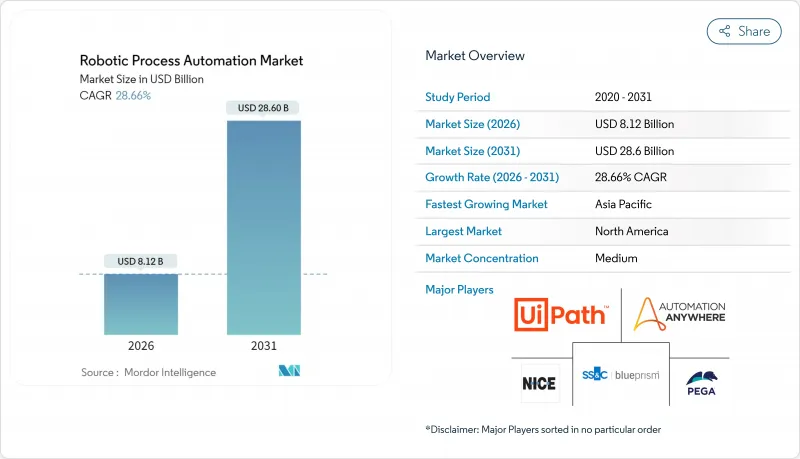

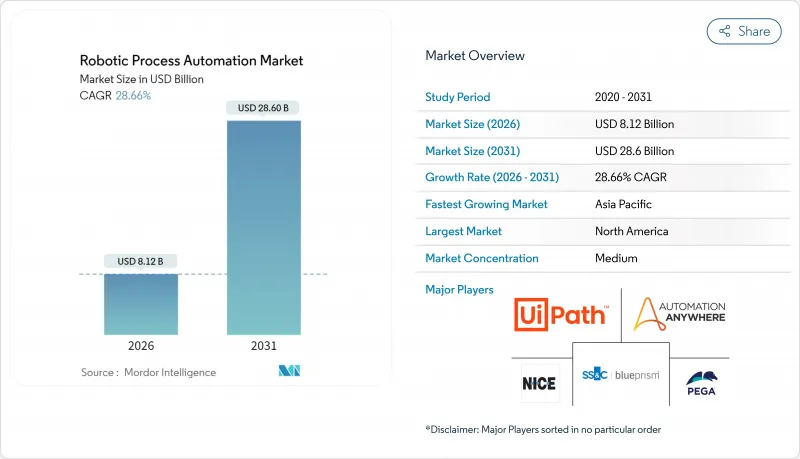

로보틱 프로세스 자동화(RPA) 시장은 2025년에 63억 1,000만 달러로 평가되었고, 2026년에는 81억 2,000만 달러에서 성장할 것으로 예상됩니다. 예측 기간(2026-2031년)에 있어서 CAGR 28.66%를 나타내, 2031년까지 28억 6,000만 달러에 달할 것으로 전망됩니다.

생성형 AI와 기존 RPA 플랫폼의 통합이 진행됨에 따라, 자동화 가능한 태스크의 범위가 넓어져, 종래는 인적 개입을 필요로 했던 비구조화 프로세스에도 기업이 대응할 수 있게 됩니다. 또한 도입주기를 단축하고 지출을 운영예산으로 이행시키는 클라우드 네이티브 배포도 시장 확대를 뒷받침하고 있습니다. 2024년 기준에서 북미는 엄격한 컴플라이언스 요건과 성숙한 기술 생태계에 힘입어 로보틱 프로세스 자동화(RPA) 시장에서 39.6%의 최대 점유율을 차지했습니다. 한편 아시아태평양은 정부에 의한 자동화 프로그램 지원과 중소기업에 의한 종량 과금형 봇의 도입으로 지역별로 가장 높은 34.5%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 벤더 간의 경쟁이 치열해지고 있으며, 인공지능에 초점을 맞춘 인수와 제휴를 통해 지능적인 문서 처리, 저 코드 설계, 자율적인 에이전트 기능을 플랫폼의 로드맵에 통합하는 움직임이 진행되고 있습니다.

소매체는 실시간 소비자 기대에 부응하기 위해 재고 조정, 출하 조정 및 반품 관리를 자동화하고 있습니다. Grupo Exito는 EC 프론트엔드와 레거시 ERP 데이터를 연계하는 전사적인 RPA 프로그램을 도입한 후 주문 처리 시간을 최대 75% 단축했습니다. 컴퓨팅 비전 모듈의 통합으로 번성기에서도 98% 이상의 정확도를 유지하고 AI 지원형 수요 예측은 공급망 변동 하에서의 이익률 관리를 지원합니다. 따라서 성숙한 전자상거래 시장과 신흥 시장 모두에서 소매업체는 자동화를 물류 혼란과 노동력 부족에 대한 필수 조치로 파악하고 있습니다.

종량 과금형 SaaS 모델은 중소기업의 진입 장벽을 낮추고 있습니다. 자나 스몰 파이낸스 은행은 On-Premise 인프라가 필요없는 UiPath 클라우드 서비스로 전환한 후 중요한 프로세스의 처리 시간을 약 70% 단축했습니다. 하이퍼스케일 제공업체가 RPA를 마켓플레이스에 통합함으로써 중소기업은 며칠 안에 안전한 봇을 도입할 수 있으며, 거래량 증가 시에만 라이선스를 확장할 수 있습니다. 애널리스트는 시민 개발자용 툴의 성숙과 업계 특화형 템플릿의 보급에 따라 2027년까지 신규 봇 도입의 40% 이상을 중소기업이 견인할 것으로 예측했습니다.

엔터프라이즈 용도 및 SaaS 용도의 빈번한 인터페이스 업데이트는 셀렉터를 비활성화하고 봇을 작동할 수 없게 하여 연간 자동화 예산의 최대 40%를 사후 대응 유지보수에 소비합니다. 터서스 디스트리뷰션사에서는 공급업체의 포맷 변경에 따라 송장 워크플로의 재설계를 강요받아 기존의 스크린 스크래핑형 봇의 취약성이 부각되었습니다. 차세대 플랫폼에서는 개체 기반 선택기와 자체 복구 기능이 추가되었지만 변경 관리 부족으로 인해 스케일 계획 지연 및 초기 단계 프로그램에 대한 신뢰 저하가 계속 발생합니다.

2025년 시점의 로보틱 프로세스 자동화(RPA) 시장에서는 규제가 엄격한 업계가 로컬 관리를 필요로 했기 때문에 On-Premise 도입이 53.62%로 여전히 주류였습니다. 그러나 클라우드 도입은 36.95%라는 최고 CAGR을 기록해 보안 인증의 확대에 따라 그 차이를 줄일 전망입니다. UiPath에 따르면 신규 계약의 80% 이상이 클라우드 구독에서 유래했으며 고객은 On-Premise 환경에 비해 50% 빠른 배포를 실현하고 있습니다. 유럽의 은행이 기밀성이 높은 결제 워크플로우를 자사 내에 유지하면서, 설계·테스트·분석에는 클라우드 테넌트를 활용하는 하이브리드 형태가 보급되고 있습니다. 이러한 유연성을 통해 기업은 거주 요건을 충족하면서 확장성을 희생하지 않고도 운영할 수 있습니다.

엣지 컴퓨팅이 성숙하면서 벤더는 로컬에서 실행하면서 클라우드에서 오케스트레이션을 받는 경량 런타임을 제공합니다. 이러한 아키텍처는 공장 현장의 봇 지연을 줄이는 동시에 서버 관리 오버헤드를 최소화합니다. 결과적으로 많은 제조업체들은 패치 적용이 단순화되고 AI 업그레이드에 즉시 액세스할 수 있기 때문에 3년 이내에 비생산 로봇을 SaaS로 마이그레이션할 계획입니다. 이러한 전환으로 구독 수익이 영구 라이선스를 능가하고 로보틱 프로세스 자동화(RPA) 시장은 계속 확대될 것으로 예측됩니다.

2025년에는 소프트웨어 플랫폼이 수익의 51.05%를 차지했지만 조직이 인적 요소를 중시한 변경 관리가 성공의 열쇠라고 인식함에 따라 서비스 분야는 CAGR 34.1%로 확대되고 있습니다. 도입 기업은 발견, 재설계, 시민 개발자를 위한 코칭을 통합하는 경우가 증가하고 있으며, 이들은 변혁 예산 전체의 약 60%를 차지하고 있습니다. SS&C Technologies는 Blue Prism 소프트웨어와 권고 서비스를 결합하여 봇 수를 3배로 늘려 1억 달러의 비용 절감을 실현했습니다.

지속적 개선 리테이너 계약 수요도 높아지고 있습니다. 지능형 자동화에는 AI 모델의 지속적인 조정이 필수적이기 때문입니다. 벤더 각 회사는 현재 개별 프로젝트의 이정표가 아닌 SLA 기반 성과를 보장하는 관리 서비스를 제공합니다. 이 전환으로 서비스 분야에 할당되는 로보틱 프로세스 자동화(RPA) 시장 규모는 더욱 확대되어 툴 도입에서 전사적인 업무 모델 재설계로 진화하는 업계 동향이 부각되고 있습니다.

로보틱 프로세스 자동화(RPA) 시장은 도입 형태(On-Premise/클라우드·SaaS), 솔루션 구성 요소(소프트웨어/서비스), 기업 규모(중소기업/대기업), 기술 유형(유인 RPA/무인 RPA/인텔리전트/인지 RPA), 최종사용자 업계(금융 및 보험·증권/IT 및 통신/의료 등) 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2025년에 39.12%의 점유율로 선두를 유지했습니다. 이는 정부기관과 금융서비스 업계에서 조기 도입의 추세와 엄격한 컴플라이언스 요건에 힘쓰고 있습니다. 미국 주택도시개발성 등의 기관에서는 급여 처리의 근대화를 위해 RPA와 머신러닝을 조합한 방법을 채용하고 있습니다. 캘리포니아 주 차량 관리국(DMV)과 같은 주 기관은 유행에 의한 혼란에도 계속 업무를 수행할 수 있도록 디지털 라이선싱 서비스 가속화를 위해 봇을 활용했습니다. 벤더 상황은 풍부한 시스템 통합사업자 능력과 숙련된 자동화 전문가의 도움으로 지속적인 파이프라인 성장을 보장합니다.

아시아태평양은 33.6%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 일본의 RPA 「Robopat DX」는 중소기업용 도입 건수가 1,700건을 돌파해, 인수 부족 시장에 있어서 풀의 근적인 수요를 나타내고 있습니다. 인도의 매니팔 병원에서는 확대되는 디지털 의료 규정에 대응하기 위해 재무 워크플로우를 자동화했습니다. 정부의 보조금 제도와 현지 언어 인터페이스를 지원함으로써 제조업과 아웃소싱 거점에서의 도입이 더욱 확대되고, 이 지역의 로봇식 프로세스 자동화(RPA) 시장을 확대될 전망입니다.

유럽의 동향은 '디지털 업무 탄력성법'에 의해 형성되고 있으며, 이 법은 은행에 자동화 워크플로우의 문서화와 스트레스 테스트를 의무화하고 있습니다. 금융기관은 2025년 컴플라이언스 마감일을 맞추기 위해 기관당 최대 1,500만 유로에 이르는 여러 해 예산을 확보하고 있습니다. 독일 제조업체는 백오피스 업무의 고급 자동화를 추진하고 있으며, 북유럽 의료 시스템은 지역 횡단적인 공유 봇 라이브러리를 도입하고 있습니다. 데이터를 On-Premise로 유지하면서 클라우드 콘솔에서 통합 관리하는 하이브리드 배포 구조가 표준이 되고 있으며, 유럽 연합 회원국 전체에서 로보틱 프로세스 자동화(RPA) 시장의 존재가 꾸준히 확대되고 있습니다.

The Robotic Process Automation Market was valued at USD 6.31 billion in 2025 and estimated to grow from USD 8.12 billion in 2026 to reach USD 28.6 billion by 2031, at a CAGR of 28.66% during the forecast period (2026-2031).

Increasing integration of generative AI with established RPA platforms widens the range of automatable tasks and lets enterprises address unstructured processes that once required human intervention. Expansion is also fueled by cloud-native deployments that shorten implementation cycles and shift spending to operating budgets. North America held the largest Robotic Process Automation market share at 39.6% in 2024, supported by stringent compliance mandates and mature technology ecosystems, while Asia-Pacific is registering the fastest regional CAGR of 34.5% as governments sponsor automation programs and SMEs adopt pay-as-you-go bots. Vendor competition is intensifying through AI-focused acquisitions and partnerships that bundle intelligent document processing, low-code design, and autonomous agent capabilities into platform roadmaps.

Retailers are automating inventory reconciliation, shipment orchestration, and return management to keep pace with real-time consumer expectations. Grupo Exito cut order-processing times by up to 75% after deploying an enterprise-wide RPA program that links e-commerce front ends with legacy ERP data. Integration of computer-vision modules maintains accuracy above 98% during peak seasons, while AI-assisted demand forecasting helps retailers manage margin pressure amid supply-chain volatility. Retailers in both mature and emerging e-commerce markets, therefore, view automation as an essential hedge against logistics disruptions and labor shortages.

Consumption-based SaaS models are lowering entry barriers for small firms. Jana Small Finance Bank shortened critical process turnaround times by nearly 70% after migrating to UiPath's cloud service, with no on-premise infrastructure required. As hyperscale providers embed RPA into their marketplaces, SMEs can deploy secure bots within days and scale licenses only when transaction volumes rise. Analysts expect SMEs to drive more than 40% of net-new bot deployments by 2027 as citizen-developer tools mature and industry-specific templates proliferate.

Frequent interface updates in enterprise and SaaS apps disrupt selectors and render bots inoperable, consuming up to 40% of annual automation budgets for reactive maintenance. Tarsus Distribution had to redesign invoice workflows when supplier formats shifted, highlighting the fragility of legacy, screen-scraping bots. Newer platforms add object-based selectors and self-healing functions, yet change-management shortcomings continue to delay scaling plans and erode confidence in early-stage programs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

On-premise installations remained dominant at 53.62% of the Robotic Process Automation market in 2025 because heavily regulated sectors required local control. Cloud deployments nevertheless posted the highest 36.95% CAGR and will narrow the gap as security certifications expand. UiPath stated that more than 80% of new bookings stem from cloud subscriptions, and customers achieve rollouts 50% faster than on-premise equivalents. The hybrid pattern is gaining ground as European banks keep sensitive payment workflows in-house while using cloud tenants for design, test, and analytics. This flexibility lets firms satisfy residency mandates without forfeiting elastic capacity.

As edge computing matures, vendors package lightweight run-times that execute locally yet receive orchestration from the cloud. Such architectures reduce latency for factory-floor bots while minimizing server administration overhead. Consequently, many manufacturers plan to migrate their non-production robots to SaaS within three years, citing simplified patching and immediate access to AI upgrades. The resulting shift will continue to boost the Robotic Process Automation market as subscription revenue overtakes perpetual licenses.

Software platforms controlled 51.05% of revenue in 2025, but services are expanding at a 34.1% CAGR as organizations recognize that people-centric change management dictates success. Implementers increasingly bundle discovery, re-engineering, and citizen-developer coaching, representing roughly 60% of total transformation budgets. SS&C Technologies realized USD 100 million in cost savings by pairing Blue Prism software with advisory services that tripled its bot count.

Demand for continuous-improvement retainers is also rising because intelligent automation requires ongoing AI model tuning. Vendors now position managed service offers that guarantee SLA-based outcomes rather than discrete project milestones. This pivot further inflates the Robotic Process Automation market size allocated to services and underscores the sector's progression from tool adoption toward enterprise-wide operating model redesign.

Robotic Process Automation Market is Segmented by Deployment (On-Premise and Cloud/SaaS), Solution Component (Software and Services), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Technology Type (Attended RPA, Unattended RPA, and Intelligent/Cognitive RPA), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained leadership with a 39.12% share in 2025, propelled by early adoption curves and rigorous compliance mandates across government and financial services. Agencies such as the U.S. Department of Housing and Urban Development employ combined RPA and machine-learning approaches to modernize benefit processing. State entities like the California DMV leveraged bots to accelerate digital licensing services, allowing continuity during pandemic disruptions. The vendor landscape benefits from abundant system-integrator capacity and skilled automation professionals, ensuring continuous pipeline growth.

Asia-Pacific is the fastest-growing geography at 33.6% CAGR. Japan's RPA Robopat DX passed 1,700 SME implementations, signaling grassroots demand in a tight labor market. India's Manipal Hospitals automated finance workflows to comply with expanding digital health regulations. Government subsidy schemes and local-language interface support will further widen adoption among manufacturers and outsourcing hubs, magnifying the Robotic Process Automation market in the region.

Europe's trajectory is shaped by the Digital Operational Resilience Act, which compels banks to document and stress-test automated workflows. Institutions have earmarked multi-year budgets reaching EUR 15 million per entity to meet the 2025 compliance deadline. German manufacturers showcase deep back-office automation, while Nordic healthcare systems deploy region-wide shared-bot libraries. Hybrid deployment structures that retain data on-premise yet orchestrate via cloud consoles are becoming the norm, steadily increasing the Robotic Process Automation market presence across European Union member states.