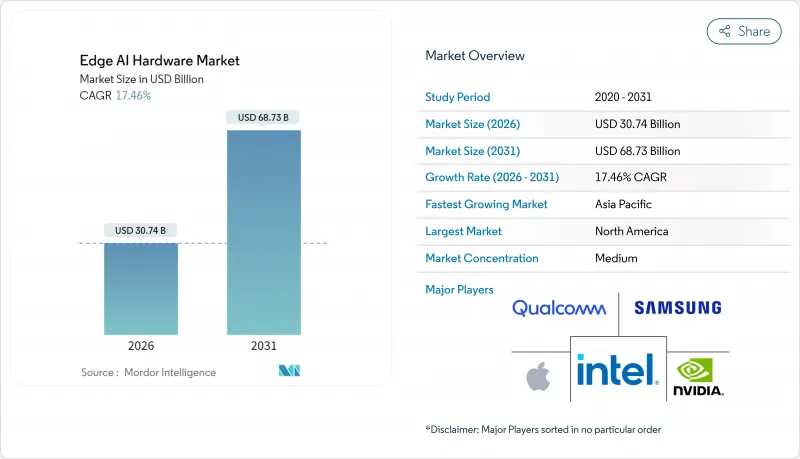

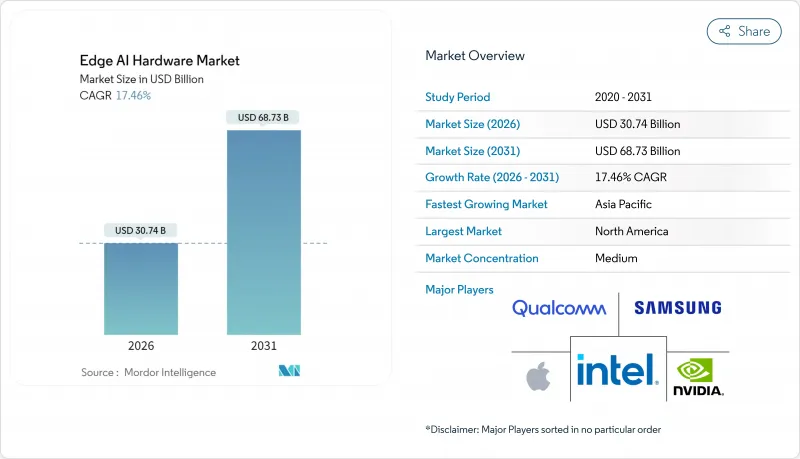

세계의 엣지 AI 하드웨어 시장은 2025년에 261억 7,000만 달러로 평가되었으며, 2026년 307억 4,000만 달러에서 2031년까지 687억 3,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 17.46%로 전망됩니다.

이 성장의 기세는 지연을 줄이고 데이터의 주권을 보호하며 에너지 소비를 줄이는 온 디바이스 추론에 대한 수요 증가로 인한 것입니다. 프리미엄급 스마트폰, AI 대응 퍼스널 컴퓨터, 필수 자동차 안전 시스템이 단기적인 성장을 지원하고 있습니다. CHIPS and Science Act(칩스 앤 과학법) 등 정부의 장려책은 국내 생산 능력을 촉진하고, 5G를 활용한 멀티 액세스 엣지 컴퓨팅(MEC)은 대응 가능한 워크로드를 확대하고 있습니다. 경쟁의 심각성은 중간 정도이며 다양한 반도체 대기업이 와트 당 성능을 최적화하는 특정 용도용 칩 공급업체에 대한 점유율을 지키고 있습니다. 첨단 파운드리에서 공급망의 집중화와 수출 규제의 확대는 지역적 복잡성을 증가시키는 한편, 자국에서의 대체 기술 개발을 촉진하고 있습니다.

최신 노트북 칩에 탑재된 전용 뉴럴 프로세싱 유닛(NPU)은 로컬 AI 처리량으로 40-50 TOPS를 달성하여 대규모 언어 모델과 생성 워크로드를 오프라인으로 즉각 응답 시간으로 실행 가능하게 합니다. Microsoft Copilot PC의 새로운 설계 기준은 모든 OEM 제조업체에게 유사한 가속 통합을 촉구하여 범용 코어가 아닌 이기종 컴퓨팅에 대한 로드맵을 이끌고 있습니다. 2030년까지 반도체 로드맵은 추론 최적화 타일을 선호하며 에지 중심 노드에 대한 지속적인 수요를 이끌어 왔습니다.

플래그쉽 모바일 프로세서는 45-50 TOPS의 추론 성능을 실현하고 AI 작업을 전용 엔진에 할당하여 배터리 수명을 연장합니다. 디바이스 내 번역, 이미지 생성, 개인 개인 어시스턴트 기능은 프리미엄 레이어 전반에 걸쳐 명확한 업그레이드 동기를 창출하여 구매 사이클을 단축합니다. 미드레인지 설계는 전년의 플래그십 기능을 계승해, 전용 AI 실리콘의 대량 출하를 확대합니다.

3nm 디바이스의 개발에는 마스크 비용으로 1억 달러 이상, 웨이퍼 1장당 2만 달러 이상의 비용이 들고, 신규 참가자의 진입을 제한하고 있습니다. 소규모 기업이 규모 확대나 틈새 분야에서의 차별화를 도모하는 가운데 업계 재편이 가속하고 있습니다. 노드 최적화 설계와 칩렛 분할은 비용을 부분적으로 상쇄하지만 기존 공급 계약을 가진 기존 기업의 이점을 더욱 강화합니다.

GPU 디바이스는 성숙한 소프트웨어 스택과 높은 병렬 처리량으로 2025년 에지 AI 하드웨어 시장 점유율의 50.12%를 차지했습니다. 예측 기간 동안 설계자가 와트당 성능을 강조함에 따라 ASIC과 NPU는 18.74%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 자동차 및 산업 분야의 구매자가 결정론적 대기 시간과 기능 안전을 우선시하기 때문에 ASIC용 에지 AI 하드웨어 시장 규모는 급격히 확대될 것으로 예측됩니다. CPU는 범용 리소스가 필요한 혼합 워크로드에서 가치를 유지하고 FPGA는 통신 및 방위 분야에서 재구성 가능한 역할로 계속 성장하고 있습니다.

칩렛 패키징은 CPU, GPU 및 NPU 타일을 공통 보드에 통합하고 각 다이를 다른 작업에 최적화하면서 메모리 인터페이스를 공유합니다. 벤더 각사는 실리콘층에서 보안 엔클레이브와 기능 안전 모니터를 통합하여 의료 및 자동차 분야의 규제 요건을 충족합니다. 다중 파운드리 전략은 지정학적 위험을 완화하지만, 고급 노드에 대한 의존성은 주요 팹과의 협상력을 유지합니다.

2025년 시점의 엣지 AI 하드웨어 시장 규모에서 스마트폰은 연간 갱신 사이클과 대량 생산을 배경으로 39.25%를 차지했습니다. 그러나 자율 항행이나 시각 해석이 저지연 추론을 필요로 하는 로봇 및 드론 분야가 가장 급속히 성장해 19.32%의 연평균 복합 성장률(CAGR)로 확대하고 있습니다. 전용 에지 보드는 시각 프로세서와 깊이 센서를 결합하여 밀리초 단위의 장애물 회피를 실현합니다.

카메라는 엣지 AI를 통합하여 인클로저 내에서 실시간 감지를 수행합니다. 이를 통해 소매 분석 및 스마트 시티의 영상 백홀 비용을 줄일 수 있습니다. 웨어러블 장비는 초저전력 신경 엔진을 채택하여 제한된 배터리 예산 하에서도 지속적으로 건강 데이터를 추출합니다. 스마트 스피커는 음성 캡처, 빔포밍, NLP 추론을 단일 칩으로 집약해, 부품 수를 줄이고 음성을 로컬로 유지하여 개인 정보를 강화합니다.

북미는 2025년 520억 달러의 CHIPS 인센티브와 자동차, 소매 및 의료 분야에서 기업 파일럿 사업의 선행 전개를 배경으로 38.92%의 수익 점유율을 차지했습니다. 스타트업 기업은 벤처 캐피탈의 집적을 활용해, 특정 분야용 가속기의 상용화를 추진하고 있습니다. 수출관리 정책에 따라 해외 판매는 제약되는 한편, 국내의 방위 및 항공우주 수요는 확보되고 있습니다.

아시아태평양은 19.27%의 연평균 복합 성장률(CAGR)로 성장하여 다른 지역을 능가하고 있습니다. 중국은 수입 규제 회피를 위해 국산 GPU 및 NPU 벤처를 지원하고, 한국은 국가 AI 칩라인에 70억 달러를 투입했습니다. 일본의 Society 5.0 구상은 결정론적 엣지 컴퓨팅이 필요한 스마트 공장 개조를 촉진하고 있습니다.

유럽은 430억 유로의 'CHIPS 법'에 따라 주권 확보 목표와 예산 현실의 균형을 맞추고 있습니다. 독일과 프랑스의 자동차산업 거점에서는 기능안전 대응의 엣지 추론을 우선하고 GDPR(EU 개인정보보호규정) 준거가 On-Premise 분석을 촉진하고 있습니다. 이스라엘의 활기찬 스타트업 에코시스템은 방위 및 의료 영상 분야의 이용 사례를 타겟으로 하여 EMEA 전역에 보드를 수출하고 있습니다.

라틴아메리카에서는 농업용 드론이나 스마트 시티 감시 시스템에 조기 도입이 진행되고 있습니다. 중동에서는 물류 및 에너지 인프라를 위한 AI를 호스팅하기 위해 에지 게이트웨이를 결합한 주권 데이터센터에 대한 투자가 가속화되고 있습니다. 아프리카는 개발 도상 지역이지만 위성 백홀과 연계한 모바일 퍼스트 전개에 의해 기존의 기술 기반을 뛰어넘는 진화를 이루고 있습니다.

The Edge AI hardware market was valued at USD 26.17 billion in 2025 and estimated to grow from USD 30.74 billion in 2026 to reach USD 68.73 billion by 2031, at a CAGR of 17.46% during the forecast period (2026-2031).

Momentum stems from rising demand for on-device inference that cuts latency, safeguards data sovereignty, and lowers energy consumption. Premium-tier smartphones, AI-enabled personal computers, and mandatory automotive safety systems anchor near-term growth. Government incentives such as the CHIPS and Science Act encourage domestic production capacity, while 5G-powered multi-access edge computing (MEC) broadens the addressable workload. Competitive intensity is moderate as diversified semiconductor leaders defend share against application-specific chip suppliers that optimize performance per watt. Supply-chain concentration at advanced foundries and widening export controls add regional complexity but also stimulate indigenous alternatives.

Dedicated neural processing units (NPUs) in the latest laptop chips achieve 40-50 TOPS of local AI throughput, allowing large language models and genera-tive workloads to run offline with instant response times. New design baselines from Microsoft Copilot+ PCs compel every OEM to integrate similar acceleration, steering roadmaps toward heterogeneous compute rather than general-purpose cores. Semiconductor roadmaps through 2030 now prioritize inference-optimized tiles, driving sustained demand for edge-centric nodes.

Flagship mobile processors deliver 45-50 TOPS inference and extend battery life by scheduling AI tasks to dedicated engines. On-device translation, generative imaging, and personal-assistant features create clear upgrade motives across premium tiers, shortening replacement intervals. Mid-range designs will inherit last year's flagship capabilities, expanding volume shipments of specialized AI silicon.

Developing a 3 nm device demands over USD 100 million in masks and USD 20,000 per wafer, constraining access for new entrants. Consolidation accelerates as smaller firms seek scale or niche differentiation. Design-for-node co-optimization and chiplet partitioning partially offset cost but reinforce the advantage for incumbents with existing supply contracts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

GPU devices captured 50.12% Edge AI hardware market share in 2025 owing to mature software stacks and high parallel throughput. Over the forecast horizon, ASICs and NPUs are projected to post a 18.74% CAGR as designers emphasize performance per watt. The Edge AI hardware market size for ASICs is expected to rise sharply as automotive and industrial buyers prioritize deterministic latency and functional safety. CPUs retain value where mixed workloads require general-purpose resources, and FPGAs grow in reconfigurable roles across telecom and defense.

Chiplet packaging combines CPU, GPU, and NPU tiles on common substrates, optimizing each die for distinct tasks while sharing memory interfaces. Vendors integrate security enclaves and functional-safety monitors at the silicon layer, satisfying regulatory mandates in healthcare and automotive deployments. Multi-foundry strategies mitigate geopolitical risk, yet advanced-node dependence keeps negotiating leverage with leading fabs.

Smartphones accounted for 39.25% of the Edge AI hardware market size in 2025, leveraging annual refresh cycles and large unit volumes. Robots and drones, however, represent the fastest trajectory, climbing at 19.32% CAGR as autonomous navigation and vision analytics demand low-latency inference. Specialized edge boards pair vision processors with depth sensors, enabling millisecond obstacle avoidance.

Cameras integrate edge AI to execute real-time detection within enclosures, reducing video backhaul costs for retail analytics and smart cities. Wearables adopt ultra-low-power neural engines that extract health insights continuously under limited battery budgets. Smart speakers consolidate voice capture, beamforming, and NLP inference on single chips, shrinking the bill of materials and enhancing privacy by keeping audio local.

The Edge AI Hardware Market Report is Segmented by Processor (CPU, GPU, and More), Device (Smartphones, Cameras and Smart Vision Sensors, and More), End-User Industry (Consumer Electronics, Automotive and Transportation, and More), Deployment Location (Device Edge, Near Edge Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 38.92% revenue in 2025 on the back of USD 52 billion CHIPS incentives and early enterprise pilots in automotive, retail, and healthcare. Start-ups leverage venture capital density to commercialize domain-specific accelerators. Export-control policy constrains outbound sales, yet secures domestic defense and aerospace demand.

Asia-Pacific is advancing at a 19.27% CAGR, outpacing all other regions. China funds native GPU and NPU ventures to circumvent import restrictions, while South Korea allocates USD 7 billion for national AI chip lines. Japan's Society 5.0 agenda stimulates smart-factory retrofits that require deterministic edge compute.

Europe balances sovereignty aims with budget realities under its EUR 43 billion Chips Act. Automotive hubs in Germany and France prioritize functional-safe edge inference, while GDPR compliance encourages on-premise analytics. Israel's vibrant start-up ecosystem targets defense and medical imaging use cases, exporting boards across EMEA.

Latin America sees early adoption in agriculture drones and smart-city surveillance. The Middle East accelerates investment in sovereign data centers coupled with edge gateways to host AI for logistics and energy infrastructure. Africa remains nascent but leapfrogs legacy stacks through mobile-first deployments allied with satellite backhaul.