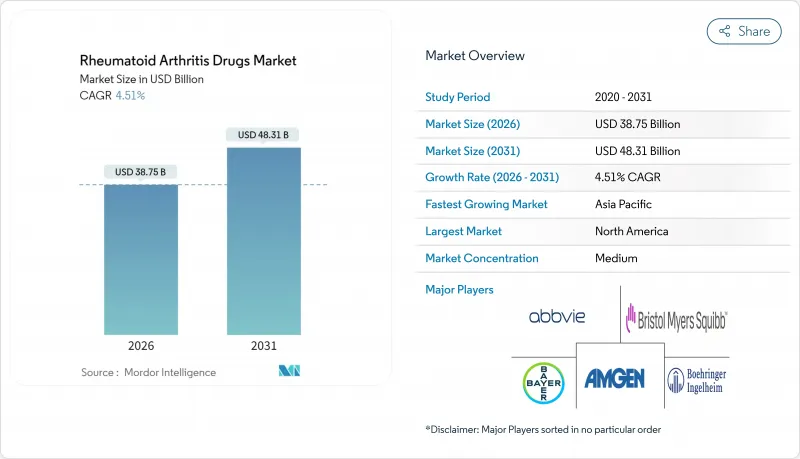

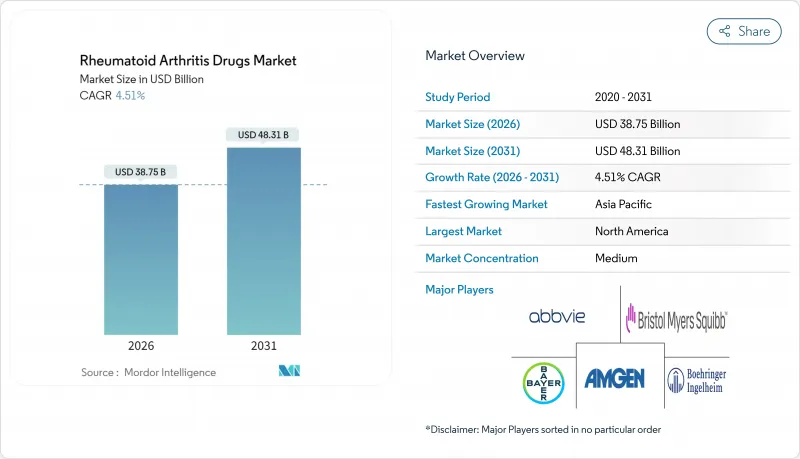

2026년 류마티스 관절염 치료제 시장 규모는 387억 5,000만 달러로 추정되며, 2025년 370억 8,000만 달러에서 성장을 계속하고 있습니다.

2031년까지의 예측으로는 483억 1,000만 달러에 이르고, 2026년부터 2031년에 걸쳐 CAGR 4.51%를 나타낼 것으로 예상됩니다.

이 성장 궤적은 차세대 바이오 의약품이 바이오시밀러 진입에 의한 수익 압축을 상쇄하는 한편, 지속적인 질병 유병률이 수요를 지지하는 성숙한 시장 환경을 반영하고 있습니다. 10유형의 아달리무마브 바이오시밀러가 미국 및 EU 시장에 진입함에 따라 경쟁 구도는 격화되고 있지만, 비메키주맙이나 우파다시티닙 등 정밀 설계된 바이오의약품은 프리미엄 가격 설정과 급속한 보급을 유지하고 있습니다. 보험 적용 범위 확대, 가격 협상 프레임워크, 중국의 수량 기준 조달 체계로 환자 접근이 확대되는 한편, 증상 추적과 전자 기록을 통합한 디지털 헬스툴이 조기 진단과 치료 최적화를 지원하고 있습니다. 한편, 각사는 방어적 합병과 파이프라인의 다양화를 추진하고 있으며, 아비사만으로도 2024년 초부터 바이오시밀러에 의한 수익 침식을 완화하고 장기 성장을 위한 재배치를 도모하기 위해 220억 달러 이상을 인수에 투입했습니다.

인구동태의 변화에 의해 세계적으로 고령자의 비율이 증가하는 가운데, 연령 조정 이환율은 상승을 계속하고 있습니다. 카타르 등 사회인구통계지수가 높은 국가에서는 가장 급격한 발생률이 기록되고 있지만 진단능력 향상에 따라 신흥 시장에서도 비슷한 동향을 볼 수 있습니다. 미국에서는 환자 1인당 연간 평균 직접 비용이 2만 4,068달러에 이르고, 비RA 환자군의 4배 이상으로 상승합니다. 이 경제적 부담은 효과적인 장기 치료에 대한 수요를 지원하고 류마티스 관절염 치료제 시장의 수량 성장을 뒷받침하고 있습니다. 선진국에서는 의료 시스템의 정비가 진행되어 생물학적 제제의 도입이 가속되는 한편, 저소득 지역에서는 전문 의료에 대한 자금 배분이 증가하는 경향이 있습니다.

2025년 초에 비메키주맙 등에 대한 FDA 승인은 기존의 TNF 억제를 넘어선 치료 옵션을 확대합니다. 업데이트된 규제 지침은 시험 설계를 간소화하면서, 특히 안전 경고 후 야누스 키나제 억제제에 대한 시판 후 모니터링을 유지합니다. 거세포성 동맥염에서 우파다시티닙의 EU 승인은 전체 염증성 질환에 대한 플랫폼 확장을 뒷받침합니다. 임상의는 표적 약물과 예후 바이오마커의 병용을 증가시키고 있으며, 관해율의 향상과 고액 치료비에 대한 지불 의향 증가로 이어지고 있습니다. 이러한 신규 승인은 기존 생물학적 제제의 독점권 상실과 함께 파이프라인을 새롭게 함으로써 류마티스 관절염 치료제 시장을 활성화시킵니다.

생물학적 제제를 이용한 DMARD의 연간 평균 치료비는 3만 6,053달러인 반면 기존 요법에서는 1만 2,509달러이며, 지불자의 예산과 환자의 부담능력에 압박이 걸려 있습니다. 미국 민간 보험 가입자의 자기 부담액은 4배로 증가했으며 HMO 플랜에서는 특히 급격한 상승이 보였습니다. 바이오시밀러는 85% 할인으로 제공될 수 있지만 리베이트 구조와 보험 적용 부족으로 인해 실제 절약 효과가 상쇄되는 경우가 많으며 시장 침투는 제한적입니다. 신흥국에서는 불충분한 상환제도가 접근을 더욱 제한하고 있으며, 잠재적인 수요에도 불구하고 류마티스 관절염 치료제 시장의 성장을 억제하고 있습니다.

2025년 시점에서 바이오의약품은 류마티스 관절염 치료제 시장의 67.48%를 차지했으며, 2031년까지 8.76%라는 가장 빠른 CAGR을 나타낼 것으로 전망되고 있습니다. 이것은 리산 키주맙과 같은 블록버스터 항체 약물과 차세대 플랫폼의 지속적인 투입을 지원합니다. 바이오시밀러의 침투가 진행되고 있는 가운데, 이 부문은 견조한 수요를 유지하고 있습니다. 특히 아비의 스카이리지와 림복은 2025년 1분기에 총 51억 4,000만 달러의 매출을 달성했으며, 특허 가까이에 있는 TNF 억제제 사업으로부터의 전략적 전환이 옳다는 것을 증명했습니다. 기존의 저분자 DMARD를 중심으로 하는 의약품은 기초적인 임상적 역할을 유지하고 있지만, 난치성 질환에 대한 처방의의 표적 치료제로의 이행에 의해 성장이 완만해질 전망입니다.

미래의 성과는 파이프라인의 두께와 특허 관리에 달려 있습니다. 항CD79b 항체와 세포독성 약제를 결합시킨 항체 약물 복합체는 전신성 면역억제를 억제하면서 항염증 작용을 발휘하는 신규 모달리티의 좋은 예입니다. 한편, 머크사가 취득한 초기 단계의 B세포 고갈요법은 면역학 분야에 대한 지속적인 자본 배분을 시사하고 있습니다. 바이오시밀러의 가격 우위성이 확대되는 가운데, 창약기업은 뛰어난 편의성, 광범위한 적응증 확대, 동반진단 전략에 의한 차별화를 도모해, 류마티스 관절염 치료제 시장에서의 프리미엄 가격의 유지와 라이프사이클 가치의 연장을 목표로 하고 있습니다.

2025년 시점에서 DMARDs는 46.02% 시장 점유율을 차지하고 11.34%의 연평균 복합 성장률(CAGR) 예측을 기록했습니다. 이것은 JAK, TYK2, IRAK4 억제제와 같은 기존의 표준 치료보다 효과적으로 구조적 손상을 방지하는 표적 합성 돌연변이의 확대에 견인되었습니다. 메토트렉세이트는 제1선택제로서의 지위를 유지하고 있지만, 치료효과 불충분한 환자에 대해 처방의가 JAK 억제제로 이행했기 때문에 2025년 점유율은 34%로 저하되었습니다. 토실리주맙과 같은 인터루킨-6 억제제는 만성 치료에서 중요한 지표인 실제 임상 지속률에서 TNF 억제제를 초과하는 업적을 보여줍니다.

DMARD(질환-변형성 류마티스 약물) 시장 규모는 규제적 신속 승인 과정 및 바이오마커 기반 용량의 최적화로 확대되고 있습니다. m6A 메틸화 억제를 이용한 병용 요법은 뼈의 건전성 유지에 전임상 단계에서 유망한 결과를 보여줍니다. NSAIDs(비스테로이드성 항염증제)와 코르티코스테로이드는 교량요법이나 보조요법으로서의 역할이 증가하고 있습니다만, 안전성 감시 프로그램에 의해 사용량은 억제되고 있습니다. DMARD의 혁신은 종합적으로 정밀의료로의 결정적인 전환을 강조하고 이 부문의 핵심 지위를 더욱 확고히 하고 있습니다.

북미는 2025년 견고한 상환제도와 고부가가치치료법의 조기 도입을 배경으로 류마티스 관절염 치료제 시장의 40.92% 점유율을 유지했습니다. 미국에서는 2025년 메디케어 파트 D 상한 적용 전 류마티스 관절염 환자(메디케어 수급자)의 연간 약물 관련 비용이 2만 3,544달러에 이르렀고, 고정 수입의 고령층에서의 비용 감도의 높이가 부각되었습니다. 1년간 10유형의 휴미라 바이오시밀러가 출시되었으며, 아비의 미국 매출은 감소했고 환자의 접근성은 확대되었습니다. 한편, 캐나다의 지불기관은 지출억제를 위해, 단계적인 바이오시밀러 전환 정책을 채용하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.12%로 가장 높은 성장률을 나타낼 전망입니다. 중국에서는 수량 기준의 조달 틀이 가격 인하와 국내 제조 촉진을 동시에 실현하여 바이오 의약품의 생산을 지원하고 있습니다. 일본에서는 연령층별 이용 상황에 미묘한 차이가 보이고, 생물학적 제제의 사용률은 젊은층의 50.9%에서 80대에서는 13.7%로 저하됩니다. 이는 안전에 대한 우려와 비용 상쇄 전략을 반영합니다. 인도에서는 국민건강보험(아유슈만 바랏)의 도입과 전자약국의 급속한 확대가 마찬가지로 기초 수요를 밀어 올리고 있습니다.

유럽에서는 중앙 집권 규제 경로와 핀란드 약국 대체 법안과 같은 바이오 시밀러에 우호적 인 법률로 꾸준한 한 자리 성장이 예상됩니다. 각국의 의료기술평가기관은 비용효과를 점점 더 중시하고 있으며, 바이오시밀러의 토실리주맙과 인플릭시맙의 보급을 가속화하고 있습니다. 라틴아메리카, 중동 및 아프리카에서는 새로운 성장이 예상됩니다. 브라질 및 걸프 협력 회의(GCC) 국가에서는 민간 보험의 확대와 전문의의 능력 향상으로 베이스가 작고 치료 보급률이 향상되고 있습니다.

Rheumatoid Arthritis Drugs Market size in 2026 is estimated at USD 38.75 billion, growing from 2025 value of USD 37.08 billion with 2031 projections showing USD 48.31 billion, growing at 4.51% CAGR over 2026-2031.

This trajectory reflects a maturing landscape in which next-generation biologics offset revenue compression from biosimilar entry while sustained disease prevalence underpins demand. Competitive intensity has grown as ten adalimumab biosimilars reached US and EU markets, yet precision-engineered biologics such as bimekizumab and upadacitinib continue to secure premium pricing and rapid uptake. Broader insurance coverage, price negotiation frameworks, and China's volume-based procurement schemes are widening patient access, while digital health tools that integrate symptom tracking with electronic records support earlier diagnosis and therapy optimization. Meanwhile, companies pursue defensive mergers and pipeline diversification-AbbVie alone spent more than USD 22 billion on acquisitions since early 2024 to mitigate biosimilar erosion and reposition for long-term growth.

Age-standardized prevalence continues to climb as demographic transition increases the proportion of older adults worldwide. High socio-demographic index countries such as Qatar log the steepest incidence, yet emerging markets now see parallel trends as diagnostic capacity improves. In the United States, average annual direct costs reach USD 24,068 per patient, more than quadruple non-RA cohorts. This economic burden sustains demand for efficacious long-term therapies, reinforcing volume growth for the rheumatoid arthritis drugs market. Health-system readiness in developed countries accelerates biologic adoption, while lower-income regions increasingly allocate funds to specialty care.

FDA authorizations for agents such as bimekizumab in early 2025 broaden therapeutic choice beyond traditional TNF inhibition. Updated regulatory guidance streamlines trial design yet maintains post-market vigilance, especially for Janus-kinase inhibitors after safety warnings. Upadacitinib's EU clearance in giant cell arteritis underscores platform extension across inflammatory diseases. Clinicians increasingly combine targeted agents with prognostic biomarkers, improving remission rates and fueling premium willingness to pay. These novel approvals energize the rheumatoid arthritis drugs market by refreshing pipelines as legacy biologics lose exclusivity.

Annual biologic DMARD spending averages USD 36,053 versus USD 12,509 for conventional therapy, straining payer budgets and patient affordability. Private-insurance out-of-pocket obligations for US patients quadrupled, with HMO plans seeing the steepest hikes. Although biosimilars sometimes list at 85% discounts, rebate structures and coverage gaps often negate savings, limiting real-world penetration. In emerging economies, inadequate reimbursement frameworks further restrict access, tempering growth in the rheumatoid arthritis drugs market despite underlying demand.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Biopharmaceuticals controlled 67.48% of the rheumatoid arthritis drugs market in 2025 and generated the fastest 8.76% CAGR outlook through 2031, underpinned by blockbuster antibodies like risankizumab and the continual launch of next-generation platforms. The segment reflects robust uptake even as biosimilar infiltration intensifies. Notably, AbbVie's Skyrizi and Rinvoq together delivered USD 5.14 billion in Q1 2025, validating strategic pivoting away from expiring TNF franchises. Pharmaceuticals, chiefly conventional small-molecule DMARDs retain a foundational clinical role yet face moderated growth as prescribers migrate to targeted agents for refractory disease.

Future performance hinges on pipeline depth and patent stewardship. Antibody-drug conjugates that twin anti-CD79b antibodies with cytotoxics illustrate how novel modalities can deliver anti-inflammatory action while limiting systemic immunosuppression. Meanwhile, early-stage B-cell depletion therapies acquired by Merck signal sustained capital allocation to immunology. As biosimilar discounts gain traction, innovators seek differentiation via superior convenience, broader label indications, and companion diagnostics tactics likely to preserve premium pricing and extend lifecycle value within the rheumatoid arthritis drugs market.

DMARDs commanded a 46.02% market share in 2025 while recording an 11.34% CAGR forecast, propelled by the expansion of targeted synthetic variants such as JAK, TYK2, and IRAK4 inhibitors that halt structural damage more effectively than historical standards. Methotrexate remains the first-line anchor, yet its share slipped to 34% in 2025 as prescribers escalated to JAK inhibitors for inadequate responders. Interleukin-6 inhibitors like tocilizumab outperform TNF inhibitors in real-world persistence, a key metric in chronic therapy.

The rheumatoid arthritis drugs market size for DMARDs, buoyed by regulatory fast-track pathways and biomarker-guided dosing. Combination regimens exploiting m6A methylation suppression show preclinical promise in preserving bone integrity. NSAIDs and corticosteroids increasingly serve as bridging or adjunctive agents, their volume tempered by safety surveillance programs. Collectively, DMARD innovation underscores a decisive shift toward precision medicine, further cementing the segment's centrality.

The Rheumatoid Arthritis Drugs Market Report is Segmented by Type of Molecule (Pharmaceuticals, Biopharmaceuticals), Drug Class (Non-Steroidal Anti-Inflammatory Drugs, and More), Route of Administration (Oral, Parenteral, Topical), End User (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 40.92% share of the rheumatoid arthritis drugs market in 2025, supported by robust reimbursement and early adoption of premium therapies. In the United States, Medicare beneficiaries with rheumatoid arthritis incurred USD 23,544 annual drug-related costs before the 2025 Medicare Part D cap, highlighting cost sensitivity among fixed-income seniors. Ten Humira biosimilars launched within a single year, trimming AbbVie's US sales yet broadening patient access, while Canadian payers adopt tiered biosimilar switching policies to curb expenditure.

Asia-Pacific registers the highest 9.12% CAGR through 2031. China's biopharmaceutical output, supported by a volume-based procurement framework that simultaneously lowers prices and incentivizes domestic manufacturing. Japan presents nuanced age-stratified utilization, with biologic use tapering from 50.9% in youth to 13.7% in octogenarians, reflecting safety concerns and cost-offset strategies. India's rollout of national health insurance (Ayushman Bharat) and rapid e-pharmacy expansion similarly lift baseline demand.

Europe contributes steady single-digit growth, anchored by centralized regulatory pathways and biosimilar-friendly legislation such as Finland's pharmacy substitution bill. National health technology assessment agencies increasingly favor cost-effectiveness, accelerating the uptake of biosimilar tocilizumab and infliximab. Latin America and the Middle East and Africa offer emerging upside; expanding private insurance in Brazil and Gulf Cooperation Council countries, coupled with rising specialist capacity, improves treatment penetration, albeit from a smaller base.