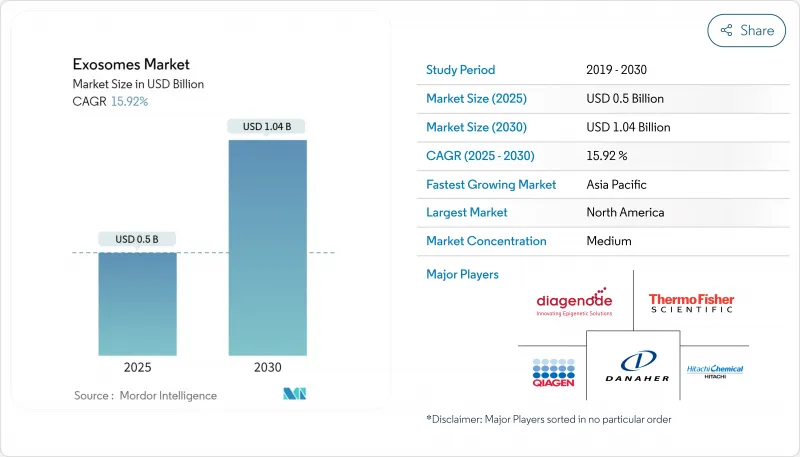

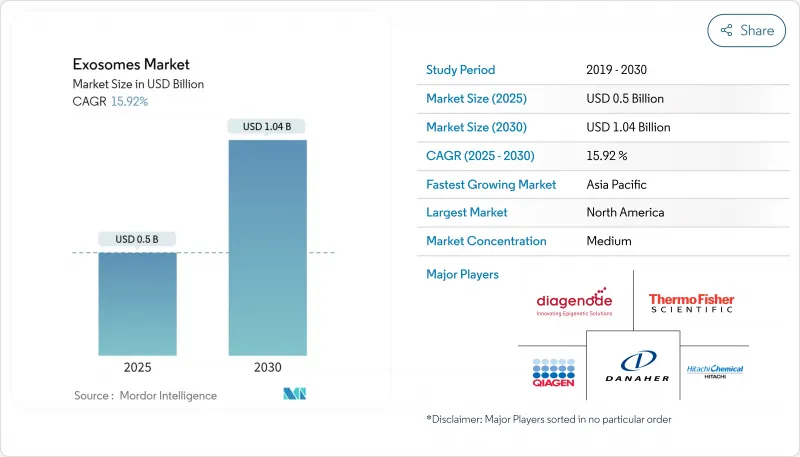

엑소좀 시장은 2025년에 7억 1,000만 달러로 추정되고, 2025-2030년 CAGR 25.5%로 성장할 전망이며, 2030년에는 22억 1,000만 달러에 달할 것으로 예측되고 있습니다.

강한 기세는 나노사이즈의 소포가 생물학적 장벽을 넘어 면역원성이 낮은 화물을 전달할 수 있기 때문이며, 엑소좀을 차세대 진단제나 표적 치료제의 바람직한 플랫폼으로 자리매김하고 있습니다. 북미는 규제환경 정비 및 연구개발 자금의 충실에 힘입어 채용을 선도하고 있으며, 아시아태평양은 생물의학 이노베이션에 대한 공공 투자를 배경으로 급증하고 있습니다. 키트 및 시약은 분리를 단순화하기 위해 큰 점유율을 차지하지만, 사용자가 복잡한 분석을 아웃소싱하기 때문에 서비스 및 소프트웨어가 급성장하고 있습니다. 현재 진단제가 최대의 용도를 차지하고 있지만 임상적 증거가 높아짐에 따라 치료 프로그램도 가속화되고 있습니다.

세계의 암 이환율은 상승 경향에 있으며, 종양의 생물학을 실시간으로 추적하는 저침습 검사 수요에 박차를 가하고 있습니다. 엑소좀 기반의 리퀴드 바이옵시는 종양에 특이적인 핵산과 단백질을 포함하여 조기 발견 및 동적 모니터링이 가능합니다. 2024년 미국암 학회에서 발표된 조사에서는 엑소좀 검정과 CA19-9를 조합하면 1단계-2의 췌장암의 97%가 검출되었습니다. 동시에, 연구 그룹은 종양 유래 소포를 정밀 약물 페이로드를 위해 공학적으로 설계하고, 표적 외독성을 감소시키며, 새로운 치료의 길을 열고 있습니다. 따라서, 종양학은 엑소좀 시장의 유일한 가장 큰 촉진요인이고, 계속해서 플랫폼의 진화와 임상 수용의 촉매가 되고 있습니다.

미국 FDA는 소포를 생리활성에 근거하여 평가하는 반면, 유럽의약청은 선진 치료제로 하고 있습니다. 현재 가이던스 초안에서는 중요 품질 특성 시험과 방출 기준이 명시되어 있습니다. 일본의 재생의료제품에 대한 신속화 패스웨이는 더욱 기세를 가져옵니다. 보다 명확한 규제는 승인 리스크를 줄이고 후기 단계의 자본을 끌어들입니다.

이종 분리 방법은 입자 수, 입자 크기 분포 및 생물학적 활성이 다른 소포 제제를 생성합니다. 2024년에 Journal of Nanobiotechnology 잡지에 게재된 총설에서는 연구실이 명목상 유사한 키트를 사용하고 있어도 큰 편차가 있는 것으로 보고되었습니다. 합의된 표준이 없으면 연구 간의 비교가 어려워지고 변환된 진보가 지연됩니다. 국제세포 및 유전자치료학회(International Society for Cell & Gene Therapy)에 의한 지속적인 대처는 든든한 것이지만, 널리 보급하는 것이 중기적인 과제이며, 엑소좀 시장의 궤도 수정을 가져올 가능성이 있습니다.

키트 및 시약은 분리의 단순화와 운영자의 변동을 억제하는 역할을 반영하여 엑소좀 시장의 2024년 매출의 47%를 차지했습니다. ExoEasy Maxi Kit와 같은 기존 제품은 혈장, 혈청, 소변에서 일관된 소포 수율을 제공합니다. 이 부문은 정기적인 소모품 수요와 정착된 사용자 익숙성에서 이익을 얻습니다. 서비스 및 소프트웨어는 규모가 작고 실험실이 멀티오믹스 프로파일링과 바이오인포매틱스를 외주하고 있기 때문에 CAGR 39.7%로 확대하고 있습니다. 수탁연구기관은 현재 샘플처리와 AI 주도 분석을 번들하여 바이오마커 탐색에 필수적인 파트너로 자리매김하고 있습니다. 자동 비드 기반 풀다운 플랫폼과 더 높은 처리량을 제공하는 벤치 탑 나노 플로우 사이토 미터를 뒷받침하여 계측기가 3위 슬라이스를 차지합니다. 통합이 깊어짐에 따라 공급업체는 하드웨어와 소비 가능한 소프트웨어의 번들을 출시하는 경우가 많아지고, 엑소좀 시장에서의 끈기가 강해지고 있습니다.

소모품은 안정적인 마진을 보장하고 장비는 일회성 설비 투자를 명령하며 소프트웨어는 데이터 중심 경상 수익을 보장합니다. 이러한 상호작용은 도구 제조업체와 분석 전문가 간의 파트너십을 장려하여 엔드 투 엔드 워크플로우를 제공합니다. 시약, 자동화 및 클라우드 파이프라인을 원활한 사용자 경험에 연결할 수 있는 공급업체는 예측 기간 동안 엑소좀 시장 점유율을 확대할 것으로 보입니다.

분리법은 2024년 워크플로우 수익의 55%를 차지했으며, 재현성 있는 실험에 중요하다는 점을 강조합니다. 초원심법은 규모의 제한에도 불구하고 여전히 널리 채택되고 있는 반면, 중합체 침전 키트는 빠른 소량 처리로 인기를 끌고 있습니다. Biological Dynamics의 ExoVerita Pro와 같은 독특한 솔루션은 혈장에서 소포를 고순도로 농축하기 위해 교류 자기장을 통합합니다. CAGR 38.5%로 확대되는 다운스트림 분석은 이 분야의 분석축을 보여줍니다. 단일 소포 나노 유동 세포 계측기는 현재 바이러스에 가까운 분해능으로 표면 항원을 프로파일링하고 탠덤 질량 분석은 한 번의 분석으로 수천 개의 단백질 카고 종을 확인합니다. AI 모델은 멀티오믹스 시그니처를 질병 표현형에 연결하고 원시 측정값을 임상적으로 실용적인 지표로 변환합니다. 분리 워크플로우가 성숙함에 따라 경쟁업체와의 차별화는 데이터의 풍부함과 해석 속도로 이동하고 있으며, 이는 엑소좀 시장 내 기술 대응 서비스 제공업체에게 선호되고 있습니다.

장기적인 전망에서 분리에서 분석까지의 통합 파이프라인은 턴어라운드 시간을 며칠에서 몇 시간으로 단축합니다. 센서가 내장된 온칩 분획을 포함하는 공급업체는 벤치탑 원심분리를 시대에 뒤떨어지게 할 가능성이 있으며, 모범 사례 워크플로우를 더욱 재정의하여 엑소좀 시장 전체의 새로운 수익층을 확보할 수 있습니다.

북미가 엑소좀 시장의 중심이며, 2024년의 수익 점유율은 53%였습니다. 미국은 NIH의 보조금과 FDA의 가이던스 초안이 제조에 대한 기대를 명확히 하고 있는 경우도 있어 임상시험이나 벤처기업의 시작이 활발합니다. 하버드 대학, 매사추세츠 공과대학(MIT), 메릴랜드 주립대학 앤더슨교(MD Anderson) 등 주요 학술 거점은 기술 스핀아웃을 촉진하는 세포외 소포 전문센터를 운영하고 있습니다. 리퀴드 바이옵시의 상환 코드가 보급되고, 치료 자산이 후기 단계에 들어감에 따라, 이 지역 시장 규모는 2030년까지 급증할 것으로 예측됩니다. 진단제가 현재의 주류를 차지하는 한편, 신경종양학 및 심대사성 질환을 위한 인공소포 치료제가 매우 중요한 임상시험에 가까워지고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역이며 CAGR 예측은 39.0%입니다. 중국, 일본, 한국은 전용 트랜스레이셔널 프로그램에 자금을 제공하고 생명공학 제조를 위한 세제 혜택을 제공합니다. 한국의 Brexogen의 라이선싱 계약은 이 지역 최초의 엑소좀 치료제의 아웃라이선싱의 이정표가 되어 상업적 성숙을 강조하고 있습니다. 현지 규제 당국은 ATMP의 틀에 따라 조화를 이루는 가이드라인을 초안하여 국경을 넘는 임상시험을 쉽게 수행할 수 있습니다. 현재는 진단약이 매출의 중심을 차지하고 있지만, 현지의 CDMO가 GMP 스위트를 확대해, 임상 데이터가 밝혀짐에 따라, 치료제 프로그램이 점유율을 확대하는 태세가 갖추어지고 있습니다.

유럽은 독일, 영국, 프랑스에서 3위를 차지했습니다. 유럽의약청(EEA)의 ATMP 패스웨이는 소포약의 지침이지만, 효력 측정과 미국의 기능적 메트릭에 중점을 두는 방법이 다르기 때문에 국제적인 임상시험의 조정이 복잡해질 수 있습니다. 호라이즌 유럽은 벤치사이드에서 베드사이드로 가는 다국적 컨소시엄에 자금을 제공하여 기술 검증을 가속화하고 있습니다. 제약회사는 특히 신경퇴행성 질환이나 희소질환의 적응증에서 공동개발을 위해 대륙의 연구력을 활용하도록 되어 있습니다. 중동, 아프리카 및 남미는 아카데믹 센터 오브 엑설런스를 중심으로 신흥 시장을 형성하고 있습니다. 공중 보건에 대한 노력과 만성 질환 증가로 엑소좀 진단제와 현지 제조 치료제가 점차 보급되어 엑소좀 시장의 세계적인 확산이 기대됩니다.

The exosomes market is valued at USD 0.71 billion in 2025 and is forecast to climb to USD 2.21 billion by 2030, tracking a 25.5% CAGR during 2025-2030.

Strong momentum stems from the ability of nano-sized vesicles to cross biological barriers and deliver cargo with low immunogenicity, positioning exosomes as a preferred platform for next-generation diagnostics and targeted therapeutics. North America leads adoption, propelled by a supportive regulatory environment and heavy R&D funding, while Asia-Pacific is expanding fastest on the back of public investment in biomedical innovation. Kits & Reagents hold the lion's share because they simplify isolation, yet Services & Software are growing quicker as users outsource complex analytics. Diagnostics currently represent the largest application, although therapeutic programs are accelerating as clinical evidence mounts.

Global cancer incidence is climbing, spurring demand for minimally invasive tests that track tumor biology in real time. Exosome-based liquid biopsies harbor tumor-specific nucleic acids and proteins that enable earlier detection and dynamic monitoring. A 2024 study presented at the American Association for Cancer Research showed that an exosome assay detected 97% of stage 1-2 pancreatic cancers when paired with CA 19-9. Concurrently, research groups are engineering tumor-derived vesicles for precision drug payloads, reducing off-target toxicities and opening new therapeutic avenues. Oncology thus remains the single largest driver for the exosomes market, catalyzing platform evolution and clinical acceptance.

The U.S. FDA evaluates vesicles based on physiological activity, whereas the European Medicines Agency frames them under Advanced Therapy Medicinal Products. Draft guidance now specifies critical-quality-attribute testing and release criteria. Japan's expedited pathway for regenerative products provides further momentum. Clearer regulations reduce approval risk and attract late-stage capital, a modest but meaningful tailwind for the exosomes market over the long term.

Heterogeneous isolation methods generate vesicle preparations with divergent particle counts, size distributions, and bioactivity. A 2024 review in Journal of Nanobiotechnology documented wide variability even when laboratories used nominally similar kits. Without agreed-upon standards, cross-study comparisons suffer, slowing translational progress. Ongoing efforts by the International Society for Cell & Gene Therapy are encouraging, but widespread adoption remains a mid-term challenge that may temper the exosomes market trajectory.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Kits & Reagents generated 47% of 2024 revenue in the exosomes market, reflecting their role in simplifying isolation and reducing operator variability. Off-the-shelf products such as the ExoEasy Maxi Kit deliver consistent vesicle yields across plasma, serum, and urine. The segment benefits from recurring consumable demand and entrenched user familiarity. Services & Software, while representing a smaller base, are scaling at a 39.7% CAGR as laboratories outsource multi-omics profiling and bioinformatics. Contract research organizations now bundle sample processing with AI-driven analytics, positioning themselves as indispensable partners for biomarker discovery. Instruments occupy the third-largest slice, buoyed by automated bead-based pull-down platforms and benchtop nano-flow cytometers that offer higher throughput. As integration deepens, vendors increasingly release hardware-consumable-software bundles, strengthening stickiness in the exosomes market.

A parallel dynamic is reshaping competitive priorities: consumables secure stable margins, instruments command one-time capex, and software unlocks data-centric recurring revenue. The interplay is encouraging partnerships between toolmakers and analytics specialists to offer end-to-end workflows. Vendors able to tie reagents, automation, and cloud pipelines into a seamless user experience will capture incremental exosomes market share during the forecast period.

Isolation Methods accounted for 55% of workflow revenue in 2024, underscoring their centrality to reproducible experimentation. Ultracentrifugation remains widely adopted despite scale limitations, while polymer precipitation kits gain traction for rapid small-volume processing. Proprietary solutions such as Biological Dynamics' ExoVerita Pro integrate alternating current fields to enrich vesicles from plasma with high purity. Downstream Analysis, expanding at a 38.5% CAGR, exemplifies the field's analytical pivot. Single-vesicle nano-flow cytometry now profiles surface antigens at near-virus resolution, and tandem mass spectrometry identifies thousands of protein cargo species per run. AI models link multi-omic signatures to disease phenotypes, converting raw readouts into clinically actionable indices. As isolation workflow matures, competitive differentiation is shifting to data richness and interpretation speed, an opportunity for tech-enabled service providers within the exosomes market.

The long-term outlook favors integrated isolation-to-analysis pipelines that compress turnaround time from days to hours. Vendors embedding on-chip fractionation with embedded sensors could eventually render bench-top centrifugation obsolete, further redefining best-practice workflows and unlocking new revenue layers across the exosomes market.

The Exosomes Market Report is Segmented by Product (Kits and Reagents, and More), Workflow (Isolation Methods [Ultracentrifugation, and More] and Downstream Analysis), Biomolecule Type (Proteins & Peptides, and More), Application (Diagnostics and Therapeutics), End-User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America anchors the exosomes market with a 53% revenue share in 2024. The United States hosts the majority of clinical trials and venture-backed start-ups, aided by NIH grants and FDA draft guidance that clarifies manufacturing expectations. Leading academic hubs such as Harvard, MIT, and MD Anderson operate specialized extracellular-vesicle centers that foster technology spin-outs. Exosomes market size in the region is projected to climb sharply through 2030 as liquid biopsy reimbursement codes roll out and therapeutic assets enter late-stage studies. Diagnostics dominate current uptake, while engineered vesicle therapeutics for neuro-oncology and cardiometabolic diseases approach pivotal trials.

Asia-Pacific is the fastest-expanding territory, with a forecast 39.0% CAGR. China, Japan, and South Korea fund dedicated translational programs and offer tax incentives for biotech manufacturing. South Korea's Brexogen licensing deal marked the region's first exosome therapeutic out-licensing milestone, underscoring commercial maturation. Regional regulators are drafting harmonized guidelines patterned after ATMP frameworks, which will ease cross-border trial execution. While diagnostics currently headline revenue, therapeutic programs are poised to gain share as local CDMOs scale GMP suites and clinical data emerge.

Europe ranks third, supported by Germany, the United Kingdom, and France. The European Medicines Agency's ATMP pathway guides vesicle drugs, yet diverging emphasis on potency assays versus U.S. functional metrics can complicate global trial alignment. Horizon Europe funds multinational consortia that bridge bench to bedside, accelerating technology validation. Pharmaceutical companies increasingly leverage continental research strength for co-development, particularly in neurodegenerative and rare-disease indications. Middle East & Africa and South America form nascent markets centered on academic centers of excellence. Targeted public-health initiatives and rising chronic-disease prevalence should kindle gradual uptake of exosome diagnostics and, longer term, locally manufactured therapeutics, expanding the global footprint of the exosomes market.