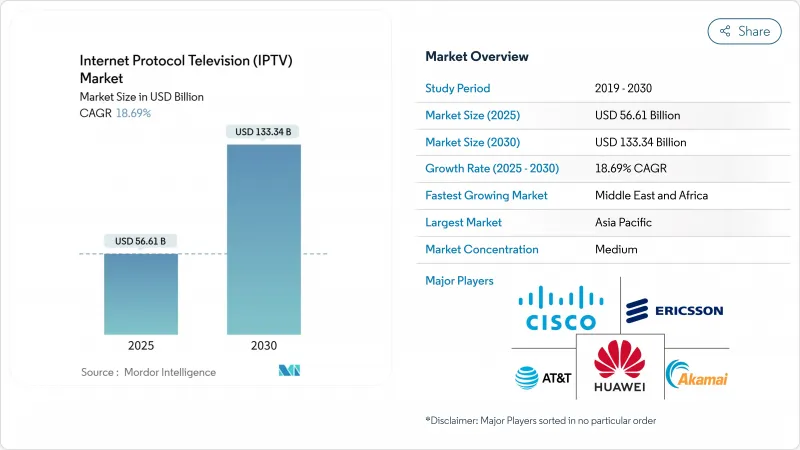

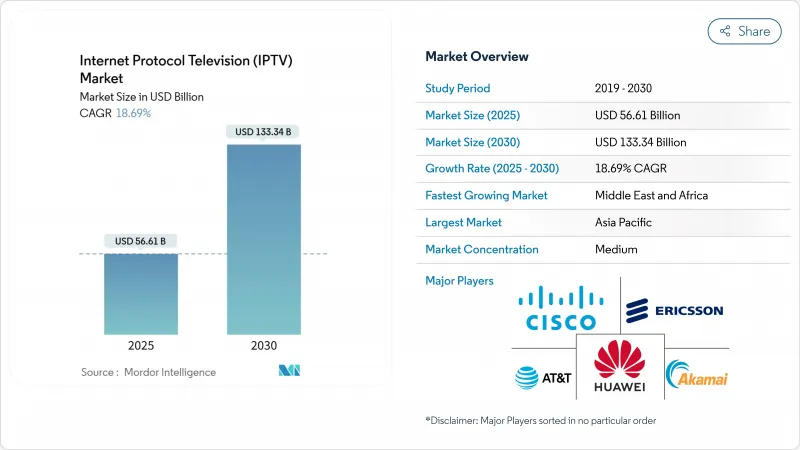

인터넷 프로토콜 TV(IPTV) 시장 규모는 2025년에 566억 1,000만 달러, 2030년에는 1,333억 4,000만 달러에 이르고, 예측 기간 중 CAGR은 18.69%를 나타낼 전망입니다.

파이버 투 더 홈(FTTH)의 보급, 4K/8K 비디오에 대한 의욕이 높아지고, 하이브리드 가입자와 광고 모델이 일체가 되어 다음 수요층을 파내고 성공의 척도를 가입자 증가에서 전달 1메가비트당 시청 시간 증가로 이행시킵니다. 멀티캐스트 지원 아키텍처를 통한 전송 비용 절감은 대략적인 이자율을 늘리고, 연결된 TV 광고 삽입은 엔트리 레벨 계획에서 사용자 1인당 평균 수익을 높입니다. 이미 고밀도 파이버 실적를 소유하고 있는 사업자는 가구가 지연이 없는 초고해상도 스트림을 경험할 때 프리미엄 레이어 캡처가 가속된다고 보고합니다.

미국 사업자는 2024년에 1,200만 가구의 FTTH를 신규로 부설했고, 일본, 한국, 독일 사업자는 대도시권 전체에 대칭적인 기가비트 커버리지를 확대했습니다. 파이버 광대역 어소시에이션은 기존의 파이버는 35년의 수명으로 초당 600테라비트에 대응해, 소비자용 비디오의 라스트마일의 제약을 없앨 수 있다고 지적하고 있습니다. 그 결과 스트리밍 공급자는 고객을 프리미엄 번들에 고정하는 8K 스포츠와 HDR 네이처 다큐멘터리를 자신있게 제공하게 되었습니다. 일본의 한 통신 사업자는 10기가비트 플랜의 가구가 1기가비트 유저보다 32%나 많은 울트라 HD 시간을 스트리밍하고 있음을 밝혀 대역폭과 참여가 직결되어 있음을 증명했습니다. 2025년에 아시아태평양에서 25G와 50G PON이 도입되면 볼루메트릭 비디오와 홀로그래픽 비디오의 기반이 갖추어지며 오늘날의 설비투자가 미래의 몰입형 포맷에 대한 보험으로 바뀌게 됩니다.

서유럽의 기존 기업은 2024년에 클라우드 네이티브 허브를 시작하여 국가 캐치업, 정액제 비디오 온 디맨드, 라이브 스포츠를 하나의 검색 레이어로 통합했습니다. 스페인에서는 신규 광대역 가구의 3분의 2가 60일 이내에 운영자 대시보드를 통해 적어도 하나의 타사 앱을 활성화하여 선형 광고 감소를 상쇄하는 홀세일 플랫폼 비용을 창출했습니다. 미국에서는 스트리밍 딜리버리 7개사의 과금 통합을 통해 광대역 요금을 인상하지 않고 사용자 1인당월4달러 증가를 달성했습니다. 지역 파이버 벤처는 턴키 어그리게이션 미들웨어 라이선스를 취득하고 레거시 케이블 박스를 구축하고 제한된 설비 투자에도 불구하고 IPTV 시장의 화제의 일각을 차지하게 되었습니다. 국부적으로 볼 때 발견의 편의성은 배달 파이프를 매장으로 변환하고 운영자는 컨텐츠 파트너를 늘릴 때마다 수익을 창출 할 수 있습니다.

소비자가 광대역 및 모바일 연결에 지출을 집중하고 채널 번들이 옵션 애드온으로 쫓겨나면서 북미 유료 TV 가구는 2024년에 추가로 4% 감소합니다. 스카이 브라질이 2024년 4월에 광섬유로 축발을 옮긴 것은 기존 사업자가 OTT 난립에 대한 유일한 헤지로서 인프라 소유권을 어떻게 생각하고 있는지를 돋보이게 합니다. 유럽의 케이블 그룹은 FTTH를 과도하게 구축하거나 동축을 DOCSIS 4.0으로 업그레이드하여 추종하고 있지만 가입자의 성장은 평평하게 유지됩니다. 고객의 가치는 낮은 지연 액세스로 이동하고 컨텐츠는 코어 드라이버가 아니라 업셀입니다. 사업자가 IP 전달의 경제성을 강화하지 않는 한 IPTV 시장은 총 시청 시간이 증가하더라도 ARPU가 정체될 위험이 있습니다.

사업자가 매니지드 오퍼레이션, 플랫폼 통합, 고객 지원을 아웃소싱하고 있기 때문에 2024년 IPTV 시장 규모의 61%를 서비스가 차지합니다. 컨텐츠 비용을 증가시키지 않고 시청 시간을 증가시키는 AI 주도의 개인화 엔진에 대한 예산이 증가하고 있습니다. 공급업체는 클라우드 네이티브 지원 데스크 및 예측 유지보수를 제공하여 해지 및 트럭 롤 비용을 절감합니다. 마진은 참여에 따라 다르므로 추천 알고리즘을 판매하는 서비스 파트너는 할인율을 요구합니다. IPTV 시장은 또한 보안, 분석 및 과금을 하나의 SLA로 통합하고 사업자가 광섬유 확장에 집중할 수 있도록 하는 통합업체에게도 보상을 제공합니다.

전송 및 인코딩 기기는 베이스는 작은 것, 4K 스포츠의 라이브 중계나 인터랙티브·오버레이에 저지연 에지 엔코더가 필수가 되기 때문에 2030년까지 연평균 복합 성장률(CAGR) 22.4%를 보일 것으로 예측됩니다. 운영자는 2025년 현장 업그레이드를 통해 소비자 게이트웨이에 멀티캐스트 모듈을 통합하여 비트 전송률을 손상시키지 않고 시간당 스트리밍 비용을 3분의 1로 줄일 수 있음을 배웠습니다. H.264에서 AV1, VVC로 코덱의 진화가 가속화되는 가운데, 펌웨어 업그레이드 가능성은 이제 판매 포인트가 되고 있습니다. 따라서 하드웨어 공급업체는 8K 채택이 증가하더라도 설비 투자를 유지할 수 있는 향후 설계를 시장에 투입하고 있습니다. 경쟁사와의 차별화는 규제 당국과 투자자들이 점점 주시하는 지표인 배달 기가비트당 전력 효율로 전환하고 있습니다.

2024년에는 IPTV 시장 점유율의 74.3%를 구독이 차지하지만, 이는 많은 가구가 여전히 광고가 없는 카탈로그나 번들된 스포츠 패스를 선호하기 때문입니다. 멀티 스크린 허용, 클라우드 DVR, 크로스 디바이스 재개는 특히 가족들 사이에서 지각 가치를 유지합니다. 사업자는 극장 공개 작품과 교환 가능한 스트리밍 크레딧을 제공함으로써 로열티 프로그램을 충실히 하여 월액제 OTT 라이벌로의 이행을 막고 있습니다. 하지만 같은 기업은 프리미엄 패키지와 카니버리 없이 낮은 예산 지향 시청자를 얻기 위해 저가의 광고 계층을 계속 도입하고 있습니다.

AVoD는 CAGR 28.7%로 급성장하고 있는 분야로, 가구 수준의 타겟팅과 쇼퍼블 게재위치를 지원하는 애드테크놀로지의 성숙이 그 원동력이 되고 있습니다. 2025년 1월 캐나다에서 실시된 한 식료품점 캠페인에서는 요리 프로그램 스트림 내에서 9%의 클릭연결율을 기록했으며 광고가 컨텐츠와 일치하는 경우 구매 의욕을 입증했습니다. 운영자는 수요 측 플랫폼을 미들웨어에 통합하여 단순한 캐리지 비용이 아닌 광고 수익의 직접적인 공유를 얻습니다. 페이퍼 뷰는 권투나 콘서트와 같은 주요 프로그램에는 여전히 유효하지만, 평생 가치를 극대화하기 위해 이벤트 방영권을 중급 구독 번들에 공급하는 경우가 늘고 있습니다. 원래 PPV의 마이크로 결제를 위해 만들어진 도구는 칩과 라이브 상거래를 위해 재사용되어 티켓뿐만 아니라 시청자 1인당 수익을 확대하고 있습니다.

IPTV 시장은 컴포넌트(하드웨어, 서비스), 수익 모델(구독 기반, 페이퍼뷰, 광고 지원), 스트리밍 유형(라이브/리니어 TV, 타임 시프트/리플레이 TV, 주문형 비디오), 디바이스/액세스 플랫폼(스마트 TV, 모바일/태블릿, PC/랩톱, 셋톱박스, 미디어 스트리머), 배포 방식(멀티캐스트 IPTV, 유니. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 IPTV 시장의 35.8%를 차지했으며, FTTH의 보급, 스마트폰의 높은 보급률, 다국어 라이브러리에 힘입어 수익을 독점했습니다. 중국의 플랫폼은 주요 스포츠의 베이징어와 광동어의 해설을 사이멀 방송하여 방영권료를 극대화하고 있습니다. 일본의 8K 위성 방송 시험 방송은 도시 지역의 광섬유 가구를 다운 샘플링 제로를 보장하는 프리미엄 플랜으로 유도했습니다. 인도 Tier-II 도시에서는월699루피(8.45달러)의 광섬유 + 로컬 OTT 팩이 채택되어 케이블 홈이 IP 생태계로 변환되었습니다. 하이퍼로컬 드라마는 타겟 광고에서 성공을 거두었으며 운송 비용이 낮아지면 문화적 특수성이 확장될 수 있음을 입증합니다.

중동 및 아프리카는 기반이 작지만 아날로그 방송 종료 기한과 저렴한 스마트폰이 수요를 자극하기 때문에 2030년까지 연평균 복합 성장률(CAGR)은 24.7%를 나타낼 전망입니다. 북아프리카의 한 방송국은 라마단의 드라마를 데이터 절약을 위해 480p로 스트리밍 전달해 120만명의 독특한 시청자를 모았습니다. 나이지리아의 오픈 액세스 회랑은 대역폭을 도매 가격으로 임대하고 멀티 캐스트 지원 라우터로 도시 전역의 Wi-Fi를 가능하게합니다. 케냐와 가나에서는 전통적인 케이블로 규모가 확대되지 않은 농촌 지역에서 광섬유 부설을 촉진하기 위한 정부 자금이 투입되고 있습니다. 가장 효과적인 해적판 대책 툴로서, 저렴하고 고품질의 스트리밍 서비스가 가장 효과적인 불법복제 방지 수단으로 떠오르고 있습니다.

북미와 유럽은 성숙하지만 슈퍼 어그리게이션 수수료와 연결된 TV 광고를 통한 수익화가 계속되고 있습니다. 북유럽의 광섬유 협동조합은 기가비트 액세스와 4개의 인디 스트리머를 번들하여월54.90유로(60.14미국)로 제공. 미국의 통신사업자는 제로레이팅을 모바일 플랜에 활용하고, 가구수의 신장 고민에도 불구하고 가입자를 유지하고 있습니다. 라틴아메리카는 다른 길을 걷고 있습니다. 지역 FTTH에 충당되는 주파수 대역 경매의 수익으로 안데스 시장은 케이블에서 IP로 전환하여 지역 IPTV 시장 전망을 재구성할 수 있습니다.

The IPTV market size is estimated at USD 56.61 billion in 2025 and is projected to scale to USD 133.34 billion by 2030, reflecting an 18.69% CAGR during the forecast window.

Fiber-to-the-home (FTTH) ubiquity, rising 4 K/8 K video appetite, and hybrid subscription-advertising models act together to unlock the next demand layer, moving the metric of success from headline subscriber additions to incremental viewing hours per delivered megabit. Lower transport cost from multicast-assisted architectures widens gross margins, while connected-TV ad insertion boosts average revenue per user on entry-level plans. Operators that already own dense fiber footprints report faster premium-tier uptake once households experience latency-free ultra-high-definition streams.

Operators in the United States lit 12 million new FTTH homes in 2024, while peers in Japan, South Korea, and Germany extended symmetrical gigabit coverage to entire metropolitan belts. The Fiber Broadband Association notes that existing fibers can accommodate 600 terabits per second over a 35-year lifespan, eliminating last-mile constraints for consumer video. As a result, streaming providers confidently debut 8 K sports and HDR nature documentaries that lock customers into premium bundles. A Japanese carrier disclosed that households on its 10-gigabit plan stream 32% more ultra-HD hours than 1-gigabit users, proving a direct bandwidth-to-engagement link. Deployments of 25 G and 50 G PON in Asia-Pacific during 2025 quietly lay the groundwork for volumetric and holographic video, turning today's capex into insurance against future immersive formats.

Western European incumbents launched cloud-native hubs in 2024 that unify national catch-up, subscription video-on-demand, and live sports in one search layer. In Spain, two-thirds of new broadband households activated at least one third-party app through the operator dashboard inside 60 days, generating wholesale platform fees that offset linear ad declines. Billing integration across seven U.S. streamers added USD 4 per user in incremental monthly revenue without raising broadband prices. Regional fiber ventures license turnkey aggregation middleware to leapfrog legacy cable boxes, placing them squarely in the IPTV market conversation despite limited capex. The larger picture is that discovery convenience converts distribution pipes into storefronts where operators monetize every additional content partner.

North American pay-TV households fell another 4% in 2024 as consumers focused spending on broadband and mobile connectivity, relegating channel bundles to optional add-ons. Sky Brasil's April 2024 pivot toward fiber underscores how incumbents view infrastructure ownership as the sole hedge against pure-play OTT disruption. European cable groups follow by over-building FTTH or upgrading coax to DOCSIS 4.0, yet subscriber growth remains flat. Customer value perception has shifted toward low-latency access, making content an upsell, not a core driver. Unless operators strengthen IP delivery economics, the IPTV market risks ARPU stagnation even if total viewing hours rise.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services represented 61% of the IPTV market size in 2024 as operators outsourced managed operations, platform integration, and customer support. Budgets increasingly flow to AI-driven personalization engines that raise viewing minutes without inflating content costs. Vendors offer cloud-native support desks and predictive maintenance that lower churn and truck-roll expenses. Because margins hinge on engagement, service partners selling recommendation algorithms command premium rates. The IPTV market also rewards integrators who wrap security, analytics, and billing into one SLA, letting operators focus on fiber expansion.

Transmission & encoding equipment, although smaller in base, is projected to grow at a 22.4% CAGR through 2030 as low-latency edge encoders become mandatory for live 4K sports and interactive overlays. Operators learned in the 2025 field upgrades that embedding multicast modules in consumer gateways cuts per-hour streaming cost by one-third without compromising bitrates. Firmware upgradability is now a selling point as codec evolution from H.264 to AV1 and VVC gathers pace. Hardware suppliers thus market future-proof designs that preserve capex even when 8K adoption rises. Competitive differentiation is shifting toward power efficiency per delivered gigabit, a metric regulators and investors increasingly scrutinize.

Subscriptions controlled 74.3% of the IPTV market share in 2024 because many households still prefer ad-free catalogs and bundled sports passes. Multi-screen allowances, cloud DVR, and cross-device resumption sustain perceived value, especially among families. Operators enrich loyalty programs by offering streaming credits redeemable for theatrical releases, preventing churn to month-to-month OTT rivals. Yet the same players keep introducing lower-priced ad tiers to capture budget-conscious viewers without cannibalizing premium packages.

AVoD is the fastest-growing slice, racing at 28.7% CAGR, fuelled by maturing ad tech that supports household-level targeting and shoppable placements. A January 2025 Canadian campaign for a grocer logged a 9% click-through rate within cooking show streams, evidencing purchase intent when ads align with content. Operators integrate demand-side platforms into middleware, capturing a direct share of ad revenue rather than mere carriage fees. Pay-per-view remains useful for marquee boxing or concerts, but event rights increasingly feed mid-tier subscription bundles to maximize lifetime value. Tools originally built for PPV micropayments are repurposed for tipping and live commerce, broadening revenue per viewer beyond tickets alone.

IPTV Market is Segmented by Component (Hardware, Services), Revenue Model (Subscription-Based, Pay-Per-View, Advertising-Supported), Streaming Type (Live/Linear TV, Time-Shifted/Replay TV, Video-On-Demand), Device/Access Platform (Smart TV, Mobile and Tablet, PC/Laptop, Set-Top Box and Media Streamer), Delivery Method (Multicast IPTV, Unicast IPTV), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominated revenue with 35.8% of the IPTV market in 2024, propelled by FTTH roll-outs, high smartphone penetration, and multilingual libraries. Chinese platforms simulcast Mandarin and Cantonese commentary on premier sports, maximizing rights fees. Japan's 8 K satellite trials nudged urban fiber households into premium plans that guarantee zero down-sampling. Tier-II Indian cities adopted bundled fiber plus local OTT packs at INR 699 (USD 8.45) per month, converting cable homes into IP ecosystems. Hyper-local dramas thrive on targeted advertising, proving that cultural specificity scales when transport costs fall.

The Middle East and Africa holds a smaller base but is forecast for a 24.7% CAGR through 2030 as analog switch-off deadlines and cheap smartphones stimulate demand. A North African broadcaster streamed Ramadan dramas at 480p to conserve data, attracting 1.2 million unique viewers. Nigeria's open-access corridors lease bandwidth at wholesale rates, enabling city-wide Wi-Fi with multicast-ready routers that lessen piracy by improving legitimate quality. Government funds earmarked for rural fiber accelerate uptake in Kenya and Ghana, where traditional cable never reached scale. Affordable, high-quality streams emerge as the most effective antipiracy tool.

North America and Europe are mature, yet monetization continues via super-aggregation fees and connected-TV ads. A Nordic fiber cooperative bundled gigabit access with four indie streamers for EUR 54.90 (USD 60.14) per month, tapping patriotic content demand amid macro pressures. U.S. carriers leverage zero-rating into mobile plans, retaining subscribers despite slower household growth. Latin America represents divergent paths: Brazil readies ATSC 3.0 hybrid terrestrial-IP, whereas Argentina and Chile rely on satellite backhaul pending fiber investment. Spectrum auction proceeds earmarked for rural FTTH could let Andean markets leapfrog cable straight to IP, reshaping the regional IPTV market landscape.