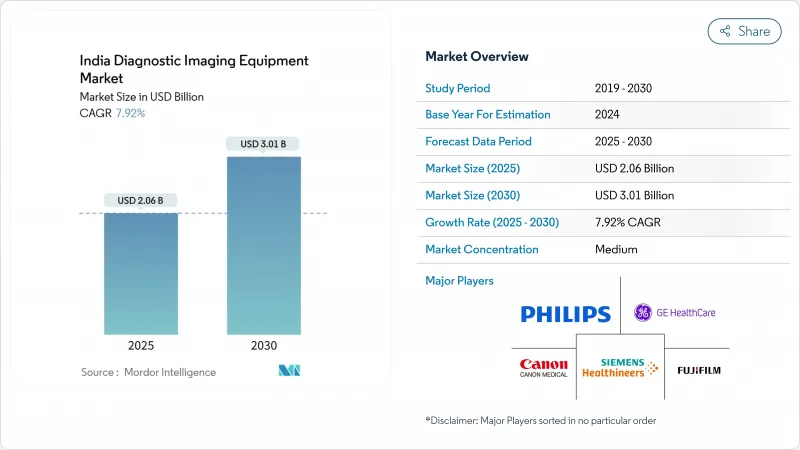

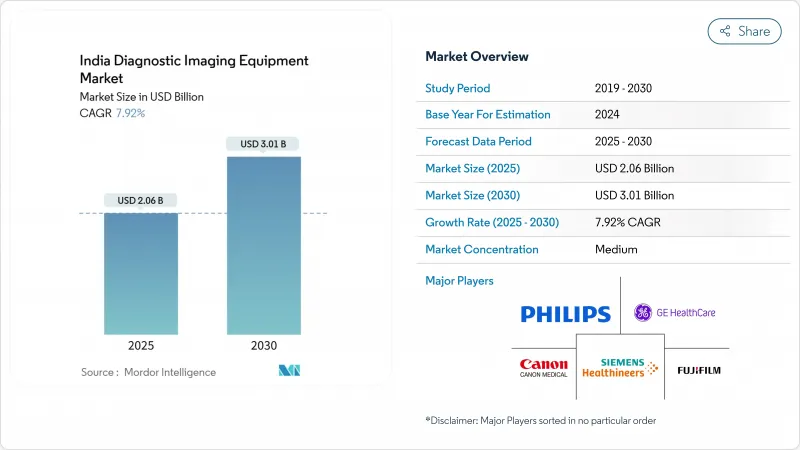

인도의 영상 진단 장비 시장 규모는 2025년에 20억 6,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 7.92%로, 2030년에는 30억 1,000만 달러에 달할 것으로 예상됩니다.

이 성장 궤도는 생산 연동형 장려금 제도 하에서 자립으로의 전환을 반영하며, 현재는 MRI 스캐너, CT 시스템 및 이전에 수입된 기타 장비를 생산하는 19개 그린필드 공장에 자금이 공급되고 있습니다. 검사 비용의 30-50% 삭감이 기대되는 인도 최초의 국산 1.5T MRI 스캐너를 비롯한 국산 기술 혁신이 고도 영상 진단 도입의 장벽을 낮추고 있습니다. 만성 질환 증가, 노인 집단의 확대, 보험 적용 가능한 진단 풀을 확대하는 국민 보험의 추진 등 역학적 변천이 수요를 뒷받침하고 있습니다. 한편, 다국적 벤더는 AI를 강화한 플랫폼과 밀폐형 헬륨 자석의 개발에 주력하는 한편, 국내 기업은 비용 우위성과 정책 인센티브를 활용해 기존 벤더에 과제하고 있습니다.

당뇨병은 인도 성인의 11.4%를 차지하고 고혈압은 35.5%를 차지하고 암 이환율은 2031년까지 인구 10만명당 549명으로 증가할 것으로 예측됩니다. 이 수치는 조기 병변의 검출과 치료 반응을 모니터링할 수 있는 CT 혈관 조영, 다상 MRI, PET-CT 워크플로우에 대한 지속적인 요구를 이끌어 냅니다. 의료기관은 단일 양식실에서 종양학적 및 심장 대사학적 경로를 간소화하는 통합 스위트룸으로 전환하고 있으며, 하이 슬라이스 CT 및 3T MRI에 대한 설비 투자를 가속화하고 있습니다. 60세 이상의 여성은 비전염성 질환의 유병률이 높고, 스캐너의 처리량 계획이나 코일 재고에 영향을 미치기 때문에 성별에 특화된 영상 진단 프로토콜이 출현하고 있습니다. 따라서 만성 질환의 급증은 인도의 영상 진단 장비 시장 전체의 조달 결정에도 영향을 미칩니다.

60세 이상의 인도인 수는 꾸준히 증가하고 있으며 평균 수명은 남부와 서부 주에 집중되어 있습니다. 노화와 관련된 근골격계의 변성, 신경퇴행성 질환, 심혈관 리모델링은 낮은 복용량과 편안함을 위해 최적화된 영상 진단 시스템을 필요로 합니다. 병원은 장시간의 치료를 견딜 수 없는 허약한 환자에 대응하기 위해 이중 에너지 X선 흡수 측정, 저대비 심장 CT, 침묵 MRI 시퀀싱를 추가하고 있습니다. 따라서 벤더는 와이드 보어, 노이즈 저감 소프트웨어, 자동 포지셔닝 등 환자 중심의 인체 공학을 중시하고 있습니다.

MRI와 CT 스캐너는 중규모 병원의 설비 예산의 20-25%를 소비하기 때문에 설비 투자액은 여전히 큰 장애물이 되고 있습니다. 소규모 시설은 1억 8,000만 달러의 중고기 유통 시장에 의존하고 있으며, 이는 현재 의료기기 거래 전체의 10%에 해당합니다. 이해관계자는 세액을 인하하면 도입이 확대될 것으로 X선·진단 키트의 GST 인하를 요구하는 로비 활동을 계속하고 있습니다. 수입품보다 30-50% 싼 가격의 국산 MRI 프로토타입은 구제를 약속하지만, 스케일업은 임상 성능 검증과 애프터세일즈 네트워크에 달려 있으며, 인도의 영상 진단 장비 시장에서의 보급을 아직 억제하는 요인이 되고 있습니다.

2024년 인도의 영상 진단 장비 시장에서는 응급 의료나 1차 케어로의 보급에 의해 X선 시스템이 29.23%의 점유율을 유지했습니다. 그러나 컴퓨터 단층 촬영은 심장 칼슘 스코어링, 외상 영상 진단 및 종양 병기 진단 프로토콜이 2차 및 3차 센터에서 보급됨에 따라 CAGR이 가장 빠른 8.97%를 나타낼 것으로 예측됩니다. 검출기의 저가격화와 이미지의 선명화로 디지털 X선 촬영장치의 업그레이드가 급속히 진행되어 아날로그 시스템을 대체하고 있습니다. AIIMS 델리에서 임상 검증이 예정된 국내 1.5T 프로토타입에 힘입어 고자장 MRI의 설치도 증가하고 있어 스캔요금을 30% 이상 삭감할 수 있어 동 부문 내 인도의 영상 진단 장비 시장 규모를 확대합니다.

CT 벤더는 스펙트럼 영상, 금속 아티팩트 저감, 원격 서비스 진단의 번들화를 추진하고 있어, 다운타임의 단축과 검사 단가의 경제성 향상을 도모하고 있습니다. 핵의학 검사는 3차 암 거점에 한정된 틈새 영역에 머물고 있지만, PET-CT 수요는 정밀 종양학의 견인역으로 증가하고 있습니다. 초음파 검사는 산과, 소화기과, 응급검사에서는 여전히 선택되는 모달리티이지만, 원외진료에서는 핸드헬드 프로브가 대두해 왔습니다. 전반적으로, 모더리티 믹스의 변화는 인도의 영상 진단 장비 시장 전체에서 기술의 고도화와 합리적인 가격이 어떻게 자본 예산을 결정하고 있는지를 돋보이게합니다.

2024년 인도의 영상 진단 장비 시장 규모에서 차지하는 고정 설비의 비율은 82.41%로, 수십 년간의 인프라가 입원 환자의 영상 진단과 외상 치료를 향하고 있음을 반영했습니다. 그러나 모바일 및 핸드헬드 기기는 CAGR 8.12%를 나타낼 전망이며, 이는 농촌지구나 기업의 웰니스 캠프에 서비스를 제공하는 정부의 밴이 뒷받침하고 있습니다. 핸드헬드 초음파 검사는 소아 폐렴에 대해 99.11%의 감도를 나타내며, 흉부 엑스레이를 초과하여 휴대용 진단의 임상적 유용성을 입증합니다. 카트형 초음파 진단 장치와 모바일 DR 장치에는 핫스팟 연결 기능이 탑재되어 이미지를 클라우드 PACS로 전송하여 즉시 읽을 수 있습니다.

배터리 밀도, 무선 데이터 전송, 견고한 케이스 등의 진보로 재해 지역이나 스포츠 의학에의 전개가 넓어지고 있습니다. 세계 기금을 통한 휴대용 엑스레이 솔루션의 승인은 이 범주의 정당성을 더욱 향상시키고 있습니다. 시간이 지남에 따라 모바일 스캐너를 사용하면 과도한 부담을 겪고있는 3 차 의료 센터에서 영상 진단의 부하를 줄이고 인도의 영상 진단 장비 시장을 새로운 지역으로 확장하고 자산의 ROI를 개선합니다.

The India Diagnostic Imaging Equipment Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 3.01 billion by 2030, at a CAGR of 7.92% during the forecast period (2025-2030).

This growth trajectory reflects the country's shift toward self-reliance under the Production Linked Incentive scheme, which has funded 19 greenfield plants that now manufacture MRI scanners, CT systems, and other devices previously imported. Indigenous innovation, including India's first home-grown 1.5 T MRI scanner expected to cut examination costs by 30-50%, is lowering barriers to advanced imaging adoption. Demand is reinforced by an epidemiological transition marked by rising chronic disease prevalence, an expanding elderly cohort, and a national insurance push that is enlarging the reimbursable diagnostic pool. Meanwhile, multinational vendors are doubling down on AI-enhanced platforms and sealed-helium magnets, while domestic firms leverage cost advantages and policy incentives to challenge incumbents.

Diabetes now affects 11.4% of Indian adults, while hypertension touches 35.5%, and cancer incidence is forecast to increase to 549 per 100,000 inhabitants by 2031. These numbers translate into sustained need for CT angiography, multiphase MRI, and PET-CT workflows capable of detecting early lesions and monitoring therapy response. Providers are shifting from single-modality rooms to integrated suites that streamline oncologic and cardiometabolic pathways, accelerating capital expenditure on high-slice CT and 3 T MRI. Gender-specific imaging protocols are emerging as women above 60 years show higher non-communicable disease prevalence, influencing scanner throughput planning and coil inventory. The chronic disease surge is therefore rewiring procurement decisions across the India diagnostic imaging equipment market.

The number of Indians aged 60 years and above is climbing steadily, with higher life expectancy concentrated in southern and western states. Age-related musculoskeletal degeneration, neuro-degenerative conditions, and cardiovascular remodeling demand low-dose, comfort-optimized imaging systems. Hospitals are adding dual-energy X-ray absorptiometry, low-contrast cardiac CT, and silent MRI sequences to accommodate frail patients who may not tolerate lengthy procedures. In turn, vendors emphasize patient-centric ergonomics such as wide bores, noise-reduction software, and automated positioning, hallmarks now critical to competing in the India diagnostic imaging equipment market.

Capital intensity remains a formidable hurdle as MRI and CT scanners can consume 20-25% of a mid-size hospital's equipment budget. Smaller facilities rely on a USD 180 million secondary market for pre-owned units, which now equals 10% of overall medical equipment trade. Stakeholders continue to lobby for GST cuts on X-ray and diagnostic kits, arguing that a lower tax slab would widen adoption. Indigenous MRI prototypes priced 30-50% below imports promise relief, but scale-up hinges on validated clinical performance and after-sales networks, factors that still temper diffusion in the India diagnostic imaging equipment market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

X-ray systems retained 29.23% share of the India diagnostic imaging equipment market in 2024 thanks to ubiquity in emergency and primary care. Computed tomography, however, is projected to post the fastest 8.97% CAGR as cardiac calcium scoring, trauma imaging, and oncology staging protocols proliferate in secondary and tertiary centers. Digital radiography upgrades, driven by lower detector prices and sharper images, are rapidly supplanting analog systems, while AI algorithms now automate fracture detection and tuberculosis screening. High-field MRI installations are also climbing, aided by domestic 1.5 T prototypes slated for clinical validation at AIIMS Delhi, which could shrink scan fees by over 30% and amplify the India diagnostic imaging equipment market size within the segment.

CT vendors increasingly bundle spectral imaging, metal-artifact reduction, and remote service diagnostics, reducing downtime and improving cost-per-study economics. Nuclear medicine retains a niche footprint confined to tertiary oncology hubs, yet PET-CT demand rises as precision oncology gains traction. Ultrasound remains the modality of choice for obstetrics, gastroenterology, and emergency evaluations, but handheld probes are gaining ground in out-of-hospital care. Overall, modality mix evolution underscores how technological sophistication and affordability now co-determine capital budgets across the India diagnostic imaging equipment market.

Fixed installations accounted for 82.41% of the India diagnostic imaging equipment market size in 2024, reflecting decades-old infrastructure geared to inpatient imaging and trauma care. Yet mobile and handheld devices are escalating at an 8.12% CAGR, buoyed by government vans serving rural districts and corporate wellness camps. Handheld ultrasound offers 99.11% sensitivity for pediatric pneumonia, surpassing chest X-ray and validating portable diagnostics' clinical utility. Cart-based ultrasound and mobile DR units now include hotspot connectivity, funneling images to cloud PACS for instant reads.

Advances in battery density, wireless data transfer, and rugged casings have broadened deployment in disaster zones and sports medicine. Global Fund endorsements of portable X-ray solutions further legitimize the category. Over time, utilization of mobile scanners redeploys imaging load away from overburdened tertiary centers, expanding the India diagnostic imaging equipment market into new geographies while improving asset ROI.

The India Diagnostic Imaging Equipment Market Report is Segmented by Modality (MRI, Computed Tomography, Ultrasound, X-Ray, Nuclear Imaging, Other Modalities), Portability (Fixed Systems, Mobile and Hand-Held Systems), Application (Cardiology, Oncology, and More), End User (Hospitals, Diagnostic Imaging Centers, and More), and Regional Zone (North India, and More). The Market Forecasts are Provided in Terms of Value (USD).