폴리유산 시장 : 등급별, 원재료별, 용도별, 최종 이용 산업별, 지역별 - 예측(-2030년)

Polylactic Acid Market by Grade, Application, End-use Industry, Raw Material, and Region - Global Forecast to 2030

상품코드:1798377

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 268 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

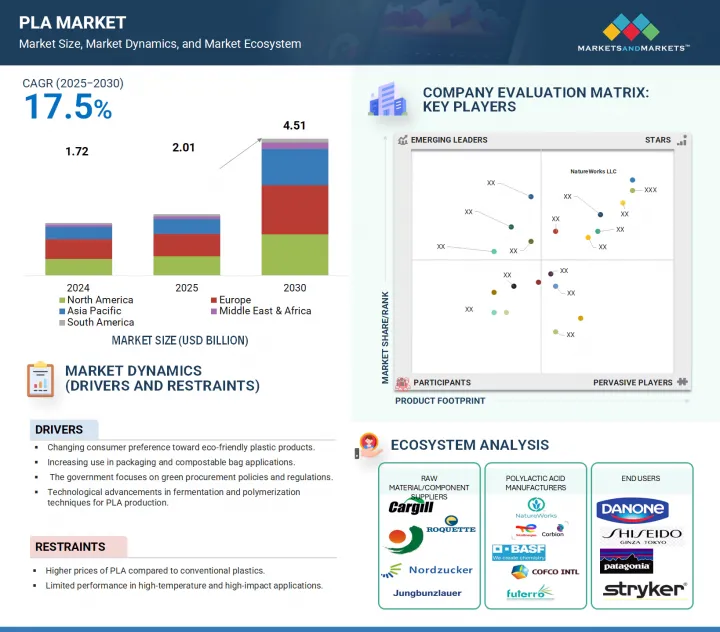

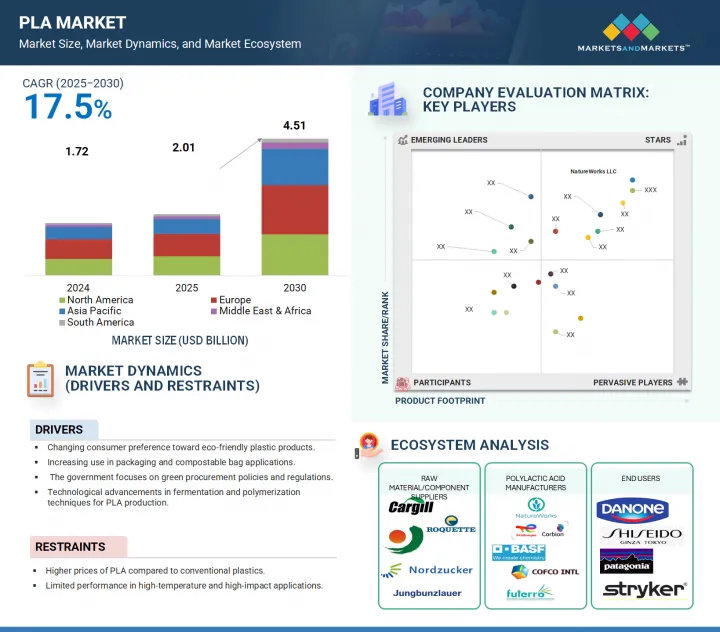

세계의 폴리유산(PLA) 시장 규모는 2025년 20억 1,000만 달러에서 2030년에는 45억 1,000만 달러로 확대되어 예측 기간 CAGR은 17.5%가 될 것으로 예상되고 있습니다.

이러한 성장의 대부분은 식음료 분야에서 퇴비화 가능한 포장재에 대한 수요 증가와 특히 아시아태평양, 유럽 및 북미에서 새로운 대규모 산업용 PLA 생산 공장의 설립에 기인합니다.

조사 범위

조사 대상 연도

2023-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만/10억 달러), 킬로톤(KT)

부문

등급별, 원재료별, 용도별, 최종 이용 산업별, 지역별

대상 지역

아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미

또한, 내열성과 화학적 재활용이 가능한 PLA의 개발이 진행되어 자동차, 전자제품, 내구소비재 등의 용도로 보다 폭넓은 시장 개척의 기회가 생기고 있습니다. 바이오 정제 공장에 대한 투자, 원료의 다양화, 지속 가능한 포장재 개발에 대한 브랜드들의 노력에 힘입어 시장 개척 전망은 여전히 밝습니다. 바이오 의료기기 시장, 복합재료, 저탄소 제조시스템의 새로운 용도도 장기적인 성장 기회를 제공할 것으로 보입니다.

필름 및 시트 응용 분야는 PLA 시장에서 두 번째로 빠르게 성장하는 분야가 될 것으로 예측됩니다. PLA 필름은 우수한 투명성, 밀폐성, 용도에 따라 생분해성으로 인해 유연한 식품 포장, 농업용 멀칭 필름, 퍼스널케어용 포장재, 다양한 라벨 용도 등 다양한 용도로 사용되고 있습니다. 이 시장 부문에서는 기존의 다층 플라스틱 필름에서 벗어나 인증된 퇴비화 가능 포장 제품에 대한 수요가 증가함에 따라 PLA 기반 필름을 대체품으로 채택하는 것이 더 쉬워지고 있습니다. 퇴비화 가능한 패키징 분야의 세계 이니셔티브를 지원한 프로젝트에서 PLA 기반 필름이 라미네이팅, 보온 밀봉, 코팅 응용 분야 및 지속 가능한 제품을 적극적으로 추구하는 기타 부문에서 PLA 기반 필름의 사용이 증가하고 있는 것으로 나타났습니다. 를 보여줍니다.

압출 등급 PLA 부문은 포장, 건축 및 소비자 응용 분야에서 바이오 시트, 필름 및 프로파일에 대한 수요 증가로 인해 2024년 PLA 시장에서 두 번째로 빠르게 성장하는 부문이 될 것으로 예측됩니다. PLA는 표준 압출 장비를 사용할 수 있고, 내열성, 기계적 안정성이 향상되어 경질과 연질 모두에서 기존 폴리머를 대체할 수 있는 유력한 대안으로 여겨지고 있습니다. 특히 성형성, 투명성, 퇴비화성이 요구되는 클램쉘 용기, 블리스 터 팩, 라미네이트 소재, 기타 포장 제품, 특히 성형성, 투명성, 퇴비화가 필요한 경우 효과적인 대안으로 활용이 증가함에 따라 압출 성형 분야는 더욱 발전하고 있습니다. 식품 포장 및 산업용 시트 시장이 보다 지속 가능한 재료로 전환하는 가운데, 압출 등급 PLA 부문은 저렴한 대안을 제공함과 동시에 대규모의 효율적인 가공을 실현하고 환경에 미치는 전반적인 영향을 줄일 수 있습니다. 공 압출 및 다층 PLA 구조와 같은 다른 혁신은이 부문의 국제적인 발자국을 늘리는 데 도움이 될 것으로 보입니다.

옥수수 전분 부문은 2024년 사탕수수에 이어 두 번째로 빠르게 성장하는 PLA 원료 공급원입니다. 옥수수 전분은 특히 북미, 유럽, 중국에서 젖산 발효를 위한 가장 두드러지고 쉽게 구할 수 있는 원료로 남아 있습니다. 강력한 공급망, 경쟁력 있는 가격, 높은 발효 가능한 당 함량이라는 장점이 있어 대규모 PLA 생산에 매력적입니다. 옥수수를 원료로 한 PLA 시장 개척은 생분해성 포장재 및 농업용 필름에 대한 소비자 및 규제 당국 수요 증가, 특히 옥수수 가공 인프라가 잘 구축된 신흥국 시장에서 수요 증가에 힘입은 바 큽니다. 또한, 유전자 변형이 없는 밭에서 재배된 옥수수를 발효시켜 탄소 효율이 높은 생산 방법을 개발하기 위한 연구가 진행 중이기 때문에 지속가능성에 대한 인식이 높아져 옥수수 전분의 마케팅 전망이 개선될 가능성이 높습니다.

중동 및 아프리카는 2024년 PLA 지역 시장 중 두 번째로 빠르게 성장할 것으로 예측됩니다. 플라스틱 오염에 대한 인식 증가, 바이오 대체 포장재의 채택, 지속 가능한 개발 목표(SDGs)를 향한 이 지역의 추진이 개발의 원동력이 되고 있습니다. 중동 및 아프리카의 각국 정부는 일회용 플라스틱을 줄이기 위한 법률을 도입하고 있으며, 이 지역에서 사업을 운영하는 다국적 FMCG 기업들은 지속가능성 약속을 위해 PLA 기반 재료로 전환하고 있습니다. 또한, 걸프 국가, 남아프리카, 북아프리카 국가들의 식품 포장, 소비재, 농업 부문의 확대는 PLA 채택의 유망한 기반이 되고 있습니다. 이 지역은 또한 바이오매스 자원에 대한 비용 경쟁력 있는 접근을 제공하고, 그린 테크놀러지 및 바이오 산업에 대한 해외 직접 투자를 유치하여 PLA 시장의 성장을 더욱 촉진하고 있습니다.

대상 기업: NatureWorks LLC(미국), TotalEnergies Corbion(네덜란드), BASF SE(독일), COFCO(중국), Futerro(벨기에), Danimer Scientific(미국), Toray Co. Industries(독일), 미쓰비시 화학 주식회사(일본), 유니티카 주식회사(일본)를 대상으로 합니다.

PLA 시장의 주요 업체들의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석 정보를 전해드립니다.

조사 대상

이 보고서는 PLA 시장을 등급(열성형 등급, 사출 성형 등급, 압출 성형 등급, 블로우 성형 등급), 용도(경질 열성형 제품, 필름 및 시트, 병), 최종 이용 산업(포장, 소비재, 농업, 섬유, 바이오 의료), 원료(사탕수수, 옥수수 전분, 캐슈, 고등어), 지역(아시아, 북미, 유럽, 중동 및 아프리카, 일본, 중국) 고등어, 사탕수수), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)을 기준으로 분류하고 있습니다. 본 보고서의 조사 범위에는 PLA 시장의 성장에 영향을 미치는 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 기업에 대한 종합적인 분석을 통해 사업 개요, 제공 제품, PLA 시장 관련 제휴, 계약, 제품 출시, 사업 확장, 인수 등 주요 전략에 대한 통찰력을 제공합니다. 또한, PLA 산업 생태계의 신생 스타트업의 경쟁 분석도 함께 수록되어 있습니다.

이 보고서는 시장 리더와 신규 시장 진출기업에게 전체 PLA 시장과 그 하위 부문의 수익 추정치를 제공합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 사업 포지셔닝에 대한 더 나은 고찰을 얻고, 적절한 시장 개척 전략을 수립하는 데 도움이 될 것입니다. 또한, 이해관계자들이 시장의 흐름을 이해하고 시장 성장 촉진요인 및 과제에 대한 정보를 제공하는 데 도움이 됩니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

폴리유산 시장의 매력적인 기회

폴리유산 시장(등급별)

폴리유산 시장(원재료별)

폴리유산 시장(용도별)

폴리유산 시장(최종 이용 산업별)

폴리유산 시장(국가별)

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

Porter의 Five Forces 분석

밸류체인 분석

특허 분석

가격 분석

폴리유산 평균 판매 가격(지역별, 2022년-2030년)

폴리유산 평균 판매 가격(등급별, 2022년-2030년)

폴리유산 평균 판매 가격(최종 이용 산업별, 2024년)

2024년 시장 상위 3사 별 평균 판매 가격

폴리유산 제조 방법

원재료 분석

에코시스템/시장 매핑

사례 연구

규제 상황

무역 분석

고객의 비즈니스에 영향을 미치는 동향/혼란

2025년-2026년 주요 컨퍼런스 및 이벤트

구입 결정에 영향을 미치는 주요 요인

기술 분석

제6장 폴리유산 시장(등급별)

서론

열성형

사출성형

압출

블로우 성형

기타

제7장 폴리유산 시장(원재료별)

서론

사탕수수

옥수수 전분

카사바

설탕 무우

기타

제8장 폴리유산 시장(용도별)

서론

경질 열성형품

필름 및 시트

보틀

기타

제9장 폴리유산 시장(최종 이용 산업별)

서론

포장

소비재

농업

섬유

바이오메디컬

기타

제10장 폴리유산 시장(지역별)

서론

아시아태평양

중국

인도

일본

한국

기타

유럽

독일

영국

프랑스

이탈리아

스페인

기타

북미

미국

캐나다

멕시코

남미

브라질

기타

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

기타

제11장 경쟁 구도

개요

주요 시장 진출기업의 전략

시장 점유율 분석

매출 분석

기업 평가와 재무 지표

제품/브랜드 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제12장 기업 개요

주요 시장 진출기업

NATUREWORKS LLC

TOTALENERGIES CORBION

BASF SE

COFCO

FUTERRO

DANIMER SCIENTIFIC

TORAY INDUSTRIES, INC.

EVONIK INDUSTRIES

MITSUBISHI CHEMICAL GROUP CORPORATION

UNITIKA LTD.

기타 기업

BIOWORKS CORPORATION

ADBIOPLASTICS

MUSASHINO CHEMICAL LABORATORY, LTD.

HANGZHOU PEIJIN CHEMICAL CO.,LTD.

AKRO-PLASTIC GMBH

FUJIAN GREENJOY BIOMATERIAL CO., LTD.

PLAMFG

FKUR

OTTO CHEMIE PVT. LTD.

RAGHAV POLYMERS

VAISHNAVI BIO TECH

HENAN SINOWIN CHEMICAL INDUSTRY CO., LTD.

EMNANDI BIOPLASTICS

UNILONG INDUSTRY CO., LTD.

PRAJ INDUSTRIES

제13장 부록

LSH

영문 목차

영문목차

The global PLA market is expected to increase from USD 2.01 billion in 2025 to USD 4.51 billion by 2030, translating into a CAGR of 17.5% over the forecast period. Much of this growth can be attributed to increasing demand for compostable packaging in the food and beverage sector, along with the rise of new large-scale industrial PLA production plants, particularly in the Asia Pacific, Europe, and North America regions.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million / Billion) Volume (KT)

Segments

Application, Grade, End-use Industry, Raw Material, and Region

Regions covered

Asia Pacific, North America, Europe, Middle East & Africa, and South America

Additionally, ongoing developments of PLA that are heat-resistant or can be chemically recycled are opening up broader market opportunities for applications in automotive, electronics, and durable goods. The market outlook remains positive, supported by investments in bio-refineries, diversification of feedstocks, and commitments by brands to develop sustainable packaging. Emerging applications in the biomedical device market, composites, and low-carbon manufacturing systems will also present long-term growth opportunities perspective.

"Films & Sheets to Be Second Fastest-Growing Segment in the PLA Market"

The films and sheets application area is expected to be the second-fastest growing segment in the PLA market. PLA films are used in various applications, including flexible food packaging, agricultural mulch films, personal care wrappers, and different labeling uses due to their excellent transparency, sealability, and, for some applications, biodegradability. Within this market segment, it has become easier to adopt PLA-based film as a replacement because of the global shift away from traditional multilayer plastic films and the increasing demand for certified compostable packaging products. Projects that have supported global initiatives in compostable packaging show a rising use of PLA-based films in waiting-to-laminate, thermo-sealing, coating applications, and other segments actively pursuing sustainability products.

"Extrusion grade to be second fastest-growing segment in PLA market"

The extrusion grade PLA segment was the second fastest-growing segment in the PLA market in 2024, due to the increased demand for bio-based sheets, films, and profiles in packaging, construction, and consumer applications. PLA is considered a viable alternative to conventional polymers, in both rigid and flexible approaches, given that PLA can utilize standard extrusion equipment, improvements in thermal resistance, and mechanical stability. The extrusion segment is further advancing due to its increased use as a viable alternative for clamshell containers, blister packs, laminated materials, and other packaging products, especially where formability, clarity, and compostability are necessary. As the food packaging and industrial sheets market shifted toward more sustainable materials, the extrusion grade PLA segment offers inexpensive alternatives, while also offering large-scale, efficient processing, and reducing the overall impact on the environment. Other innovations, such as co-extrusion and multilayer PLA structures, will help increase the segment's footprint internationally.

"The corn starch segment was the second fastest-growing segment of PLA market in 2024."

The corn starch segment was the second-fastest growing source of PLA raw material in 2024, following sugarcane. Corn starch remains the most prominent and readily available feedstock for the fermentation of lactic acid, especially in North America, Europe, and China. It benefits from a strong supply chain, competitive prices, and high fermentable sugar content, making it attractive for large-scale PLA production. Growth in corn-based PLA is supported by increasing consumer and regulatory demand for biodegradable packaging and agricultural films, particularly in developed markets with well-established corn processing infrastructure. Additionally, ongoing research into fermenting non-GMO field corn and developing more carbon-efficient production methods will likely enhance perceptions of sustainability and improve marketing prospects for corn starch.

"Middle East & Africa to be second fastest-growing regional market for PLA"

The Middle East & Africa is anticipated to be the second fastest-growing regional PLA market in 2024. Growth is being driven by increasing awareness of plastic pollution, adoption of bio-based packaging alternatives, and the region's push toward sustainable development goals (SDGs). Governments in the Middle East & Africa are introducing legislation to reduce single-use plastics, and multinational FMCG companies operating in the region are shifting to PLA-based materials for their sustainability pledges. Additionally, the expansion of food packaging, consumer goods, and agriculture sectors across Gulf nations, South Africa, and North African countries provides a promising foundation for PLA adoption. The region also offers cost-competitive access to biomass resources and is attracting foreign direct investment in green technology and bio-based industries, further fueling its PLA market growth.

By Company Type: Tier 1: 23%, Tier 2: 42%, and Tier 3: 35%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: NatureWorks LLC (US), TotalEnergies Corbion (Netherlands), BASF SE (Germany), COFCO (China), Futerro (Belgium), Danimer Scientific (US), TORAY INDUSTRIES, INC. (Japan), Evonik Industries (Germany), Mitsubishi Chemical Group Corporation (Japan), and UNITIKA LTD. (Japan) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the PLA market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the PLA market based on grade (thermoforming grade, injection molding grade, extrusion grade, blow molding grade), application (rigid thermoforms, films & sheets, bottles), end-use industry (packaging, consumer goods, agricultural, textile, bio-medical), raw material (sugarcane, corn starch, cassava, sugarbeet), and region (Asia Pacific, North America, Europe, South America, Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities impacting the growth of the PLA market. A comprehensive analysis of key industry players provides insights into their business overview, products offered, and key strategies such as partnerships, agreements, product launches, expansions, and acquisitions related to the PLA market. Additionally, this report features a competitive analysis of emerging startups in the PLA industry ecosystem.

Reasons to Buy the Report

The report will provide market leaders and new entrants with estimates of revenue figures for the overall PLA market and its subsegments. This report will help stakeholders understand the competitive landscape, gain better insights into positioning their businesses, and develop appropriate go-to-market strategies. It will also help stakeholders understand the market's pulse and offer information on key drivers, restraints, and challenges opportunities.

The report provides insights into the following points:

Assessment of primary drivers (changing consumer preference toward eco-friendly plastic products, Increasing use in packaging and compostable bag applications, government focus on green procurement policies and regulations, technological advancements in fermentation and polymerization techniques for PLA production) restraints (higher prices of PLA than conventional plastics and limited performance in high-temperature and high-impact applications), opportunities (development of new end-use applications, High growth potential in emerging economies of Asia Pacific, versatility of PLA in multiple sectors such as 3D printing, agriculture, and textiles), and challenges (lower thermal stability and mechanical performance compared to traditional plastics, competition from other biodegradable or recycled plastics and High production costs and complexity in scaling up).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the PLA market.

Market Development: Comprehensive information about profitable markets-the report analyzes the PLA market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the PLA market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as NatureWorks LLC (US), TotalEnergies Corbion (Netherlands) , BASF SE (Germany), COFCO (China), Futerro (Belgium), Danimer Scientific (US), TORAY INDUSTRIES, INC. (Japan), Evonik Industries (Germany), Mitsubishi Chemical Group Corporation (Japan), and UNITIKA LTD. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 GROWTH RATE ASSUMPTIONS/FORECAST

2.5.1 SUPPLY SIDE

2.5.2 DEMAND SIDE

2.6 RISK ASSESSMENT

2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYLACTIC ACID MARKET