts are Provided in Terms of Value (USD).