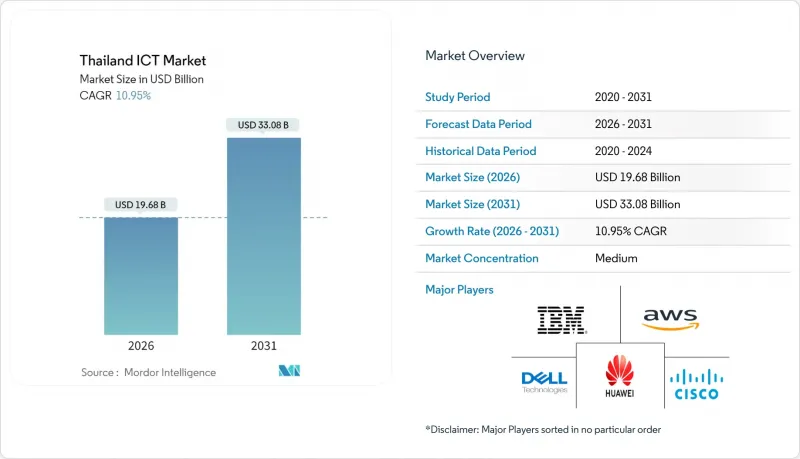

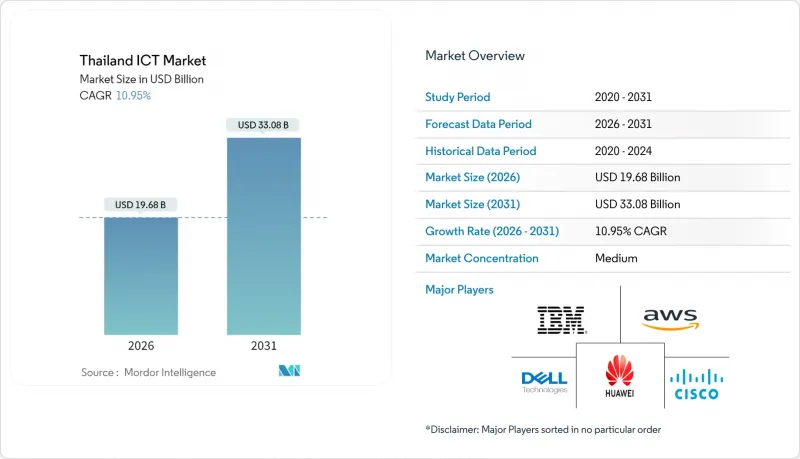

태국의 ICT 시장은 2025년 177억 4,000만 달러에서 2026년에는 196억 8,000만 달러로 성장하며, 2026-2031년에 CAGR 10.95%로 추이하며, 2031년에는 330억 8,000만 달러에 달할 것으로 예측됩니다.

이러한 확대는 전국적인 5G 네트워크 구축, 하이퍼스케일 데이터센터 투자, 정부 주도의 클라우드 퍼스트 정책을 원동력으로 삼아 지역 디지털 허브로 도약하려는 중국의 의지를 반영하고 있습니다. 통신 서비스 프로바이더들은 산업용 IoT를 위한 5G 네트워크 슬라이싱을 통해 매출을 창출하고 있으며, 10억 달러 이상의 외국인 직접투자가 AI 지원 액체 냉각 시설에 유입되어 데이터센터 생태계를 지원하고 있습니다. 태국 ICT 시장은 동부 경제 회랑의 인더스트리 4.0 현대화, 사이버 보안 서비스 수요 증가, 핀테크 기반 확대를 위한 가상 은행 라이선스 부여로 지원되고 있습니다. 한편, 인력 부족과 데이터 현지화 규제 강화로 인한 컴플라이언스 비용 증가라는 과제에 직면해 있습니다.

2024년까지 전국적인 5G 구축으로 95%의 인구 커버리지를 달성하고, 제조업의 예지보전 및 실시간 물류 추적과 같은 엣지컴퓨팅의 이용 사례를 가능하게 합니다. 통신사업자들은 네트워크 슬라이싱을 도입하여 미션 크리티컬한 용도를 위한 전용 처리량을 제공함으로써 소비자 대상의 음성 및 데이터 통신을 넘어 기업 대상의 수입원을 개발하고 있습니다. 국가방송통신위원회의 주파수 할당과 인프라 공유 규정은 지방의 구축 비용을 낮추고, 방콕 이외의 지역에서의 도입을 가속화하고 있습니다. 동부 경제 회랑의 제조업체들은 5G 센서와 AI 분석을 통합하여 예기치 않은 다운타임을 줄이고 처리량을 향상시키고 있습니다. 5G 단말기 보급률 상승은 가입자 전환을 촉진하여 사용자 1인당 월평균 데이터 소비량을 두 자릿수 기가바이트대로 끌어올리고 있습니다.

2024년 이후 모든 공공기관은 On-Premise 조달을 예외적으로 정당화해야 하며, 각 부처는 ISO 27001 및 개인정보보호법에 따라 인증된 국내 클라우드 지역으로 레거시 시스템을 이전하고 있습니다. 150억 바트(4억 7,000만 달러) 규모의 '스마트 네이션 스마트 라이프' 프로그램은 공유 API 게이트웨이와 'ThaiLLM'이라는 주권형 거대 언어 모델 플랫폼 구축을 지원하며, 이는 정부 인증 클라우드에서 호스팅됩니다. 국영기업은 단일 조달 포털을 통해 서비스 카탈로그를 공개하고, 민간 공급업체에 명확한 통합 로드맵을 제공합니다. 이 정책은 규제 산업에서도 비슷한 움직임을 촉진하고 있으며, 금융기관은 정부의 프레임워크를 기준으로 클라우드 보안 기반을 평가했습니다. 그 결과, 클라우드 기술, 레퍼런스 아키텍처, 조달 템플릿이 민간 부문에 침투하여 태국 ICT 시장은 시너지 효과를 누리고 있습니다.

태국 중소기업 10곳 중 9곳은 공식적인 디지털 투자 계획이 없는 것으로 나타났으며, 클라우드로 전환한 기업도 다단계 인증이나 역할 기반 접근 제어와 같은 기본적인 보안 설정을 소홀히 하는 경우가 많았습니다. 제로 트러스트 프레임워크에 대한 인식 부족으로 인해 중소기업은 피싱과 랜섬웨어의 위협에 노출되어 몇 주 동안 업무가 마비될 위험에 직면해 있습니다. SME 4.0 프로그램을 통한 정부 보조금은 교육 및 컨설팅 비용을 보조하고 있지만, 경영자들이 당장의 자금조달을 우선시하므로 이용률은 30% 미만에 그치고 있습니다. 보험 인수회사가 중소기업의 정보 유출 빈도 증가를 반영하여 사이버 보험의 보험료가 상승하는 추세입니다. 지속적인 기술 개발이 없다면, 태국 ICT 시장은 도시 외 지역에서의 클라우드 보급이 둔화될 위험에 직면하게 될 것입니다.

2025년 태국 ICT 시장 점유율의 가장 큰 비중(32.08%)을 차지한 분야는 IT 서비스로, 매니지드 서비스 계약과 멀티 클라우드 마이그레이션 프로젝트가 주도했습니다. 통신사는 네트워크 운영센터를 외부에 위탁하고, 제조업체는 예지보전 도입을 위해 시스템 통합사업자를 활용하고 있습니다. 이러한 틀 안에서 클라우드 서비스는 기업이 모놀리식 용도를 API 기반 마이크로서비스로 재구축하는 움직임에 따라 CAGR 11.45%를 나타낼 것으로 예측됩니다. 하드웨어 수요는 5G 무선 설비 업그레이드와 데이터센터 설비 투자에 힘입어 견고한 성장세를 유지하는 반면, 사이버 보안 지출은 지속적인 위협 요인으로 인해 가속화되고 있습니다.

설비투자(CapEx)에서 운영비용(OpEx)으로의 전환은 벤더의 매출모델을 재구성합니다. PTT Exploration and Production이 클라우드 네이티브 개발 플랫폼으로 전환한 결과, 용도 출시 주기가 480% 단축되어 레거시 시스템 현대화 효과를 입증했습니다. 저지연 요구 사항을 충족하기 위해 제조 공장에 엣지 컴퓨팅 장비가 보급되어 국가방송통신위원회(NBTC) 표준 인증을 획득한 하드웨어 공급업체에 새로운 수입원을 가져다주고 있습니다. 태국 ICT 시장에서는 비즈니스 분석가들이 용도 프로토타입을 만들 수 있는 로우코드 개발 툴이 도입되어 부족한 개발자 인력에 대한 부담을 덜어주고 있습니다.

The Thailand ICT market is expected to grow from USD 17.74 billion in 2025 to USD 19.68 billion in 2026 and is forecast to reach USD 33.08 billion by 2031 at 10.95% CAGR over 2026-2031.

This expansion reflects the country's push to become a regional digital hub, propelled by nationwide 5G coverage, hyperscale data-center investment, and a government cloud-first mandate. Telecommunications service providers monetize 5G network slicing for industrial IoT, while foreign direct investment exceeding USD 1 billion in AI-ready, liquid-cooled facilities anchors the data-center ecosystem. The Thailand ICT market is also buoyed by Industry 4.0 modernization across the Eastern Economic Corridor, rising demand for cybersecurity services, and virtual-bank licensing that expands fintech infrastructure. At the same time, the market confronts talent shortages and stricter data-localization rules that heighten compliance costs.

Nationwide 5G roll-out reached 95% population coverage by 2024, enabling edge-computing use cases for predictive maintenance in manufacturing and real-time logistics tracking. Operators deploy network-slicing to offer dedicated throughput for mission-critical applications, unlocking enterprise revenue streams that move beyond consumer voice and data. The National Broadcasting and Telecommunications Commission's spectrum allocations and infrastructure-sharing rules lower deployment costs for rural areas, accelerating adoption outside Bangkok. Manufacturers in the Eastern Economic Corridor integrate 5G sensors with AI analytics to cut unplanned downtime and boost throughput. Rising 5G handset penetration fuels subscriber migration, pushing average data consumption to double-digit gigabyte levels per user each month.

Since 2024, every public-sector agency must justify on-premises procurements as exceptions, prompting ministries to migrate legacy systems onto domestic cloud regions certified under ISO 27001 and the Personal Data Protection Act. The THB 15 billion (USD 0.47 billion) Smart Nation Smart Life program funds shared API gateways and a sovereign large-language-model platform dubbed ThaiLLM hosted in government-approved clouds. State-owned enterprises now publish service catalogs through a single procurement portal, giving private vendors a clear roadmap for integration. The policy has catalyzed similar behavior in regulated industries, with financial institutions benchmarking cloud-security baselines against the government framework. As a result, the Thailand ICT market enjoys a multiplier effect as cloud skills, reference architectures, and procurement templates trickle into the private sector.

Nine in ten Thai SMEs lack formal digital investment plans, and many who do migrate to cloud overlook basic security configurations such as multi-factor authentication or role-based access. Limited awareness of zero-trust frameworks leaves smaller firms exposed to phishing and ransomware that can cripple operations for weeks. Government vouchers under the SME 4.0 program subsidize training and consulting, yet usage remains below 30% because owners prioritize immediate cash-flow concerns. Cyber-insurance premiums climb as underwriters factor in elevated breach frequency among small businesses. Without continuous skills development, the Thailand ICT market risks slower cloud uptake outside the urban core.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

IT Services contributed the largest 32.08% slice of the Thailand ICT market share in 2025, led by managed services contracts and multi-cloud migration projects. Telecom operators outsource network operations centers, and manufacturers engage system integrators for predictive-maintenance deployments. Within this umbrella, Cloud Services is forecast to grow at an 11.45% CAGR as enterprises refactor monolithic applications into API-driven microservices. Hardware demand holds steady on the back of 5G radio upgrades and data-center capital expenditure, while cybersecurity outlays accelerate due to persistent threat vectors.

The migration from capex to opex spending reshapes vendor revenue models. PTT Exploration and Production's move to a cloud-native development platform reduced application release cycles by 480%, illustrating payoffs realized when legacy systems are modernized. Edge-computing appliances proliferate in manufacturing plants to meet low-latency requirements, creating fresh revenue for hardware vendors certified under National Broadcasting and Telecommunications Commission standards. The Thailand ICT market incorporates low-code development tools that empower business analysts to prototype applications, easing pressure on scarce developer talent.

The Thailand ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, Communication Services), End-User Enterprise Size (Small and Medium Enterprises, Large Enterprises), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, and More). The Market Forecasts are Provided in Terms of Value (USD).