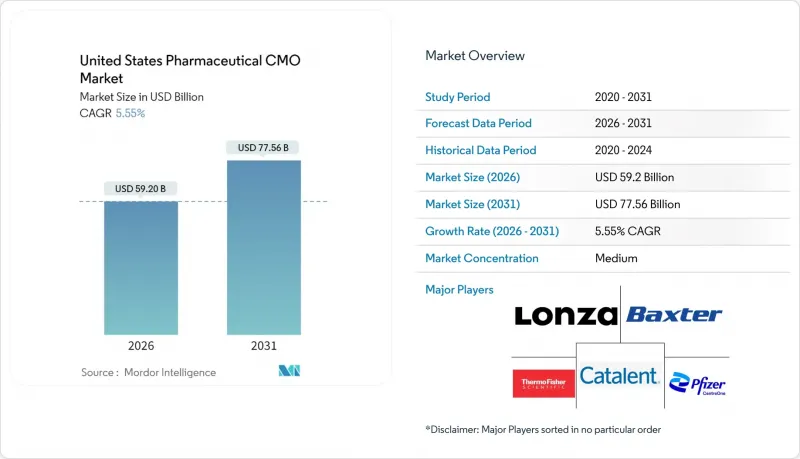

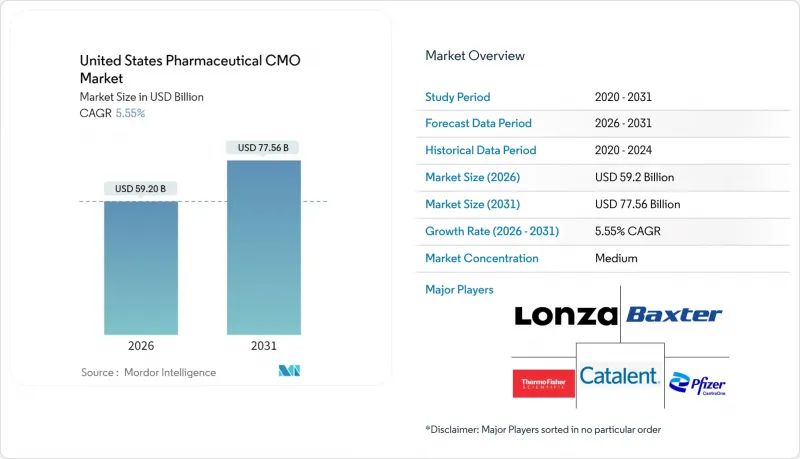

미국의 의약품 CMO 시장은 2025년 560억 9,000만 달러에서 2026년에는 592억 달러로 성장하고, 2026-2031년 CAGR 5.55%로 성장을 지속하여, 2031년까지 775억 6,000만 달러에 이를 것으로 예측되고 있습니다.

이러한 상승 추세는 혁신 기업이 자본 배분을 최적화하고 복잡한 화학 물질 및 생물학적 제제에 대한 외부 전문 지식을 활용하면서 전문 아웃소싱으로의 결정적인 전환을 반영합니다. 공급망 보안 관련 법규, 무균 시설의 병목현상, 그리고 빠르게 발전하는 생물학적 제제 파이프라인은 구조적 성장 요인으로 계속 존재할 것입니다. 고활성 API(원료의약품) 시설과 연속 생산 라인에 대한 투자 활동은 지속되는 한편, 바이오보안법으로 인한 니어쇼어링 계획으로 생산은 신뢰할 수 있는 곳으로 회귀하고 있습니다. 경쟁 환경은 기술적 깊이와 규제 대응의 신뢰성을 겸비한 CDMO에 유리하게 작용하고 있습니다. 제약사 스폰서들이 표면적인 가격보다 품질과 중복성을 중시하는 경향이 강해지고 있기 때문입니다. M&A의 활동성은 지속되고 있으며, 수직 통합형 거래가 서비스 범위와 지리적 확장을 재구성하고 있습니다.

제약 스폰서들은 고정자산 부담을 가변적 비용의 파트너십과 교환하는 추세가 지속되고 있습니다. 블록버스터 제품군에서 흔히 볼 수 있었던 다년간의 생산 능력 임대는 변화하는 치료법 구성에 대응할 수 있는 유연한 마스터 서비스 계약으로 대체되었습니다. 이 전략은 연구개발 자금을 확보하여 CDMO의 현대화를 촉진하고, 자산 경량화 운영 모델을 요구하는 투자자의 압력에 부합합니다. 파이프라인은 풍부하지만 자본에 제약이 있는 신생 바이오기업들은 현재 cGMP 역량을 거의 전적으로 아웃소싱에 의존하고 있으며, 이러한 의존성은 미국의 의약품 CMO 시장이 쉽게 수익화할 수 있는 부분입니다.

단일클론항체, 세포치료제, 유전자 편집 구조체는 장기적인 생산 수요를 창출하고 있지만, 이를 자체적으로 충족시킬 수 있는 원료의약품 제조업체는 거의 없습니다. 바이오 의약품에 필요한 정밀한 환경 제어와 일회용 바이오리액터는 기술적 장벽을 높이고 전문 CDMO의 매력을 증폭시키고 있습니다. 종양학 및 희귀질환 분야의 스폰서 기업들은 소규모 배치 생산, 실시간 분석, 규제 대응이 가능한 엔드투엔드 바이오의약품 파트너를 선호합니다. 이러한 우선순위에 따라 바이오의약품은 미국의 의약품 CMO 시장에서 가장 빠르게 성장하는 수익원으로서 입지를 굳건히 하고 있습니다.

표준화된 저분자 공정은 가격이 규제 리스크 허용치를 초과하는 경우, 여전히 해외 이전이 진행될 것입니다. 아시아 CMO들은 미국 기업에 비해 30-50% 할인을 제시하고 있으며, 상품화된 API의 경우 이 차이는 더욱 확대됩니다. 국내 업체들은 품질 기록, 사이버 복원력, 물류 신뢰성 등의 특성을 강조하며 대응하고 있습니다. 이는 팬데믹 이후 공급망 병목 현상으로 인해 점점 더 엄격하게 심사되는 속성입니다.

2025년 매출에서 API 제조가 차지하는 비중은 41.78%로, 미국의 의약품 CMO 시장 규모에서 API 제조가 차지하는 근본적인 역할을 뒷받침하고 있습니다. 6.41%의 성장 궤적은 복잡한 화학 반응, 고활성 물질의 봉쇄, 입체 선택적 합성에 대한 지속적인 수요를 반영합니다. CDMO는 Kg 규모의 반응기와 제로 액체 배출 설비를 갖춘 CDMO는 특히 고활성 페이로드를 필요로 하는 종양학 파이프라인을 위한 장기 공급 계약을 체결하고 있습니다.

다운스트림 공정의 최종 제제 제조는 고형제, 액상제, 주사제 등으로 나뉘며, 각기 다른 규제 요건을 가지고 있습니다. 무균 충전 및 포장 라인은 설비 부족에 직면하고 있지만, 소유 구조가 분산되어 있음에도 불구하고 높은 수익률을 유지하고 있습니다. 포장 및 표시 서비스는 규모는 작지만 의약품 유통안전강화법(DSCSA)의 직렬화 대응으로 그 중요성이 커지고 있습니다. 미국의 의약품 CMO 시장에서 포장 분야의 점유율은 최종 단계의 맞춤화 및 콜드체인 대응 키트를 제공하는 시설에 편중되어 있습니다.

저분자 의약품은 2025년 56.74%의 점유율을 유지하며, 확립된 공정 노하우와 경구용 고형제에 대한 세계 수요의 혜택을 누릴 것으로 예측됩니다. 그러나 첨단 치료제(세포, 유전자, RNA 기반 제품)는 2031년까지 7.05%의 높은 CAGR을 보이고 있습니다. 스폰서 기업은 B등급 클린룸, 바이러스 벡터용 설비, 폐쇄형 아이솔레이터를 갖춘 CDMO(개발제조수탁기관)를 선호합니다.

바이오로직스는 항체 및 융합단백질 플랫폼의 성숙에 따라 지속적으로 규모를 확장하고 있습니다. 배치 간 변동성과 엄격한 당쇄 프로파일의 요구로 인해 일회용 바이오리액터 그룹과 대용량 크로마토그래피 스키드를 보유한 바이오로직스 전문업체에 아웃소싱을 추진하고 있습니다. 미국 내 첨단 치료제의 의약품 CMO 시장 규모는 여전히 생산능력에 제약이 있어 신규 공장 건설 및 타겟을絞한 인수가 촉진되고 있습니다.

The United States pharmaceutical contract manufacturing market is expected to grow from USD 56.09 billion in 2025 to USD 59.2 billion in 2026 and is forecast to reach USD 77.56 billion by 2031 at 5.55% CAGR over 2026-2031.

This upward trajectory reflects a decisive shift toward specialized outsourcing as innovators optimize capital allocation and tap external expertise for complex chemistries and biologics. Supply-chain security legislation, sterile-facility bottlenecks, and the fast-moving biologics pipeline remain the structural growth drivers. Investment activity continues in high-potency API suites and continuous-manufacturing lines, while near-shoring programs triggered by the BIOSECURE Act are pulling production back to trusted locations. Competitive dynamics favor CDMOs that pair technical depth with regulatory reliability, as pharmaceutical sponsors elevate quality and redundancy over headline pricing. M&A intensity remains high, with vertical integration deals reshaping service breadth and geographic reach.

Pharmaceutical sponsors continue to trade fixed-asset burdens for variable-cost partnerships. Multiyear capacity leases, once typical for blockbuster portfolios, have given way to flexible master service agreements that accommodate changing modality mixes. The strategy frees cash for R&D, presses CDMOs to modernize, and aligns with investor pressure for asset-light operating models. Emerging biotech companies-often pipeline-rich yet capital-constrained-rely almost exclusively on outsourced current-Good-Manufacturing-Practice (cGMP) capability, a reliance that the United States pharmaceutical contract manufacturing market readily monetizes.

Monoclonal antibodies, cell therapies, and gene-editing constructs fuel long-dated manufacturing demand that few originators can meet internally. The precise environmental controls and single-use bioreactors required for biologics raise technical barriers and amplify the appeal of expert CDMOs. Oncology and rare-disease sponsors prefer end-to-end biologics partners capable of small batch runs, real-time analytics, and regulatory engagement. These priorities cement biologics as the fastest-growing revenue stream within the United States pharmaceutical contract manufacturing market.

Standardized small-molecule processes still migrate offshore when pricing eclipses regulatory-risk tolerance. Asian CMOs quote 30-50% discounts versus U.S. peers, a spread that widens for commoditized APIs. Domestic providers counter by emphasizing quality records, cyber-resilience, and logistics reliability-attributes increasingly scrutinized after pandemic bottlenecks.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

API manufacturing contributed 41.78% of 2025 revenues, underscoring its foundational role in the United States pharmaceutical contract manufacturing market size. Growth at a 6.41% trajectory reflects sustained demand for complex chemistries, high-potency containment, and stereoselective syntheses. CDMOs with kilogram-scale reactors and zero-liquid-discharge utilities secure long-term supply agreements, particularly for oncology pipelines requiring potent payloads.

Downstream, finished-dosage manufacture encompasses solid, liquid, and injectable routes, each with distinct compliance regimes. Sterile fill-finish lines confront capacity scarcity, supporting higher margins despite fragmented ownership. Packaging and labeling services, though smaller, gain relevance under DSCSA serialization. The United States pharmaceutical contract manufacturing market share in packaging tilts toward facilities offering late-stage customization and cold-chain kitting.

Small molecules retained a 56.74% share in 2025, benefiting from entrenched process know-how and global demand for oral solids. Yet advanced therapies-cell, gene, and RNA-based products-post a leading 7.05% CAGR to 2031. Sponsors favor CDMOs equipped with Grade B cleanrooms, viral-vector suites, and closed-system isolators.

Biologics continue to scale as antibody and fusion-protein platforms mature. Batch variability and stringent glycosylation profiles spur outsourcing to biologics specialists with single-use bioreactor fleets and high-capacity chromatography skids. The United States pharmaceutical contract manufacturing market size for advanced therapies remains capacity-constrained, incentivizing greenfield builds and targeted acquisitions.

The United States Pharmaceutical CMO Market Report is Segmented by Service Type (API Manufacturing, Secondary Packaging, and More), Drug Molecule Type (Small Molecule, Biologics, and More), Scale of Operation (Clinical-Phase Manufacturing, Commercial-Scale Manufacturing), End User (Big Pharma, Generic Pharma, and More), Therapeutic Area (Oncology, Cardiovascular, and More). The Market Forecasts are Provided in Terms of Value (USD).