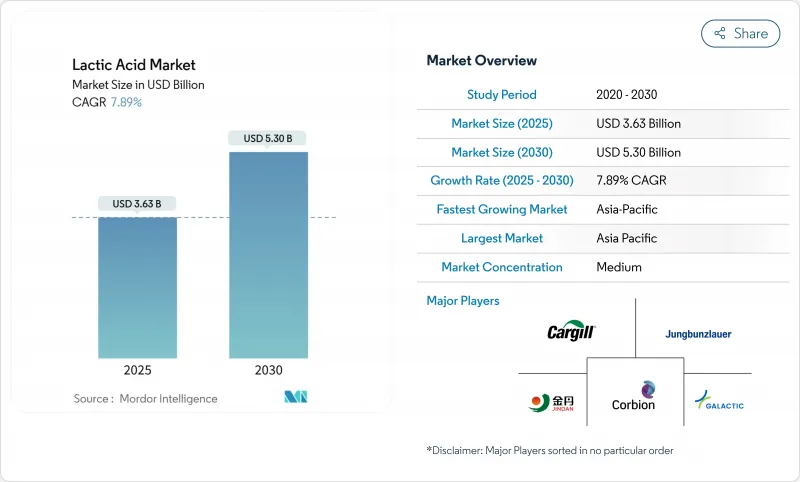

세계의 젖산 시장 규모는 2025년 36억 3,000만 달러에서 2030년에는 53억 달러에 달하고, CAGR 7.89%로 확대될 것으로 예측됩니다.

시장 확대의 주요 요인은 생분해성 플라스틱, 의약품 부형제, 산업용 세정제로의 용도 확대입니다. 생분해성 플라스틱 분야는 환경 문제에 대한 우려와 기존 플라스틱에 대한 엄격한 규제에 의해 성장하고 있습니다. 의약품에서 젖산은 약물 제제 및 방출 제어 시스템에 필수적입니다. 산업용 세척 분야에서는 항균 및 환경적 적합성을 위해 젖산이 사용됩니다. 3D 프린팅 분야에서는 젖산 기반 재료가 기계적 특성과 생체적합성을 향상시키는 이점이 있습니다. 업계는 수직 통합, 다양한 원료 공급원 및 공정 최적화를 통해 경쟁력을 유지하며 제조업체가 원료 가격 변동을 효과적으로 관리할 수 있도록 합니다. 여기에는 고급 발효 기술, 효율적인 정제 공정 도입, 밸류체인 전반에 걸친 전략적 파트너십 구축 등이 포함됩니다.

젖산 식품 첨가물에서 폴리머 전구체로의 진화는 폴리유산(PLA) 용도가 시장 전체의 CAGR에 기여함으로써 시장의 현저한 성장을 이끌고 있습니다. 2025년까지 상업운전을 시작할 예정인 NatureWorks의 태국에 있는 6억 달러의 시설은 젖산 생산, 젖산 합성, PLA 중합을 하나의 시설로 통합함으로써 이 전환을 실증하고 있습니다. 이 시설의 통합적 접근은 생산 효율을 최적화하고 운영 비용을 절감하는 것을 목표로 합니다. 유럽 연합(EU)의 단일 사용 플라스틱 지침은 특정 포장 용도에 생분해성 대체품을 요구함으로써 시장 성장을 지원하고 PLA 채택에 유리한 규제 프레임워크를 만들어 내고 있습니다. UAE에서 계획된 Emirates Biotech의 시설은 세계 최대의 PLA 공장이 될 예정이며, 이 시장에 중동 투자가 증가하고 있음을 보여주고 있으며, 이 지역의 지속 가능한 재료 생산에 대한 노력을 부각하고 있습니다. PLA 기술의 3D 프린팅 필라멘트 및 의료기기로의 확장은 시장의 잠재력을 넓히고 제조 및 헬스케어 용도에 혁신적인 솔루션을 제공합니다. FDA에 의한 폴리L-락트산의 안면 지방 감소 치료에 대한 승인은 고가치 의료 분야에서의 다목적성 및 안전성 프로파일을 나타냅니다. 지지적인 규제 프레임워크, 지속적인 기술 진보, 제조 능력의 향상이 결합되어 PLA가 2030년까지의 젖산 시장 성장의 주요 원동력이 되어, 업계 정세를 재형성하고, 지속 가능한 재료 솔루션의 새로운 기회를 창출합니다.

식품 및 음료 분야는 젖산의 가장 큰 최종 시장임에 변함이 없으며 클린 라벨 제품과 자연 보존 방법에 대한 수요 증가가 성장을 지원합니다. FDA에 의한 젖산의 GRAS(Generally Recognized as Safe: 일반적으로 안전하다고 인정됨) 지정은 적정 제조 규범(Good Manufacturing Practice)에 한정된 제한으로, 식품 제조업체에 제품 처방, 안전 컴플라이언스, 품질 관리 대책에 관한 종합적인 규제 지침을 제공합니다. USDA(미국 농무성)의 조사에서는 젖산의 살모넬라균에 대한 유효성을 확인하고, 관리된 시험에서 병원균의 감소율을 실증하고, 기존 유제품 발효 공정 이외에도 사용이 확대되고 있습니다. 젖산의 항균 특성은 다양한 식품 매트릭스에서 폭넓게 문서화되어 있으며, 특히 식용육 및 가금류 처리 환경에서 효능을 나타내고 있습니다. 유럽식품안전기관은 소고기 제염에 젖산을 2-5%의 농도로 사용하는 것을 추천하고 있어 식품안전 프로토콜, 미생물 제어 전략, 식육가공 전체의 위생기준에서 젖산의 역할을 강화하고 있습니다. 식물 유래 유제품 분야에서 제조업체는 특정 유산균 균주를 이용하여 이취를 억제하고 영양 흡수를 높이고 식감 프로파일을 개선하고 유기적 특성 개선, 기능적 이점, 보존 기간 연장을 통해 제품 차별화의 기회를 창출하고 있습니다. 젖산의 식물성 유제품에의 응용은 특히 요구르트 대체물 및 치즈 대체물과 같은 발효 제품에서 단백질 안정화 및 풍미 개발에 유망한 결과를 나타냅니다.

제조 비용은 시장 성장을 크게 저해하며, 특히 가격에 민감한 산업 분야에서 젖산의 경쟁력에 영향을 미칩니다. 발효 기반 생산 공정은 환경 혜택에도 불구하고 합성 화학 경로와 비교하여 특수 생물 반응기, 고급 분리 장치 및 복잡한 정제 시스템에 많은 자본 투자가 필요합니다. Corbion의 2024년 자본 시장 프레젠테이션은 지속적인 비용 경쟁력 과제를 해결하기 위해 종합적인 업무 효율성 개선과 전략적 구조화 이니셔티브를 강조하고 있습니다. 현재의 비용 구조는 젖산이 합성 방부제 및 산미료와 직접 경쟁하는 범용 용도에 큰 영향을 미치며 우수한 환경적 이점과 지속 가능한 특성에도 불구하고 가격에 민감한 분야에서 시장 침투를 제한합니다. 높은 생산 비용은 원재료 조달에서 최종 제품 유통에 이르는 밸류체인 전반에 영향을 미치며, 제품의 품질과 지속가능성 기준을 확보하면서 경쟁력 있는 가격 설정을 유지하려는 제조업체에게 추가적인 과제를 제기하고 있습니다.

천연 발효는 2024년 젖산 시장 점유율의 88.14%를 차지하고 2030년까지 연평균 복합 성장률(CAGR)은 8.34%를 보일 것으로 예측됩니다. 바이오 제품에 대한 소비자의 선호도는 지속 가능한 생산 방법과 환경 문제에 대한 의식 증가로 인해 발생합니다. 특히 식음료 용도에서는 천연 유래 산을 지지하는 식품안전규제가 이 생산방법의 우위성을 더욱 강화하고 있습니다. 주로 석유 중간체로부터의 합성 생산은 화학제조 및 산업용도와 같은 비용이 우선적으로 고려되는 특정 산업 분야를 대상으로 합니다.

천연 발효의 기술적 진보로는 다른 원료의 동시 발효를 가능하게 하는 다기질 처리, 변환 효율을 향상시키는 유전자 편집 유산균주, 생산 수율을 향상시키는 in situ 생성물 제거 기술 등이 있습니다. 과실 폐기물과 리그노셀룰로오스계 잔사를 이용한 실증 프로젝트의 성공은 식용 작물과 경쟁하지 않고 생산 규모를 확대할 수 있는 가능성을 나타냅니다. 이러한 대체 원료 공급원에는 농업 잔류물, 식품 가공 폐기물, 임업 제품별 등이 포함됩니다. 이러한 원료의 다양화는 순환경제의 원칙을 추진하면서 곡물가격 변동으로부터 유산시장을 보호하는 데 도움이 됩니다.

액체 젖산은 식품, 의약품 및 클린 인 플레이스(CIP) 용도의 직접 펌프 시스템에 적합하기 때문에 2024년 64.82%의 판매 점유율을 차지했습니다. 대부분의 산업용 바이오리액터와 다운스트림 충전 장치는 리퀴드 핸들링 작업을 위해 특별히 설계되고 최적화되어 있기 때문에 이 형태는 시장의 우위를 유지합니다. 산업 전반에 걸친 액체 처리 시스템에 대한 광범위한 인프라 투자는 이러한 이점을 더욱 강화하고 있습니다. 고형제 부문은 CAGR 8.66%로 성장하고 있으며, 특히 보관 및 운송 조건이 엄격한 지역에서의 동물사료 프리믹스나 드라이브 렌드의 퍼스널케어 제품에서의 채용이 증가하고 있습니다. 이 성장은 또한 수명이 긴 제품에 대한 수요 증가와 벌크 제조 공정에서의 취급의 용이성에도 뒷받침됩니다.

분무 건조 및 결정화 공정에서의 최근 기술 발전으로 제조업체는 선적 무게를 크게 줄이면서 제품의 순도 수준을 높게 유지할 수 있습니다. 이러한 개선에는 최적화된 입자 크기 분포와 향상된 수분 제어 시스템이 포함됩니다. 멤브레인 기술과 증발 공정을 결합한 새로운 하이브리드 시스템은 여러 생산 시설에서 수행된 파일럿 연구에 따라 에너지 소비를 10% 이상 줄입니다. 이러한 효율 개선으로 액체와 고체의 역사적인 가격차가 서서히 축소되어 다양한 용도에서 고체의 경쟁력이 높아지고 있습니다. 특수 포장 솔루션의 개척과 보존 안정성 향상으로 신흥 시장에서 고형 젖산의 매력이 더욱 높아지고 있습니다.

아시아태평양은 2024년 31.08% 시장 점유율을 차지했으며, 2030년까지 9.08%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 지역은 태국, 중국, 인도의 통합 제조 시설을 통해 경쟁 우위를 유지하고 있으며, 이러한 시설은 입수하기 쉬운 사탕수수와 옥수수 원료로부터 혜택을 누리며 설치 톤당 필요한 자본 지출도 적습니다. NatureWorks의 태국 시설은 지역 생산 원료의 가용성, 규모의 경제성 및 수출 항구에 대한 전략적 근접성을 결합하여 이 지역 전략을 구현합니다. 시장 성장은 일회용 푸드서비스 용품에 대한 국내 수요 증가와 퇴비화 가능한 쇼핑백에 대한 규제 요건에 의해 더욱 지원되고 있습니다.

북미는 확립된 옥수수 습식 밀링 인프라, 정교한 바이오 가공 능력 및 명확하게 정의된 규제 프레임워크를 통해 시장에서의 지위를 유지하고 있습니다. 이 지역은 의료, 개인 관리 및 식품 안전 분야에서 고가치 용도에 중점을 둡니다. 아시아에서 PLA 패키징 수입이 증가하고 있음에도 불구하고 북미 시장은 범위 3 배출량을 줄이기 위해 현지 조달을 선호하는 기업의 선호로 안정을 유지하고 있습니다.

유럽 시장의 성장은 주로 단일 사용 플라스틱 지침에 의해 발생하며 이 지침은 제조업체에 퇴비화 가능한 대체품의 채택을 장려합니다. Galactic과 Jungbunzlauer와 같은 기업은 규제 요건에 적응하고 의약품 및 화장품 용도로 확고한 지위를 구축하고 있습니다. 농산물 가격의 변동이 채용률에 영향을 미치는 반면, 녹색 거래 구상은 지역 발효 시설에 대한 투자를 계속 지원합니다.

The lactic acid market size is projected to increase from USD 3.63 billion in 2025 to USD 5.30 billion by 2030, at a CAGR of 7.89%.

The market expansion is primarily driven by increasing applications in biodegradable plastics, pharmaceutical excipients, and industrial cleaning products. The biodegradable plastics segment is growing due to environmental concerns and strict regulations on conventional plastics. In pharmaceuticals, lactic acid is essential for drug formulations and controlled-release systems. The industrial cleaning sector uses lactic acid for its antimicrobial properties and environmental compatibility. Growth enablers include integrated manufacturing facilities in Asia-Pacific, European regulations limiting single-use plastics, and the US FDA's GRAS (Generally Recognized as Safe) status.The 3D printing segment benefits from lactic acid-based materials that provide enhanced mechanical properties and biocompatibility. The industry maintains competitiveness through vertical integration, diverse feedstock sources, and process optimization, enabling manufacturers to manage raw material price fluctuations effectively. This includes implementing advanced fermentation technologies, efficient purification processes, and developing strategic partnerships throughout the value chain.

The evolution of lactic acid from a food additive to a polymer precursor is driving significant market growth, with Polylactic Acid (PLA) applications contributing to the overall market CAGR. NatureWorks' USD 600 million facility in Thailand, scheduled for commercial operation by 2025, demonstrates this transition by combining lactic acid production, lactide synthesis, and PLA polymerization in a single facility. The facility's integrated approach aims to optimize production efficiency and reduce operational costs. The European Union's Single-Use Plastics Directive supports market growth by requiring biodegradable alternatives for specific packaging applications, creating a regulatory framework that favors PLA adoption. The planned Emirates Biotech facility in the UAE, set to become the world's largest PLA plant, indicates increasing Middle Eastern investment in this market and highlights the region's commitment to sustainable materials production. The expansion of PLA technology into 3D printing filaments and medical devices has broadened its market potential, offering innovative solutions for manufacturing and healthcare applications. FDA approval of poly-L-lactic acid for facial fat loss treatment demonstrates its versatility and safety profile in high-value medical segments. The combination of supportive regulatory frameworks, continuous technological progress, and increased manufacturing capacity establishes PLA as the main driver of lactic acid market growth through 2030, reshaping the industry landscape and creating new opportunities for sustainable material solutions.

The food and beverage sector remains the largest end-market for lactic acid, with growth supported by increasing demand for clean-label products and natural preservation methods. The FDA's designation of lactic acid as Generally Recognized as Safe (GRAS), with restrictions limited to good manufacturing practices, provides food manufacturers with comprehensive regulatory guidance for product formulation, safety compliance, and quality control measures. USDA research confirms lactic acid's effectiveness in reducing Salmonella in poultry applications, demonstrating pathogen reduction rates in controlled studies and expanding its use beyond traditional dairy fermentation processes.The antimicrobial properties of lactic acid have been extensively documented across various food matrices, showing particular efficacy in meat and poultry processing environments. The European Food Safety Authority encourages lactic acid concentrations of 2-5% for beef carcass decontamination, strengthening its role in food safety protocols, microbial control strategies, and overall meat processing hygiene standards. In the plant-based dairy segment, manufacturers utilize specific lactic acid bacteria strains to reduce off-flavors, enhance nutrient absorption, and improve texture profiles, creating product differentiation opportunities through improved organoleptic properties, functional benefits, and extended shelf life. The application of lactic acid in plant-based dairy alternatives has also shown promising results in protein stabilization and flavor development, particularly in fermented products like yogurt alternatives and cheese substitutes.

Production costs significantly constrain market growth, particularly affecting lactic acid's competitiveness in price-sensitive industrial applications. The fermentation-based production process requires substantial capital investment in specialized bioreactors, advanced separation equipment, and complex purification systems compared to synthetic chemical routes, despite its environmental advantages. Corbion's 2024 capital market presentation emphasizes comprehensive operational efficiency improvements and strategic restructuring initiatives to address persistent cost competitiveness challenges. The current cost structure substantially impacts commodity applications where lactic acid directly competes with synthetic preservatives and acidulants, limiting market penetration in price-sensitive segments despite its superior environmental benefits and sustainable characteristics. The high production costs affect the entire value chain, from raw material procurement to final product distribution, creating additional challenges for manufacturers seeking to maintain competitive pricing while ensuring product quality and sustainability standards.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Natural fermentation accounts for 88.14% of the lactic acid market share in 2024 and is expected to grow at an 8.34% CAGR through 2030. Consumer preference for bio-based products stems from increasing awareness of sustainable production methods and environmental concerns. Food safety regulations supporting naturally derived acids, particularly in food and beverage applications, further reinforce the dominance of this production method. Synthetic production, primarily from petroleum intermediates, serves specific industrial segments where cost is the primary consideration, such as in chemical manufacturing and industrial applications.

Technological advancements in natural fermentation include multi-substrate processing, which allows for simultaneous fermentation of different raw materials, gene-edited Lactobacillus strains that improve conversion efficiency, and in situ product removal techniques that increase production yields. The successful implementation of demonstration projects using fruit waste and lignocellulosic residues indicates the potential for scaled production without competing with food crops. These alternative feedstock sources include agricultural residues, food processing waste, and forestry byproducts. This feedstock diversification helps protect the lactic acid market against fluctuations in grain prices while promoting circular economy principles.

Liquid lactic acid held a 64.82% revenue share in 2024, due to its compatibility with direct pumping systems in food, pharmaceutical, and clean-in-place (CIP) applications. This form maintains its market dominance because most industrial bioreactors and downstream filling equipment are specifically designed and optimized for liquid handling operations. The extensive infrastructure investment in liquid handling systems across industries further reinforces this dominance. The solid form segment is growing at an 8.66% CAGR, driven by increased adoption in animal feed premixes and dry-blend personal care products, particularly in regions with challenging storage and transportation conditions. The growth is also supported by the rising demand for extended shelf-life products and easier handling in bulk manufacturing processes.

Recent technological advancements in spray drying and crystallization processes enable manufacturers to maintain high product purity levels while significantly reducing shipping weights. These improvements include optimized particle size distribution and enhanced moisture control systems. New hybrid systems combining membrane technology and evaporation processes reduce energy consumption by more than 10%, according to pilot studies conducted across multiple production facilities. These efficiency improvements are gradually reducing the historical price difference between liquid and solid forms, making solid lactic acid increasingly competitive in various applications. The development of specialized packaging solutions and improved storage stability has further enhanced the appeal of solid lactic acid in emerging markets.

The Global Lactic Acid Market is Segmented by Source (Natural and Synthetic), Form (Liquid and Solid), Grade (Food Grade, Industrial Grade, and More), Application (Food and Beverages, Personal Care and Cosmetics, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Size and Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held a 31.08% market share in 2024 and is expected to grow at a 9.08% CAGR through 2030. The region maintains a competitive advantage through integrated manufacturing facilities in Thailand, China, and India, which benefit from readily available sugarcane and corn feedstock, along with lower capital expenditure requirements per installed ton. NatureWorks' Thailand facility exemplifies this regional strategy by combining local feedstock availability, economies of scale, and strategic proximity to export ports. The market growth is further supported by increasing domestic demand for disposable food service items and regulatory requirements for compostable shopping bags.

North America maintains its market position through established corn-wet-milling infrastructure, sophisticated bioprocessing capabilities, and well-defined regulatory frameworks. The region focuses on high-value applications in medical, personal care, and food safety sectors. Despite increased PLA packaging imports from Asia, the North American market remains stable due to corporate preferences for local sourcing to reduce scope 3 emissions.

Europe's market growth is primarily driven by the Single-Use Plastics Directive, which encourages manufacturers to adopt compostable alternatives. Companies like Galactic and Jungbunzlauer have adapted to regulatory requirements, establishing strong positions in pharmaceutical and cosmetic applications. While agricultural price fluctuations affect adoption rates, Green Deal initiatives continue to support investments in regional fermentation facilities.