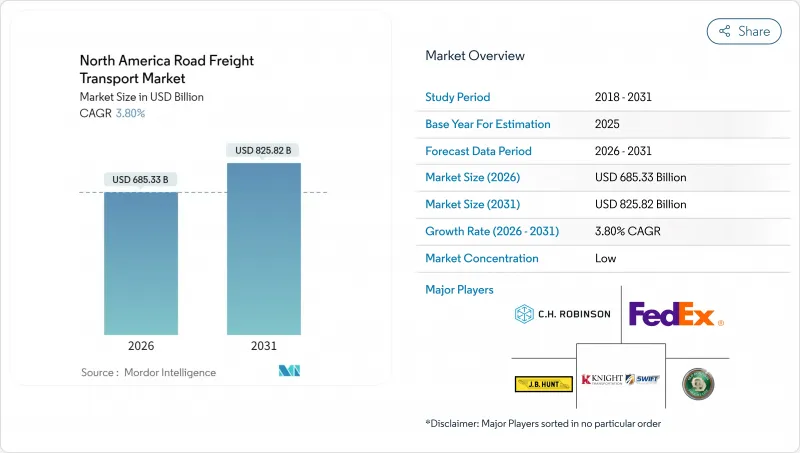

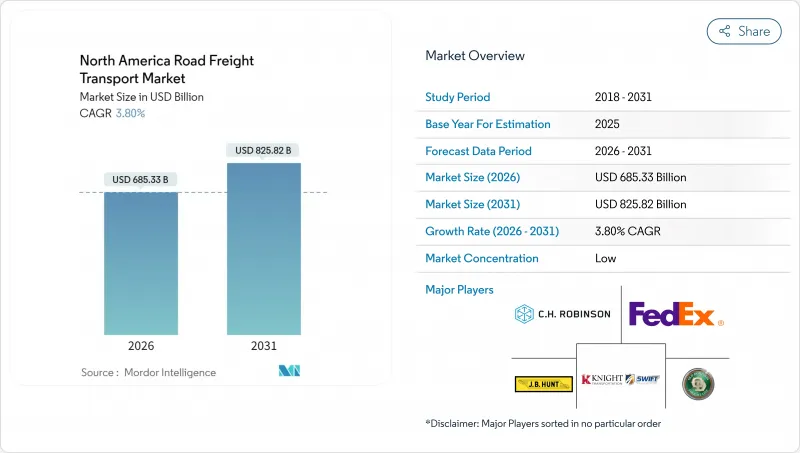

북미의 도로화물 운송 시장은 2025년에 6,602억 4,000만 달러로 평가되었고, 2026년 6,853억 3,000만 달러에서 2031년까지 8,258억 2,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 3.80%를 나타낼 전망입니다.

이러한 추세는 북미 도로 화물 운송 시장을 산업 회복력, 정책 지원 인프라 개선, 증가하는 전자상거래 물량에 힘입어 지속적인 성장 환경으로 자리매김하고 있습니다. 멕시코로의 근거리 아웃소싱, USMCA(미국-멕시코-캐나다 협정)에 따른 국경 간 무역 활성화, 재고 분산화 등이 화물 흐름을 단거리 및 고빈도 노선으로 재편하고 있습니다. 화주들은 비용 효율성을 위해 여전히 풀트럭로드(FTL) 서비스를 선호하지만, 소량화물(LTL)의 구조적 증가는 유연한 운송 능력과 화물 통합에 대한 수요 증가를 반영합니다. 규모 중심 운송업체들이 전문 업체를 인수함에 따라 경쟁 강도는 여전히 높은 수준을 유지하는 한편, 자율주행 시범 운영과 무공해 파워트레인의 광범위한 도입은 기술 주도형 생산성 도약을 예고합니다. 규제 동향?특히 온실가스 배출 제한 및 차축 중량 개정?은 소규모 운송업체가 감당하기 어려운 준수 비용을 발생시켜 통합 추세를 강화하고 있습니다.

소매업체들이 당일 배송 약속을 지키기 위해 재고를 소비자에게 더 가깝게 이동시키면서 100마일 미만의 단거리 화물은 2024년까지 연평균 20% 성장했습니다. 대도시의 밀집된 수요는 터미널 수용 능력을 압박하고 도시 제한을 극복할 수 있는 운전자 확보 경쟁을 심화시킵니다. 식료품 및 의약품 전자상거래 채널은 온도 조절 화물 투자를 촉진하여 운송업체들이 냉장 차량을 확대하도록 유도합니다. 경로 최적화 알고리즘은 거리보다 정차 밀도에 초점을 맞춰 도시 전문성을 가진 지역 전문업체에 유리합니다. 배송 시간대 및 무공해 구역에 관한 지역 조례는 최종 배송 구간용 배터리 전기 밴의 조기 도입을 가속화합니다.

인프라 투자 및 고용법은 고속도로 및 교량에 1,100억 달러를 충당해, 차선 증설이나 병목 해소에 의한 운송 시간 단축과 트럭 생산성 향상을 실현합니다. 미네소타에서는 1마일 당 1일 4시간 이상의 트럭 지연을 일으키는 22개의 화물 병목을 특정. 일리노이 주, 텍사스 주, 캘리포니아 주에도 비슷한 문제가 있습니다. 2025년부터 2028년까지의 프로젝트 완료로 I-35, I-95 등 주요 간선 도로의 용량이 확대됩니다. 단, 공사에 의한 우회에 의해 일시적으로 운송량이 억제될 가능성이 있습니다. 포장 품질 향상은 유지 관리 비용을 줄이고 트레일러의 수명을 늘려 총 소유 비용을 줄입니다.

상업용 운전면허 신규 취득자보다 은퇴자가 많아 2024년 기준 약 8만 명의 운전자 부족이 예상됩니다. 운송사 설문조사에 따르면 두 자릿수 임금 인상, 유지 보너스, 근무 일정 유연성이 주요 비용 상승 요인으로 꼽혔습니다. 위험물, 대형 화물, 냉장 운송 등 특수 부문은 추가 인증 장벽으로 인해 더 심각한 인력 부족을 겪고 있습니다. 생활 방식 요인과 운행 시간 제한으로 젊은 신규 입사자가 줄어들면서, 운송사들은 대기 시간 단축을 위해 운전자 보조 기술과 드롭 트레일러 프로그램에 투자해야 합니다.

제조업은 2025년 수익의 31.68%를 차지했으며 북미의 도로화물 운송 시장에서 가장 큰 점유율을 얻었습니다. 금속, 기계 및 자동차 부품이 수출 노선의 운송량을 주도하는 반면, 수입 원재료 흐름은 안정적인 트레일러 회전을 유지합니다. 도매 및 소매업과 관련된 북미의 도로화물 운송 시장 규모는 옴니채널 재고 전략과 마이크로플루필먼트 거점의 확충에 의해 보다 빠른 확대가 전망됩니다.

도매 및 소매 업체들은 재고를 더 자주 소량으로 재주문하여 LTL(소량 화물) 운송 증가를 촉진하며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 4.33%로 성장할 것으로 전망됩니다. 건설 화물은 경기 부양 자금 지원 프로젝트로부터 상당한 상승 효과를 흡수하는 반면, 석유 및 가스 화물은 상품 사이클에 따라 변동합니다. 재생에너지 부품(터빈 블레이드, 태양광 패널, 배터리 팩)은 ‘기타’ 범주에 속하며 특수 장비와 호송 서비스가 필요합니다.

국내 운송은 2025년 매출의 62.30%를 차지했으며, 이는 광범위한 미국 내 및 캐나다 내 유통망을 반영합니다. 안정적인 지역 계약은 차량 가동률을 유지하고 통관 위험을 제한하여 경제 변동 속에서도 북미 도로 화물 운송 시장을 견고하게 지탱합니다.

FTL(완전 트럭 적재)은 2025년 매출의 79.35%를 차지하며, 화주들이 문간 배송 속도와 제한된 취급을 선호함을 보여줍니다. 계절적 수요 급증(특히 연말 성수기)은 FTL 용량을 압박하여 현물 운임 상승을 유발하고 디젤 가격 연동 계약 재협상의 기회를 창출합니다. LTL이 차지하는 북미 도로 화물 운송 시장 규모는 상대적으로 작으나, 전자상거래 반품 물량과 중소기업(SME)의 운송 수요 증가로 2026-2031년 연평균 4.18%의 더 빠른 성장률을 보일 전망입니다.

지역별 LTL 전문업체들은 크로스독 자동화 및 API 연결성에 대규모 투자를 진행하여 고객이 실시간으로 요금 비교 및 추적이 가능하도록 합니다. Knight-Swift가 2026년까지 전국적 LTL 네트워크 구축을 목표로 하는 것은 자산 집약적 트럭로드 기존 업체들이 보다 균형 잡힌 수익 구조로 다각화하는 방식을 보여줍니다.

The North America road freight transport market was valued at USD 660.24 billion in 2025 and estimated to grow from USD 685.33 billion in 2026 to reach USD 825.82 billion by 2031, at a CAGR of 3.80% during the forecast period (2026-2031).

This trajectory positions the North America road freight transport market as a steady growth environment sustained by industrial resilience, policy-backed infrastructure upgrades, and rising e-commerce volumes. Nearshoring to Mexico, USMCA-enabled cross-border trade, and inventory decentralization are reshaping freight flows toward shorter-haul, higher-frequency lanes. Shippers continue to favor Full-Truck-Load (FTL) services for cost efficiency, yet the structural rise of Less-than-Truck-Load (LTL) reflects mounting demand for flexible capacity and shipment consolidation. Competitive intensity remains elevated as scale-oriented carriers acquire specialized providers, while widespread adoption of autonomous driving pilots and zero-emission powertrains signals a technology-driven productivity leap. Regulatory trends-most notably greenhouse-gas limits and axle-weight revisions-create compliance costs that smaller fleets struggle to absorb, reinforcing consolidation momentum.

Short-haul freight under 100 miles grew 20% annually through 2024 as retailers moved stock closer to consumers to meet same-day delivery promises. Dense metropolitan demand strains terminal capacity and intensifies competition for drivers who can navigate urban restrictions. Grocery and pharmaceutical e-commerce channels push temperature-controlled freight investment, prompting carriers to expand refrigerated fleets. Route-optimization algorithms focus on stop density rather than distance, advantaging regional specialists with urban expertise. Local ordinances on delivery time windows and zero-emission zones accelerate early adoption of battery-electric vans for final-mile routes.

The Infrastructure Investment and Jobs Act earmarks USD 110 billion for highways and bridges, unlocking lane additions and bottleneck removals that lower transit times and boost truck productivity. Minnesota identified 22 freight chokepoints causing over 4 hours of daily truck delay per mile; similar pain points exist in Illinois, Texas, and California. Project completions scheduled between 2025-2028 will expand capacity on key corridors such as I-35 and I-95, although construction detours may temporarily suppress throughput. Better pavement quality reduces maintenance expenses, extending tractor-trailer life cycles and lowering the total cost of ownership.

Retirements outpace new Commercial Driver's License entrants, leaving fleets short by an estimated 80,000 drivers in 2024. Carrier surveys cite double-digit pay increases, retention bonuses, and schedule flexibility as key cost escalators. Specialized segments-hazmat, oversized, and refrigerated-face steeper shortages due to extra certification hurdles. Lifestyle factors and hours-of-service limits deter younger recruits, compelling fleets to invest in driver-assist technology and drop-trailer programs to reduce waiting times.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing generated 31.68% of 2025 revenue, the highest slice of the North America road freight transport market share. Metals, machinery, and automotive parts dominate outbound lane volume, while inbound raw-material flows maintain steady trailer turns. The North America road freight transport market size tied to wholesale and retail trade is poised for faster expansion, aided by omnichannel inventory strategies and micro-fulfillment buildouts.

Wholesale and retail traders reorder stock more frequently and in smaller quantities, fueling LTL shipment growth, and are projected to grow at a CAGR of 4.33% between 2026-2031. Construction freight absorbs a meaningful uplift from stimulus-funded projects, whereas oil-and-gas cargoes fluctuate with commodity cycles. Renewable-energy components-turbine blades, solar panels, and battery packs-enter the "Others" bucket and demand specialized equipment and escorts.

Domestic hauls represented 62.30% of 2025 turnover, reflecting extensive intra-U.S. and intra-Canada distribution networks. Stable regional contracts anchor fleet utilization and limit customs risk, keeping the North America road freight transport market robust during economic swings.

International volumes, while smaller, eye a 4.38% CAGR between 2026-2031. Lower border dwell times and harmonized documentation under USMCA attract shippers seeking one-bill cross-border solutions. Large carriers embed bilingual customer service and bonded warehousing to capitalize on the upswing.

FTL held 79.35% of 2025 sales, underscoring shippers' preference for door-to-door speed and limited handling. Seasonality spikes, notably retail holiday peaks, tighten FTL capacity, pushing spot rates upward and opening openings for contract renegotiations tethered to diesel indexation. The North America road freight transport market size captured by LTL is smaller but should grow faster with a CAGR of 4.18% between 2026-2031 on the back of e-commerce returns and SME shipping needs.

Regional LTL specialists invest heavily in cross-dock automation and API connectivity so customers can rate-shop and track in real time. Knight-Swift's ambition to build a national LTL grid by 2026 illustrates how asset-heavy truckload incumbents diversify toward more balanced revenue streams.

The North America Road Freight Transport Market Report is Segmented by End User Industry (Manufacturing, and More), Destination (Domestic and International), Truckload Specification (FTL and LTL), Distance (Long and Short Haul), Goods Configuration (Fluid Goods and Solid Goods), Temperature Control (Non-Temperature and Temperature Controlled), Containerization, and Country. The Market Forecasts are Provided in Terms of Value (USD).