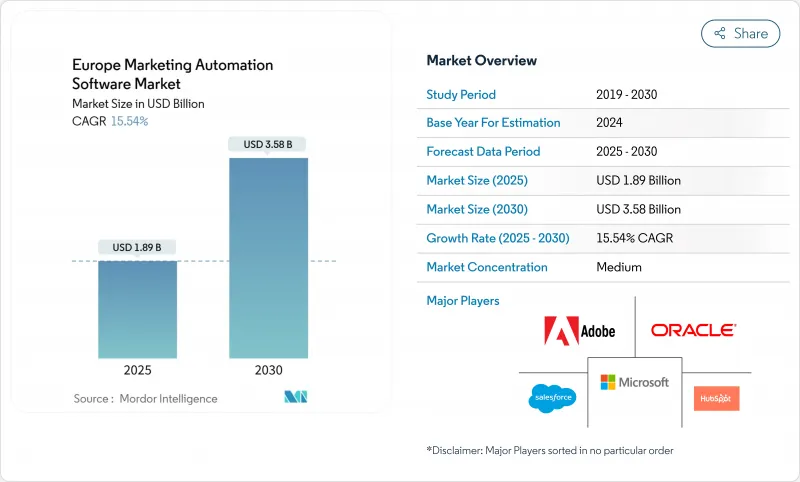

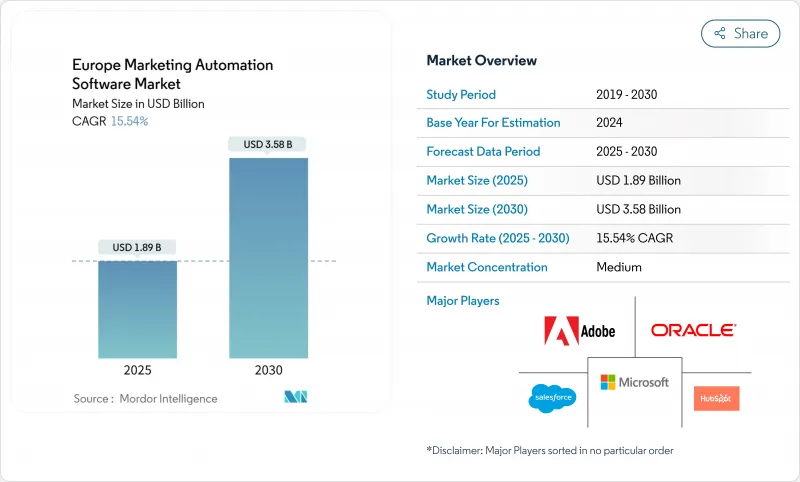

유럽의 마케팅 자동화 소프트웨어 시장은 2025년 18억 9,000만 달러로, 2030년까지 35억 8,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 15.54%로 예상됩니다.

2030년까지 75%의 클라우드 도입을 목표로 하는 EU의 디지털 단일 시장 대책은 79억 유로(85억 5,000만 달러)의 디지털 유럽 프로그램(Digital Europe Programme)과 함께 중소기업의 SaaS 도입을 조성함으로써 당면의 확대를 지원하고 있습니다. 한편, 2023년 이 지역의 전자상거래 경제규모는 8,870억 유로(9,600억 달러)이며, GDPR(EU 개인정보보호규정)에 준거하면서, 세밀한 개인화를 실현하는 고객 중심의 인게이지먼트 툴에 대한 수요가 높아지고 있습니다. 세계 플랫폼 벤더가 유럽에서의 사업 기반을 강화하는 한편, 현지 전문가들은 다국어와 규제에 관한 전문 지식으로 차별화를 도모하기 때문에 경쟁의 격렬함이 증가하고 있습니다. 확장 가능한 컴플라이언스 관리를 제공하기 위해 클라우드 배포 모델이 주류를 이루고 있지만 기업의 지출 이동이 가장 빠른 것은 GDPR(EU 개인정보보호규정)에 익숙한 구현 인력과 기술을 번들로 한 관리 서비스입니다. 독일의 18.5% CAGR과 DACH-북유럽 국가들이 AI 주도의 개인화에 주력하고 있는 것은 AI 준비와 마케팅 자동화 도입의 관련성을 돋보이게 하고 있습니다.

DACH 및 북유럽 소매 업계에서는 AI를 활용한 엔진이 침투하고 있으며, 경영 간부의 65%가 2025년 핵심 성장 요인으로 AI를 꼽았습니다. 마케팅 담당자는 이 지역의 고급 클라우드 인프라와 높은 데이터 공유 동의율을 활용하여 전환을 높이는 추천 모델을 구축하고 있습니다. Telmore는 AI 주도 개인화를 채택한 후 매출이 11% 증가한 것을 기록하고 동업 타사의 채용을 가속화하는 정량화 가능한 ROI를 나타냅니다. 80%의 기업이 AI 예산의 증액을 계획하고 있지만, ROI를 증명할 수 있는 것은 단 12%이기 때문에 강력한 측정 프레임워크를 가진 조기 도입 기업이 경쟁력을 획득하고 있습니다. 독일의 기업들은 생셩형 인공지능을 사용하여 캠페인 제작 및 리포팅을 간소화하고 반복적인 작업을 줄이고 직원을 애널리틱스로 전환하고 있습니다. 그 결과, DACH-북유럽은 차세대 개인화 기능의 테스트 베드 역할을 하고, 그 후 유럽 전역에 보급될 것입니다.

79억 유로(85억 5,000만 달러)의 디지털 유럽 프로그램은 클라우드 규제를 조화시키고 현지 지도를 하는 유럽 디지털 혁신 허브에 자금을 제공함으로써 중소기업의 장벽을 낮추고 있습니다. 표준화된 API는 데이터의 이식성을 향상시키고, 서로 다른 마케팅 용도 간의 통합을 용이하게 하며, 벤더 록인의 위험을 완화합니다. EU 기업의 클라우드 도입률은 41%에 달했으며 2030년에는 75%에 이를 것으로 예측됩니다. 이러한 정책을 몰아넣으면 중견 기업의 구매자에게 컴플라이언스의 복잡성이 줄어들고 유럽 마케팅 자동화 소프트웨어 시장에서의 대응 가능한 수요가 확대됩니다.

마케팅 기술 숙련과 법적 통찰을 겸비한 전문가는 제한되어 있기 때문에 구현 프로젝트는 점점 더 정체되고 있습니다. 은행의 노동력 재편은 2007년부터 2022년 사이에 전통적인 역할의 고용이 21% 축소된 후 데이터 전문가의 이업종간 경쟁을 보여줍니다. 중소기업은 불균형한 영향을 받아 외부의 관리형 서비스에 의존하게 되어 서비스 부문의 CAGR이 16.1%임을 설명하고 있습니다. 유럽의 디지털 혁신 허브(Digital Innovation Hubs)에 의한 인증 이니셔티브는 구제책이 되지만, 당면한 인력 부족이 중소기업에서 도입의 발판이 됩니다.

2024년 유럽 마케팅 자동화 소프트웨어 시장 매출의 72%는 소프트웨어가 차지했으며, 2030년까지 연평균 복합 성장률(CAGR)은 매니지드 서비스가 16.1%로 성장할 것으로 예상되어 컴플라이언스 노하우의 아웃소싱을 선호하는 기업의 경향이 밝혀졌습니다. 서비스의 급증은 기업이 핵심 기능과 마찬가지로 기술적 실행과 법규의 검증을 중요시하고 있음을 보여줍니다. 소프트웨어에서는 통합 제품군이 포인트 도구를 능가하고 있는데, 이는 구매자들이 데이터 프라이버시 감사와 AI 모델 거버넌스를 위한 진실된 하나의 소스를 요구하기 때문입니다. 전문 서비스는 레거시 시스템 통합과 GDPR(EU 개인정보보호규정) 갭 분석을 통해 성공을 거두었으며 컨설턴트 회사와 시스템 통합자를 공급업체 선택의 게이트키퍼로 자리매김하고 있습니다.

AI 방법의 모니터링 강화는 설계를 통한 감사 가능성을 통합한 솔루션 설계도에 중점을 둡니다. 벤더는 패키지 소프트웨어와 권고 리테이너를 결합하여 연금 형식의 수익을 창출합니다. 따라서 유럽의 마케팅 자동화 소프트웨어 업계에서는 GDPR(EU 개인정보보호규정), PSD2, 섹터별 의무에 걸친 역동적인 룰셋을 지원하므로 소프트웨어 마진과 하이터치 서비스가 결합된 블렌드 비즈니스 모델을 볼 수 있습니다.

클라우드 옵션은 2024년 유럽 마케팅 자동화 소프트웨어 시장의 78%를 차지하며, 소버린과 신뢰할 수 있는 클라우드 프레임워크에 대한 EU의 지원으로 강화됩니다. 클라우드 도입은 CAGR 15.8%로 확대되고 있는데, 이는 지속적인 플랫폼 업데이트를 통해 고객이 설비 투자를 급증시키지 않고 새로운 데이터 처리 의무를 흡수할 수 있기 때문입니다. 마케팅 팀은 실시간으로 여정을 개인화하는 AI 모델을 실행하는 탄력적인 컴퓨팅에서 이익을 얻고 있습니다. On-Premise는 공공 부문 및 방위 부문 고객이 엄격한 데이터 레지던시를 요구하는 경우에만 지속됩니다.

규제 당국은 자동화된 동의 로깅, 위반 통지, 암호화 관리를 지원하는 클라우드의 중앙 관리 영역을 지원합니다. 이러한 규제의 무결성은 인식되는 위험을 줄이고 보다 광범위한 클라우드 마이그레이션에 박차를 가합니다. Oracle과 Palantir가 EU의 안전한 클라우드 지역에서 제휴한 파트너십은 하이퍼스케일 제공업체가 주권에 관한 이야기를 충족하기 위해 스택을 지역화하는 방법을 보여줍니다. 클라우드로의 마이그레이션이 성숙함에 따라 클라우드 벤더는 제로 트러스트 아키텍처 및 사전 인증된 AI 샌드박스와 같은 부가 가치 계층에서 경쟁할 것으로 보입니다.

유럽의 마케팅 자동화 소프트웨어 시장은 컴포넌트별(소프트웨어, 서비스), 전개 형태별(클라우드 기반, On-Premise), 조직 규모별(중소기업, 대기업), 채널 및 기능별(메일 마케팅, 소셜 미디어 마케팅, 캠페인 관리 등), 최종 사용자 산업별(소매 및 E-Commerce, BFSI 등), 국가별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

The Europe marketing automation software market is valued at USD 1.89 billion in 2025 and is forecast to reach USD 3.58 billion by 2030, registering a brisk 15.54% CAGR across the period.

Ongoing EU Digital Single Market measures that target 75% cloud adoption by 2030, together with the EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme, underpin near-term expansion by subsidizing SaaS adoption among small and medium-sized enterprises. Meanwhile, the region's EUR 887 billion (USD 960 billion) e-commerce economy in 2023 fuels demand for customer-centric engagement tools that remain compliant with GDPR while still delivering granular personalization. Competitive intensity is increasing as global platform vendors reinforce European footprints while local specialists differentiate through multilingual and regulatory expertise. Cloud deployment models dominate because they offer scalable compliance controls, yet the fastest corporate spending shift is toward managed services that bundle technology with GDPR-fluent implementation talent. Germany's 18.5% CAGR and the DACH-Nordics focus on AI-driven personalization highlight the link between AI readiness and marketing automation uptake, whereas EU AI Act obligations and a scarcity of certified data-privacy architects temper roll-out velocity.

AI-enabled engines have permeated DACH and Nordic retail, with 65% of executives naming AI a core growth lever in 2025. Marketers exploit the regions' advanced cloud infrastructure and high data-sharing consent rates to roll out recommendation models that elevate conversion. Telmore recorded an 11% uplift in sales after adopting AI-driven personalization, illustrating quantifiable ROI that accelerates peer adoption. As 80% of companies earmark higher AI budgets yet only 12% prove ROI, early adopters with strong measurement frameworks gain competitive distance. German practitioners use generative AI to streamline campaign production and reporting, cutting repetitive tasks and redeploying staff toward analytics. Consequently, the DACH-Nordic corridor functions as a test bed for next-wave personalization capabilities that subsequently diffuse across Europe.

The EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme lowers barriers for SMEs by harmonizing cloud regulations and funding European Digital Innovation Hubs that provide hands-on guidance. Standardized APIs improve data portability, easing integration among disparate marketing applications and mitigating vendor lock-in risks. Cloud adoption among EU enterprises stands at 41% and is slated to reach 75% by 2030, translating into a sizeable new customer pool for SaaS-based marketing automation. These policy tailwinds curtail compliance complexity for mid-market buyers and amplify addressable demand within the Europe marketing automation software market.

Implementation projects increasingly stall because only a narrow cadre of professionals combines martech proficiency with legal insight. Banking workforce realignment illustrates cross-industry competition for data specialists after a 21% employment contraction in traditional roles between 2007 and 2022. SMEs are disproportionately affected, leading to a reliance on external managed services, which explains their 16.1% CAGR within the services component. Certification initiatives by European Digital Innovation Hubs provide relief, but near-term talent gaps constrain uptake within smaller economies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software continued to generate 72% of Europe marketing automation software market revenue in 2024, though managed services outpaced with a 16.1% CAGR to 2030, underscoring corporates' preference for outsourced compliance know-how. The services surge signals that enterprises consider technical execution and regulatory validation equally critical as core functionality. Within software, integrated suites eclipse point tools because buyers demand one source of truth for data privacy audits and AI model governance. Professional services thrive on legacy-system integration and GDPR gap analysis, positioning consultancies and system integrators as gatekeepers for vendor selection.

Heightened AI Act scrutiny places a premium on solution blueprints that embed auditability by design. Vendors combine packaged software with advisory retainers, generating annuity-style revenue. The Europe marketing automation software industry will therefore see blended business models, where software margins pair with high-touch services to address dynamic rule-sets spanning GDPR, PSD2, and sector-specific mandates.

Cloud options owned 78% of the Europe marketing automation software market in 2024, bolstered by EU backing for sovereign and trusted cloud frameworks. Cloud deployments are expanding at 15.8% CAGR because continuous platform updates help clients absorb new data-handling obligations without capex spikes. Marketing teams benefit from elastic compute to run AI models that personalize journeys in real time. On-premise persists only where public-sector or defense clients demand strict data residency.

Regulators favor cloud's centralized control planes that support automated consent logging, breach notification, and encryption management. This regulatory alignment reduces perceived risk, spurring broader cloud migration. Partnerships, such as Oracle's tie-up with Palantir for secure EU cloud regions, illustrate how hyperscale providers localize stacks to satisfy sovereignty narratives. As uptake matures, cloud vendors will compete on value-add layers like zero-trust architectures and pre-certified AI sandboxing.

Europe Marketing Automation Software Market is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), Organisation Size (Small and Medium Enterprises, Large Enterprises), Channel / Function (Email Marketing, Social Media Marketing, Campaign Management, and More), End-User Industry (Retail and E-Commerce, BFSI, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).