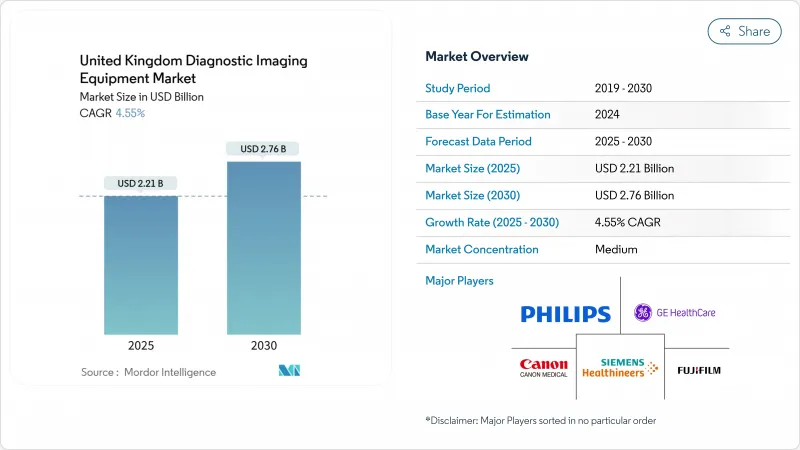

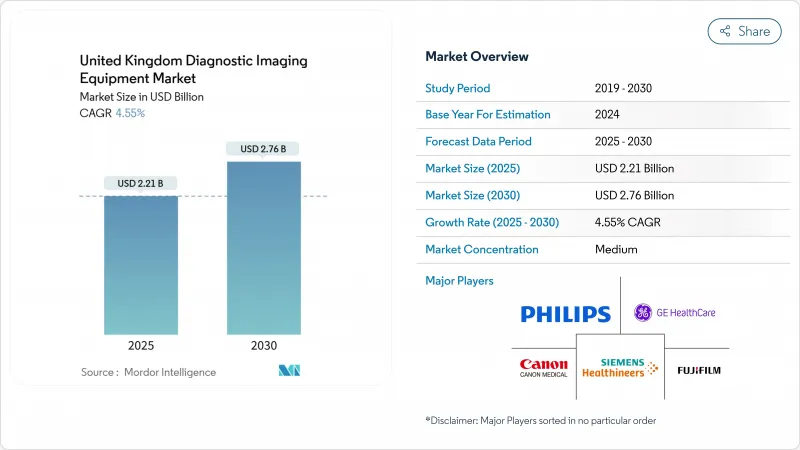

영국의 영상 진단 장비 시장 규모는 2025년에 22억 1,000만 달러로 추정되며, 예측 기간 중(2025-2030년)의 CAGR은 4.55%로, 2030년에는 27억 6,000만 달러에 달할 것으로 예상됩니다.

안정적인 성장은 NHS의 자본주입, 특히 신속한 스캐너 교환과 160개 지역 진단센터의 전개를 맡는 290억 달러의 현대화 기금에 달려 있습니다. 고령화, 만성질환의 만연, 가이드라인 주도의 검진 프로그램 등이 함께 연간 화상처리 건수는 2024년 4,500만건을 크게 웃돌아 구조적인 수요가 고정화되었습니다. 브렉지트 관련 공급망 마찰은 동시에 Siemens Hertiners의 2억 5천만 파운드 옥스포드 MRI 공장과 같은 온쇼어 제조에 박차를 가하고 수입 위험을 억제하며 차세대 연구 개발을 지원합니다. 기술 채용은 AI 대응 스캐너와 매니지드 익립먼트 서비스(MES) 계약에 기울여 초기 투자 부담을 경감하면서 갱신 사이클을 가속시킵니다. 방사선기사의 결원이 30%에 달하는 등 노동력 부족이 심각해지고 있어 직원을 증원하지 않고 처리량을 유지하는 워크플로우 자동화에 대한 관심이 높아지고 있습니다.

심혈관질환, 종양성질환, 대사성질환 증가가 멀티모달리티 진단 수요에 박차를 가하고 있으며, 2025년 예측되는 NHS 스캔 건수 4,700만 건 중 만성질환이 차지하는 비율이 급증하고 있습니다. 암 검진의 확대에 의해 진단, 병기 분류, 감시의 각 단계에 있어서 화상 진단의 강도가 증가해, 스캐너의 이용률이 한층 더 높아지고 있습니다. 당뇨병과 관련된 혈관 평가와 노인의 근골격계의 변성은 모달리티 진단량 증가에 박차를 가하고 있습니다. NICE 가이드라인은 침습적 절차보다 영상 진단을 점점 더 지지하고 CT 혈관 조영과 MRI 관절 조영에 대한 의존성을 강화하고 있습니다. 누적 효과는 환자 1인당 평생 스캔 횟수 증가이며, 모달리티를 넘어서는 내구성 있는 수익을 지원합니다.

교육병원은 AI를 활용한 CT, MRI, X선 시스템의 조달을 이끌고, 검사 시간을 단축하고, 반복 검사를 삭감함으로써, 부족한 직원의 능력을 해방합니다. NICE는 2024년에 4개의 AI 골절 검출 툴을 승인했습니다. 디지털 유방 단층촬영술가 2차원 유방촬영을 암 발견률로 웃돌아 전국적인 업그레이드 로드맵을 촉구합니다. MAGNETOM Flow와 같은 낮은 헬륨 1.5 T MRI 플랫폼은 실행 비용을 최대 30% 절감하고 예산과 지속가능성을 모두 충족합니다. Synthetic-CT 알고리즘은 이미지의 충실성을 보호하면서 방사선량을 줄이고 공급자가 IR(ME) R 2024의 기준값과 규정을 충족하는 데 도움을 줍니다.

MRI 스위트의 증축은 차폐나 에어컨의 업그레이드를 포함하면 200만 파운드를 넘습니다. 서비스 계약은 매년 구매 가격의 10%를 늘리고 운영 기간 동안 트러스트는 비용이 많이 드는 경비에 묶여 있습니다. 진료 보상의 관세는 선진적 모달리티의 실질 비용보다 늦기 때문에 임상적 이익에도 불구하고 조기 도입의 억제요인이 되고 있습니다. CT 스캐너의 57%가 5년 이상 경과되었으며 노후화로 인해 유지보수 비용과 예정되지 않은 가동 중지 시간이 증가하여 처리량과 수익이 떨어지고 있습니다. 이러한 비용 압력은 소규모 시설이 현대화 프로그램에 참여하는 속도를 지연시킵니다.

X-ray는 저소유 비용, 보편적인 임상 적응, 최소한의 설비 요건으로 인해 2024년 영국 영상 진단 장비 시장 점유율의 34.12%를 차지했습니다. 이 부문은 응급실, 외래 진료소, 지역 진단센터 등 거의 보편적인 전개를 즐깁니다. 디지털 X선 촬영장치의 업그레이드는 노후화된 CR 스위트를 대체하여 검출기의 감도를 높이고 방사선을 최대 40% 절감합니다. 이동식 DR 유닛은 침대 측에서 촬영을 가능하게 하고 감염 관리 프로토콜을 지원하며 환자의 운송 시간을 단축합니다. 그럼에도 불구하고 수평 성장이 예상되는 것은 포화 상태와 진료 보상의 상한을 반영합니다.

MRI는 가장 빠른 CAGR 5.97%를 보여 전립선 멀티파라메트릭 검사, 간철 정량화, 태아 영상 등의 이용 사례를 확대함으로써 영국의 영상 진단 장비 시장을 확대합니다. 고자계 3T 및 신흥 7T 플랫폼은 고해상도 연부 조직 조영을 필요로 하는 신경학 및 정형외과의 하위 전문성을 포착합니다. 헬륨광의 MAGNETOM Flow와 GE 헬스케어의 새로운 초고성능 1.5T 그래디언트 시스템은 운영 경비를 억제하고 대응 가능한 구매층을 넓힙니다. 하이브리드 PET-MR은 종양 연구센터에 틈새 매력이지만 산학 협력의 자금 제공의 혜택을 받고 있습니다. CT, 초음파, 핵의학 영상, 투시, 유방촬영은 계속 중요하지만, 새로운 도입보다 교체가 주인이 되어 한 자리대 중반의 성장을 기록했습니다.

2024년 영국 영상 진단 장비 시장 규모의 80.84%는 고정실이며, 높은 처리량의 CT, MRI, 인터벤셔널 실험실에 대한 병원의 근본적인 수요를 반영했습니다. 대규모 교육 병원은 공유 제어 영역과 통합 RIS/PACS를 갖춘 멀티룸 스위트에 투자하여 85% 이상의 가동률을 달성하고 있습니다. 쉴드 벙커와 갠트리의 무게 제한으로 인해 이러한 시스템은 견고하게 설치 장소에 묶여 있습니다. 보증 기간의 연장과 모듈식 업그레이드는 자산의 수명을 연장시키지만, MES 협약은 장비의 갱신 주기를 단축시킵니다.

반대로 모바일 핸드헬드 플랫폼은 CAGR 6.12%로 성장을 지속하고, 진단을 환자 가까이에 두는 분산 파도를 타고 있습니다. 지역 진단센터는 트레일러 기반의 CT 및 MRI 유닛에 의존하고, 지방을 순회함으로써 실제 점포에 비용을 들이지 않고 하루 40 스캔을 실현하고 있습니다. 버터플라이 네트워크의 1,699 파운드 핸드헬드 초음파는 기존의 5만 달러 장바구니를 스마트폰 크기의 프로브로 압축하고 21개의 트러스트로 POC(Point-of-Care)를 채용하고 있습니다. 휴대용 C 암과 미니 투시 시스템은 데이 케이스의 수술 허브를 지원하고 이미지 처리 능력을 더욱 분산시킵니다. 성장의 핵심은 NHS 디지털 인증 패스웨이를 통해 진행하는 임상의의 훈련과 진료 보상 조정입니다.

The United Kingdom Diagnostic Imaging Equipment Market size is estimated at USD 2.21 billion in 2025, and is expected to reach USD 2.76 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Stable growth rests on NHS capital injections, notably the USD 29 billion modernization fund that underwrites rapid scanner replacement and the roll-out of 160 Community Diagnostic Centres, each configured for high-throughput MRI, CT, and ultrasound workflows. An aging population, chronic disease prevalence, and guideline-driven screening programs combine to lift annual imaging volumes well above the 45 million procedures conducted in 2024, locking in structural demand. Brexit-related supply chain friction simultaneously spurs on-shore manufacturing such as Siemens Healthineers' GBP 250 million Oxford MRI plant, curbing import risk and anchoring next-generation R&D. Technology adoption tilts toward AI-enabled scanners and managed-equipment-service (MES) contracts that accelerate refresh cycles while easing up-front capital strain. Workforce shortages, with 30% radiologist vacancies, amplify interest in workflow automation that maintains throughput without proportional staff additions.

Escalating cardiovascular, oncologic, and metabolic disorders fuel multi-modality imaging demand, with chronic cases now accounting for the fastest-growing share of the 47 million NHS scans projected for 2025. Cancer screening expansions extend imaging intensity across diagnosis, staging, and surveillance stages, further tightening scanner utilization. Diabetes-related vascular assessments and musculoskeletal degeneration in an older workforce add to modality-agnostic volume growth. NICE guidelines increasingly favor imaging over invasive procedures, reinforcing reliance on CT angiography and MRI arthrography. The cumulative effect is a higher lifetime scan count per patient, anchoring durable revenue across modalities.

Teaching hospitals spearhead procurement of AI-augmented CT, MRI, and X-ray systems that compress exam times and slash repeats, thereby freeing scarce staff capacity. NICE approved four AI fracture-detection tools in 2024, signposting regulatory acceptance and accelerating hospital tender requirements for embedded analytics. Digital breast tomosynthesis outperforms 2-D mammography in cancer pick-up rates, prompting nationwide upgrade roadmaps. Low-helium 1.5 T MRI platforms, such as MAGNETOM Flow, cut running costs by up to 30%, satisfying both budgetary and sustainability mandates. Synthetic-CT algorithms reduce radiation dose while safeguarding image fidelity, helping providers meet IR(ME)R 2024 thresholds and regulations.

MRI suite build-outs exceed GBP 2 million once shielding and HVAC upgrades are counted, a figure that eclipses annual capital envelopes for many community hospitals. Service contracts add another 10% of purchase price each year, locking trusts into steep overheads for the full operational life. Reimbursement tariffs lag real costs for advanced modalities, disincentivizing early adoption despite clinical gains. Aging assets-57% of CT scanners are now older than five years-raise maintenance outlays and unplanned downtime, dampening throughput and revenue. Collectively, these cost pressures slow the pace at which smaller facilities can join modernization programs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

X-ray retained 34.12% of United Kingdom diagnostic imaging equipment market share in 2024, owing to low ownership costs, ubiquitous clinical indications, and minimal facility prerequisites. The segment enjoys near-universal deployment across emergency rooms, outpatient clinics, and community diagnostic centres. Digital radiography upgrades replace aging CR suites, boosting detector sensitivity and cutting radiation by up to 40%. Mobile DR units enable bedside imaging, supporting infection-control protocols and reducing patient transport time. Nevertheless, flat growth expectations reflect saturation and reimbursement ceilings.

MRI exhibits the fastest 5.97% CAGR, extending the United Kingdom diagnostic imaging equipment market by expanding use cases such as prostate multiparametric scans, liver iron quantification, and fetal imaging. High-field 3 T and emerging 7 T platforms capture neurology and orthopaedics subspecialties that demand high-resolution soft-tissue contrast. The helium-light MAGNETOM Flow and GE HealthCare's new ultra-premium 1.5 T gradient system limit operational expense, widening the addressable buyer base. Hybrid PET-MR holds niche appeal for oncology research centres but benefits from pooled academic-industry funding. CT, ultrasound, nuclear imaging, fluoroscopy, and mammography remain critical but record mid-single-digit growth, largely tied to replacement rather than net-new installs.

Fixed rooms delivered 80.84% of the United Kingdom diagnostic imaging equipment market size in 2024, reflecting entrenched hospital demand for high-throughput CT, MRI, and interventional labs. Large teaching hospitals invest in multi-room suites with shared control areas and integrated RIS/PACS, achieving capacity utilisation above 85%. Shielded bunkers and gantry weight constraints keep these systems firmly site-bound. Warranty extensions and modular upgrades prolong asset life, yet fleet renewal cycles shorten under MES arrangements.

Conversely, mobile and hand-held platforms record a 6.12% CAGR, riding the decentralisation wave that places diagnostics closer to patients. Community Diagnostic Centres rely on trailer-based CT and MRI units that rotate through rural catchment areas, delivering 40-scan daily capacity without bricks-and-mortar spend. Butterfly Network's GBP 1,699 handheld ultrasound compresses a traditional USD 50,000 cart into a smartphone-sized probe, unlocking point-of-care adoption across 21 trusts. Portable C-arms and mini-fluoroscopy systems support day-case surgical hubs, further dispersing imaging capacity. Growth hinges on clinician training and reimbursement alignment, both advancing via NHS digital accreditation pathways.

The United Kingdom Diagnostic Imaging Equipment Market Report is Segmented by Modality (MRI, Computed Tomography, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, Mammography), Portability (Fixed Systems, Mobile and Hand-Held Systems), Application (Cardiology, Oncology, Neurology, Orthopedics, and More), and End-User (Hospitals, Diagnostic Imaging Centres, Other End-Users). The Market Forecasts are Provided in Terms of Value (USD).