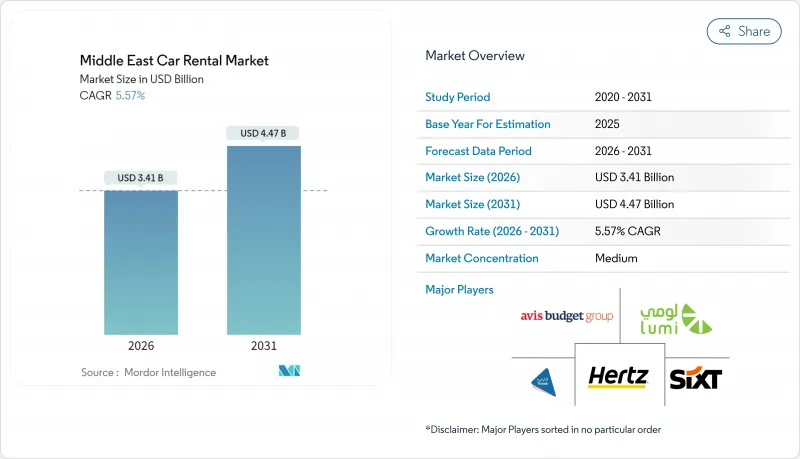

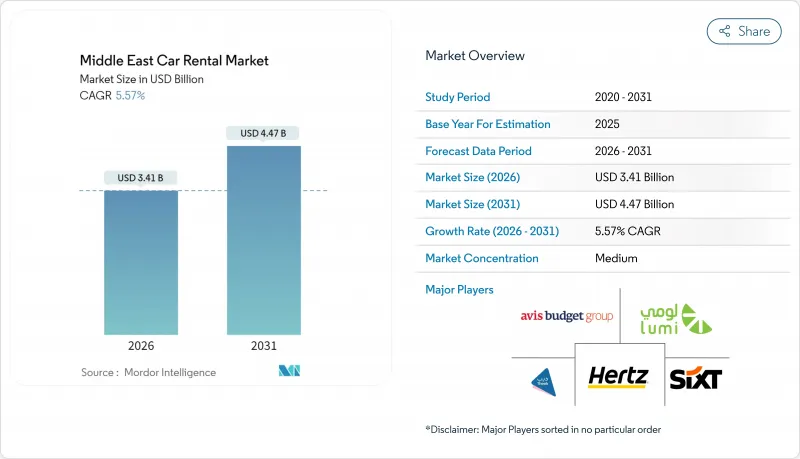

중동의 렌터카 시장 규모는 2026년 34억 1,000만 달러로 추정되고 있습니다. 이는 2025년 32억 3,000만 달러에서 성장한 수치이며, 2031년에는 44억 7,000만 달러에 이를 것으로 예측되고 있습니다. 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.57%로 전망되고 있습니다.

증가하는 국내 관광, 프리미엄 중심의 이동성 수요 및 디지털 기술의 광범위한 보급이 시장 확대를 뒷받침합니다. 2024년 외국인 방문객 수는 유행 전 수준을 32% 웃돌았으며 9,500만 명의 방문자 수와 지속적인 렌터카 수요로 이어졌습니다. 앱 기반 예약은 이미 총 거래의 약 3분의 2를 차지하고 있으며 고급차 및 전기자동차의 틈새 시장이 가장 빠른 성장률을 보이고 있습니다. 사우디아라비아의 '비전 2030'과 '2030년 엑스포' 등 정부 주도의 메가 프로젝트는 모빌리티 회랑 확대, 차량 업그레이드 촉진, 공항 외부의 새로운 수익원 개척을 추진하고 있습니다. 시장이 비교적 분산되고 있는 상황과 대규모 벤처 자금 조달이 결합되어 추가적인 산업 재편이 예상됩니다.

GCC 국가에서는 2024년 관광업이 현저한 회복을 보였습니다. 사우디아라비아에서는 관광객 수가 69% 급증했고, 관광 수입은 606억 달러에 달했습니다. 아랍에미리트(UAE)에서는 여행 및 관광업이 GDP에 599억 달러(경제 규모의 11.7%에 해당)를 공헌했습니다. 2025년 초반에는 카타르에서 관광객이 100만 명 가량 크게 증가했습니다. 한편, 쿠웨이트에서는 관광객 중심의 인프라에 대해 대량의 투자가 이루어지면서 추가적인 차량 수요 증가를 나타내고 있습니다. 이러한 국경을 넘은 이동에는 사업자의 관할 구역을 넘은 전략적인 차량 재배치, 견고한 회랑 기반 서비스 전략의 확립, 다양한 규제 프레임워크와의 적응 등의 대응이 요구됩니다. 이들은 이용률 증가를 최대한 활용하면서 진행할 필요가 있습니다.

스마트폰의 높은 보급률과 디지털 결제의 성숙도에 따라 모바일 예약이 현장 결제를 뛰어넘어 유통비용을 절감함과 동시에 사업자가 고객 데이터에 직접 접근할 수 있게 되었습니다. UAE에서는 거의 전역을 커버하는 5G 환경과 비접촉 서비스에 대한 소비자 기호가 이 동향을 가속화하고 있으며, 사우디아라비아에서는 젊은 층 인구가 모바일 이용 확대를 뒷받침하고 있습니다. 내장된 본인 확인 기능과 키리스 엔트리가 편리성을 높여 예측 분석에 의해 차량 로테이션이 최적화됩니다. 자사 앱을 소유한 기업은 제3자 수수료를 회피하고 이익률을 향상시키며 멤버십 프로그램을 통해 평생 고객 가치를 확보합니다.

대도시권에서의 라이드 헤일링 서비스의 확대는 기존에 자가용 렌트카가 선호되었던 단거리 시내 이동을 점차 흡수하고 있습니다. 그러나 여러 날에 걸친 관광, 가족 여행, 도시간 이동에 있어서 렌터카의 매력은 여전히 높으며 견조한 수요 기반을 유지하고 있습니다. 이러한 변화하는 상황에 대응하여, 사업자는 제공 서비스를 확충하고, 렌탈 체험을 높이는 프리미엄 서비스를 강조하고 있습니다. 또한 필수 내비게이션 툴을 번들하여 e-hail 플랫폼과의 제휴에 의해 원활한 복합 모빌리티 패스를 창출하고 있습니다. 장거리 이동과 고부가가치 이용을 위한 렌탈을 전략적으로 배치하여 온디맨드 라이드로의 고객 유출을 효과적으로 최소한으로 억제하여 편리성을 높이면서 개인 차량의 매력이 지속되도록 보장하고 있습니다.

2025년 중동의 렌터카 시장에서 온라인 예약은 62.12%를 차지하였고 예측 기간 동안 CAGR 6.74%로 확대될 것으로 전망됩니다. 현장 결제는 공항과 호텔에서 관광객을 계속 획득하고 있지만, 높은 간접비가 과제입니다. 모바일 퍼스트 인터페이스는 즉각적인 업그레이드, 옵션 추가, 포인트 환급을 지원하여 예약 리드 타임의 단축과 이용률 향상을 실현합니다. 장기적으로는 옴니채널 전략이 정착하고 오프라인 매장은 고객지원과 차량 인도에 주력하는 한편, 디지털 채널이 판매 및 결제 및 업셀을 담당하는 방향으로 이행할 전망입니다.

경쟁은 자사 앱과 마켓플레이스형 통합자의 대립에 초점이 맞춰져 있습니다. 실시간 차량 재고 관리, 디지털 신원 확인, 키리스 픽업을 통합한 사업자는 거래 시간을 단축하고 있습니다. UAE의 스마트폰 보급률이 도입을 가속화하고, 사우디아라비아도 광범위한 4G망에 힘입어 뒤따르고 있습니다. 쿠웨이트와 오만은 여전히 현장 예약에 의존하고 있지만, 소비자의 기대 변화에 따라 모바일 솔루션을 꾸준히 도입하고 있습니다.

2025년 중동의 렌터카 시장에서 매출의 95.10%를 레저 및 관광용 렌탈이 차지하였고, 2031년까지 연평균 복합 성장률(CAGR)7.22%로 확대될 것으로 전망됩니다. 두바이, 도하, 리야드, 무스카트에서는 대규모 이벤트와 비자 규제 완화로 관광지로서의 매력을 유지하고 있습니다. 그러나 다국적 기업이 사우디아라비아와 아랍에미리트(UAE)에 지역 본부를 두면서 법인 수요가 수익원의 다양화를 촉진하고 있습니다.

휴가 시즌의 피크와 관련된 계절 변동 위험은 연중 회의 및 프로젝트 중심의 출장으로 완화되고 있습니다. 관광객과 경영 임원 모두에 대응할 수 있는 기업은 차량 구성을 최적화하며, 관광객이 집중되는 피크 시에는 이코노미 차량을 운용하고, 비수기에는 법인 고객을 위한 럭셔리 세단을 배차하고 있습니다. 이 두 시장에 대응하는 자세가 현금 흐름을 안정시키고 전체 가동률을 높이고 있습니다.

The Middle East car rental market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 3.23 billion with 2031 projections showing USD 4.47 billion, growing at 5.57% CAGR over 2026-2031.

Rising inbound tourism, premium-oriented mobility demand, and broad digital adoption underpin the expansion. International arrivals surpassed pre-pandemic levels by 32% in 2024, translating into 95 million visitors and sustained rental demand . App-based reservations already account for close to two-thirds of total transactions, while luxury and electric fleet niches record the fastest volume gains. Government-backed megaprojects such as Saudi Arabia's Vision 2030 and Expo 2030 are widening mobility corridors, encouraging fleet upgrades, and opening new off-airport revenue pools. Moderate market fragmentation, coupled with sizable venture funding, signals further consolidation.

GCC destinations recorded a pronounced tourism recovery in 2024, led by Saudi Arabia's 69% surge in arrivals and tourism receipts of USD 60.6 billion. The United Arab Emirates contributed USD 59.9 billion to GDP from travel and tourism, equivalent to 11.7% of the economy . In the first half of 2025, Qatar welcomed a significant influx of one million visitors. Meanwhile, Kuwait is making substantial investments in visitor-centric infrastructure, indicating a rising demand for additional fleets. These cross-border movements require operators to strategically reposition vehicles across jurisdictions, establish robust corridor-based service strategies, and adapt to varying regulatory frameworks, all while leveraging the growing utilization rates.

High smartphone penetration and digital payments maturity enable mobile reservations to eclipse counter transactions, trimming distribution overheads and granting operators direct access to customer data. In the UAE, near-ubiquitous 5G coverage and consumer preference for contactless services accelerate the trend, while Saudi Arabia's youthful demographic amplifies mobile adoption. Embedded identity verification and keyless entry elevate user convenience, and predictive analytics refine fleet rotation. Firms that own proprietary apps bypass third-party commissions, enhance margins, and lock in lifetime customer value through loyalty tools.

The expansion of ride-hailing services in bustling metropolitan areas increasingly captures short city trips that once favored self-drive rentals. However, for multi-day tourism, family vacations, and intercity commutes, the allure of rental cars remains strong, sustaining a solid base of demand. In response to this shifting landscape, operators are ramping up their offerings, highlighting premium service tiers that elevate the rental experience. They're also bundling essential navigation tools and forging partnerships with e-hail platforms to create seamless blended mobility passes. By strategically positioning rentals for longer journeys and higher-value usage, they effectively minimize the loss of customers to on-demand rides, ensuring that the charm of a personal vehicle endures amidst the rising tide of convenience.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Online reservations represented 62.12% of the Middle East car rental market size in 2025 and are projected to climb at a 6.74% CAGR during the forecast period. Offline counters still capture walk-in tourists at airports and hotels, but suffer higher overheads. Mobile-first interfaces support instant upgrades, add-ons, and loyalty redemption, shrinking booking lead times and lifting utilization. In the longer run, omnichannel strategies will persist, with physical outlets pivoting toward customer support and vehicle handover while digital funnels handle sales, payments, and upselling.

Competition centers on proprietary apps versus marketplace aggregators. Operators that integrate real-time vehicle availability, digital KYC, and keyless pick-ups are lowering transaction times. The UAE's smartphone penetration accelerates uptake, and Saudi Arabia follows closely, aided by widespread 4G coverage. Kuwait and Oman remain more reliant on desk bookings but are steadily onboarding mobile solutions as consumer expectations shift.

Leisure and tourism rentals supplied 95.10% of the Middle East car rental market revenue in 2025, advancing at a forecast 7.22% CAGR through 2031. Mega-events and relaxed visa regimes sustain destination appeal across Dubai, Doha, Riyadh, and Muscat. Nevertheless, corporate demand is diversifying revenue streams as multinationals locate regional headquarters in Saudi Arabia and the United Arab Emirates.

Seasonality risk tied to holiday peaks is being diluted by year-round conferences and project-driven travel. Firms adept at serving both tourists and executives optimize fleet mix, rotating economy cars during peak visitor influx and allocating premium sedans for business accounts in shoulder months. This dual-market posture stabilizes cash flow and raises overall utilization.

The Middle East Car Rental Market is Segmented by Booking Type (Online and Offline), Application (Leisure/Tourism, Daily Utility/Business), Vehicle Type (Economy, Luxury and Premium), End-User Type (Self-Driven and Chauffeur), Service Model (On-Airport, and Off-airport/Local), Propulsion (Internal-Combustion ICE, Electric and Hybrid), and Country. The Market Forecasts are Provided in Terms of Value (USD).