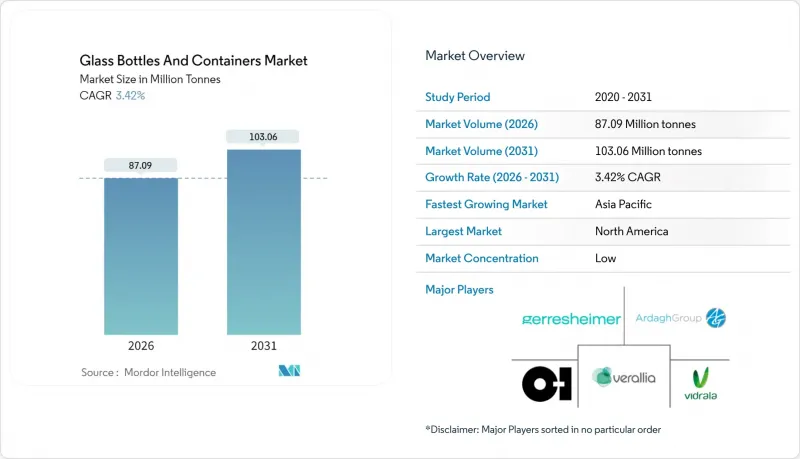

유리병 및 용기 시장은 2025년 8,421만 톤에서 2026년에는 8,709만 톤으로 성장하고, 2026-2031년 CAGR 3.42%로 성장을 지속하여, 2031년까지 1억 306만 톤에 이를 것으로 예측되고 있습니다.

에너지 가격 상승이라는 역풍에도 불구하고 일회용 플라스틱에 대한 규제 강화, 미용 및 주류 분야의 프리미엄화, 의약품 충진 및 마감 공정의 확대가 꾸준한 성장을 견인하고 있습니다. 캘리포니아주의 플라스틱 65% 감축 의무화, 프랑스의 폴리스티렌 금지 조치로 인해 이미 수요는 무한히 재활용 가능한 유리로 전환되고 있습니다. 하이브리드 용해로, 산소 연소 기술, 고칼렛 배합 레시피는 비용 리스크를 줄이는 한편, 비드라라의 260g 75cl 병과 같은 경량화 혁신은 디스플레이 효과를 손상시키지 않으면서 재료 사용량을 줄입니다. 제조업체는 특히 호박색으로 색조 차별화를 통해 빛에 민감한 의약품과 공예 음료를 보호하고 더 밝은 대체품에 대한 가치를 강화합니다.

캘리포니아주 SB54법은 2032년까지 일회용 플라스틱 포장을 65% 감축하도록 규정하고 있으며, 프랑스에서는 2025년 1월부터 스티로폼 식품 용기의 사용이 금지됨에 따라 브랜드 소유주들은 유리로 전환을 추진하고 있습니다. 유럽연합(EU)에서 논의 중인 비스페놀 A 규제는 식품 접촉 분야의 전환을 더욱 촉진할 것입니다. 유리는 무한한 폐쇄 루프를 유지하며, 확립된 문별 회수 시스템이 있기 때문에 컨버터는 설비 갱신 비용을 흡수하면서 새로운 수요를 창출하고 있습니다. 이러한 파급효과는 대형 소매점의 음료 및 조미료 라인의 유리 용기 회귀에서 두드러지게 나타납니다. 일시적인 칼렛 공급 부족, 하이브리드 용광로와 경량화가 마진 압축을 부분적으로 상쇄하여 예측 기간 동안 지속적인 상승 추세를 이끌었습니다.

고급 스킨케어 및 향수 브랜드들은 프리미엄 품질과 친환경성을 강조하기 위해 유리 용기를 확대 적용하고 있습니다. 베라리아의 100% 재생유리(PCR) 비스타보틀은 신규 원료 생산 대비 에너지 사용량을 40% 절감하여 순환형 사회와 고급스러움의 공존을 입증했습니다. 엠보싱, 그라데이션 컬러, 리필 가능한 디자인은 매장에서의 차별화를 강화하여 높은 가격대의 정당성을 뒷받침합니다. 화장품 업계에서는 포장 비용이 소매 가격에서 차지하는 비중이 작기 때문에 브랜드는 일반 음료 시장보다 단가 상승을 더 쉽게 흡수할 수 있습니다. 이러한 추세는 전 세계적으로 확대되고 있으며, 특히 북미와 서유럽에서 두드러지게 나타나고 있으며, 맞춤형 금형 및 소량 생산에 대한 롱테일 수요를 강화하고 있습니다.

2024년 영국의 전력 가격이 사상 최고 수준으로 치솟아 유리 제조업체들은 피크 요금 시간대에 생산 라인을 중단해야 했습니다. 에너지 비용은 제조 원가의 약 18%를 차지하기 때문에 가격 조정이 시장에 반영되기 전에 변동이 발생하면 수익률이 빠르게 하락할 수 있습니다. 탄소가격제는 화석연료 소비에 대한 추가적인 부담으로 작용하고 있으며, 하이브리드 원자로 및 자체 발전설비에 대한 자본투입을 가속화하고 있습니다. 한편, O-I Glass는 탈탄소화를 위해 1억 2,500만 달러의 연방 자금을 확보했지만, 중소규모의 지역 공장은 자금난에 시달리고 있어 단기적으로 공급 감소로 이어질 수 있습니다.

북미는 2025년 기준 용기용 유리 포장 시장의 55.18%를 차지할 것으로 예상되며, 이는 성숙한 문전수거 시스템과 고칼렛 배합을 촉진하는 기업의 지속가능성 목표를 배경으로 하고 있습니다. 유리포장협회가 제시한 2030년까지 재활용률 50% 달성 로드맵은 장기적인 원료 기반을 뒷받침하고 있습니다. 그러나 에너지 가격 변동과 저가 음료 분야에서의 재생 PET(rPET) 보급 확대가 물량 증가를 억제하고 있으며, 전략적 초점은 프리미엄 주류와 뷰티 케어 분야로 이동하고 있습니다.

유럽은 뒤쳐져 있지만, EU 역내 80.8%의 재활용률로 인해 칼렛 공급이 확보되어 용해로의 에너지 수요가 감소하는 혜택을 누리고 있습니다. Ardagh와 Verallia는 배출권 거래 리스크를 헤지하면서 생산량을 유지하기 위해 전기 보조식 및 수소 대응 용해로에 대한 투자를 진행하고 있습니다. 그러나 전력 가격의 압박과 환경세 부과로 인해 단기적인 수익률을 억제하고 있으며, 공유형 재생에너지 마이크로그리드 및 국경을 초월한 카렛 거래에 대한 협력이 활발해지고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR) 4.76%로 성장하여 용기용 유리 포장 시장의 격차를 빠르게 좁히고 있습니다. 인도와 중국에서는 무균 바이알을 필요로 하는 신규 제약 공장이 건설되고 있으며, 한국과 일본에서는 고급 스킨케어 제품용 프리미엄 화장품용 유리를 수입하고 있습니다. 콜롬비아 지파키라에 위치한 O-I Glass의 1억 2,000만 달러 규모의 설비 갱신은 신흥 지역에서 최첨단 기술을 재현하고 수요를 확보하는 동시에 ESG 요건을 충족하는 생산자의 자세를 보여주고 있습니다. 동남아시아 일부 지역의 경우, 칼렛 처리 인프라가 제한적이고 재생원료 사용률에 제약이 있어 유럽 및 미국 경쟁사 대비 비용 측면에서 불리한 상황입니다. 그러나 소득수준의 상승과 순환경제 추진을 위한 규제 강화로 인해 장기적으로 견조한 수요가 예상됩니다.

The Glass Bottles and Containers market is expected to grow from 84.21 million tonnes in 2025 to 87.09 million tonnes in 2026 and is forecast to reach 103.06 million tonnes by 2031 at 3.42% CAGR over 2026-2031.

Heightened regulatory pressure on single-use plastics, premiumization in beauty and spirits, and pharmaceutical fill-finish expansion are steering steady gains despite energy-price headwinds. California's 65% plastic-reduction mandate and France's polystyrene ban have already swung demand toward infinitely recyclable glass.Hybrid furnaces, oxy-fuel combustion, and high-cullet recipes are mitigating cost exposure, while lightweighting breakthroughs such as Vidrala's 260-gram 75 cl bottle trim material intensity without sacrificing shelf appeal. Producers also leverage color differentiation, especially amber, to protect light-sensitive drugs and craft beverages, reinforcing value over lighter substitutes.

California's SB 54 mandates a 65% cut in single-use plastic packaging by 2032, while France has barred expanded polystyrene food containers from January 2025, propelling brand owners to switch to glass. The European Union's pending bisphenol-A restrictions further reinforce conversion in food contact segments. Because glass maintains an endless closed loop and established curb-side collection, converters are capturing new volumes even as they absorb retooling costs. The ripple effect is evident in beverage and condiment lines moving back to glass at big-box retailers. Though cullet supply tightens temporarily, hybrid furnaces and lightweighting partially offset margin compression, paving a sustained uplift through the forecast horizon.

Luxury skincare and fragrance brands increasingly adopt glass to signal premium quality and environmental stewardship. Verallia's 100% post-consumer-recycled (PCR) Vista bottles cut energy use by 40% versus virgin production, proving that circularity can coexist with high-end aesthetics.Embossing, color gradations, and refillable designs amplify shelf differentiation and justify higher price points. Since packaging cost is a small share of retail value in beauty, brands absorb higher unit costs more easily than mass-market beverages. The trend scales globally but is most pronounced in North America and Western Europe, reinforcing long-tail demand for custom molds and short production runs.

Electricity prices in the United Kingdom spiked to record levels in 2024, compelling glassmakers to idle lines during peak tariffs. Energy constitutes roughly 18% of production costs, so volatility can erase margins faster than price adjustments reach the market. Carbon-pricing schemes further penalize fossil-fuel consumption, intensifying capital commitments toward hybrid furnaces and on-site renewables. In contrast, O-I Glass secured USD 125 million in federal funding for decarbonization, but smaller regional plants face liquidity strains, potentially curbing short-term supply.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

North America captured 55.18% of the container glass packaging market in 2025, leveraging mature curbside collection and corporate sustainability goals that encourage high-cullet recipes. The Glass Packaging Institute's roadmap to reach a 50% recycling rate by 2030 underpins the long-term feedstock base. Yet energy-price swings and growing rPET penetration in value beverages temper volume gains, shifting strategic emphasis toward premium spirits and beauty care.

Europe trails but benefits from the EU's 80.8% recycling rate, which secures cullet and lowers furnace energy demand. Ardagh and Verallia are investing in electric-boost and hydrogen-ready furnaces to hedge carbon-pricing exposure while maintaining output. However, power-price stress and environmental levies suppress near-term margins, sparking collaboration on shared renewable micro-grids and cross-border cullet trade.

Asia Pacific is the fastest-growing region, expanding 4.76% CAGR through 2031 and rapidly closing the gap in the container glass packaging market. India and China build greenfield pharmaceutical plants that require sterile vials, while South Korea and Japan import premium cosmetic glass for luxury skincare. O-I Glass's USD 120 million upgrade in Zipaquira, Colombia, signals how producers replicate best-in-class technology in emerging regions to capture demand while aligning with ESG mandates. Limited cullet infrastructure in parts of Southeast Asia constrains recycled content, creating cost penalties versus Western peers; nevertheless, rising incomes and regulatory push for circularity promise robust long-term demand.