유럽의 유리병 및 유리용기 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1628779

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

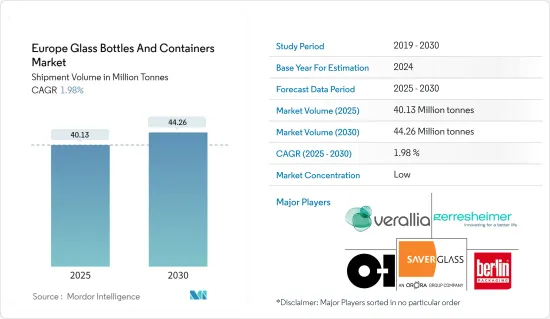

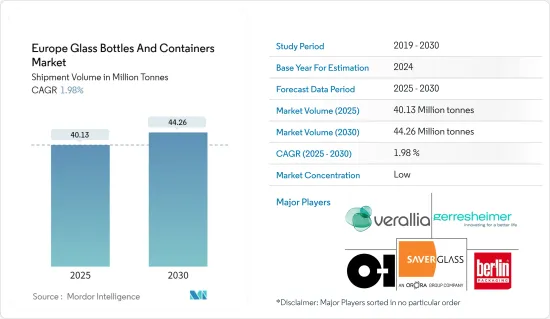

유럽의 유리병 및 유리용기 시장 규모는 출하량 기준으로 2025년 4,013만 톤에서 2030년 4,426만 톤으로 확대될 것으로 예상되며, 예측 기간(2025-2030년) 동안 1.98%의 CAGR을 기록할 것으로 예상됩니다.

유럽의 유리병 및 유리용기 시장은 포장 산업에서 중요한 부문입니다. 지속가능성 트렌드, 고급 포장에 대한 소비자 수요, 플라스틱 폐기물 감소를 목표로 하는 규제 등이 그 원동력이 되고 있습니다. 유럽은 유리 제조 산업이 발달한 지역으로 독일, 이탈리아, 프랑스, 스페인이 유리 생산 및 소비의 중심지입니다.

주요 하이라이트

유럽의 유리 용기 시장은 수십억 유로 규모로 최근 몇 년 동안 꾸준한 성장세를 보이고 있습니다. 음료, 식품, 의약품, 화장품 등 주요 부문의 수요가 이러한 성장을 주도하고 있습니다. 시장은 완만한 성장이 예상되며, 특히 알코올 음료, 화장품, 미식가 식품 등 프리미엄 포장 분야의 증가가 두드러집니다. 와인, 맥주, 증류주 등 알코올 음료가 시장의 대부분을 차지하고 있으며, 주스, 탄산음료 등 다른 음료도 큰 기여를 하고 있습니다.

유리는 재활용이 가능하기 때문에 지속가능성이 높은 포장재입니다. 유럽은 강력한 재활용 정책을 시행하고 있으며, 그 결과 유리 포장의 재활용률이 높고, 많은 국가에서 70%를 초과하는 경우가 많습니다. 플라스틱 폐기물에 대한 우려가 커지면서 유리는 환경 친화적인 대안으로 점점 더 많은 관심을 받고 있습니다.

유럽 소비자들은 유리 포장을 선호하며, 그 이유로 고급 품질, 제품 무결성 유지, 재활용성을 꼽는다. 유리 포장은 고급 제품이나 유기농 제품에 자주 사용되며, EU 순환 경제 행동 계획과 같은 EU의 이니셔티브는 재활용률을 높이고 폐기물을 줄이기 위해 노력하고 있습니다. 유리는 재활용 가능한 재료로서 이러한 목표에 부합하며, 포장 분야에서의 수요를 더욱 증가시키고 있습니다.

가장 큰 분야는 음료이며, 주류(와인, 맥주, 증류주)와 청량음료가 주를 이룹니다. 맛과 품질을 유지하기 위해 유리 병과 병이 선호됩니다. 유리는 불활성이고 무균이기 때문에 제약 산업에서 유리 용기는 의약품, 특히 액체 의약품, 백신 및 시럽 포장에 널리 사용됩니다. 화장품 업계에서는 고급스러움과 기밀성이 뛰어나 스킨케어 제품, 향수, 화장품의 고급 포장에 유리가 사용되고 있습니다.

이 지역은 유리병 및 유리용기 제품 무역에도 참여하고 있습니다. 국제 무역 센터에 따르면 유럽 국가의 유리 용기 생산능력은 크게 다릅니다. 독일이 연간 549만 3,250톤으로 1위, 이탈리아가 489만 7,205톤, 프랑스가 458만 750톤으로 그 뒤를 이었습니다.

유럽의 포장 산업은 전통적인 유리 포장에 대한 대안이 선호되면서 큰 변화를 경험하고 있습니다. 지속가능성에 대한 관심, 비용 효율성, 포장 재료의 기술 발전이 이러한 추세를 주도하고 있습니다. 그 결과, 기존 유리 포장 시장은 새로운 도전에 직면하고 있으며, 바이오플라스틱, 연질 포장, 첨단 고분자 소재와 같은 혁신적인 대체품과의 경쟁에 직면하고 있습니다. 이러한 변화는 소비자의 선호도를 변화시키고, 유리 포장 제조업체는 변화하는 시장 환경에서 시장 점유율을 유지하기 위해 전략을 조정해야 하는 상황에 직면해 있습니다.

유럽의 유리병 및 유리용기 시장 동향

음료 산업이 큰 시장 점유율을 차지

유럽에는 프랑스, 이탈리아, 스페인, 독일 등 세계 유수의 와인 생산국이 있으며, 와인 포장은 유리병이 주류를 이루고 있습니다. 유리는 와인의 풍미, 향기 및 품질을 유지하는 데 가장 적합한 재료로 널리 알려져 있으며 고급 제품과 밀접한 관련이 있습니다. 와인 산업은 유럽에서 유리 용기 수요의 주요 견인차 역할을 계속하고 있으며, 일부 국가에서는 유리 용기가 와인 포장의 80 % 이상을 차지합니다.

프랑스는 유럽 국가 중 최고의 와인 소비국으로 2023년 소비량은 약 2,440만 헥토리터에 달할 것으로 예상됩니다. 이러한 높은 수준의 소비는 프랑스에 깊이 뿌리내린 와인 문화와 일상 생활과 사교 모임에서 와인의 중요성을 반영합니다. 국제 포도-와인기구에 따르면 영국의 와인 소비량은 약 1,280만 헥토리터에 달합니다. 영국의 와인 소비량은 소비자의 취향 변화와 와인에 대한 인식의 변화에 영향을 받아 꾸준히 증가하고 있습니다.

이러한 유럽 전역의 와인 소비 추세는 포장재로서 유리병에 대한 수요가 계속되고 있음을 보여줍니다. 유리병은 와인의 풍미를 보존하고 보존 기간을 연장하며 소비자에게 고급스러운 미적 매력을 제공할 수 있기 때문에 여전히 와인 포장 옵션으로 선호되고 있습니다. 이러한 중요한 유럽 시장에서 와인 소비의 지속적인 성장은 음료 산업에서 고품질 유리 포장 솔루션에 대한 수요가 동시에 증가하고 있음을 시사합니다.

유리 용기 음료 시장은 수제 맥주, 유기농 주스, 고급 증류주 등 프리미엄 및 틈새 시장에서 강세를 보이고 있습니다. 고품질의 친환경 포장 솔루션에 대한 수요가 이러한 카테고리에서 유리 용기의 사용 확대를 주도하고 있습니다. 수제 맥주와 소량 생산 음료는 유리 포장 시장에 큰 기여를 하고 있습니다. 많은 수제 맥주 제조업체와 소규모 음료 제조업체는 고객에게 품질, 전통 및 환경적 책임을 전달하기 위해 유리 병을 선택하고 있습니다.

플라스틱 캔과 알루미늄 캔이 우세함에도 불구하고 유리병은 프리미엄 소다, 유기농 음료, 수제 청량음료 등 청량음료 시장의 틈새 분야에서 여전히 존재하고 있습니다. 천연, 유기농, 건강 지향적 음료 브랜드의 인기가 높아지는 것도 지속가능한 포장 옵션으로 유리를 사용하는 데 한몫을 하고 있습니다. 신선한 주스, 특히 콜드 프레스 주스 및 유기농 주스는 제품의 품질과 맛을 유지할 수 있기 때문에 유리로 포장되는 경우가 많습니다.

유럽에서는 플라스틱 오염에 대한 소비자의 인식이 높아지고 일회용 플라스틱에 대한 규제가 강화되면서 친환경 포장을 선호하는 경향이 강화되고 있습니다. 재활용성이 높고 품질 저하 없이 무기한 재사용이 가능한 유리는 음료 포장에 있어 환경 친화적인 소비자들에게 어필하고 있습니다.

이러한 지속가능한 선택으로의 전환은 제조업체와 소매업체가 음료를 포함한 다양한 제품에 유리 포장을 채택하는 데 영향을 미치고 있습니다. 유리의 재활용성과 재사용 가능성은 순환 경제의 원칙에 부합하며, 유럽 시장에서 유리의 매력을 더욱 높이고 있습니다. 또한, 제품의 품질을 유지하고 유통기한을 연장하는 유리 포장의 특성도 이 지역의 소비자와 생산자들 사이에서 유리 포장의 인기를 높이는 요인으로 작용하고 있습니다.

큰 시장 점유율을 차지하고 있는 독일

독일은 유럽에서 유리 용기의 중요한 시장입니다. 탄탄한 산업 부문, 포장된 제품의 높은 소비량, 지속가능성에 대한 관심이 이 시장을 뒷받침하고 있습니다. 독일에서는 주로 식음료, 화장품, 제약 산업이 유리 용기에 대한 수요를 주도하고 있습니다.

무알콜 음료 분야, 특히 프리미엄 음료 및 유기농 음료 분야에서는 주스 및 건강 음료와 같은 제품에 유리 용기를 사용하고 있습니다. 독일은 맥주의 전통이 강하고 다양한 음료 분야에서 유리 용기를 선호하며, 안전하고 불활성인 포장재를 선호하는 소비자가 많기 때문에 독일 음료 산업에서 유리 용기에 대한 수요는 매우 활발합니다.

Statistisches Bundesamt에 따르면 독일의 알코올 음료에 대한 소비자 지출은 2021년부터 2023년까지 꾸준히 증가하여 2021년에는 29.3억 달러, 2022년에는 29.5억 달러로 소폭 증가했습니다. 이 수치는 307억 달러로 증가하여 지난 3 년 동안 알코올성 음료에 대한 지출의 지속적인 증가 추세를 반영합니다.

독일은 또한 세계 최고의 유리 재활용률을 유지하고 있으며, 유리병의 90% 이상이 재활용되고 있습니다. 환경에 대한 인식이 높아짐에 따라 독일 소비자와 기업은 지속가능한 포장재로 유리를 선택하고 있습니다. 유리는 품질 저하 없이 100% 재활용이 가능하기 때문에 환경 친화적인 재료로 널리 알려져 있습니다. 특히 독일의 포장 폐기물 관련 법규와 재활용 가능한 재료를 장려하는 생산자책임재활용제도(EPR)가 확대되면서 유리 용기에 대한 선호도가 높아지고 있습니다.

독일은 유리병 및 유리용기 제품 수출에 참여하고 있습니다. 국제무역센터에 따르면 독일의 수출량은 2021년 109만 4,706톤에서 2022년 149만 4,488톤으로 36.4% 증가해 큰 폭으로 증가했습니다. 이러한 증가는 독일 제품에 대한 국제적인 수요가 증가하고 있음을 시사합니다. 이러한 증가 요인으로는 팬데믹 이후 경기 회복, 세계 무역 증가 또는 자동차, 화학, 기계, 소비재 등 특정 산업의 호황을 들 수 있습니다.

2023년 수출량은 2022년 최고치 대비 19.4% 감소한 120만 5,642톤으로 소폭 감소했습니다. 이러한 감소는 공급망 혼란, 세계 경제 문제 또는 주요 시장의 수요 패턴 변화로 인한 것으로 추정됩니다. 상품 가격 변동, 국제 수요의 변화, 우크라이나 분쟁을 포함한 지정학적 긴장 등의 요인이 2023년 독일의 수출 실적에 영향을 미쳤을 수 있습니다.

유럽의 유리병 및 유리용기 산업 개요

유럽의 유리병 및 유리용기 시장은 세분화되어 있으며, 많은 기업들이 시장 점유율을 놓고 경쟁하고 있습니다. 이러한 경쟁 환경은 기술 혁신을 촉진하고 다양한 고객 요구에 부응하기 위해 각 회사가 차별화를 추구하도록 장려하고 있습니다. O-I Glass, Inc., SAVERGLASS Group, Berlin Packaging, Verallia Group, Gerresheimer AG와 같은 주요 기업들은 다양한 제품 포트폴리오와 기술 발전으로 시장 점유율을 높이고 있습니다. 등 주요 기업들은 광범위한 제품 포트폴리오, 기술 발전, 전략적 파트너십을 통해 확고한 입지를 구축하고 있습니다.

이러한 기업들과 다른 시장 진입자들은 식품, 의약품, 화장품, 퍼스널케어 등 다양한 분야에서 활동하고 있습니다. 지속가능성과 친환경 패키징 솔루션에 대한 지속적인 관심은 이들 주요 기업의 시장 전략과 제품 개발에도 큰 영향을 미치고 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

유리병 및 유리용기 수출입 데이터

PESTEL 분석 - 유럽의 유리병 및 유리용기 산업

용기포장용 유리 업계 표준과 규제

포장용 유리 원자재 분석과 재료 검토

용기포장용 유리의 지속가능성 동향

유럽의 유리병 및 유리용기 용광로와 입지

제5장 시장 역학

시장 성장 촉진요인

친환경 제품에 대한 수요 증가

식품 및 음료 시장 수요 급증

시장 과제

유리 대체품 채용 증가에 의한 전통 시장 과제

세계의 유리병 및 유리용기 시장의 유럽의 시장 상황 분석

무역 시나리오 - 유럽의 유리병 및 유리용기 산업 수출입 패러다임의 역사와 현황 분석

제6장 시장 세분화

최종 이용 업계별

주류용

맥주와 사이다

와인·증류주

무알코올

탄산음료

유음료

수

기타 비주류

식품

화장품

의약품

기타 최종 이용 업계별

국가별

독일

이탈리아

프랑스

폴란드

영국

스페인

러시아

제7장 경쟁 구도

기업 개요

Verallia Group

BA GLASS GROUP

O-I Glass, Inc.

Vidrala, S.A.

VERESCENCE FRANCE

Gerresheimer AG

SAVERGLASS Group

ALGLASS SA

Quadpack Industries SA

Berlin Packaging

Wiegand-Glas Holding GmbH

Ardagh Group S.A.

HEINZ-GLAS GmbH & Co.

Zignago Vetro S.p.A.

Beatson Clark

제8장 보충 : 유럽의 주요 용기 유리 공장에 대한 주요 용광로 공급업체 분석

제9장 시장 향후 전망

ksm

영문 목차

영문목차

The Europe Glass Bottles And Containers Market size in terms of shipment volume is expected to grow from 40.13 million tonnes in 2025 to 44.26 million tonnes by 2030, at a CAGR of 1.98% during the forecast period (2025-2030).

The European container glass market is a crucial segment of the packaging industry. It is driven by sustainability trends, consumer demand for premium packaging, and regulations targeting plastic waste reduction. Europe boasts a well-developed glass manufacturing sector, with Germany, Italy, France, and Spain serving as central glass production and consumption hubs.

Key Highlights

The European glass container market, valued in billions of euros, has experienced steady growth in recent years. Demand across critical sectors, including food and beverages, pharmaceuticals, and cosmetics, drives this growth. The market is expected to grow moderately, with a notable increase in the premium packaging segment, particularly for alcoholic beverages, cosmetics, and gourmet food products. Alcoholic beverages, such as wine, beer, and spirits, constitute a large portion of the market, while other beverages, like juices and carbonated drinks, also contribute significantly.

Due to its recyclability, glass is a highly sustainable packaging material. Europe has implemented robust recycling policies, resulting in high glass packaging recycling rates, often surpassing 70% in numerous countries. As concerns about plastic waste grow, glass is increasingly considered an environmentally friendly alternative.

European consumers prefer glass packaging, attributing it to premium quality, product integrity preservation, and recyclability. Glass packaging is frequently associated with high-end and organic products. European Union initiatives, such as the EU Circular Economy Action Plan, drive higher recycling rates and waste reduction. Glass aligns well with these objectives as a recyclable material, further increasing its demand in the packaging sector.

The largest segment is beverages, focusing on alcoholic drinks (wine, beer, spirits) and soft drinks. Glass bottles and jars are preferred to preserve flavour and quality. Due to glass's inert nature and sterility, the pharmaceutical industry widely uses glass containers for packaging medicines, especially liquid medications, vaccines, and syrups. In cosmetics, glass is used for premium packaging of skincare products, perfumes, and cosmetics, owing to its high-end appeal and ability to provide an airtight seal.

The region also participates in the trade of container glass products. According to the International Trade Center, European countries' glass container production capacity varies significantly. Germany leads with 5,493,250 tons per year, followed by Italy at 4,897,205 tons and France at 4,580,750 tons.

The European packaging industry is experiencing a significant shift as alternatives to traditional glass packaging gain traction. Sustainability concerns, cost-effectiveness, and technological advancements in packaging materials drive this trend. As a result, established glass packaging markets face new challenges and competition from innovative alternatives like bioplastics, flexible packaging, and advanced polymer materials. This shift reshapes consumer preferences and forces glass packaging manufacturers to adapt their strategies to maintain market share in an evolving landscape.

Europe Glass Bottles And Containers Market Trends

Beverage Industry to Hold a Significant Market Share

Europe hosts several of the world's leading wine-producing nations, including France, Italy, Spain, and Germany, where glass bottles remain the dominant packaging choice for wine. Glass is widely regarded as the optimal material for maintaining wine's flavour, aroma, and quality, and it is closely associated with premium products. The wine industry continues to be a primary driver of glass container demand in Europe, with glass packaging accounting for over 80% of wine packaging in certain countries.

France remained one of the leading wine consumers among European countries, with consumption reaching approximately 24.4 million hectoliters in 2023. This high level of consumption reflects France's deep-rooted wine culture and its significance in daily life and social gatherings. According to the International Organisation of Vine and Wine, the United Kingdom consumed about 12.8 million hectoliters. The UK's wine consumption has been steadily growing, influenced by changing consumer preferences and an increasing appreciation for wine.

This trend in wine consumption across Europe indicates continued demand for glass bottles as packaging materials. Glass bottles remain the preferred packaging option for wine due to their ability to preserve flavour, extend shelf life, and provide a premium aesthetic appeal to consumers. The sustained growth in wine consumption in these critical European markets suggests a parallel increase in the demand for high-quality glass packaging solutions in the beverage industry.

The glass container beverage market shows strength in premium and niche sectors, such as craft beer, organic juices, and high-end spirits. The demand for high-quality, environmentally friendly packaging solutions drives growth in glass container usage for these categories. Craft beer and small-batch beverages contribute significantly to the market for glass packaging. Many craft brewers and small beverage producers choose glass bottles to communicate quality, tradition, and environmental responsibility to their customers.

Despite the dominance of plastic and aluminium cans, glass bottles remain in niche segments of the soft drink market, including premium sodas, organic beverages, and craft soft drinks. The increasing popularity of natural, organic, and health-focused beverage brands has contributed to using glass as a sustainable packaging option. Fresh juices, particularly cold-pressed and organic varieties, are frequently packaged in glass due to their ability to preserve product quality and taste.

Europe shows an increasing preference for environmentally friendly packaging, driven by growing consumer awareness of plastic pollution and stricter regulations on single-use plastics. Being highly recyclable and indefinitely reusable without quality loss, glass appeals to environmentally conscious consumers in beverage packaging.

This shift towards sustainable options influences manufacturers and retailers to adopt glass packaging for various products, including beverages. Glass's recyclability and reusability align with circular economy principles, further enhancing its appeal in the European market. Additionally, glass packaging's ability to preserve product quality and extend shelf life contributes to its growing popularity among consumers and producers in the region.

Germany to Hold a Significant Market Share

Germany represents a significant market for glass containers in Europe. Its robust industrial sector, high consumption of packaged goods, and increasing emphasis on sustainability support this market. The food and beverage, cosmetic, and pharmaceutical industries primarily drive the demand for glass containers in Germany.

The non-alcoholic beverage segment, especially in premium and organic categories, also embraces glass packaging for products like juices and health drinks. Germany's strong beer heritage, preference for glass in various beverage sectors, and consumer inclination towards safe, inert packaging materials collectively contribute to the robust demand for glass containers in the country's beverage industry.

According to Statistisches Bundesamt, consumer spending on alcoholic beverages in Germany has steadily increased from 2021 to 2023. In 2021, spending reached USD 29.3 billion, followed by a slight rise to USD 29.5 billion in 2022. By 2023, this figure grew to USD 30.7 billion, reflecting a consistent upward trend in the country's expenditure on alcoholic drinks over the past three years.

Germany also maintains one of the world's highest glass recycling rates, with over 90% of glass bottles being recycled. As environmental awareness grows, German consumers and companies increasingly choose glass as a sustainable packaging material. Glass is widely recognized as eco-friendly due to its 100% recyclability without quality loss. This has led to a rising preference for glass containers, particularly in light of German packaging waste laws and Extended Producer Responsibility (EPR) regulations promoting recyclable materials.

The country participates in the export of container glass products. According to the International Trade Center, Germany's export volume increased significantly from 1,094,706 tons in 2021 to 1,494,488 tons in 2022, a 36.4% rise. This increase suggests heightened international demand for German products. Factors contributing to this growth may include post-pandemic economic recovery, increased global trade, or specific industry booms in sectors like automotive, chemicals, machinery, or consumer goods.

In 2023, export volume decreased slightly to 1,205,642 tons, a 19.4% reduction from the 2022 peak. This decline may be attributed to supply chain disruptions, global economic challenges, or changing demand patterns in critical markets. Factors such as commodity price fluctuations, shifts in international demand, or geopolitical tensions, including the Ukraine conflict, could have influenced Germany's export performance in 2023.

Europe Glass Bottles And Containers Industry Overview

The European container glass market is fragmented, with numerous players competing for market share. This competitive environment fosters innovation and drives companies to differentiate their offerings to meet diverse customer needs. The market includes large multinational corporations and smaller regional manufacturers, each contributing to the industry's dynamism. Key players in this market, such as O-I Glass, Inc., SAVERGLASS Group, Berlin Packaging, Verallia Group, and Gerresheimer AG, have established strong positions through their extensive product portfolios, technological advancements, and strategic partnerships.

These companies and other market participants cater to various sectors, including food and beverage, pharmaceuticals, cosmetics, and personal care. The ongoing focus on sustainability and eco-friendly packaging solutions has also significantly influenced market strategies and product development among these key players.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Export-Import Data of Container Glass

4.3 PESTEL ANALYSIS - Container Glass Industry in Europe

4.4 Industry Standard and Regulation for Container Glass Use for Packaging

4.5 Raw Material Analysis and Material Consideration for Packaging

4.6 Sustainability Trends for Glass Packaging

4.7 Container Glass Furnace and Location in Europe

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Demand for Eco-friendly Products

5.1.2 Surging Demand from the Food and Beverage Market

5.2 Market Challenge

5.2.1 Increasing Adoption of Glass Alternatives Challenges Traditional Markets

5.3 Analysis of the Current Positioning of Europe in the Global Container Glass Market

5.4 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Europe

6 MARKET SEGMENTATION

6.1 By End-user Vertical

6.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

6.1.1.1 Beer and Cider

6.1.1.2 Wine and Spirits

6.1.2 Non-alcoholic (Qualitative Analysis For Segment Analysis)

6.1.2.1 Carbonated Soft Drinks

6.1.2.2 Dairy-based

6.1.2.3 Water

6.1.2.4 Other Non-alcoholic Beverages

6.1.3 Food

6.1.4 Cosmetics

6.1.5 Pharmaceutical

6.1.6 Other End-user Verticals

6.2 By Country

6.2.1 Germany

6.2.2 Italy

6.2.3 France

6.2.4 Poland

6.2.5 United Kingdom

6.2.6 Spain

6.2.7 Russia

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Verallia Group

7.1.2 BA GLASS GROUP

7.1.3 O-I Glass, Inc.

7.1.4 Vidrala, S.A.

7.1.5 VERESCENCE FRANCE

7.1.6 Gerresheimer AG

7.1.7 SAVERGLASS Group

7.1.8 ALGLASS SA

7.1.9 Quadpack Industries SA

7.1.10 Berlin Packaging

7.1.11 Wiegand-Glas Holding GmbH

7.1.12 Ardagh Group S.A.

7.1.13 HEINZ-GLAS GmbH & Co.

7.1.14 Zignago Vetro S.p.A.

7.1.15 Beatson Clark

8 SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO MAJOR CONTAINER GLASS PLANTS IN EUROPE