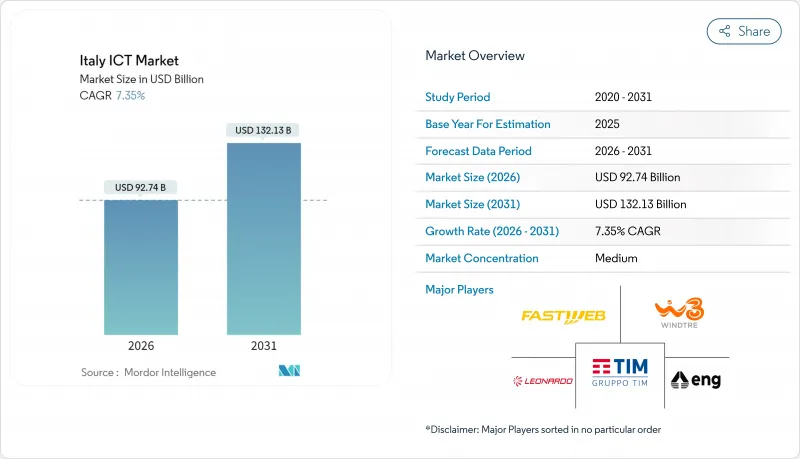

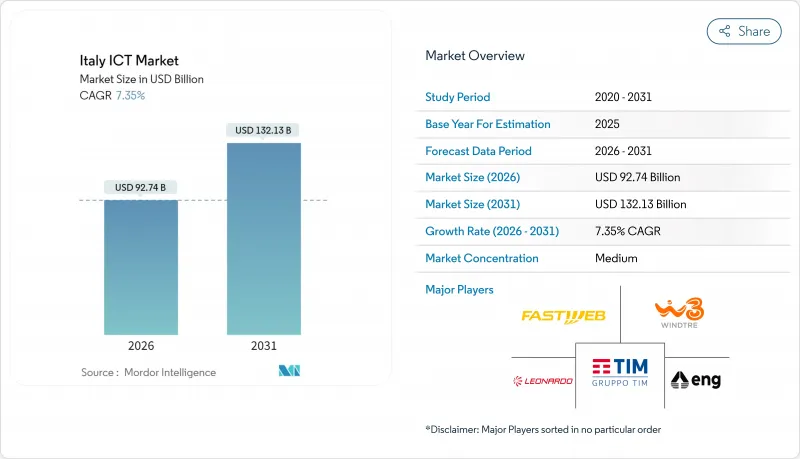

이탈리아의 ICT 시장 규모는 2025년에 863억 9,000만 달러로 평가되었고, 2026년 927억 4,000만 달러에서 2031년까지 1,321억 3,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 7.35%를 나타낼 것으로 예상됩니다.

현재의 성장세는 정부의 국가 회복 및 회복탄력성 계획, 민간 부문의 자본 유입, 레거시 시스템 의존도를 낮추는 주권 클라우드 아키텍처로의 급속한 전환에서 비롯됩니다. 북부 제조 허브에서의 엣지 컴퓨팅 시범 운영, 전국적인 5G 밀도 강화, 급증하는 사이버 보안 지출은 데이터 중심 서비스로의 전환을 가속화하고 있습니다. 동시에 하이퍼스케일러와 국내 사업자들의 투자 확대는 이탈리아의 ICT 시장을 유럽 디지털 가치 사슬의 핵심 부분으로 자리매김하게 합니다. 패스트웹(Fastweb)과 보다폰(Vodafone)의 통합으로 경쟁 강도가 높아졌습니다. 이 통합으로 기존 사업자 TIM의 인프라에 더해 두 번째 풀서비스 네트워크가 도입되어 더 넓은 연결 옵션을 제공하고 가격을 낮추는 효과를 가져왔습니다.

'피아노 트랜지치오네 5.0' 은 기업 디지털화와 에너지 효율성에 138억 달러를 투입하여 클라우드, 사이버 보안, 데이터 통합 도구에 대한 기록적인 구매 주문을 촉발했습니다. EU 회복 기금의 최소 20%를 디지털 목표에 할당하는 배분 규칙은 지출 여력을 더욱 확대합니다. 메조조르노 지역에 현지 공급 시설을 구축하는 공급업체들은 3억 2,700만 달러 규모의 남부 이탈리아 예산 라인의 혜택을 받으며, 이는 지역 격차를 해소하는 동시에 전통적으로 서비스가 부족한 지방의 수요를 끌어올립니다. 이 자금 지원 주기는 2029년까지 이탈리아의 ICT 시장을 지원하여 시스템 통합업체와 통신 사업자에게 예측 가능한 파이프라인을 창출합니다.

TIM은 2024년 클라우드 매출이 19% 성장했으며, 사이버 보안 부문의 매출은 두 배로 증가하여 클라우드 도입과 보안 수요 증가 간의 연관성을 입증했습니다. 마이크로소프트는 이탈리아 신규 데이터센터 지역 및 AI 연구소에 47억 달러를 투자하기로 약속했으며, AWS는 5년간 GDP에 9억 5,800만 달러를 투입할 엣지 존에 13억 달러를 추가 투자했습니다. 이러한 움직임은 지연 시간을 줄이고 데이터 주권 규정을 해결하며 애플리케이션 개발자를 지역 생태계로 끌어들이는 동시에 이탈리아의 ICT 시장을 활성화합니다. 현지 가용 영역과 온프레미스 엣지 서버를 결합한 하이브리드 아키텍처는 이제 대형 제조업체와 은행의 표준이 되어 2027년까지 워크로드 마이그레이션을 가속화할 것입니다.

이탈리아 국민의 기초적인 디지털 능력 보유율은 45%에 그치고, EU가 2030년까지 달성을 목표로 하는 80%의 목표를 밑돌고 있습니다. 이미 10,000명이 넘는 사이버 보안 인력이 부족하여 2027년까지 17만 5,000명의 ICT 인력 부족이 발생할 수 있어 임금 상승과 프로젝트 사이클의 장기화를 초래하고 있습니다. 대학이 배출하는 ICT 졸업생은 연간 44,000명인 반면, 필요한 인재는 88,000명에 달할 전망입니다. 이 때문에 기업은 인재의 수입이나 전문 업무의 외부 위탁을 강요하고 있습니다. PNRR(국가 부흥 및 회복 계획)과 민간 아카데미의 역량 향상 프로그램은 일정한 효과가 기대되지만, 구조적인 개선은 2028년까지 전망할 수 없으며, 이탈리아의 ICT 시장의 성장 페이스는 두드러질 전망입니다.

통신 서비스는 2025년 이탈리아의 ICT 시장에서 34.12%의 점유율을 차지했으며, 이는 상당한 규모의 5G 및 광섬유 백홀 자본 지출을 반영합니다. IT 보안/사이버보안 시장은 국가 사이버보안 전략 하에 은행, 공공기관 등이 핵심 업무 부하를 강화함에 따라 연평균 12.4% 성장률을 보이고 있습니다. 이탈리아 보안 ICT 시장 규모는 2025년 24억 7,000만 달러에 달했으며, 위협 방위 프로젝트에 배정된 24억 달러와 함께 성장할 전망입니다.

2025년부터 2026년에 걸쳐 109억 달러 규모의 엣지 대응 데이터센터 건설이 하드웨어 판매를 밀어 올리는 한편, 소매 및 물류 분야의 클라우드 네이티브 개발과 로우 코드 도입이 소프트웨어 수요를 주도합니다. IT 서비스 공급업체는 중소기업의 변혁 업무 아웃소싱으로 혜택을 보며, 하이퍼스케일러의 현지화 역량 확대로 클라우드 부문은 두 자릿수 성장을 기록하고 있습니다. 이러한 변화들은 이탈리아의 ICT 시장이 기존 통신 수익원을 넘어 성장 동력을 유지할 것임을 시사합니다.

대기업은 다년간의 디지털 아젠다와 내부 IT 팀 덕분에 2025년 이탈리아의 ICT 시장의 59.15%를 점유했습니다. 이들은 현재 AI 강화 분석, 주권 데이터 패브릭, 제로 트러스트 아키텍처를 우선시합니다. 반면 중소기업은 연평균 7.95%의 성장률로 지출을 확대할 것으로 예상되어 디지털 격차를 좁히고 잠재 수요를 확대할 전망입니다. 남부 이탈리아에서 시행 중인 3억 2,700만 달러 규모의 바우처 제도와 보조금 지원 광대역 요금제는 진입 장벽을 낮춥니다.

그러나 중소기업 조달은 여전히 분산되어 있어 사업자들이 연결성, 클라우드, 보안을 고정 가격 패키지로 묶어 제공하는 추세다. 패스트웹과 보다폰의 기업 비즈니스 유닛은 이러한 통합 상품으로 2025년 1분기 2.7% 매출 성장을 기록했습니다. 사용자 친화적 포털, 이중 언어 지원, 성장에 따른 유연한 요금제를 결합한 공급업체들이 이탈리아의 ICT 시장의 추가 기회를 선점할 위치에 있습니다.

The Italy ICT market was valued at USD 86.39 billion in 2025 and estimated to grow from USD 92.74 billion in 2026 to reach USD 132.13 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

Current momentum stems from the government's National Recovery and Resilience Plan, private-sector capital inflows, and rapid migration toward sovereign cloud architectures that reduce legacy system dependence. Edge computing pilots in Northern manufacturing hubs, nationwide 5G densification, and fast-growing cybersecurity spend reinforce the shift toward data-centric services. At the same time, heightened investment from hyperscalers and domestic operators positions the Italy ICT market as a core part of Europe's digital value chain. Competitive intensity has risen following the Fastweb + Vodafone integration, which introduced a second full-service network alongside incumbent TIM's infrastructure, enabling broader connectivity options and nudging prices lower.

The Piano Transizione 5.0 channelled USD 13.8 billion into enterprise digitalisation and energy efficiency, triggering record purchase orders for cloud, cybersecurity, and data integration tools . Allocation rules that earmark at least 20% of EU Recovery funds for digital objectives further extend the spending runway. Vendors that establish local delivery facilities in Mezzogiorno benefit from a USD 327 million Southern Italy budget line, which addresses regional gaps while lifting demand in traditionally underserved provinces. The funding cycle supports the Italy ICT market through 2029, creating a predictable pipeline for system integrators and telecom carriers.

TIM recorded 19% cloud revenue growth in 2024, while its cybersecurity unit doubled sales, proving the link between cloud adoption and stronger security demand . Microsoft pledged USD 4.7 billion for new Italian data-center regions and AI labs, and AWS added USD 1.3 billion for edge zones that will inject USD 958 million into GDP over five years. These moves lower latency, address data-sovereignty rules, and draw application developers into local ecosystems, fuelling the Italy ICT market. Hybrid architectures that combine local availability zones with on-premise edge servers are now standard for large manufacturers and banks, accelerating workload migration through 2027.

Only 45% of Italians hold basic digital capabilities, below the EU's 80% target for 2030. Unfilled cybersecurity roles already exceed 10,000, and a 175,000-person ICT shortage is possible by 2027, squeezing wages and elongating project cycles. Universities produce 44,000 ICT graduates per year against 88,000 needed, prompting firms to import talent or outsource specialised tasks. Upskilling programmes in the PNRR and private academies help, yet structural relief will not arrive before 2028, capping the growth pace of the Italy ICT market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Communication Services contributed a 34.12% share to the Italy ICT market in 2025, reflecting sizeable 5G and fiber backhaul capex. IT Security/Cybersecurity is expanding at an 12.4% CAGR as banks, utilities, and public agencies harden critical workloads under the National Cybersecurity Strategy. The Italy ICT market size for security reached USD 2.47 billion in 2025 and is projected to grow alongside USD 2.4 billion earmarked for threat-defence projects.

Edge-enabled data-center builds worth USD 10.9 billion for 2025-2026 elevate hardware sales, while software demand is fuelled by cloud-native development and low-code adoption in retail and logistics. IT Services vendors benefit from SMEs that outsource transformation tasks, and cloud units record double-digit gains as hyperscalers localise capacity. Together these shifts indicate the Italy ICT market will carry momentum beyond traditional telecom revenue streams.

Large Enterprises captured 59.15% of the Italy ICT market in 2025 thanks to multi-year digital agendas and in-house IT teams. They now prioritise AI-enhanced analytics, sovereign data fabrics, and zero-trust architectures. Conversely, SMEs are expected to expand spending at 7.95% CAGR, narrowing the digital divide and broadening addressable demand. Voucher schemes worth USD 327 million in Southern Italy, plus subsidised broadband tariffs, lower entry barriers.

SME procurement, however, remains fragmented, prompting operators to bundle connectivity, cloud, and security into fixed-price packages. Fastweb + Vodafone's Enterprise Business Unit posted 2.7% revenue growth in Q1 2025 on these converged offers. Vendors that combine user-friendly portals, bilingual support, and pay-as-you-grow terms are positioned to capture incremental Italy ICT market opportunities.

Italy ICT Market Report is Segmented by Type (IT Hardware [Computer Hardware, and More], IT Software, IT Services [Managed Service, and More], IT Infrastructure, and More), End-User Enterprise Size (Small and Medium Enterprise, Large Enterprises), End-User Industry (BFSI, IT and Telecom, and More), and Deployment Mode (On-Premise, Cloud). The Market Forecasts are Provided in Terms of Value (USD).