RPA 플랫폼 트레이닝 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

RPA Platform Training Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797751

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 170 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

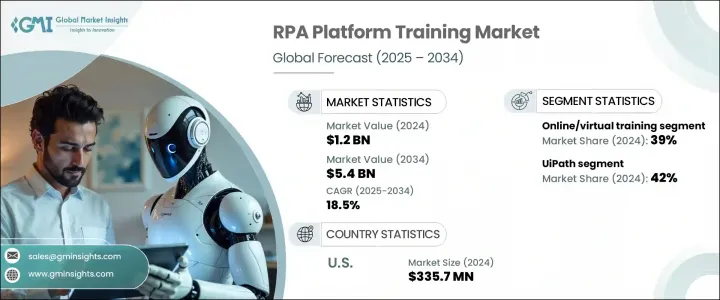

세계의 RPA 플랫폼 트레이닝 시장 규모는 2024년 12억 달러로 평가되었고, CAGR 18.5%를 나타내 2034년 54억 달러에 이를 것으로 예측됩니다.

Robotic Process Automation(RPA) 플랫폼이 계속 발전하고 AI, NLP, OCR과 같은 첨단 기술과 통합됨에 따라 교육은 기본 기술 기술에서 기업 수준의 핵심 요구 사항으로 변화하고 있습니다. 기업은 현재 자동화의 성과를 대규모로 달성하기 위해서는 체계적이고 지속적인 스킬업이 필수적이라고 생각하고 있습니다. 이러한 변화는 개발자, 분석가 및 비즈니스 사용자를 대상으로 한 역할에 따라 전문적인 교육 경로에 대한 수요를 가속화합니다.

업계 전반에 걸쳐 자동화에 대한 의존도가 증가함에 따라 하이브리드 및 모듈형 학습 프로그램이 급증하고 있습니다. 정부와 민간기업도 인재 부족을 해소하기 위해 공동으로 스킬링에 임하고 있습니다. 가상 학습 형식은 유행성(세계적 유행)에서 인기를 얻었고, 그 접근성과 확장 성의 높이에서 여전히 주류가되고 있습니다. 엔터프라이즈 고객은 특정 플랫폼에 따른 인증 자격을 강력히 지지하고 있으며, 자동화 이니셔티브 전반에 걸쳐 표준화된 구현 및 거버넌스를 보장합니다. 유력 벤더의 인증 자격은 표준 채용 기준이되고 있습니다. 교육이 디지털 전환 과제에 깊숙히 통합되어 있는 현재, 학습 플랫폼은 기업의 학습자와 자동화 노동력에 진입하는 개인 모두에게 서비스를 제공하기 위해 규모를 확대하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

당초 시장 규모

12억 달러

시장 규모 예측

54억 달러

CAGR

18.5%

온라인 교육 분야는 2024년에는 39%의 점유율을 차지했고, 2034년까지 연평균 복합 성장률(CAGR)은 20%를 나타낼 전망입니다. Virtual Delivery는 유연하고 온디맨드 특성과 분산된 팀을 지원할 수 있는 기능을 통해 비즈니스 기능 전반에 걸쳐 선호되는 모드입니다. 이러한 디지털 프로그램에는 봇 구축, 오케스트레이션 및 컴플라이언스에 대한 대화형 모듈이 포함되어 있어 확장성이 높고 기업 자동화 목표를 충족합니다.

UiPath 교육 부문은 2024년에 42%의 점유율을 차지했고 2034년까지 20%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. UiPath의 생태계는 기업, 대학 및 개인 학습자의 자동화 능력을 구축하는 데 도움이 됩니다. UiPath는 기술 및 비기술 사용자를 대상으로 설계된 체계적인 프로그램을 통해 강력한 학습 플랫폼을 통해 일관되고 확장 가능한 컨텐츠를 제공합니다. 이러한 리소스는 자동화 도입에 대한 기업의 준비 태세를 강화하면서 다양한 역할 기술을 지원합니다.

미국의 RPA 플랫폼 트레이닝 시장은 2024년 82%의 점유율을 차지했으며 3억 3,570만 달러를 창출했습니다. 이 나라는 대기업의 높은 자동화 도입률, 성숙한 디지털 학습 인프라 및 EdTech 플랫폼의 활기찬 네트워크를 통해 계속 주도하고 있습니다. AI 혁신과 기업의 디지털 전환에 있어서의 이 나라의 리더십은 RPA에 특화된 스킬 업 프로그램에 대한 왕성한 수요에 더욱 기여하고 있습니다.

RPA 플랫폼 트레이닝 시장을 형성하는 주요 기업은 Automation Anywhere, UiPath, SS&C Blue Prism, Coursera, Simplilearn, Udemy, Edureka를 포함합니다. RPA 플랫폼 트레이닝 분야의 기업은 시장의 발판을 굳히기 위해 표준화와 인재의 즉전력화라는 기업의 요구에 부응하기 위해 구조화된 역할별 학습 경로와 세계적으로 인지된 인정 자격을 개발하고 있습니다. 또한 학술기관, 기업고객, 정부와의 전략적 제휴를 통해 엄선된 컨텐츠 및 인증코스에 폭넓게 액세스할 수 있습니다. 주요 플랫폼은 원활한 액세스를 위해 클라우드 기반 배포에 투자하면서 AI와 자동화의 최신 진보를 포함하기 위해 컨텐츠를 지속적으로 업그레이드하고 있습니다. 또한 세계에 전개하기 위해 다국어 교육 모듈과 모바일 친화적인 플랫폼을 출시하고 있습니다.

목차

제1장 분석 방법

시장의 범위와 정의

분석 디자인

분석 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 분석과 검증

1차 정보

예측 모델

분석의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

업계에 미치는 영향요인

성장 촉진요인

업계 전체에서 RPA의 도입이 증가

디지털 변혁의 대처

RPA 인증 자격 수요 증가

AI와 RPA의 통합

업계의 잠재적 위험과 과제

표준화된 커리큘럼의 부족

비기술계 전문가 사이의 낮은 인지도

시장 기회

마이크로 인증 및 스킬 배지

학습 플랫폼에 AI 통합

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

스킬 갭 분석과 인재 개발

현재의 RPA 스킬 부족의 평가

미래의 노동력 요건

스킬업과 재교육의 대처

기업연수와 개인인정

학술기관과의 제휴

정부 연수 프로그램

RPA에서의 캐리어 패스 개발

가격 분석과 비용 모델

연수 비용 구조 분석

벤더의 가격 전략

구독 모델과 일괄 지불 모델

기업 연수 패키지의 가격

인증 비용 분석

연수 투자의 ROI 평가

플랫폼 간의 비용 비교

특허 분석

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경 친화적인 노력

탄소발자국의 고려

이용 사례

최상의 시나리오

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

기업 합병·인수(M&A)

사업 제휴 및 협력

신제품 발매

확장계획과 자금조달

제5장 시장 추계·예측 : 트레이닝별(2021-2034년)

주요 동향

온라인/가상 트레이닝

강의실 트레이닝

기업/엔터프라이즈 연수

인증 프로그램

제6장 시장 추계·예측 : 플랫폼별(2021-2034년)

주요 동향

UiPath

Automation anywhere

Blue prism

기타

제7장 시장 추계·예측 : 기업 규모별(2021-2034년)

주요 동향

중소기업

대기업

제8장 시장 추계·예측 : 제공 방식별(2021-2034년)

주요 동향

자기 주도 학습

강사 주도 트레이닝(ILT)

혼합 학습

워크숍 및 부트캠프

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

학생

IT 전문가

기업 직원

프리랜서/컨설턴트

제10장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

Automation Anywhere

Besant Technologies

Codecademy

Cognixia

Coursera

Edureka

Great Learning

GreyCampus

Intellipaat

Kelly Technologies

LinkedIn Learning

MindMajix

NobleProg

Pluralsight

RPA Academy

Simplilearn

Skillsoft

SS&C Blue Prism

Udemy

UiPath

KTH

영문 목차

영문목차

The Global RPA Platform Training Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 18.5% to reach USD 5.4 billion by 2034. As robotic process automation platforms continue to evolve and integrate with advanced technologies like AI, NLP, and OCR, training has shifted from a basic technical skill to a core enterprise-level requirement. Companies now view structured, ongoing upskilling as critical for achieving automation outcomes at scale. This transformation is accelerating the demand for specialized, role-based training paths tailored to developers, analysts, and business users alike.

The increasing reliance on automation across industries has driven a surge in hybrid and modular learning programs. Governments and the private sector are also launching collaborative skilling efforts to close talent gaps. Virtual learning formats gained traction during the pandemic and remain dominant due to their accessibility and scalability. Enterprise clients heavily favor certifications aligned with specific platforms, which ensures standardized implementation and governance across automation initiatives. Certifications from dominant vendors are becoming standard hiring criteria. With training now deeply embedded in digital transformation agendas, learning platforms are scaling up to serve both corporate learners and individuals entering the automation workforce.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.2 Billion

Forecast Value

$5.4 Billion

CAGR

18.5%

The online training segment held a 39% share in 2024 and will grow at a 20% CAGR through 2034. Virtual delivery is the preferred mode across business functions, given its flexible, on-demand nature and ability to support distributed teams. These digital programs include interactive modules on bot building, orchestration, and compliance, making them highly scalable and aligned with enterprise automation goals.

The UiPath training segment held a 42% share in 2024 and is anticipated to grow at a CAGR of 20% through 2034. Its ecosystem has become instrumental in building automation capability across businesses, universities, and independent learners. Through structured programs designed for both technical and non-technical users, UiPath delivers consistent, scalable content via its robust learning platform. These resources support upskilling across a wide range of roles while reinforcing enterprise readiness for automation adoption.

United States RPA Platform Training Market held an 82% share in 2024, generating USD 335.7 million. The country continues to lead due to high automation adoption among large enterprises, a mature digital learning infrastructure, and a vibrant network of EdTech platforms. Its leadership in AI innovation and corporate digital transformation further contributes to strong demand for RPA-specific upskilling programs.

The major players shaping the RPA Platform Training Market include Automation Anywhere, UiPath, SS&C Blue Prism, Coursera, Simplilearn, Udemy, and Edureka. To strengthen their market foothold, companies in the RPA platform training space are developing structured, role-specific learning paths and globally recognized certifications to meet enterprise demands for standardization and talent readiness. Strategic alliances with academic institutions, enterprise clients, and governments are also enabling broader access to curated content and certification tracks. Leading platforms are continuously upgrading content to include the latest advancements in AI and automation while investing in cloud-based delivery for seamless access. Companies are also launching multilingual training modules and mobile-friendly platforms to scale globally.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Training

2.2.3 Platform

2.2.4 Enterprise Size

2.2.5 Delivery Mode

2.2.6 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising adoption of RPA across industries

3.2.1.2 Digital transformation initiatives

3.2.1.3 Growing demand for RPA certifications

3.2.1.4 Integration of AI with RPA

3.2.2 Industry pitfalls and challenges

3.2.2.1 Lack of standardized curriculum

3.2.2.2 Limited Awareness among non-tech professionals

3.2.3 Market opportunities

3.2.3.1 Micro-certifications and skill badging

3.2.3.2 AI integration into learning platforms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Skills gap analysis and workforce development

3.8.1 Current RPA skills shortage assessment

3.8.2 Future workforce requirements

3.8.3 Reskilling and upskilling initiatives

3.8.4 Corporate training vs individual certification