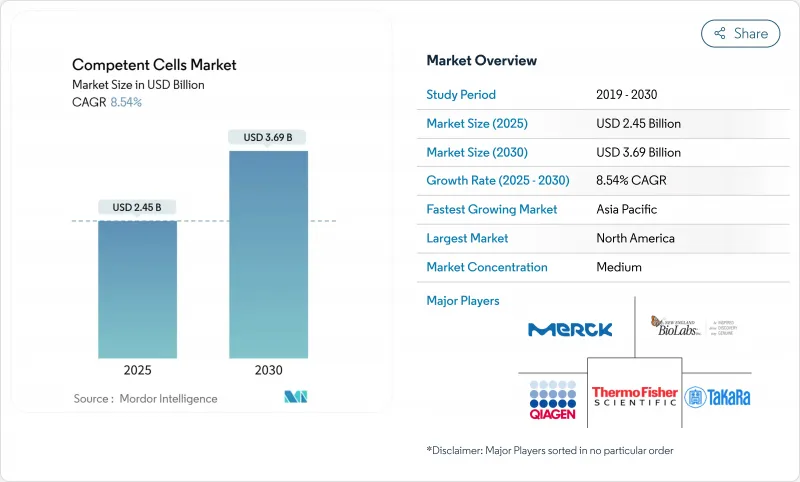

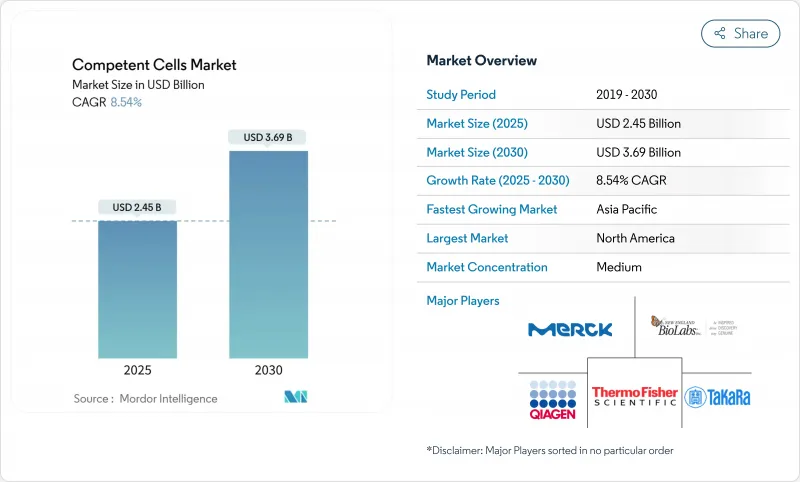

컴피턴트 셀 시장은 2025년에 24억 5,000만 달러로 추정되고, 2030년에는 36억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 8.54%로 성장할 전망입니다.

합성 생물학, 유전자 편집 플랫폼, 자동 바이오프로세싱 파이프라인에 대한 의존도가 높아짐에 따라 컴피턴트 셀은 기초 시약 클래스로 자리매김하고 있습니다. 세계의 합성 생물학 분야의 CAGR 28.3% 확대로 성장이 강화되고 대규모 플라스미드 구조를 다루는 초고효율 형질 전환 시스템 수요가 직접 증폭됩니다. CRISPR-Cas9 치료제에 대한 병행 투자, 정부 투자 바이오 파운드리, 무세포 단백질 합성의 지속적인 발전으로 맞춤형 컴피턴트 셀 포맷이 필요한 용도의 범위가 확대되고 있습니다. 실험실이 수동 벤치 절차에서 완전 자동화된 고처리량 환경으로 전환하는 동안 자동화에 적합한 패키징과 검증된 균주 성능을 갖춘 공급업체는 컴피턴트 셀 시장에서 전략적 이점을 얻고 있습니다.

정부가 지원하는 인프라 프로그램은 여러 해에 걸친 시약 지출을 고정화하고 컴피턴트 셀 시장에 예측 가능한 기준선 양을 제공합니다. 미국과학 재단의 5개 바이오파운드리에 대한 7,500만 달러의 배분은 자동화된 워크플로우를 위해 표준화된 컴피턴트 셀 로트를 재고해야 하는 상설 대용량 시설을 연구 기관에 제공하는 것입니다. 미국 국립위생연구소(National Institutes of Health)는 유전자 편집 치료제를 위해 연간 200만 달러의 예산을 추가하여 CRISPR 파이프라인에 적합한 초고효율 균주의 도입을 촉진합니다. 미·중 경제안보심사위원회에서의 정책 증언은 금세기 중반까지 바이오경제가 세계 경제 투입의 60%를 지원할 수 있을 것으로 예측되고 있으며, 장기적인 시약 수요에 유리한 공적 자금의 지속적인 투입이 강조되고 있습니다.

개발 및 제조 수탁기관(CDMO)은 2023년 198억 9,000만 달러에서 2032년에는 319억 2,000만 달러로 증가하는 생물 제제 파이프라인에 대응하기 위해 규모를 확대하고 있습니다. 업스트림 세포주 개발이 종종 하류 수율을 좌우하기 때문에 제조업체는 복잡한 플라스미드 발현 구조를 지원할 수 있는 고역가 컴피턴트 셀을 지정합니다. 아시모프의 CHO Edge 플랫폼은 5g/L 이상의 단일클론항체 역가를 보장하며, 주형 플라스미드에 대한 일관된 형질전환 효율에 의존하는 예측 가능한 균주 성능으로의 업계의 시프트를 시사하고 있습니다. Sutro Biopharma에 의해 4,500L 규모로 확장된 무세포 발현 시스템은 시험관내 단백질 합성을 위해 조정된 특수한 유능한 세포의 대응가능한 시장을 더욱 확대하고 있습니다.

바이오 의약품의 승인 1건에 걸리는 개발비의 중앙값은 23억 달러로, 스폰서는 모든 시약 클래스에서 비효율을 배제할 필요에 강요되고 있습니다. 단클론 항체의 경우 캡처 크로마토그래피만으로 총 비용의 25%를 차지할 수 있습니다. GMP 등급의 플라스미드 수요를 4에서 1로 줄이는 안정적인 생산자 세포주는 유능한 세포 설계와 관련된 경제적 레버리지의 명확한 증거를 제공합니다. 이러한 경제성은 개발 비용을 세계 생산량으로 상각할 수 없는 소규모 공급업체에게 마진 압박을 제공합니다.

화학적으로 제조된 균주는 2024년에 65.65%의 매출을 기록했습니다. 비용 효율적인 제조와 자본 설비가 제한된 교육 연구실에 적합한 알기 쉬운 염화칼슘 프로토콜이 이를 지원합니다. 표준 제품은 일상적인 분자 클로닝에 충분한 1×10^6cfu/μg의 효율을 제공하며, 유능한 세포 시장의 강력한 수량 기준을 유지합니다. 그러나 일렉트로 컴피턴트 포맷은 일관된 서브마이크로리터의 분주를 필요로 하는 자동 일렉트로포레이션 플랫폼에 견인되어 CAGR이 가장 빨리 9.21%를 기록합니다. 매우 요구되는 CRISPR 파이프라인에서 주요 일렉트로컴피턴트 제품은 5 X 10^9cfu/마이크로그램 이상의 효율을 인증하고 있으며, 이는 대부분의 화학적 동등품의 상한을 초과합니다. 실험실이 로봇에 의한 액체 취급 처리량에 맞게 형질전환 단계를 자동화함에 따라 일렉트로 컴피턴트 제품의 컴피턴트 셀 시장 규모는 2030년까지 6억 5,000만 달러 이상에 달할 것으로 예측되고 있습니다.

화학적 기법의 혁신은 계속되고 있습니다. recA 균주인 대장균 BW25113은 최적화된 화학 프로토콜을 이용하여 XL1-Blue MRF'의 100배의 형질 전환을 달성하고 대형 플라스미드의 클로닝 성공률로 440배에서 1267배의 향상을 기록하고 있습니다. 이러한 성능은 기존의 일렉트로포레이션에 의한 효율 격차를 없애고 일렉트로포레이터가 없는 연구기관에도 어필합니다. 따라서 컴피턴트 셀 시장은 화학 형식의 비용 우위 및 일렉트로 컴피턴트 라인의 성능 향상과 자동화의 매력의 균형을 맞추고 있습니다.

북미는 생명과학 분야의 풍부한 자금, 규제의 명확성, GMP 시설의 밀집한 네트워크로 2024년 매출의 42.31%를 차지했습니다. Thermofisher Scientific은 37개 주 64곳의 생산 기지에 20억 달러를 투자할 것으로 밝혀졌으며, 프리미엄 컴피턴트 셀룰로트의 대규모 콜오프를 보장하는 현지 바이오프로세스 능력을 확보하고 있습니다. 세포 기질의 특성화에 대한 FDA 지침은 품질 기준을 추가로 표준화하고, 로트 불합격의 위험을 줄이며, 추적 가능한 공급망을 가진 국내 공급업체를 선호합니다. 북미의 컴피턴트 셀 시장 규모는 CRISPR 치료제의 후기 임상시험 시작과 함께 2030년까지 16억 달러 이상에 달할 것으로 예측됩니다.

아시아태평양은 성장 엔진이며 2030년까지 연평균 복합 성장률(CAGR)은 9.43%입니다. 일본은 2030년까지 생명공학 생산량을 3배의 15조엔으로 하는 것을 목표로 하고 있으며, 포유류나 세균의 워크플로우용으로 커스터마이즈된 플랫폼주에 자금을 제공하는 로컬 벤처 라운드를 지원하고 있습니다. 중국의 동남아시아 제조 회랑으로의 축족은 지정학적 역풍에 대한 헤지가 되어 6억 명의 잠재 환자를 저비용의 생물제제 공장에 연결시킵니다. 인도의 생물제제 로드맵은 2025년까지 120억 달러의 가치를 목표로 하고 있으며, 바이오시밀러에 대한 정책적 인센티브는 자동화 대응의 유능한 세포를 대규모로 조달하는 현지 CDMO에 활력을 줍니다.

유럽에서는 독일, 아일랜드, 스위스에 제약 허브가 정착되어 꾸준한 흡수를 유지하고 있습니다. 호비온과 iBET의 벤처 기업인 ViSync Technologies는 복잡한 생물학적 제제의 안정성 및 배달 장애물을 해결하기 위해 위탁 제제 제조업체가 학술 기관과 팀을 구성하는 방법을 보여줍니다. 첨단 치료제에 대한 EMA 지침이 FDA 기준에 부합하여 대서양을 넘어 공급업체 인증이 용이해집니다. EU가 자금을 지원하는 Horizon 프로젝트는 산업용 바이오 제조에 대학 참여를 장려하고 연구 등급의 컴피턴트 셀에 대한 기준 수요를 늘리고 있습니다. 이러한 지역적 협력으로 인구 증가의 둔화에도 불구하고 유럽의 컴피턴트 셀 시장은 균형 잡힌 궤도를 유지하고 있습니다.

The competent cells market stood at USD 2.45 billion in 2025 and is forecast to climb to USD 3.69 billion by 2030, advancing at an 8.54% CAGR over the period.

Increasing reliance on synthetic biology, gene-editing platforms, and automated bioprocessing pipelines positions competent cells as a foundational reagent class. Growth is reinforced by the 28.3% CAGR expansion of the global synthetic biology sector, which directly amplifies demand for ultra-high-efficiency transformation systems that can handle large plasmid constructs. Parallel investments in CRISPR-Cas9 therapeutics, government-funded biofoundries, and continuous advances in cell-free protein synthesis broaden the scope of applications that require tailored competent cell formats. As laboratories transition from manual bench procedures to fully automated high-throughput environments, suppliers with automation-friendly packaging and validated strain performance gain a strategic edge in the competent cells market.

Government-backed infrastructure programs have locked in multiyear reagent spending, giving the competent cells market predictable baseline volumes. The National Science Foundation's USD 75 million allocation to five biofoundries equips institutions with permanent, high-capacity facilities that must stock standardized competent cell lots for automated workflows . The National Institutes of Health adds a focused USD 2 million annual stream for genome-editing therapeutics, stimulating uptake of ultra-high-efficiency strains suitable for CRISPR pipelines . Policy testimony before the U.S.-China Economic and Security Review Commission projects that the bio-economy could underpin 60% of global economic inputs by mid-century, underscoring continued public financing that favors long-term reagent demand.

Contract development and manufacturing organizations (CDMOs) are scaling to meet a biologics pipeline that rose from USD 19.89 billion in 2023 toward USD 31.92 billion by 2032. As upstream cell line development often dictates downstream yields, manufacturers specify high-titer competent cells capable of supporting complex plasmid expression constructs. Asimov's CHO Edge platform guarantees >= 5 g/L monoclonal antibody titers, signaling an industry shift toward predictable strain performance that relies on consistent transformation efficiency for template plasmids. Cell-free expression systems taken to 4,500 L scale by Sutro Biopharma further widen the addressable market for specialized competent cells tuned for in vitro protein synthesis.

A single biopharmaceutical approval carries a median USD 2.3 billion development price tag, which forces sponsors to eliminate inefficiencies across every reagent class. For monoclonal antibodies, capture chromatography alone can swallow 25% of total cost of goods; upstream strain choice therefore receives intense scrutiny. Stable producer cell lines that cut GMP-grade plasmid demand from four to one provide clear evidence of the economic leverage tied to competent cell design. These economics place margin pressure on smaller vendors that cannot amortize development costs across global volumes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Chemically prepared strains contributed 65.65% revenue in 2024, supported by cost-efficient manufacturing and straightforward calcium chloride protocols that suit teaching laboratories with limited capital equipment. Standard products deliver 1 X 106 cfu/µg efficiency sufficient for routine molecular cloning, preserving the strong volume base of the competent cells market. Electrocompetent formats, however, post the quickest 9.21% CAGR, driven by automated electroporation platforms that need consistent sub-microliter aliquots. For ultra-demanding CRISPR pipelines, leading electrocompetent offerings certify efficiencies above 5 X 10⁹ cfu/µg, which outpaces the ceiling of most chemical counterparts. The competent cells market size for electrocompetent products is forecast to add USD 650 million through 2030 as labs automate transformation steps to match robotic liquid handling throughput.

Innovation within chemical methods continues. Escherichia coli BW25113, a recA+ strain, achieves 100-fold improvements in transformation over XL1-Blue MRF' using an optimized chemical protocol, and records 440- to 1,267-fold boosts in cloning success for large plasmids. Such performance erodes the traditional efficiency gap with electroporation and appeals to institutes lacking electroporators. The competent cells market therefore balances the entrenched cost advantage of chemical formats with the rising performance and automation appeal of electrocompetent lines.

The Competent Cells Market Report is Segmented by Type (Chemically Competent Cells, Electrocompetent Cells), Application (Protein Expression, Cloning & Sub-Cloning, Mutagenesis, Others), End User (Biopharmaceutical Companies, Academic and Research Institutes, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America anchors 42.31% of 2024 revenue owing to deep life-science capital pools, robust regulatory clarity, and a dense network of GMP facilities. Thermo Fisher Scientific's pledge to invest USD 2 billion across 64 manufacturing sites in 37 states secures local bioprocessing capacity that guarantees large call-offs for premium competent cell lots. FDA guidance on cell-substrate characterization further standardizes quality benchmarks, reducing lot rejection risk and favoring domestic suppliers with traceable supply chains. The competent cells market size in North America is projected to surpass USD 1.6 billion by 2030 as CRISPR therapeutics enter late-phase trials.

Asia-Pacific is the growth engine, advancing at 9.43% CAGR through 2030. Japan aims to triple its biotechnology output to 15 trillion yen by 2030, supporting local venture rounds that finance platform strains customized for mammalian and bacterial workflows. China's pivot toward Southeast Asian manufacturing corridors hedges against geopolitical headwinds, linking 600 million potential patients to lower-cost biologics factories. India's biologics roadmap targets USD 12 billion value by 2025, and policy incentives for biosimilars energize local CDMOs that procure automation-ready competent cells at scale.

Europe sustains steady uptake through entrenched pharmaceutical hubs in Germany, Ireland, and Switzerland. The Hovione-iBET venture ViSync Technologies demonstrates how contract formulators team with academic institutes to solve stability and delivery hurdles for complex biologics. EMA guidelines on advanced therapy medicinal products align with FDA standards, facilitating trans-Atlantic supplier qualification. EU-funded Horizon projects encourage university participation in industrial biomanufacturing, lifting baseline demand for research-grade competent cells. Collectively, regional cooperation keeps the competent cells market in Europe on a balanced trajectory despite slower underlying population growth.