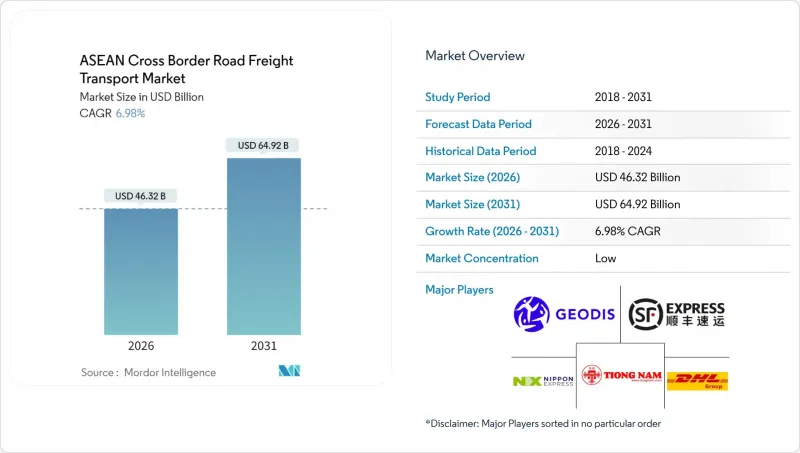

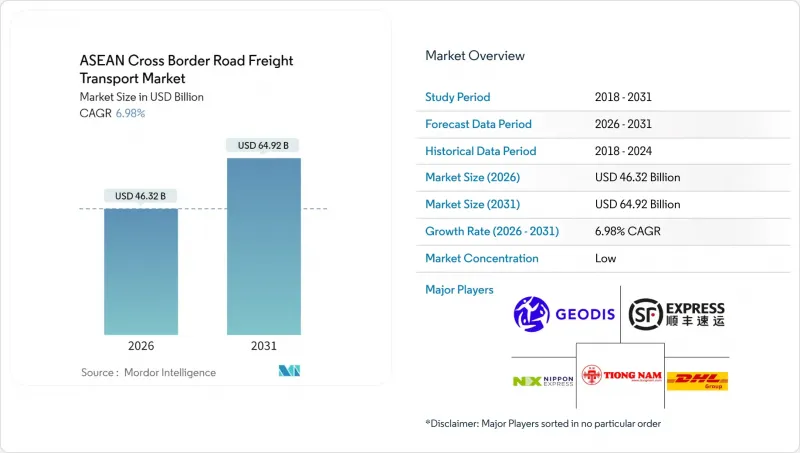

2026년 ASEAN의 국경 간 도로 화물 운송 시장 규모는 463억 2,000만 달러로 추정되며, 2025년 433억 달러에서 성장이 전망됩니다.

2031년까지 649억 2,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 6.98%로 확대될 것으로 전망됩니다.

아세안 역내 무역은 2030년까지 8,000억 달러 규모로 확대될 것으로 예상되며, 예측 가능한 트럭 운송 능력에 대한 관심이 높아지고 있습니다. 한편, 아세안 단일창구 도입으로 국경통관 평균 소요일수가 4일 단축되어 착륙비용 절감 및 서비스 신뢰도 향상을 실현하고 있습니다. 아세안 세관운송시스템(ACTS)의 API 인프라를 활용한 디지털 화물 플랫폼은 공회전율을 줄이고 실시간 화물 가시성을 원하는 다국적 화주들의 관심을 받고 있습니다. 한편, 캄보디아, 라오스, 미얀마, 베트남(CLMV)에 대한 제조업의 외국인직접투자(FDI) 재분배가 새로운 부품 운송 통로를 구축하고, 인도네시아의 니켈 가공 다운스트림 부문의 급격한 성장은 안정적인 위험물 운송량을 창출하여 인증된 운송업체에 이익을 가져다주었습니다. 지속적인 운전자 부족, 새로운 연료 가격 제도, 쿤밍-비엔티안 노선의 철도 경쟁은 여전히 주요 역풍 요인으로 작용하고 있습니다.

소량화물의 급격한 증가로 인해 시장은 기존의 풀트럭 운송 모델에 도전이 되는 소량, 고빈도 운송으로 전환되고 있습니다. 한편, 긴급성을 요하는 국경 간 운송 노선에서는 프리미엄 가격 책정이 가능합니다. J& T익스프레스는 2025년 2분기 동남아시아에서 16억 9,000만 개의 소량화물을 취급하여 전년 동기 대비 65.9% 증가. 현재 5,400대의 장거리 운송 차량이 매일 여러 국경을 넘나들고 있습니다. 마켓플레이스에서는 익일 배송 보장 및 API 지원 배송 상태 업데이트에 대한 요구가 점점 더 높아지고 있으며, 이로 인해 운송 업체들은 텔레매틱스 및 동적 경로 설정 도구의 도입을 촉진하고 있습니다. 이러한 디지털 통합은 국경 간 특송 서비스의 성장을 지원하고, 운송 시간을 단축하여 플랫폼 경제의 표준을 채택한 운송 회사의 경쟁 우위를 높이고 있습니다.

아세안 세관통관시스템(ACTS)은 컴플라이언스 처리의 구조적 변화를 가져오고, 단일 전자보증제도를 통해 다자간 통관을 간소화하고 서류작업을 크게 줄일 수 있습니다. 싱가포르-말레이시아-태국을 잇는 선행 도입 회랑에서는 체류 시간이 24시간에서 6시간 미만으로 단축되어 트레일러 회전율 향상과 자산 수익률 개선을 실현하고 있습니다. 싱가포르가 2025년에 시행하는 차량 허가 절차 업그레이드는 도로 운송 서류를 ACTS 데이터 필드와 일치시켜 원활한 운송을 지원합니다. AEO(Authorized Economic Operator) 우선 차선은 규정 준수 운송업체를 우대하는 계층적 프레임워크를 더욱 명확히 하고, 비정규 트럭 운전자의 진입 장벽을 높임과 동시에 화주들이 검증된 차량으로 전환하도록 유도합니다.

지역 간 임금 격차와 인구통계학적 변화로 인해 자격을 갖춘 운전자의 공급이 부족합니다. 일본에서는 특정기능비자제도를 통한 베트남인, 인도네시아인 오퍼레이터의 수용이 자국의 부족을 보충하는 한편, 현지 공급원을 더욱 고갈시키고 있습니다. 노후화된 차량은 다운타임이 증가하고, 2024년 말레이시아의 디젤 보조금 폐지 이후 연료 가격 변동에 따라 사업자들은 재투자를 주저하고 있습니다. 위험물 운송 및 온도 관리 운송에 대한 인증 요건은 부족을 악화시키고 이러한 틈새 분야에서 운전자의 프리미엄을 높이고 있습니다. 태국에서 유로6 트럭에 대한 세금 환급을 포함한 차량 업데이트 프로그램은 그 타격을 부분적으로 완화하지만, 임박한 노동력 불일치를 완전히 상쇄할 수는 없습니다.

2025년 아세안 역내 국경간 도로 화물 운송 시장에서 제조업이 33.78%를 차지하였습니다. 이는 전자제품, 자동차, 의류 부품의 적시 공급망이 정착되고 있음을 반영합니다. 부품 운송이 집중되는 중국-베트남, 베트남 - 태국 등의 회랑에서는 일일 루프 운행이 트레일러 가동률의 높은 수준을 유지하여 대형 3PL 기업의 대용량 구매를 지속하고 있습니다. 중국 플러스 원의 투자 유입으로 베트남과 캄보디아는 조립 거점으로서의 입지를 굳히고 있으며, 최종 조립라인을 위한 국경 간 셔틀 운행 수요를 높이고 있습니다. 도소매업은 기반 규모는 작지만, 2026년부터 2031년까지 8.08%의 CAGR로 다른 업종을 능가하는 성장이 예상됩니다. 이는 엄격한 납기와 잦은 배송이 필요한 B2C 소량화물의 급증에 따른 것입니다. 이 두 가지 경향은 화물 구성을 복잡하게 만들고, 운송 사업자는 드라이밴에서 온도 관리 장치까지 설비를 다양화하여 여러 분야에서 수익을 확보해야 합니다.

석유 및 가스, 광업, 채석업 클러스터는 인도네시아의 니켈 가공 붐으로 인한 구조적 상승 효과를 누리고 있습니다. 이로 인해 위험물 대응을 위한 특수 장비가 장착된 트럭이 필요하게 되었습니다. 태국과 베트남의 수산물 콜드체인 확대는 냉동 운송 경로를 추가하고, 건설자재는 중국의 일대일로 구상과 연계된 대규모 도로 및 철도 프로젝트의 수혜를 받고 있습니다. 부문 구성의 변화는 벌크 상품 중심에서 벗어나 고부가가치, 정시성 화물이 고수익을 창출하는 균형 잡힌 포트폴리오로 전환하고 있음을 보여줍니다. 이러한 발전은 아세안 역내 국경 간 도로 화물 운송 시장의 규모 확대를 뒷받침하며, 차량 업데이트와 운전자 기술 향상이 전략적으로 필수적이라는 것을 입증합니다.

ASEAN cross border road freight transport market size in 2026 is estimated at USD 46.32 billion, growing from 2025 value of USD 43.3 billion with 2031 projections showing USD 64.92 billion, growing at 6.98% CAGR over 2026-2031.

Rising intra-ASEAN trade, valued at USD 800 billion by 2030, is sharpening the focus on predictable trucking capacity, while the ASEAN Single Window continues to trim average border clearance by four days, lowering landed costs and elevating service reliability. Digital freight platforms tapping the ASEAN Customs Transit System (ACTS) API infrastructure reduce empty-mile rates and attract multinational shippers that require real-time shipment visibility. At the same time, manufacturing FDI reallocations toward Cambodia, Laos, Myanmar, and Vietnam (CLMV) anchor fresh component corridors, while Indonesia's downstream nickel-processing boom creates steady hazardous-goods volumes that reward certified carriers. Persistent driver shortages, new fuel-pricing regimes, and rail competition from the Kunming-Vientiane route remain the principal headwinds.

Soaring parcel volumes have moved the market toward smaller, higher-frequency shipments that challenge legacy full-truckload models yet unlock premium pricing for expedited cross-border lanes. J&T Express handled 1.69 billion parcels in Southeast Asia during Q2 2025, a 65.9% year-on-year rise, relying on 5,400 long-haul vehicles that now traverse multiple borders daily. Marketplaces increasingly insist on guaranteed next-day delivery windows and API-enabled status updates, prompting fleets to install telematics and dynamic routing tools. This digital integration supports growth in cross-border express services and compresses transit windows, heightening the competitive advantage of carriers that embrace platform economy standards.

The ASEAN Customs Transit System represents a structural change in compliance processing, providing a single electronic guarantee regime that simplifies multi-country clearances and slashes paperwork. Early-adopter corridors linking Singapore, Malaysia, and Thailand report dwell-time reductions from 24 hours to under six, producing higher trailer turns and improved asset yields. Singapore's 2025 upgrade of vehicle-permit procedures aligns road-haul documentation with ACTS data fields, underpinning seamless transfers. Authorized Economic Operator (AEO) fast-track lanes further demarcate a tiered framework that rewards compliant carriers, raising barriers for informal truckers and nudging shippers toward vetted fleets.

Regional wage gaps and demographic shifts squeeze the pool of qualified drivers, with Japan recruiting Vietnamese and Indonesian operators under its specified-skills visa to plug its own shortages, further draining local supply. Older vehicles require more downtime, and operators hesitate to reinvest amid fuel-price volatility following Malaysia's 2024 diesel subsidy removal. Certification requirements for hazardous and temperature-controlled haulage exacerbate scarcities, inflating driver premiums in these niches. Fleet renewal programs, including tax rebates in Thailand for Euro 6 trucks, partially soften the blow, yet cannot fully offset the immediate labor mismatch.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing contributed 33.78% to the ASEAN cross border road freight transport market share in 2025, reflecting entrenched just-in-time supply chains for electronics, automotive, and apparel components. Component-heavy corridors-such as China to Vietnam and Vietnam to Thailand-register daily loops that underpin elevated trailer utilization rates and sustain high-capacity purchases among large 3PLs. The influx of China-plus-one investment cements Vietnam and Cambodia as assembly hubs, inflating demand for cross-border shuttle runs feeding final-assembly lines. Wholesale and retail trade, although accounting for a smaller base, will outrun every other sector at an 8.08% CAGR between 2026-2031, propelled by surging B2C parcel flows that call for tight delivery windows and frequent dispatches. These twin patterns build a more complex freight mix that forces carriers to diversify equipment-from dry vans to temperature-controlled units-ensuring they capture value across multiple verticals.

The oil and gas, mining, and quarrying cluster receives a structural uplift from Indonesia's nickel-processing boom, which necessitates specialized truck fleets outfitted for hazardous materials. Cold-chain build-outs for fisheries in Thailand and Vietnam add reefer lanes, while construction materials benefit from large-scale road and rail projects entwined with China's Belt and Road initiatives. The sector mix signals a shift away from dominance by bulk commodities toward a balanced portfolio where high-value, time-critical loads command premium yields. This evolution underpins the ASEAN cross border road freight transport market size expansion trajectory, reinforcing the strategic imperative for fleet renewal and driver up-skilling.

The ASEAN Cross Border Road Freight Transport Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Manufacturing, Construction, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Country (Indonesia, Malaysia, Thailand, Vietnam, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).