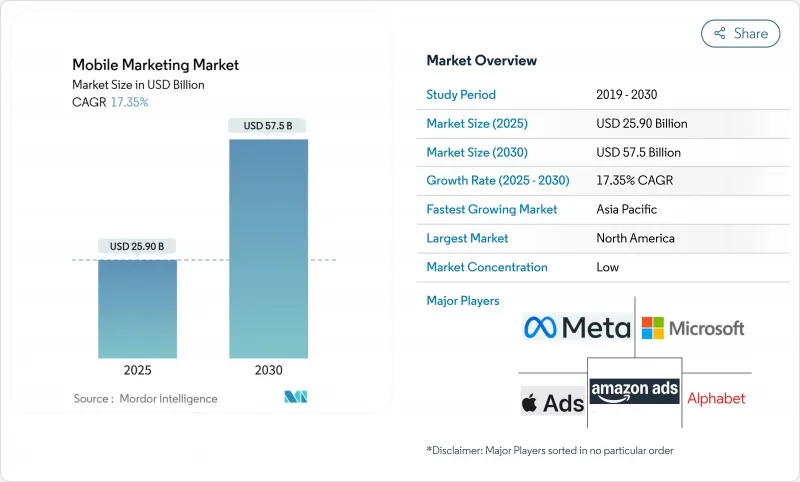

모바일 마케팅 시장 규모는 2025년에 259억 달러로 평가되었고, 2030년에 575억 3,000만 달러로 상승할 것으로 예측되며, 예측 기간 중 CAGR은 17.35%를 나타낼 전망입니다.

발견, 평가, 구매 과정이 지속적으로 휴대용 화면으로 이동하면서 스마트폰은 상거래, 미디어, 고객 서비스의 기본 진입점이 되었습니다. 이에 광고주들은 신원 확인, 동의 관리, 크리에이티브 자동화가 하나의 워크플로 내에서 통합되는 데이터 중심의 참여 순간으로 예산을 전환하고 있습니다. 이러한 기능을 단일 사용자 인터페이스 아래 통합한 플랫폼 제공업체들은 브랜드 팀이 도구 간 전환 없이 여정을 테스트, 측정, 최적화할 수 있기 때문에 점진적인 지출 증가를 이끌어내고 있습니다. 아시아태평양 지역의 20% CAGR은 5G 커버리지, 디지털 지갑, 슈퍼앱 생태계의 복합적 효과를 시사하는 반면, 유럽의 엄격한 개인정보 보호 규정은 마케터들이 1인칭 데이터 자산과 폐쇄형 측정 체계를 강화하도록 압박하고 있습니다.

서버 측 이벤트 수집 및 동의 기반 기기 토큰이 미국 주요 퍼블리셔들 사이에서 브라우저 수준 쿠키를 대체하고 있습니다. 이러한 프레임워크를 도입한 브랜드들은 매칭률에서 두 자릿수 개선을 보고하며, 주(州) 차원의 개인정보 보호 의무를 충족하면서도 더 풍부한 세분화를 가능케 합니다. 동일한 메커니즘이 규정 준수 보고를 자동화하여 재무팀이 기술 투자로서 개인정보 보호 업그레이드를 활용할 수 있게 합니다. 따라서 마케팅 및 리스크 부서가 공유 지표에 맞춰 협력하고, 광고주는 규제가 강화되는 상황에서도 개인화된 접근을 지속할 수 있습니다. 이러한 성과는 규정 준수형 신원 확인이 비용 센터가 아닌 성장 가속기로 자리매김하고 있음을 입증합니다.

상용 5G 네트워크가 아시아 주요 도시 대부분을 커버하며 모바일 동영상 평균 로딩 시간을 100밀리초 미만으로 단축했습니다. 마케터들은 이에 대응해 사용자가 가상 환경에 상품을 배치해 본 후 원터치 결제가 가능한 인터랙티브 증강현실(AR) 제품 데모를 선보이고 있습니다. 2024년 서울 게임 컨벤션에서 네트워크 엣지에서 실시간 A/B 전환을 실행한 결과, 동일 크리에이티브를 4G에서 실행했을 때 대비 이탈률이 약 25% 감소했습니다. 이 경험은 대역폭이 단순한 배포 업그레이드 기능을 넘어 몰입형 스토리텔링을 촉진하는 창의적 캔버스 역할을 한다는 점을 보여줍니다. 5G가 더욱 밀집화됨에 따라 모바일 마케팅 시장은 더욱 풍부한 자산 형식과 높은 전환 효율성을 경험하게 될 것입니다.

주류 브라우저에서 서드파티 쿠키가 사라지면서 크로스디바이스 그래프가 축소되고, 마케터들은 확률적 측정과 증분 효과 실험으로 전환되고 있습니다. 사용자 수준 보고서에 의존하던 재무 관리자들은 이제 인과적 기여도에 초점을 맞춘 리프트 기반 대시보드로 전환 중입니다. 학습 주기는 길어지지만, 확률적 신호가 개인정보 변동성을 견디므로 예산 배분은 점차 안정화됩니다. 성과 기반 마케터들은 단기적 마찰을 겪지만, 이러한 전환은 궁극적으로 더 탄력적인 기획 프로세스를 만들어 모바일 마케팅 시장을 향후 규제 변동으로부터 보호합니다.

플랫폼 소프트웨어는 2024년 매출의 67%를 차지하며 모바일 마케팅 시장의 운영 핵심 기반으로서의 지위를 확고히 했습니다. 공급업체들은 엔지니어링 지원 없이도 브랜드 팀이 실시간에 가까운 상태로 규칙을 테스트할 수 있는 로우코드 여정 빌더와 프라이버시 대시보드를 내장하고 있습니다. 서비스 라인은 규모는 작지만, 기업들이 클린룸 구축, 크리에이티브 자동화 및 지역별 규제에 대한 지침을 요구함에 따라 더 빠르게 확장되고 있습니다. 자문 업무는 미디어 차익 거래에서 기술 지원으로 전환되며, 새로운 수수료 풀을 창출하고 공급망 전반에 걸쳐 가치 포착을 재조정하고 있습니다. 예측 기간 동안 소프트웨어 업그레이드는 고객 유지율을 유지할 것이며, 서비스 계약은 고객 락인을 심화시킬 것입니다.

기술 서비스는 또한 광고주와 퍼블리셔 간의 복잡한 데이터 공유 계약을 중재하여 동의 기반 식별자 채택을 원활하게 합니다. 기술과 전문성에 대한 이중 수요는 하이브리드 제공업체가 더 큰 지갑 점유율을 확보할 수 있는 위치에 놓이게 합니다. 결과적으로, 소프트웨어가 주도적 점유율을 유지하는 가운데 구성 요소 서비스와 연계된 모바일 마케팅 시장 규모는 전체 시장 성장률을 앞지를 것으로 전망됩니다.

위치 인텔리전스는 모바일 마케팅 시장 규모의 10% 중반을 차지하며 2030년까지 연평균 22% 성장률(CAGR)을 기록해 다른 솔루션 클러스터를 추월할 준비가 되어 있습니다. 향상된 스택은 GPS, 블루투스 비콘, 장소별 Wi-Fi를 결합하여 미터 단위 이하의 정확도로 쇼핑객 체류 구역을 특정합니다. 순간 맞춤형 제안은 일반 쿠폰보다 사용률과 장바구니 가치 지표에서 우수한 성과를 보입니다. QR 코드는 진열대와 화면을 연결하는 가교 기술로 재등장합니다. 2025년 베를린에서 진행된 청량음료 프로모션은 병뚜껑 하단의 일련번호 코드를 활용해 소비자를 즉시 보상이 제공되는 모바일 게임으로 유도했습니다.

푸시 알림은 여전히 높은 열람률로 필수적이지만, 오케스트레이션 엔진이 예측된 피로도에 따라 발송 빈도를 조절해 수신 거부율을 방지합니다. 리테일러가 알림에 리치 미디어를 접목함에 따라 위치 신호는 타이밍을 더욱 정밀하게 조정해 참여도를 높이고 사용자당 지출을 증가시킵니다. 매핑 API, 분석, 크리에이티브 툴링을 단일 인터페이스에 통합한 공급업체들은 경쟁 우위를 확대하고 모바일 마케팅 시장 내 점유율을 높일 것입니다.

모바일 마케팅 시장은 구성 요소별(플랫폼, 서비스), 솔루션 유형별(모바일 웹, SMS 및 MMS, 기타), 유통 채널별(소셜 미디어 마케팅, 제휴 마케팅, 기타), 기업 규모별(대기업, 중소기업), 전개 형태별(클라우드, 온프레미스), 최종 사용자 산업별(소매 및 전자상거래, T&T) 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 매출의 38%를 차지하며 광고 기술 혁신의 시험장 역할을 강조했습니다. 주별 개인정보 보호법 개정으로 퍼스트파티 데이터 프로그램이 가속화되어 더 높은 매칭률과 규정 준수형 신원 그래프를 이끌어냈습니다. 이벤트 등급 위치 플랫폼은 2028년 로스앤젤레스 올림픽을 앞두고 등장하여 티켓팅, 매점, 스폰서 메시지를 통합된 모바일 흐름으로 결합합니다. 2024년 미식축구 플레이오프 기간 중 실시된 시험 운영에서 매점 대기 시간에 맞춰 제공된 동적 오퍼는 방문객 수 증가 없이 1인당 지출을 증가시켜 미디어 가치 이상의 운영적 이점을 보여주었습니다. 퍼블리셔들이 개인정보 보호형 ID 통합을 서두르면서 벤처 투자는 안정세를 유지하며 광범위한 모바일 마케팅 시장을 지원하고 있습니다.

아시아태평양 지역은 5G 속도, 슈퍼앱 생태계, 소셜 커머스 규범의 복합적 효과로 20% 연평균 성장률(CAGR)을 기록할 전망입니다. 2024년 동남아시아 주요 슈퍼앱 내 화장품 캠페인은 증강현실 체험과 채팅 내 결제 기능을 결합해 구매 과정을 60초 미만으로 단축하고 단위 판매량을 3배 증가시켰습니다. 인도에서는 지역어 음성 검색이 도달 범위를 확대하며, 플랫폼 운영사들이 문해율이 낮은 계층을 위한 음성 기반 광고 형식을 출시하도록 촉진하고 있습니다. 이러한 혁신은 기술 준비도만큼이나 문화적 습관에 따라 채택 곡선이 달라진다는 점을 입증합니다. 빠른 스마트폰 교체 주기와 낮은 데이터 비용은 모바일 마케팅 시장을 더욱 확장시킵니다.

유럽의 엄격한 개인정보 보호법은 쿠키 기반 도달을 제한하지만, 소매업체들은 폐쇄형 리테일 미디어 네트워크를 통해 로열티 프로그램을 수익화함으로써 대응하고 있습니다. 2025년 네덜란드 식료품 체인은 공급업체가 스폰서 제품 타일을 구매해 체인의 모바일 지갑으로 확장되는 셀프서비스 포털을 출시했습니다. 이를 통해 며칠 내로 종단간 어트리뷰션이 가능해졌습니다. 규모는 작지만 북유럽 국가들은 유럽 최고 수준의 사용자당 모바일 참여율을 기록하며, 소비자 신뢰가 확보될 때 개인정보를 존중하는 개인화가 번창함을 입증했습니다. 규제 명확성은 단기 성장을 저해하지만 장기적 안정성을 조성하여 해당 지역 전반에 걸친 모바일 마케팅 시장의 꾸준한 확장을 뒷받침합니다.

The mobile marketing market size is valued at USD 25.9 billion in 2025 and is forecast to climb to USD 57.53 billion by 2030, advancing at a 17.35% CAGR during the outlook period.

Continuous migration of discovery, evaluation, and purchase to handheld screens has turned smartphones into the default entry point for commerce, media, and customer service. Advertisers are therefore diverting budgets toward data-rich engagement moments where identity resolution, consent management, and creative automation converge inside one workflow. Platform providers that integrate these functions under a single user interface are winning incremental spend, because brand teams can test, measure, and optimise journeys without toggling between tools. Asia-Pacific's 20% CAGR signals the compounding effect of 5G coverage, digital wallets, and super-app ecosystems, while Europe's stringent privacy rules push marketers to fortify first-party data assets and closed-loop measurement.

Server-side event collection and consented device tokens are replacing browser-level cookies across major United States publishers. Brands embedding these frameworks report doubled-digit improvements in match rates, enabling richer segmentation while meeting state-level privacy mandates. The same mechanisms automate compliance reporting, allowing finance teams to capitalise on privacy upgrades as technology investments. Marketing and risk units, therefore, align on shared metrics, and advertisers can sustain personalised outreach even as regulations tighten. These gains validate that compliant identity resolution is becoming a growth accelerator rather than a cost centre.

Commercial 5G networks now serve most tier-one Asian cities, pushing average mobile video load times well below 100 milliseconds. Marketers respond with interactive augmented-reality product demos that let users virtually place items in their environment before one-tap checkout. Live A/B switches executed at the network edge during a 2024 gaming convention in Seoul cut abandonment by nearly 25% versus identical creative on 4G. The experience reveals that bandwidth acts as a creative canvas, spurring immersive storytelling rather than functioning only as a distribution upgrade. As 5G densifies, the mobile marketing market will see richer asset formats and higher conversion efficiency.

Third-party cookies are vanishing from mainstream browsers, shrinking cross-device graphs, and forcing marketers toward probabilistic measurement and incrementality experiments. Finance controllers who relied on user-level reports now train on lift-based dashboards focused on causal contribution. Learning cycles lengthen, yet budget allocations gradually stabilise because probabilistic signals tolerate privacy volatility. While performance marketers face near-term friction, the shift ultimately produces more resilient planning processes, cushioning the mobile marketing market against future regulatory swings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Platform software contributed 67% of 2024 revenue, affirming its status as the operating backbone of the mobile marketing market. Vendors embed low-code journey builders and privacy dashboards that let brand teams test rules in near real time without engineering support. Services lines, though smaller, are expanding faster as enterprises seek guidance on clean-room deployment, creative automation and regional regulations. Advisory practices pivot from media arbitrage to technical enablement, carving fresh fee pools and rebalancing value capture along the supply chain. Over the forecast horizon, software upgrades will sustain retention, while service engagements deepen customer lock-in.

Technical services also mediate complex data-sharing agreements between advertisers and publishers, smoothing the adoption of consented identifiers. This dual need for technology and expertise positions hybrid providers to harvest greater wallet share. As a result, the mobile marketing market size tied to component services is projected to outpace overall market growth, even as software retains lead share.

Location intelligence holds a mid-teen fraction of the mobile marketing market size and is poised for a 22% CAGR, eclipsing other solution clusters by 2030. Enhanced stacks blend GPS, Bluetooth beacons, and venue Wi-Fi, pinpointing shopper dwell zones with sub-metre accuracy. Moment-specific offers then outperform generic coupons on redemption and basket value metrics. QR codes re-emerge as bridge technology between shelf and screen; a 2025 soft-drink promotion in Berlin used under-cap serialised codes to funnel consumers into a mobile game with instant rewards.

Push alerts remain indispensable for their superior open rates, but orchestration engines throttle frequency against predicted fatigue to prevent opt-outs. As retailers embed rich media into these alerts, location signals further sharpen timing, deepening engagement, and raising spending per user. Providers that integrate mapping APIs, analytics, and creative tooling within one interface widen their moat and expand their share within the wider mobile marketing market.

Mobile Marketing Market is Segmented by Component (Platform, Services), Solution Type (Mobile Web, SMS and MMS, and More), Distribution Channel (Social Media Marketing, Affiliate Marketing, and More), by Enterprise Size (Large Enterprises, Smes), Deployment Mode (Cloud, On-Premises), by End-User Industry (Retail and E-Commerce, Media and Entertainment / OTT), Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 38% of 2024 revenue, underscoring its role as a test bed for ad-tech innovation. State privacy amendments accelerate first-party data programs, leading to higher match rates and compliant identity graphs. Event-grade location platforms emerge ahead of the 2028 Los Angeles Olympics, merging ticketing, concessions, and sponsor messaging into unified mobile flows. Trials during the 2024 football playoffs demonstrated that dynamic offers aligned with concession wait times raised per-capita spend without adding foot traffic, showing operational upside beyond media value. Venture investment remains steady as publishers race to integrate privacy-safe IDs, supporting the broader mobile marketing market.

Asia-Pacific is forecast to post a 20% CAGR, reflecting the compounding effect of 5G speed, super-app ecosystems, and social commerce norms. A 2024 cosmetics campaign inside a leading Southeast Asian super-app combined augmented-reality try-ons with in-chat checkout, shrinking purchase journeys to under 60 seconds and tripling unit sales. In India, vernacular voice search expands reach, prompting platform owners to launch speech-driven ad formats for low-literacy segments. These innovations confirm that adoption curves depend on cultural habits as much as technology readiness. Rapid smartphone replacement cycles and low data costs further expand the mobile marketing market.

Europe's stringent privacy statutes restrict cookie-based reach, but retailers counter by monetising loyalty programs through closed-loop retail media networks. A 2025 Dutch grocery chain launched a self-service portal where suppliers buy sponsored product tiles that extend into the chain's mobile wallet, enabling end-to-end attribution within days. Nordic countries, although smaller, record the continent's highest per-user mobile engagement, proving that privacy-respecting personalisation thrives when consumer trust is secured. Regulatory clarity dampens short-term growth yet fosters long-term stability, supporting steady expansion of the mobile marketing market across the region.