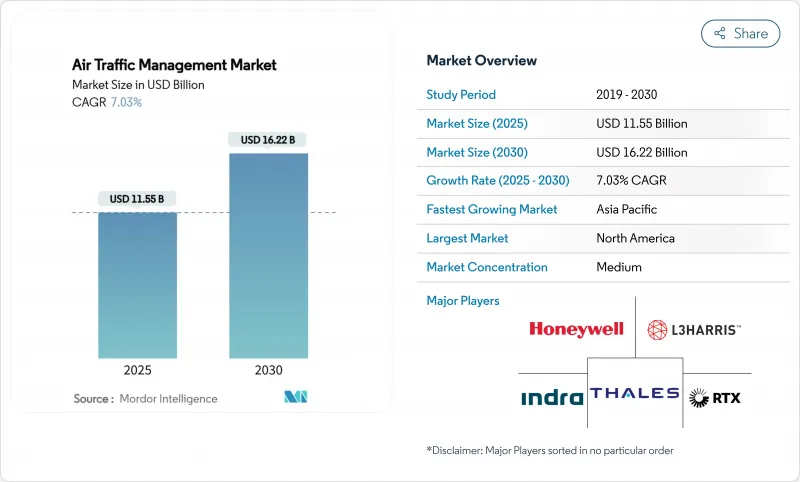

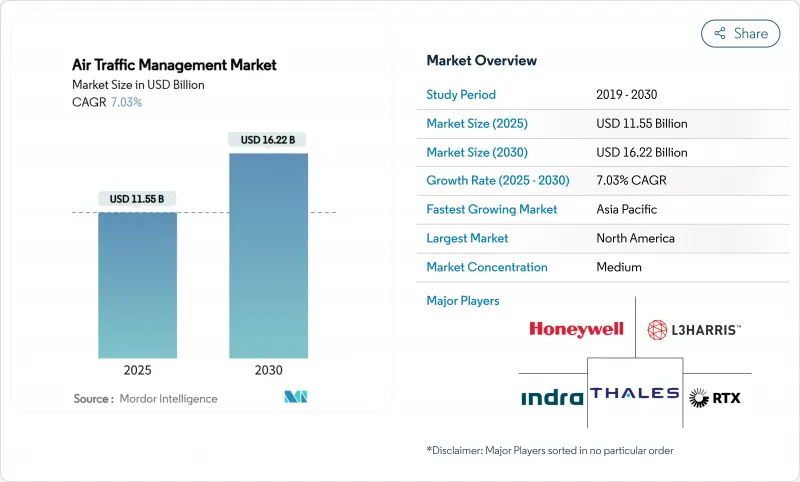

세계의 항공 교통 관리 시장 규모는 2025년에 115억 5,000만 달러로 평가되었고, 2030년에 162억 2,000만 달러에 이를 전망입니다.

항공 분야의 견고한 수요는 기존 인프라 교체, 위성 기반 감시 시스템 통합, 전례 없는 교통량 처리 필요성에서 비롯됩니다. 미국 연방항공청(FAA)은 313개 항공교통시설 중 285개가 여전히 인력 부족 상태임을 확인하며, 기술 도입을 가속화하는 긴급한 용량 병목 현상을 부각시켰습니다. 아시아 지역의 수십억 달러 규모 공항 프로그램 확대, 자동 종속 감시 방송(ADS-B)의 광범위한 의무화, 무인 항공기 운용 증가 등이 종합적으로 항공 교통 관리 시장의 긍정적 성장 전망을 강화하고 있습니다. 미국의 NextGen 프로그램, 유럽의 SESAR 디지털 스카이 이니셔티브, 신흥 허브 지역의 유사 투자 등 정부 지원 현대화 노력은 시스템 공급업체에 안정적인 수익 파이프라인을 제공합니다. 한편, 인공지능 기반 흐름 관리 및 클라우드 네이티브 아키텍처로의 전환은 소프트웨어 중심 혁신이 이제 항공 교통 관리 시장 내 고객 지출의 더 큰 비중을 주도하고 있음을 보여줍니다.

중동, 아프리카, 남아시아 전역에서 총 1조 달러 규모의 공항 개발 프로그램이 용량 수요를 재정의하고 항공 교통 관리 시장을 부양하고 있습니다. 에티오피아의 계획된 메가 공항 도시는 연간 1억 1천만 명의 승객을 처리할 예정이며, 이는 국가의 현재 수용 능력을 4배 이상 늘리는 것이며 확장 가능한 충돌 해결 소프트웨어에 대한 수요를 촉진할 것입니다. UAE의 350억 달러 규모의 알 막툼 국제공항 재개발은 첫날부터 차세대 ATM 기능을 내장하여 비용이 많이 드는 개조를 피합니다. 인도가 2035년까지 220개 이상의 신규 공항 건설을 목표로 함에 따라 항공 교통 관리 시장 내 상호운용 가능한 감시·항법·통신 시스템에 대한 요구가 더욱 높아지고 있습니다. 이러한 대규모 확장은 흐름 관리의 복잡성을 증폭시켜 인공지능 기반 자동화 플랫폼의 가속화된 도입을 촉진하고 있습니다.

의무적 ADS-B 장비 설치가 초기 도입국을 넘어 확산되고 있습니다. NAV CANADA는 2024년 5월 국내 B급 공역에서 ADS-B Out을 시행하며 규제 기관이 준수 기한을 단축하는 방식을 보여주었습니다. 현재 12개국이 지정된 항로에 ADS-B 규정을 적용 중이며, ICAO의 PBN 프레임워크는 구현을 조화시키기 위한 협력적 기준을 제공합니다. 유럽의 개정된 규정 2023/1770은 이전 2011년 규정이 폐지되었음에도 개조 추진력을 유지하며 항공 교통 관리 시장의 지속적인 하드웨어 및 소프트웨어 업그레이드를 보장합니다. 지역별 의무 사항의 다양성은 여전히 항공기 운영사에 도전 과제로 작용하지만, 이번 10년 동안 감시 항공 전자 장비 및 지상 인프라에 대한 지속적인 수요를 보장합니다.

2022년부터 2023년 사이 항공 관련 사이버 공격이 131% 증가한 것은 클라우드 도입과 상호 연결된 네트워크가 초래한 취약점을 부각시킵니다. 유럽항공안전청(EASA)의 향후 Part-IS 규정은 2025년까지 사이버 위험 감독을 항공 교통 안전 규정에 통합할 예정이지만, 지역별 성숙도 격차는 여전히 큽니다. 항공사를 대상으로 한 랜섬웨어 공격이 급증하고 있으며, 항공우주 OEM 업체들도 피해를 입고 있습니다. Resecurity 보고서에 따르면 해당 공격이 6배 증가한 것으로 나타났으며, 이는 운영 중인 항공 교통 관리 시장 인프라에 연쇄적 영향이 발생할 가능성을 시사합니다. 항공교통관제기관(ANSP)들이 제로 트러스트 아키텍처와 부문에 투자하고 있지만, 완전한 규정 준수를 위한 비용과 복잡성으로 인해 단기 현대화 예산이 위축되고 있습니다.

항공 교통 관제(ATC)는 2024년 항공 교통 관리 시장 점유율의 50.04%를 유지하며 유인 항공의 안전성과 효율성 유지에 있어 그 기초적 역할을 강조했습니다. 무인 교통 관리(UTM)는 규제 기관이 시야를 벗어난 드론 비행을 허용함에 따라 연평균 9.45%의 성장률을 보이며 확장 중이며, 통합 소프트웨어는 미래 수용 능력에 필수적입니다. ATC에 할당된 항공 교통 관리 시장 규모는 절대적으로 계속 성장하고 있지만, UTM 플랫폼이 국가 예산에서 자금 우선순위를 얻음에 따라 그 점유율은 완화될 것입니다.

통합 상황 인식 대시보드 수요 증가로 항공 교통 흐름 및 용량 관리(ATFCM)와 항공 정보 관리(AIM) 플랫폼이 핵심 ATC 기능과 점차 융합되고 있습니다. 탈레스의 TopSky와 같은 통합 솔루션은 유인·무인 항공기 통합 감시를 제공하여 항공 교통 관리 시장 내 벤더 종속성 강화 기회를 확대하고 있습니다.

2024년 항공 교통 관리 시장 규모에서 하드웨어는 67.21%를 차지했으며, 이는 의무화된 레이더 업그레이드, 디지털 무선 통신 장비, 감시 센서 수요를 반영한 것입니다. 그러나 소프트웨어는 AI 의사 결정 지원, 클라우드 호스팅, 데이터 분석 모듈이 배포 후 가치를 더함에 따라 연평균 8.21% 성장률로 가장 빠르게 성장하는 구성 요소다. 서비스 수익은 ANSP(항공 교통 서비스 제공자)가 복잡성 관리를 위해 라이프사이클 지원을 아웃소싱함에 따라 함께 확대됩니다.

소프트웨어 정의 아키텍처는 현장 방문 없이도 신속한 기능 배포를 가능하게 하여 투자 회수 기간을 단축하고 자본 지출(CapEx)에서 운영 지출(OpEx)로의 전환을 촉진합니다. 이 모델은 기존 업체와 신규 진입자들이 개방형 API와 지속적 전달 파이프라인을 우선시하도록 유도하여 광범위한 항공 교통 관리 시장의 경쟁 구도를 재편하고 있습니다.

2024년 북미는 FAA의 NextGen 프로그램이 지속해서 측정 가능한 용량 및 연료 절감 효과를 창출함에 따라 항공 교통 관리 시장 점유율 30.20%를 유지했습니다. 그러나 285개 시설의 인력 부족으로 드러난 관제사 부족 문제는 연방 예산의 자본 배분 증가에도 불구하고 단기 처리량을 제약하고 있습니다. 캐나다는 인드라(Indra)와의 궤적 기반 운영 협력 계약 및 진행 중인 UTM 시험을 통해 차세대 서비스에 대한 지역적 의지를 강화하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 8.45%의 성장률로 가장 빠르게 성장하는 지역으로, 나리타 공항의 연간 운항 편수 증가(30만 편에서 50만 편으로)와 같은 공항 수용 능력 확장에 힘입어 성장하고 있습니다. 인도가 2035년까지 220개 이상의 공항을 추가로 구축하고 드론 물류 전용 통로를 신설함에 따라 상당한 규모의 항공 교통 관리 시장이 열릴 전망입니다. 멜버른과 싱가포르에 위치한 탈레스 혁신 연구소와 L3해리스의 FTI 인도 게이트웨이는 글로벌 공급업체들이 고성장 수요 중심지에 근접할 수 있도록 지원합니다.

유럽은 단일 유럽 하늘 2+ 프레임워크 하의 정책 조정과 디지털화 및 지속가능성을 강조하는 개정된 SESAR 투자 계획의 혜택을 누립니다. 대륙 교통량의 14%를 담당하는 COOPANS의 TopSky-ATC One 전환 사례는 협력적 조달이 소규모 항공교통관제기관(ANSP)이 최고 수준의 솔루션을 확보하는 데 어떻게 기여하는지 보여줍니다. 의무화된 지속가능 연료 혼합을 포함한 환경적 우선순위는 EU 차원의 탈탄소화 목표와 부합하는 비행 경로 최적화 애플리케이션에 대한 인센티브를 제공하여 항공 교통 관리 시장 내 지출 증가를 촉진합니다.

The global air traffic management market size is estimated at USD 11.55 billion in 2025, and is projected to reach USD 16.22 billion by 2030, translating into a steady 7.03% CAGR over the forecast period.

Robust demand stems from the aviation sector's need to replace legacy infrastructure, integrate satellite-based surveillance, and handle unprecedented traffic volumes. The Federal Aviation Administration (FAA) confirms that 285 of its 313 air traffic facilities remain understaffed, highlighting urgent capacity bottlenecks that accelerate technology procurement. Expansion of multi-billion-dollar airport programs in Asia, widespread mandates for Automatic Dependent Surveillance-Broadcast (ADS-B), and increasing unmanned aircraft operations collectively reinforce the positive growth outlook for the air traffic management market. Government-funded modernization efforts such as the United States' NextGen program, Europe's SESAR Digital Sky initiative, and similar investments across emerging hubs provide a stable revenue pipeline for system suppliers. Meanwhile, the shift toward AI-enabled flow management and cloud-native architectures illustrates how software-centric innovation now drives a larger share of customer spending within the air traffic management market.

Airport development programs valued at USD 1 trillion across the Middle East, Africa, and South Asia are redefining capacity needs and boosting the air traffic management market. Ethiopia's planned mega-airport city will handle 110 million passengers annually-more than quadrupling the nation's current capacity-and drive demand for scalable conflict-resolution software. The USD 35 billion Al Maktoum International Airport redevelopment in the UAE embeds next-generation ATM capability from day one, avoiding costly retrofits. India's target of over 220 new airports by 2035 further elevates the requirement for interoperable surveillance, navigation, and communication systems within the air traffic management market. These large-scale expansions amplify the complexity of flow management, spurring accelerated deployment of AI-enabled automation platforms.

Mandatory ADS-B equipage continues to spread beyond early adopters. NAV CANADA enforced ADS-B Out in domestic Class B airspace in May 2024, illustrating how regulators compress compliance timelines. Twelve nations now impose ADS-B rules for designated corridors, while ICAO's PBN framework provides collaborative benchmarks to harmonize implementation. Europe's updated Regulation 2023/1770 sustains retrofit momentum despite the repeal of the earlier 2011 rule, ensuring continued hardware and software upgrades for the air traffic management market. The variability of regional mandates still challenges fleet operators, but it guarantees sustained demand for surveillance avionics and ground infrastructure through the decade.

A 131% rise in aviation-related cyberattacks between 2022 and 2023 underscores vulnerabilities created by cloud adoption and interconnected networks. EASA's forthcoming Part-IS regulation will integrate cyber-risk oversight into air traffic safety rules by 2025, but maturity gaps across regions remain significant. Ransomware campaigns against airlines and aerospace OEMs, including a six-fold increase reported by Resecurity, indicate the potential for cascade effects on operational air traffic management market infrastructure. While ANSPs invest in zero-trust architectures and segmentation, the cost and complexity of full compliance dampen short-term modernization budgets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Air Traffic Control (ATC) retained 50.04% of the air traffic management market share in 2024, underscoring its foundational role in keeping manned aviation safe and efficient. Unmanned Traffic Management (UTM) is expanding at a 9.45% CAGR as regulators clear beyond-visual-line-of-sight drone flights, making integration software essential for future capacity. The Air Traffic Management market size allocated to ATC continues to grow in absolute terms, but its share will moderate as UTM platforms gain funding priority in national budgets.

Air Traffic Flow and Capacity Management (ATFCM) and Aeronautical Information Management (AIM) platforms increasingly blur with core ATC functions, driven by demand for unified situational awareness dashboards. Integrated suites like Thales's TopSky provide consolidated manned-and-unmanned oversight, reinforcing vendor lock-in opportunities in the air traffic management market.

Hardware contributed 67.21% of the air traffic management market size in 2024, reflecting mandated radar upgrades, digital radios, and surveillance sensors. Software, however, is the fastest-growing component at 8.21% CAGR, benefiting from AI decision-support, cloud hosting, and data analytics modules that add post-deployment value. Services revenue scales alongside ANSPs as they outsource lifecycle support to manage complexity.

Software-defined architectures allow rapid feature deployment without extensive site visits, shortening payback periods and catalyzing a shift from CapEx to OpEx. This model incentivizes incumbents and new entrants to prioritize open APIs and continuous delivery pipelines, reshaping competition in the broader air traffic management market.

The Air Traffic Management Market Report is Segmented by Domain (Air Traffic Control, Air Traffic Flow and Capacity Management, Aeronautical Information Management, and More), Component (Hardware, Software, and Services), Application (Communication, Navigation, Surveillance, and More), End-Use (Commercial Aviation, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 30.20% of the air traffic management market share in 2024 as the FAA's NextGen program continued to generate measurable capacity and fuel-saving benefits. However, controller shortages highlighted by 285 understaffed facilities restrain near-term throughput despite rising capital allocations from federal budgets. Canada's collaborative contracts with Indra for trajectory-based operations and ongoing UTM trials reinforce regional commitment to next-generation services.

Asia-Pacific is the fastest-growing region at an 8.45% CAGR to 2030, propelled by airport capacity expansions such as Narita's slot increase from 300,000 to 500,000 flights annually. India's rollout of more than 220 airports by 2035 and emerging drone logistics corridors unlock a sizeable addressable Air Traffic Management market. Thales innovation labs across Melbourne and Singapore, and L3Harris's FTI India gateway position global suppliers close to high-growth demand centers.

Europe benefits from policy coordination under the Single European Sky 2+ framework and a refreshed SESAR investment plan emphasizing digitization and sustainability. COOPANS' TopSky-ATC One migration, covering 14% of continental traffic, showcases how cooperative procurement helps smaller ANSPs access best-in-class solutions. Environmental priorities, including mandated sustainable fuel blending, incentivize flight-path optimization applications that align with EU-wide decarbonization goals, driving incremental spending within the air traffic management market.