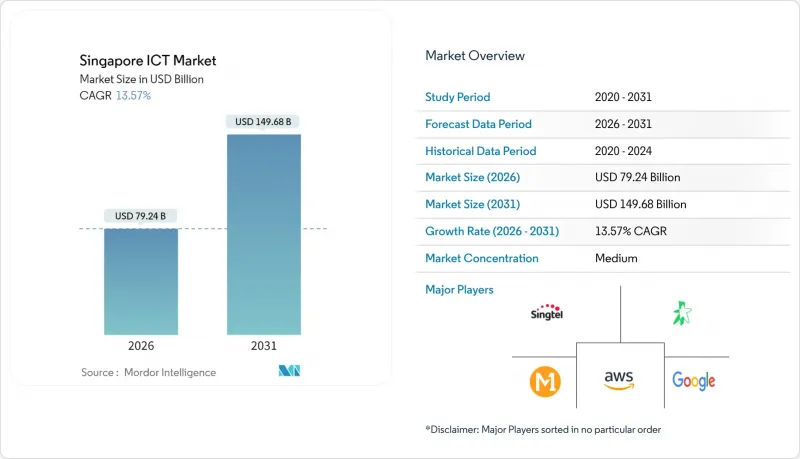

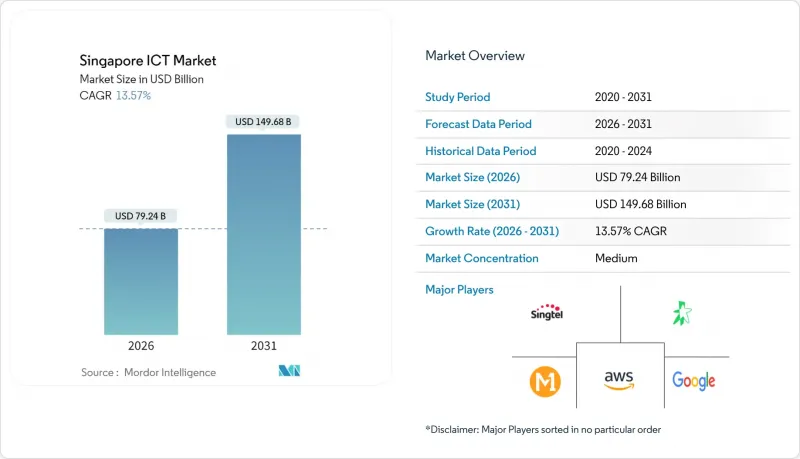

싱가포르의 ICT 시장은 2025년 697억 7,000만 달러에서 2026년에는 792억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 13.57%로 추이하며, 2031년까지 1,496억 8,000만 달러에 달할 것으로 예측되고 있습니다.

싱가포르의 급격한 성장은 스마트네이션 2.0의 자금 조달, 하이퍼스케일 데이터센터 투자, 기업의 클라우드 및 AI 플랫폼으로의 전환 가속화에 힘입은 바 있습니다. 다국적 클라우드 프로바이더들은 현지 용량 확대를 위해 경쟁하는 반면, 중소기업(SME)은 SaaS(Software as a Service)를 활용하여 대기업과의 역량 격차를 메우고 있습니다. 또한 의료 분야의 디지털화, 디지털 전문 은행 면허, 고급 분석의 장벽을 낮추는 국가 AI 계산 자원(NACR)의 도입도 업계의 추진력을 높이고 있습니다. 그러나 지출 증가는 전력망의 한계와 사이버 보안 인력 부족과 충돌하여 운영 비용 상승과 프로젝트 리드 타임의 장기화를 초래하고 있습니다.

스마트 네이션 2.0은 싱가포르를 디지털 도입에서 디지털 퍼스트 거버넌스로 전환하기 위해 2024년도에 사이버 보안, 데이터 플랫폼, 현대화된 인프라에 33억 달러를 투자할 예정입니다. 이 지출은 분석 엔진, 엣지 디바이스, 실시간 처리 툴의 조달을 가속화하여 공공 부문을 넘어선 수요를 창출할 것입니다. 이러한 기준을 반영하는 규제 요건으로 인해 특히 금융 및 의료 분야의 민간 조직은 레거시 시스템을 업데이트해야 하는 상황에 처해 있습니다. API 오케스트레이션과 크로스 플랫폼 보안을 전문으로 하는 벤더는 대규모 다년 계약을 직접 수주할 수 있으며, 상호 운용 가능한 프레임워크는 산업 간 통합의 마찰을 줄일 수 있습니다.

클라우드 우선 정책으로 인프라 계획이 전환되면서 클라우드 워크로드는 17.7% 증가한 반면, On-Premise 구축은 11.2% 성장에 그쳤습니다. 멀티 클라우드 전략은 벤더 종속성을 줄이고 데이터 주권 규제를 충족하기 위해 35억 달러 규모의 국내 클라우드 시장을 주도하고 있습니다. 중소기업은 구독형 AI, 분석, 자동화를 활용하여 대기업 수준의 역량을 확보하기 위해 가장 빠른 속도로 AI를 도입하고 있습니다. 분산 환경의 규제 준수를 위한 통합 모니터링 대시보드, 하이브리드 연결 기반, 자동화된 정책 거버넌스에 대한 2차적 수요도 나타나고 있습니다.

사이버 보안 전문가가 2,800-4,400명 부족한 상황은 도입 일정 지연과 인건비 상승을 초래하고 있습니다. 한편, 보안 수요는 2029년까지 48억 2,000만 달러에 달할 것으로 예측됩니다. 이 부족은 AI 엔지니어와 클라우드 아키텍트에도 영향을 미치고, 중소기업은 다국적 기업과 보상 측면에서 경쟁할 수 밖에 없습니다. IBM의 'SkillsBuild' 등 정부 지원 기술 향상 프로그램(4,500명의 학습자 대상)을 통해 부족분은 점진적으로 해소되고 있습니다. 따라서 기업은 부족한 전문인력에 대한 의존도를 낮추는 로우코드 플랫폼, AI 지원 개발, 매니지드 서비스로의 전환을 꾀하고 있습니다.

2025년 기준 IT 인프라는 싱가포르 ICT 시장 규모의 25.86%를 차지하며, 데이터센터, 네트워크 장비, 서버 용량에 대한 지속적인 투자가 이루어지고 있습니다. AWS의 120억 달러 계획 등 하이퍼스케일 확장 노력이 이 부문을 견인하고 있지만, 가상화로 인한 서버 랙의 고밀도화에 따라 전년 대비 성장률은 둔화되는 추세입니다. IT 소프트웨어는 클라우드 네이티브 플랫폼, AI 툴체인, 워크플로우 자동화 제품군에 힘입어 16.35%의 연평균 복합 성장률(CAGR)로 다른 카테고리를 능가하는 성장세를 보이고 있습니다. 이러한 소프트웨어로의 전환은 컨테이너 오케스트레이션, 마이크로서비스 보안, 애자일 통합 서비스에 대한 수요를 증가시키고 있습니다. 인프라와 용도의 병행적 확장이 균형 잡힌 성장 기반을 지원하고 있습니다. 기업용 소프트웨어의 경우 구독형 요금제 도입이 증가하고 있으며, 이는 설비투자의 급격한 증가를 억제하고 현금흐름을 평준화시키고 있습니다. 하드웨어 분야는 상품화로 인해 이익률이 축소되는 반면, 특화된 AI 가속기나 엣지 디바이스는 프리미엄 가격을 유지하고 있습니다. SAP와 같은 주요 벤더들은 싱가포르에 R&D 거점을 두고 산업별 AI 모델과 현지 이용 사례를 연계하는 '디지털 혁신 액셀러레이터'를 운영하고 있습니다. 대용량 인프라와 첨단 소프트웨어의 상호 작용은 선순환을 만들어 싱가포르 ICT 시장의 상승 궤도를 유지하고 있습니다.

2025년 기준 싱가포르 ICT 시장의 66.78%를 대기업이 차지하고 있으며, 예산과 사내 인력을 활용하여 복잡한 멀티 도메인 디지털화를 추진하고 있습니다. 그러나 많은 기업이 이미 1차 전환을 완료했으므로 성장률은 12.84%로 둔화되었습니다. 반면 중소기업은 정부 보조금과 도입 주기를 단축하는 클라우드 계약에 힘입어 14.88%의 연평균 복합 성장률(CAGR)을 기록했습니다. 턴키 AI 서비스의 보급 확대로 소규모 기업도 고가의 하드웨어를 소유하지 않고도 챗봇, 분석 툴, 로보틱 프로세스 자동화(RPA)를 통합할 수 있게 되었습니다. 인재 육성 구상이 중소기업에 디지털 인재 공급 파이프라인을 유지하고 있습니다. IBM의 'SkillsBuild'는 데이터 분석 및 사이버 보안 분야의 무료 자격증 과정을 제공하는 한 예입니다. 생산성 솔루션 보조금과 같은 재정적 인센티브는 대상 기술 투자의 최대 70%를 상환하여 도입 조건의 평준화를 더욱 촉진하고 있습니다. 중소기업이 규모를 확대함에 따라 매니지드 서비스 프로바이더와 부가가치 재판매 업체에게 중요한 고객 기반을 형성하고 싱가포르 ICT 시장을 지원하는 다양한 벤더 생태계를 강화하고 있습니다.

The Singapore ICT market is expected to grow from USD 69.77 billion in 2025 to USD 79.24 billion in 2026 and is forecast to reach USD 149.68 billion by 2031 at 13.57% CAGR over 2026-2031.

Singapore's surge pivots on Smart Nation 2.0 funding, hyperscale data-center investments, and accelerated enterprise migration to cloud and AI platforms. Multinational cloud providers are racing to expand local capacity, while small and medium enterprises (SMEs) leverage software-as-a-service to close capability gaps with larger rivals. Sector momentum is also reinforced by healthcare digitalization, digital-only banking licenses, and the National AI Compute Resource (NACR) that lowers barriers to advanced analytics. Heightened spending, however, collides with power-grid limits and a widening cybersecurity talent gap that lifts operating costs and elongate project lead times.

Smart Nation 2.0 moves Singapore from digital adoption toward digital-first governance, channeling USD 3.3 billion in fiscal 2024 into cybersecurity, data platforms, and modernized infrastructure. The outlay accelerates procurement of analytics engines, edge devices, and real-time processing tools, catalyzing demand far beyond the public sector. Regulatory requirements that mirror these standards push private organizations, especially in finance and healthcare, to upgrade legacy systems. Vendors specializing in API orchestration and cross-platform security gain direct access to large multi-year contracts, while interoperable frameworks reduce integration friction across verticals.

Cloud-first policies have flipped infrastructure planning, with cloud workloads growing 17.7% against 11.2% for on-premise deployments. Multi-cloud strategies lessen vendor lock-in and satisfy data-sovereignty rules, prompting a USD 3.5 billion domestic cloud market. SMEs drive the fastest uptake, using subscription-based AI, analytics, and automation to match big-company capabilities. Secondary demand is emerging for unified observability dashboards, hybrid connectivity fabrics, and automated policy governance that keep distributed environments in regulatory compliance.

A shortage of 2,800 to 4,400 cybersecurity professionals shackles rollout schedules and elevates salary costs, even as security demand is set to hit USD 4.82 billion by 2029. The gap extends to AI engineers and cloud architects, forcing SMEs to compete with multinationals on compensation. Government-backed upskilling programs, including IBM's SkillsBuild, which targets 4,500 learners, will narrow deficits only gradually. Firms therefore pivot to low-code platforms, AI-assisted development, and managed services that reduce reliance on scarce specialists.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

IT infrastructure owned 25.86% of Singapore ICT market size in 2025, underlining continued investment in data centers, networking gear, and server capacity . The segment benefits from hyperscale expansion commitments such as AWS's USD 12 billion plan, but year-on-year growth is moderating as virtualization densifies server racks. IT software outpaces all other categories with a 16.35% CAGR, propelled by cloud-native platforms, AI toolchains, and workflow automation suites. This software pivot lifts demand for container orchestration, micro-services security, and agile integration services. Parallel expansion of infrastructure and applications underpins a balanced growth profile. Companies increasingly adopt subscription pricing for enterprise software, flattening capex spikes and smoothing cash flows. Hardware margins tighten amid commoditization, though specialized AI accelerators and edge devices command premiums. Major vendors such as SAP anchor R&D in Singapore, exemplified by its Digital Innovation Accelerator that aligns industry-specific AI models with local use cases . The interplay of high-capacity infrastructure with advanced software creates a virtuous cycle that keeps the Singapore ICT market on its upward trajectory.

Large enterprises held 66.78% of Singapore ICT market share in 2025, leveraging budgets and in-house talent to execute complex, multi-domain digitization. Growth, however, is slowing to 12.84% as many have already completed first-wave transformations. SMEs, in contrast, are posting a 14.88% CAGR, driven by government grants and cloud subscriptions that compress deployment cycles. The widening availability of turnkey AI services empowers small firms to integrate chatbots, analytics, and robotic process automation without owning expensive hardware. Training initiatives keep the pipeline of digital talent flowing to smaller companies. IBM's SkillsBuild is one example that provides free certification tracks for data analytics and cybersecurity . Financial incentives such as the Productivity Solutions Grant reimburse up to 70% of qualifying tech investments, further equalizing adoption conditions. As SMEs scale, they form a sizeable customer base for managed-service providers and value-added resellers, reinforcing a diversified vendor ecosystem that underpins the Singapore ICT market.

The Singapore ICT Market Report is Segmented by Type (IT Hardware, IT Software, and More), End-User Enterprise Size (Small and Medium Enterprises and Large Enterprises), Deployment Model (On-Premise, and More), and End-User Industry (Government and Public Administration, and More). The Market Forecasts are Provided in Terms of Value (USD).