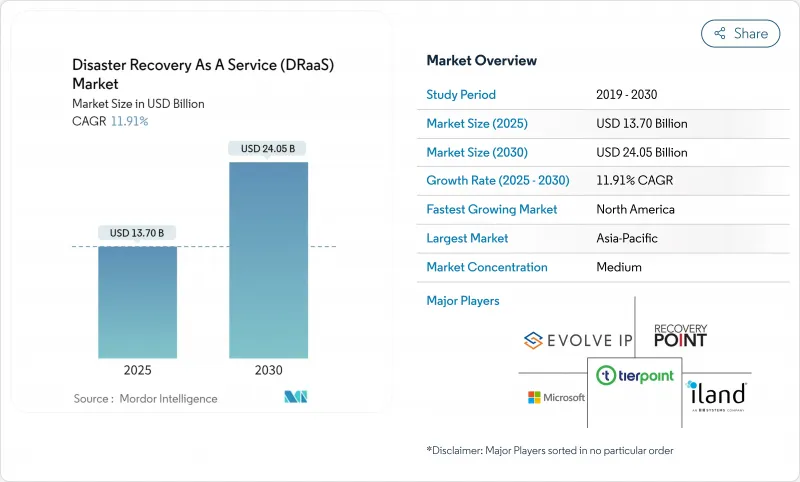

DRaaS(Disaster Recovery As A Service) 시장은 2025년에 137억 달러, 2030년에는 240억 5,000만 달러에 이르고, CAGR 11.91%를 나타낼 것으로 예측됩니다.

랜섬웨어 급증, 규제 요건 확대, 클라우드 퍼스트 인프라 전략적 기울기로 기업 연속성 프로그램이 재구성되어 클라우드 네이티브 복구 제품에 대한 수요가 증가하고 있습니다. 기업은 현재 공격 중에 계속 업무를 수행하기 위해 신속하고 자동화된 페일오버가 필요합니다. 기존 테이프 및 디스크 백업은 더 이상 위험위원회와 이사회를 만족시킬 수 없습니다. 테스트된 복구 계획을 요구하는 사이버 보험 조항 증가는 보험료와 DRAaS의 성숙한 채용 간의 링크를 더욱 견고하게 만듭니다. 동시에, 구독 모델은 자본 지출을 줄여 대기업과 중소기업 모두가 엔터프라이즈급 탄력성을 활용할 수 있도록 합니다. 공급업체는 현재 오케스트레이션 인텔리전스, 멀티클라우드 지원 및 지속가능성 증명으로 경쟁하고 있습니다.

2024년에는 IT 팀의 87%가 SaaS의 데이터 유출을 경험했지만 신속한 복구에 자신이 있는 것은 단 14%를 나타낼 전망입니다. 건강 관리 제공업체는 HIPAA를 준수하고 환자 관리의 연속성을 보호하기 위해 클라우드 네이티브 복구를 채택합니다. 사이버 보험 회사는 검증된 장애 조치 기능에 보험료 할인을 적용하고 CFO는 DRaaS 채용에 대한 명확한 재무 논거를 얻을 수 있습니다.

DRaaS는 보조 사이트 및 전문 직원에게 자본 지출을 제거하고 사용 비용을 조정하는 종량 과금 구독으로 대체합니다. Veeam의 보고에 따르면, 88%의 조직이 2년 이내에 DRAaS로 이행할 계획이며, 그 동기로서 비용 최적화가 상위에 올랐다고 합니다. 구독 가격은 하드웨어의 진부화를 방지하고 IT 팀은 하드웨어 유지 관리보다 혁신 프로젝트에 집중할 수 있습니다. 중소기업의 경우 규모에 따른 투자 없이 엔터프라이즈급 복구가 가능하므로 경제적으로 특히 매력적이며 DRaaS(Disaster Recovery As A Service) 시장에 대응할 수 있는 범위가 넓어집니다.

레거시 On-Premise 자산과 여러 퍼블릭 클라우드를 통합하면 조직 내 팀을 피곤하게 되며 조직은 서로 다른 API 및 보안 모델을 배울 수 있습니다. 미국 안보국은 하이브리드 복구 스크립트의 신뢰성을 유지하기 위해 지속적인 테스트와 Infrastructure-as-Code 연습을 조언합니다. 기술 부족은 매니지드 DRAaS 파트너에 대한 의존을 촉진하지만 구매자가 깊은 자동화와 규제에 대한 이해를 요구하여 공급자를 평가하기 때문에 판매주기가 장기화됩니다.

풀매니지드 제공 제품은 턴키 오케스트레이션, 모니터링, 컴플라이언스 보고서에 대한 기업 수요를 배경으로 2024년 DRaaS(Disaster Recovery As A Service) 시장 점유율의 47.20%를 차지했습니다. 고객은 멀티클라우드 엔지니어링 및 24시간 365일 복구 수행을 포함하여 사내 인력을 줄여야 하는 활동으로 제공업체에 의존합니다. 셀프 서비스 옵션은 지원에 의존하며 CAGR 12.40%를 나타낼 전망입니다. 이는 중소기업이 자율성과 비용의 균형을 맞춘 구성 가능한 포털을 선호하기 때문입니다. 어시스트형은 양자의 중간적인 위치에 있어, 클라우드의 스킬을 어느 정도 가지면서, 게다가 런북의 서포트를 필요로 하는 중견 기업에 적합합니다.

매니지드 서비스의 기세는 보다 광범위한 현실을 돋보이게 합니다. 2025년에 91개의 NPS를 획득한 HYCU와 같은 공급업체는 서비스의 충실도와 고객 경험이 기능의 동등성을 능가한다는 것을 보여줍니다. 그 결과, DRaaS(Disaster Recovery As A Service) 시장은 보다 높은 연간 매출 배율을 정당화하는 프리미엄 지원층과 가격에 민감한 틈새를 추구하는 상품 셀프 서비스 계층이라는 서비스 품질의 세분화가 보다 선명해질 것으로 예측됩니다.

퍼블릭 클라우드는 하이퍼스케일 이코노미와 온디맨드 확장성 덕분에 58.10%의 매출을 유지하고 있지만, 하이브리드/멀티클라우드 구성은 기업이 집중 위험을 헤지하고 레지던시 규칙을 충족함으로써 14.60%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 기업이 중요한 데이터베이스를 소블린 클라우드에 복제하는 한편, 기밀성이 낮은 용도를 세계 지역으로 페일오버할 수 있기 때문에 DRaaS(Disaster Recovery As A Service) 시장 규모는 급속히 확대될 것으로 예측됩니다. 엄격한 데이터 분류가 필요한 워크로드와 에어 갭이 필요한 워크로드에는 프라이빗 클라우드가 뿌리깊습니다.

Verizon은 하이브리드의 유연성을 현대 연속성 계획의 핵심이라고 부릅니다. N2WS 설문조사도 이에 동의하고 있으며, 멀티클라우드 복제는 공급업체의 잠금을 줄이고 페일오버 세분화를 향상시킬 것이라고 지적합니다. 그러나 서로 다른 클라우드간에 동일한 복구 시간 목표를 오케스트레이션하는 것은 여전히 복잡하며 클라우드 특정 특이성을 추상화하는 도구의 필요성이 지적되었습니다.

북미는 하이퍼스케일 클라우드 가용성, 성숙한 사이버보험 생태계, 규범적인 규제 프레임워크을 융합시킴으로써 2024년 39.80%의 점유율을 유지했습니다. 랜섬웨어의 다발은 이사회 수준의 긴급성을 높이고 연방 정부 클라우드 운영 모범 사례 가이드는 공공 기관에 청사진 기준을 제공합니다. 특히 금융기관은 보험료 할인을 실증적인 DR 테스트와 연결하고 도입이 더욱 진행되고 있습니다. 아시아태평양의 DRaaS(Disaster Recovery As A Service) 시장은 가격 경쟁에 노출되어 있지만, 에지 도입과 ESG 보고 증가로 수요가 견조해지고 있습니다.

아시아태평양의 CAGR이 가장 높은 14.80%를 기록한 이유는 각국 정부가 GDP를 촉진하기 위해 클라우드 성장을 지지하고 있기 때문입니다. 아시아 개발 은행은 클라우드 정책 개선으로 2024년부터 2028년 사이에 지역 GDP를 최대 0.7% 밀어올릴 수 있을 것으로 예측했습니다. 일본과 호주는 아키텍처의 청사진을 형성하는 엄격한 데이터 주권 점검을 부과하고 있습니다. ADB의 2025년 재해 대책 가이드를 참고로 AI 센서와 클라우드 기반 복구를 통합하고 있습니다. 은행은 Fintech의 민첩성에 맞게 DRAaS를 채택하고 제조업은 공급망 보장을 위해 지리적으로 분산된 장애 조치에 의존합니다.

유럽에서는 도입 인센티브와 컴플라이언스 장애 간의 균형을 맞추고 있습니다. GDPR(EU 개인정보보호규정)과 EU 클라우드 인증법은 지역 내 복제를 의무화하고 설계를 제약하지만 주권에 따른 'EU 지역 내 전용' 복구 노드에 대한 수요도 유발합니다. 공공 부문의 디지털 서비스 목표는 공급자에 대한 노력을 가속화하고 금융 기관은 디지털 운영 탄력성 법(DORA)을 충족하기위한 투자를 계속하고 있습니다. 비용의 압력에도 불구하고 시민 서비스를 유지할 필요성으로 인해 시장은 계속 확대되고 있습니다.

The Disaster Recovery as a Service market stands at USD 13.7 billion in 2025 and is forecast to reach USD 24.05 billion by 2030, expanding at an 11.91% CAGR.

A steep rise in ransomware, expanding regulatory mandates, and a strategic tilt toward cloud-first infrastructure are reshaping corporate continuity programs and fueling demand for cloud-native recovery offerings. Enterprises now require rapid, automated failover to keep operations running during an attack; traditional tape or disk backups no longer satisfy risk committees or boards. Growing cyber-insurance clauses that insist on tested recovery plans further tighten the link between premiums and mature DRaaS adoption. At the same time, the subscription model lowers capital outlays, enabling both large enterprises and SMEs to access enterprise-grade resilience. Vendors now compete on orchestration intelligence, multi-cloud reach, and sustainability credentials, because organizations evaluate providers on both operational and environmental performance.

Attackers now exfiltrate data within hours after compromise, forcing organizations to adopt immutable snapshots and isolated recovery zones that only modern DRaaS platforms supply at scale.In 2024, 87% of IT teams experienced SaaS data loss, yet only 14% felt confident about rapid recovery. Healthcare providers embrace cloud-native recovery to stay HIPAA-compliant and safeguard patient care continuity. Cyber-insurance carriers reward verified failover capabilities with premium discounts, giving CFOs a clear financial argument for DRaaS adoption.

DRaaS removes capital spending on secondary sites and specialist staff, replacing them with pay-as-you-go subscriptions that align cost to use. Veeam reports that 88% of organizations plan to shift toward DRaaS within two years, ranking cost optimization as their top motivation. Subscription pricing prevents hardware obsolescence and frees IT teams to focus on transformation projects rather than hardware upkeep. SMEs find the economics especially compelling because enterprise-grade recovery becomes attainable without scale-driven investments, broadening the total addressable Disaster Recovery as a Service market.

Integrating legacy on-premises assets with several public clouds stretches internal teams and forces organizations to learn disparate APIs and security models. The US National Security Agency advises constant testing and infrastructure-as-code practices to keep hybrid recovery scripts reliable. Skills shortages drive reliance on managed DRaaS partners but also prolong sales cycles, as buyers evaluate providers for deep automation and regulatory comprehension.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fully Managed offerings controlled 47.20% of Disaster Recovery as a Service market share in 2024 on the back of enterprise demand for turnkey orchestration, monitoring, and compliance reporting. Customers lean on providers for multi-cloud engineering and 24X7 recovery execution, activities that would otherwise balloon internal headcount. Self-Service options, though lean on assistance, post a 12.40% CAGR because SMEs prefer configurable portals that balance autonomy with cost. Assisted models sit between both ends, suiting mid-market firms that own some cloud skills yet still need run-book support.

Managed service momentum underscores a broader reality: resilience now spans infrastructure, applications, and regulatory proof. Vendors like HYCU, which scored a 91 NPS in 2025, showcase how service depth and customer experience trump feature parity. As a result, the Disaster Recovery as a Service market will likely witness sharper service-quality segmentation, where premium support tiers justify higher annual-recurring-revenue multiples, while commodity self-service tiers chase price-sensitive niches.

Public Cloud retains 58.10% revenue thanks to hyperscale economies and on-demand scalability, yet Hybrid/Multi-Cloud configurations command a 14.60% CAGR as firms hedge concentration risk and satisfy residency rules. Disaster Recovery as a Service market size for Hybrid deployments is forecast to expand swiftly because enterprises can replicate critical databases to a sovereign cloud while failing over less-sensitive apps to global regions. Private Cloud persists for workloads steeped in strict data classifications or requiring air-gapping.

Verizon calls hybrid flexibility the linchpin of modern continuity planning verizon. N2WS research agrees, noting that multi-cloud replication cuts vendor lock-in and improves failover granularity. However, orchestrating identical recovery time objectives across divergent clouds remains complex, opening room for tooling that abstracts cloud-native idiosyncrasies.

The Disaster Recovery As A Service Market is Segmented by Service Type (Fully Managed, Assisted, and More), Deployment Model (Public Cloud, Private Cloud, and More), Service Component (Backup and Recovery, Real-Time Replication, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Vertical (BFSI, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America maintained a 39.80% share in 2024 by blending hyperscale cloud availability, mature cyber-insurance ecosystems, and prescriptive regulatory frameworks. High ransomware prevalence amplifies board-level urgency, while the Federal Cloud Operations Best Practices Guide supplies public agencies with blueprint standards. Financial institutions, in particular, tie premium discounts to demonstrable DR testing, further cementing uptake. Although the region's Disaster Recovery as a Service market now sees price competition, rising edge deployments and ESG reporting keep demand resilient.

Asia-Pacific registers the highest 14.80% CAGR as governments champion cloud growth to spur GDP. The Asian Development Bank projects that improved cloud policies can lift regional GDP by up to 0.7% between 2024 and 2028. Singapore's aggressive "cloud-first" posture sets policy benchmarks, while Japan and Australia impose rigorous data-sovereignty checks that shape architectural blueprints. National disaster exposure drives mandates for resilient ICT backbones, with agencies referencing ADB's 2025 disaster-preparedness guide to integrate AI sensors and cloud-based recovery. Banks adopt DRaaS to match fintech agility, and manufacturers rely on geo-distributed failover for supply-chain assurance.

Europe balances adoption incentives and compliance roadblocks. GDPR and incoming EU Cloud Certification laws oblige in-region replication, constraining design but also triggering demand for sovereignty-aligned "intra-EU only" recovery nodes. Sustainability legislation boosts interest in "Green-DRaaS," leveraging renewable-powered data centers to hit corporate emissions targets.Public-sector digital-service goals accelerate provider outreach, while financial entities continue to invest to satisfy the Digital Operational Resilience Act (DORA). Despite cost pressure, the imperative to preserve citizen-facing services keeps the market expanding.