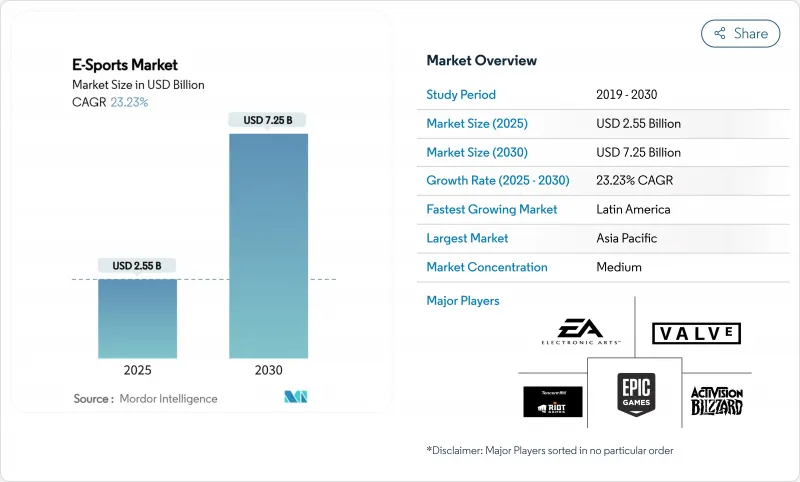

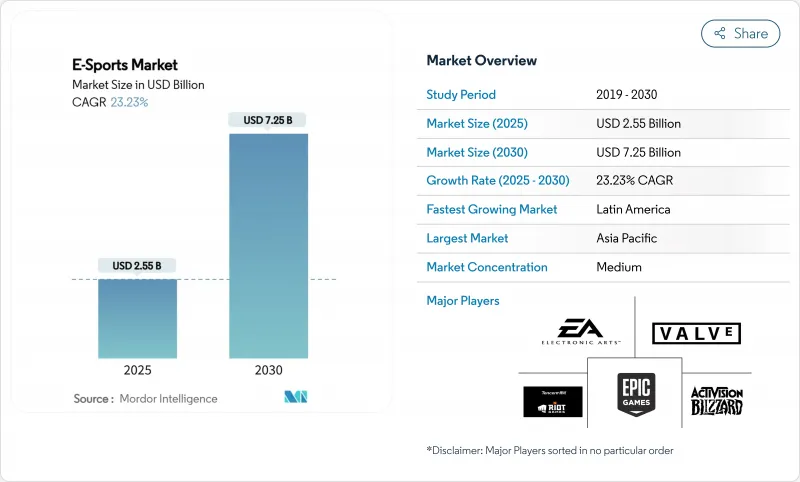

e스포츠 시장 규모는 2025년에 25억 5,000만 달러로 추정되고, 2030년에는 72억 5,000만 달러에 이를 것으로 예측되며, CAGR 23.23%로 확대될 전망입니다.

아시아태평양의 견고한 디지털 인프라, 퍼블리셔가 운영하는 프랜차이즈 리그의 성숙, 게임 내 수익화 증가가 톱 라인의 성장을 가속화하고 있습니다. 독점적 스트리밍 시청권 계약은 스폰서 의존이 완화되기 시작하더라도 시청자 규모를 예측 가능한 미디어 시청권 수익으로 꾸준히 전환하고 있습니다. 모바일 접근성, 블록체인 지원 자산 소유, 정부 자금 이니셔티브는 참여 및 수익 다양성을 확대하면서 장르 혁신, 특히 배틀 로얄 형식은 메인스트림 시청자를 유치하고 있습니다. 독립 토너먼트 운영자가 보다 공정한 지적재산권 조건을 요구하고, 퍼블리셔가 지배한 리그 구조에 압력을 가하면 경쟁의 역학이 변화하고 있습니다.

5G의 광범위한 도입으로 연결 속도가 크게 향상되고, 대기 시간이 단축되며 모바일 타이틀이 토너먼트급 경쟁 경험을 제공할 수 있습니다. Airtel과 같은 주요 통신 사업자는 평균 처리량이 크게 향상되었으며 청중의 비디오 품질과 게임 내 응답성이 향상되었다고 보고했습니다. 휴대 단말기의 보급이 진행됨에 따라, 이전에는 충분한 서비스를 받지 못했던 지방 도시와 2급 도시가 조직적인 플레이에 진입하게 되어, e스포츠 시장은 전통적인 도시의 중심지를 훨씬 넘어 확대하고 있습니다. 지역 커뮤니케이션 그룹은 게임 크레딧 경력 직접 결제, 데이터 번들 스폰서십, 공동 브랜드 토너먼트를 통해 증가액를 얻고 있습니다. 그 결과, 높은 서비스 품질이 참여를 촉진하고, 참여가 게임 내 지출을 증가시키며, 지출 증가가 게시자와 스폰서의 주목을 받는 선순환이 탄생합니다. 따라서 모바일 에코시스템 규모의 이점은 e스포츠 시장에서 결정적인 성장의 기둥이 되고 있습니다.

e스포츠의 모멘트, 스킨, 실적과 연관된 비대체성 토큰(NFTs)의 소유권을 확인할 수 있어 기업은 안심하고 거래할 수 있게 되는 동시에, 퍼블리셔는 2차 시장 거래에서 영속적인 충성도를 얻을 수 있습니다. 주요 타이틀 내의 파일럿 프로그램은 콜렉터블 드롭을 라이브 방송에 직접 통합하여 시청과 소비의 루프를 강화하고 있습니다. 주요 개발자들 사이에서 논의된 상호 운용성 기준은 자산이 여러 게임을 건너는 것을 허용하고, 사용자의 투자를 늘리며, 제품 수명주기를 연장할 수 있습니다. 초기 단계의 마켓플레이스에서는 이미 유동성이 높아지고 있어 희소 가치가 높은 프레스티지 오리엔티드인 디지털 아이템에 대한 수요가 높아지고 있는 것을 나타내고 있습니다. 대회 주최자에게는 블록체인 인프라가 상금 풀과 참가비 분배를 자동화하고 운영 오버헤드를 줄이며 분쟁을 줄입니다. 이 기술이 성숙하면 블록체인은 구조적으로 광고 주기에 좌우되기 어려운 새로운 수익원이 될 것으로 기대됩니다.

유럽의 브랜드 마케팅 담당자는 디지털 광고 성장이 느려지는 동안 예산을 단축하고 있습니다. 스폰서십은 2024년 수익의 60.27%를 차지했기 때문에 팀과 대회 운영자는 마케팅 지출 전환에 매우 민감합니다. 특히 패스트 푸드, 알코올, 도박 등 규제 강화로 활성화 캠페인이 복잡해지는 범주에서는 투자 대 효과에 대한 조사가 높아지고 있습니다. 따라서 라이츠 홀더는 미디어 권리 경매 및 게임 내 아이템 판매를 통해 수입을 분산시켜 변동성을 완화하고 있습니다. 그러나 대체 소스를 획득하기 위해서는 시청자의 가치를 입증하기 위한 데이터 분석을 강화해야 하며, 규모가 작은 기업에게는 압박이 됩니다. 그러므로 유럽에서 e스포츠 시장의 단기 성장은 스폰서십 비율이 균형을 되찾을 때까지 세계 평균보다 낮을 수 있습니다.

e스포츠 시장은 스폰서십에서 2024년 수익의 60.27%를 창출했는데, 플랫폼이 독점 컨텐츠에 프리미엄을 지불하고 있기 때문에 미디어 라이츠 라인의 확대가 가속화되고 있습니다. 미디어 라이츠로 인한 e스포츠 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 19.8%로 확대되어 스폰서십과의 차이가 서서히 줄어들 것으로 예측됩니다. 대회 주최자는 현금 흐름을 안정시키고 이벤트 예산 편성 위험을 줄이는 다년간 방송 계약에서 이익을 얻고 있습니다. 한편, 게시자는 게임 클라이언트에 라이브 스트림 창을 통합하여 시청을 마이크로트랜잭션에 연결하는 즉시 구매 프롬프트를 제공합니다. 게시자와 수익 공유 계약을 맺은 팀은 이러한 매출을 얻어 외부 브랜드 계약에 대한 의존도를 완화할 수 있습니다. 동시에 시청 및 수익 토큰과 라이브 베팅 오버레이와 같은 실험적 수익 형태도 평가됩니다. 수입원의 다양화는 e스포츠 시장이 성숙한 스포츠 시설에 전형적인 균형 잡힌 구성으로 전환하고 있음을 시사합니다.

미디어 저작권 증가는 제작의 질에도 상승 압력을 가하고 있습니다. 고해상도 피드, 다국어 설명, 실시간 통계 오버레이는 시청 기준을 높이고 스튜디오 및 가상현실 단계에 자본 지출을 촉구합니다. 이러한 투자는 미래의 권리 주기에서 협상력을 강화합니다. 소규모 주최자에게는 풀링된 프로덕션 허브와 프랜차이즈된 이벤트 서킷이 경쟁력을 유지하기 위한 비용 분배 경로를 제공합니다. 이러한 변화를 종합하면 예측 기간이 끝날 때까지 e스포츠 시장의 수익 계층 구조가 재구성될 가능성이 높습니다.

Twitch는 2024년 e스포츠 시장의 시청 시간 점유율로 74.89%를 차지했으며, 선행자 커뮤니티 도구와 제작자와의 깊은 관계에 힘입었습니다. 그러나 YouTube Gaming은 검색과 하이라이트 반복 기능과의 긴밀한 통합으로 2030년까지 CAGR 24.38%로 성장할 전망이며 시청량의 차이를 줄입니다. Huya와 DouYu와 같은 지역 특화형 서비스는 중국 내에서 많은 시청자를 획득하고 있으며, Nimo TV는 현지화된 언어 지원이 시청 시간을 증가시키는 동남아시아에서 지지를 받고 있습니다. 플랫폼 경쟁의 중심은 대기 시간 단축, 클립 작성의 용이성, 제작자의 수익 창출률입니다. 프리미엄 스포츠 경쟁과 마찬가지로 주요 토너먼트 독점 계약은 가입자 증가를 촉진합니다. 컨텐츠 권리가 각 서비스 간에 세분화됨에 따라 시청자는 소셜 개요과 집계된 결과 대시보드에 의존하게 되어 트래픽 예측이 복잡해지고 있습니다.

상업적인 관점에서 플랫폼은 애드쉐어와 칩 이코노미의 하이브리드 모델을 채용해 상위 1% 이외의 인플루언서를 끌어들이려고 합니다. 스트림 중에 상품 및 티켓을 구매할 수 있는 네이티브 전자상거래 위젯을 구현하여 수익을 늘릴 수 있습니다. Amazon MGM Studios가 주요 다큐멘터리 시리즈를 제작하는 것처럼 전통적인 미디어 플레이어가 이 싸움에 진입하면 메인스트림 스폰서를 획득할 수 있는 배달 레인이 늘어납니다. 그 결과, 멀티플랫폼 환경은 주최자에게 협상의 유연성을 제공하지만, 회복을 방지하기 위해 고급 권리 관리가 요구됩니다. 전반적으로 이러한 역학은 플랫폼의 다양성을 e스포츠 시장의 구조적 특징으로 강화합니다.

e스포츠 시장은 수익 모델별(미디어 라이츠, 광고 및 스폰서십 등), 스트리밍 플랫폼별(Twitch, Youtube Gaming 등), 디바이스 유형별(PC, 모바일 및 핸드헬드, 콘솔), 게임 장르별(MOBA, FPS 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 수익의 57.3%를 창출하였고, e스포츠 시장의 핵심으로 자리매김했습니다. 통신 사업자 주도의 5G 투자, 경기장 건설에 대한 정부 보조금, 주류 엔터테인먼트로서의 게임의 문화적 수용이 이 주도권을 유지하고 있습니다. 한국과 같은 국가는 학업 e스포츠 리그를 제도화하고 안정적인 인재 파이프라인을 확보하는 한편, 중국의 지자체 보조금은 디지털 스포츠 전용 파크에 기업 집적을 촉구하고 있습니다. 이 지역의 모바일 퍼스트 인구 통계는 캐주얼 플레이에서 e스포츠 시청으로의 평균을 초과하는 전환을 지원하며, 디지털 아이템 판매 및 토너먼트 티켓 판매를 통해 생태계 자체 자금 조달을 강화하고 있습니다. 이러한 구조적 이점은 1인당 참여도를 지속적으로 높이고 있으며, 게시자의 세계 컨텐츠 전략에 있어 이 지역은 필수적인 존재가 되고 있습니다.

북미는 e스포츠 시장에서 가장 성숙한 프랜차이즈 리그 인프라를 자랑합니다. 고액의 프랜차이즈 수수료가 지속성과 수익 공유에 참여할 수 있게 하고 NBA와 NFL 출신의 소유자 그룹을 끌어들이고 있습니다. 이러한 구성은 강력한 머천다이징과 스폰서십 패키지를 홍보하는 반면, 특정 회로 전체에서 4억 달러로 추정되는 이연 수수료 부채는 하위 순위 팀의 지급 능력에 의문을 제기하고 있습니다. 또한 게시자의 수익이 다양해지면서 헤드라인 노출이 줄어들고 전리품 구조에 대한 규제 모니터링이 복잡해지고 있습니다. 홈 앤 어웨이 방식 등의 운영 혁신은 지역 밀착형 팬 기반과 실험적인 시도이지만 팀의 흑자화에는 비용 제어가 필수적입니다.

라틴아메리카는 2030년까지 연평균 복합 성장률(CAGR)이 19.2%로 주요 지역 중 가장 빨라질 것으로 예측되며, 이는 광대역 보급률 향상과 젊고 모바일 중심 시청자들에게 지원되고 있습니다. 브라질은 이 지역의 총 상금과 시청자 수를 독점하고 있으며, 포르투갈어 방송과 지역 스폰서 로스터에 대한 브랜드 투자가 효과적입니다. 경제적 변동과 환율 변동으로 인해 사용자 1인당 평균 소비가 줄어들었지만 세계 게시자는 가격에 민감하게 반응하는 마이크로트랜잭션 번들과 유연한 구독 계층을 조정합니다. 이러한 적응은 단위당 마진을 손상시키지 않고 퍼널의 도달 범위를 넓히고 대륙 전체의 e스포츠 시장의 기세를 유지합니다.

유럽의 규제 모자이크는 독특한 궤도를 형성합니다. 프랑스와 같은 각국 정부는 보조금과 행사 개최에 대한 인센티브를 할당하고 있지만, 광고와 도박에 관한 법률이 다르기 때문에 국경을 넘어선 토너먼트의 조화는 늦어지고 있습니다. 웨일즈 개발 계획은 e스포츠의 혁신 허브를 통한 경제 다양화를 목표로 한 국가 전략을 보여줍니다. 최저 급여의 의무화 및 건강보험 등 선수 복지 기준이 주목되어 비용 구조에 영향을 주고 있습니다. 유럽의 시청자는 다국어를 소비하기 때문에 시장에 대한 침투를 목표로 하는 방송국에 있어서, 현지화에 대한 투자는 양도할 수 없습니다. 장기적으로 유럽의 구조적 접근은 상업적 실험을 약간 지연시킬 수 있지만, 선수들의 보호 및 방송 전문성을 강화할 가능성이 높습니다.

The E-Sports market size is estimated at USD 2.55 billion in 2025 and is forecast to reach USD 7.25 billion by 2030, expanding at a 23.23% CAGR.

Robust digital infrastructure in Asia-Pacific, the maturation of publisher-run franchise leagues, and rising in-game monetization are accelerating top-line growth. Exclusive streaming-rights deals are steadily converting audience scale into predictable media-rights income, even as sponsorship dependence begins to ease. Mobile accessibility, blockchain-enabled asset ownership, and government funding initiatives are widening participation and revenue diversity, while genre innovation, especially battle-royale formats, continues to draw mainstream viewers. Competitive dynamics are shifting as independent tournament operators demand fairer intellectual-property terms, placing pressure on publisher-controlled league structures.

Widespread 5G deployment is materially raising connection speeds and lowering latency, allowing mobile titles to deliver tournament-grade competitive experiences. Large operators such as Airtel report meaningful uplifts in average throughput, which improves spectator video quality and in-game responsiveness . As handset penetration climbs, previously under-served rural and tier-two cities gain entry to organized play, expanding the esports market well beyond traditional urban hubs. Regional telecommunications groups are capturing incremental value through direct-carrier billing for game credits, data-bundle sponsorship, and co-branded tournaments. The result is a virtuous cycle: higher service-quality drives engagement, engagement boosts in-game spend, and elevated spend draws more publisher and sponsor attention. The mobile ecosystem's scale advantage is therefore becoming a decisive growth pillar for the esports market.

Verifiable ownership of non-fungible tokens (NFTs) tied to esports moments, skins, and achievements gives players the confidence to trade securely while rewarding publishers with perpetual royalties on secondary-market transactions. Pilot programs inside major titles now embed collectible drops directly into live broadcasts, tightening the loop between viewing and spending. Interoperability standards under discussion among leading developers could allow assets to traverse multiple games, deepening user investment and extending product life cycles. Early-stage marketplaces already show robust liquidity, signaling pent-up demand for scarce, prestige-oriented digital items. For tournament organizers, blockchain infrastructure automates distribution of prize pools and appearance fees, cutting operational overhead and reducing disputes. As the technology matures, blockchain promises to anchor an additional revenue stream that is structurally less exposed to advertising cycles.

European brand marketers are tightening budgets as broader digital advertising growth decelerates. Because sponsorship still represents 60.27% of 2024 revenue, teams and tournament operators remain highly sensitive to shifts in marketing outlay. Return-on-investment scrutiny is rising, especially in categories such as fast food, alcohol, and gambling where tightening regulations complicate activation campaigns. Rights holders are therefore diversifying income through media-rights auctions and in-game item sales to buffer volatility. However, capturing alternative sources requires stronger data analytics to demonstrate audience value, pressuring smaller entities that lack scale. Near-term growth of the esports market in Europe may therefore trail global averages until sponsorship ratios rebalance.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The esports market generated 60.27% of its 2024 revenue from sponsorship, but the media-rights line is scaling faster as platforms pay premiums for exclusive content. The esports market size attributable to media rights is forecast to expand at a 19.8% CAGR through 2030, gradually narrowing the gap with sponsorship. Tournament organizers benefit from multi-year broadcast deals that stabilize cash flow and de-risk event budgeting. Meanwhile publishers integrate live-stream windows within game clients, enabling instant purchase prompts that link viewing to micro-transactions. Teams aligned with publishers through revenue-share agreements gain exposure to these sales, easing dependence on external brand deals. At the same time, experimental revenue formats, such as view-and-earn tokens or live-betting overlays, are under evaluation. The growing diversity of income sources signals an esports market migrating toward the balanced mixes typical of mature sports properties.

Media-rights growth also exerts upward pressure on production quality. High-definition feeds, multi-language commentary, and real-time statistics overlays elevate viewing standards, prompting capital expenditure on studios and virtual-reality stages. These investments strengthen negotiation leverage in future rights cycles. For smaller organizers, pooled production hubs and franchised event circuits offer a cost-sharing route to remain competitive. Collectively, these shifts are likely to recalibrate the revenue hierarchy within the esports market by the end of the forecast window.

Twitch dominated 2024 with a 74.89% slice of the esports market share in viewing hours, underpinned by first-mover community tools and deep creator relationships. Yet YouTube Gaming's tighter integration with search and highlight-repeat functions positions it for a 24.38% CAGR through 2030, closing the volume gap. Region-specific services such as Huya and DouYu aggregate large domestic audiences in China, while Nimo TV gains traction in Southeast Asia where localized language support wins incremental watch-time. Platform competition centers on latency reduction, clip-creation ease, and monetization rates for creators. Exclusive deals for marquee tournaments swing subscriber sign-ups, echoing competition in premium sports. As content rights fragment across services, viewers increasingly rely on social snippets and aggregated results dashboards, complicating traffic forecasts.

From a commercial standpoint, platforms are adopting hybrid ad-share and tip-economy models to attract influencers outside the top 1% percentile. Implementation of native e-commerce widgets, allowing merchandise or ticket purchase during streams, broadens revenue capture. Traditional media firms entering the fray illustrated by Amazon MGM Studios' production of documentary series around majors-inject additional distribution lanes that can unlock mainstream sponsors. The resulting multi-platform environment provides organizers with negotiation flexibility but demands sophisticated rights-management to prevent cannibalization. Overall, these dynamics reinforce platform diversity as a structural feature of the esports market.

E-Sports Market is Segmented by Revenue Model (Media Rights, Advertising and Sponsorship, and More), Streaming Platform (Twitch, Youtube Gaming, and More), by Device Type (PC, Mobile/Handheld, Console), Game Genre (MOBA, First-Person Shooter (FPS) and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated 57.3% of 2024 revenue, positioning it as the cornerstone of the esports market. Carrier-led 5G investment, government subsidies for arena construction, and cultural acceptance of gaming as mainstream entertainment sustain this leadership. Countries such as South Korea institutionalize scholastic esports leagues, ensuring a steady talent pipeline, while China's municipal grants encourage corporate clustering around dedicated digital-sports parks. The region's mobile-first demographics underpin above-average conversion from casual play to esports viewership, reinforcing ecosystem self-finance through digital item sales and tournament ticketing. These structural advantages support persistently high per-capita engagement, making the region indispensable for publishers' global content strategies.

North America showcases the most mature franchise-league infrastructure inside the esports market. High franchise fees buy permanency and revenue-share participation, drawing ownership groups from NBA and NFL backgrounds. While this configuration fosters robust merchandising and sponsorship packages, deferred fee obligations estimated at USD 400 million across certain circuits raise solvency questions for lower-ranked teams. Regulatory oversight around loot-box mechanics adds complexity, though diversified publisher revenue mitigates headline exposure. Operational innovations such as home-and-away formats are experimenting with localized fan bases, but cost-control remains pivotal to returning teams to profitability.

Latin America is projected to deliver a 19.2% CAGR through 2030, the fastest among major regions, buoyed by improving broadband coverage and a youthful, mobile-centric audience. Brazil dominates regional prize pools and viewership, validating brand investment in Portuguese-language broadcasts and locally-sponsored rosters. Economic volatility and currency swings temper average spend per user, yet global publishers increasingly tailor price-sensitive micro-transaction bundles and flexible subscription tiers. These adaptations widen funnel reach without compromising per-unit margins, sustaining momentum for the esports market across the continent.

Europe's regulatory mosaic shapes a distinct trajectory. National governments such as France allocate grants and event-hosting incentives, but cross-border tournament harmonization lags due to divergent advertising and gambling laws. The Welsh development plan illustrates sub-national strategies aimed at economic diversification through esports innovation hubs. Player-welfare standards, including minimum-salary mandates and health coverage, gain prominence, influencing cost structures. Because European audiences consume multiple languages, localization investment is non-negotiable for broadcasters seeking market penetration. Over time, Europe's structured approach is likely to strengthen athlete protections and broadcasting professionalism, though it may marginally slow commercial experimentation.