유럽의 민간 항공기 객실 좌석 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Commercial Aircraft Cabin Seating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693709

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

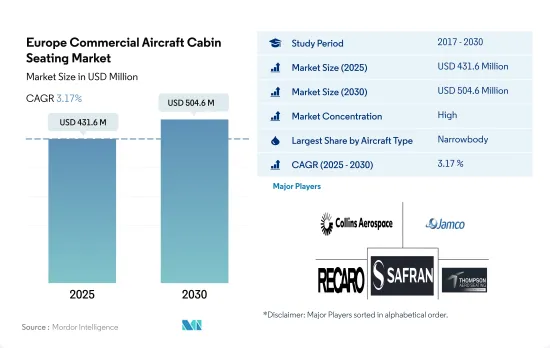

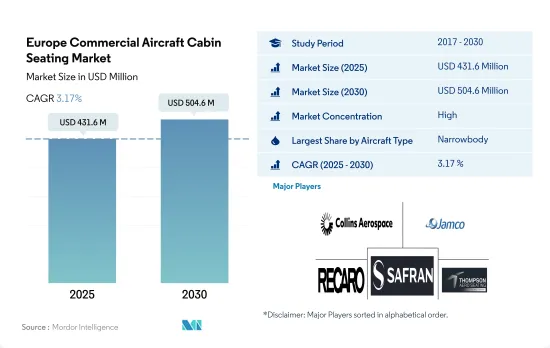

유럽의 민간 항공기 객실 좌석 시장 규모는 2025년 4억 3,160만 달러로 추정되고, 2030년에는 5억 460만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 3.17%로 성장할 것으로 예측됩니다.

유럽에서는 기술적 특성이 개선되고 승객의 여행 편의성이 향상된 항공기 좌석 수요가 급증할 것으로 예상

최신 세대의 항공기용 좌석는 연료비를 삭감하고 항공기의 지속가능성을 높이기 위해 경량의 비금속 재료로 만들어져 경량 설계가 되어 있습니다.

비즈니스 클래스에 대한 기호가 높아지고 있기 때문에 이코노미 클래스보다 넓은 공간을 개발한 충실한 좌석 구조가 불가결해지고 있습니다.

2017-2022년까지 협폭동체가 납입기수의 대부분을 차지해 전체의 82%를 차지했습니다.

혁신적인 객실 좌석 채용 증가, 호화로운 하늘 여행에 대한 수요 증가, 방대한 수의 항공기 주문 등의 요인이 예측 기간 중 시장을 견인할 것으로 예측됩니다.

저렴한 항공사의 급증과 승객의 좌석 체험 향상에 대한 수요가 유럽 시장의 성장을 뒷받침할 것으로 예상

항공기의 쾌적한 좌석의 중요성이 높아지고 있으며, 그 주요 이유는 더 나은 승객 경험을 제공하기 위해서입니다. 유럽 항공사는 주요 국가의 항공 여객 수송량 증가에 대응하기 위해 항공기 증비 계획을 실시했습니다.

유럽의 3대 항공사 그룹, 영국 및 스페인의 다국적 항공사 IAG, 독일의 Lufthansa와 Air France는 2023년의 좌석 용량을 대폭 개선해, 2022년에 비해 노선망 전체로 건전한 용량을 확보하고 있습니다.

민간항공기 제조업체, 즉 Boeing과 Airbus는 이 지역에서 많은 항공기를 납입할 전망입니다.

이 지역에서는 LCC의 성공률이 높습니다. Air France, British Airways, and Lufthansa 등, 이 지역의 대형 항공사는 항공기 시장에서의 여객 체험 전체의 향상에 주력하고 있습니다.

유럽 민간 항공기 객실 좌석 시장 동향

시장 성장의 주요 이유는 유럽에서 항공기 보유수의 확대와 여객항공 수요 증가입니다.

유럽은 2022년에 항공 여객 수송량이 가장 많은 2위 지역이 되었습니다. 항공사는 항공 수요 증가에 대응하기 위해 장비의 대형화에 주력하고 있으며, 그 결과 유럽에서는 신조 항공기 수요가 대폭 증가할 가능성이 있습니다.

2017-2022년 사이에 총 1,206대의 신조 항공기가 유럽에 납입되고, 2023-2030년 사이에 추가로 2,647대의 신조 제트기가 납입됨 과거에 유럽에서 새롭게 납품된 제트기는 세계의 민간 항공기 납품수의 약 25%에 달했습니다.

2023년 6월 현재 이 지역에서는 약 3,000대 이상의 Airbus기가 납품되고 있으며, 협폭동체 부문에서는 A320ceo, A320neo, A321ceo, A321neo, 광폭동체 부문에서는 A330-300, A350-900이 주요 납품이었습니다. Ryanair, Lufthansa, Wizz Air, Aeroflot Group, Air France-KLM, EasyJet 등 유럽의 대형 항공사 몇사는 협폭동체와 광폭동체 혼합기를 포함해 1,600기 이상의 항공기의 수주 잔을 안고 있습니다.

항공 여객 수송량 증가는 국내 및 국제 항공 여행 수요 증가에 의해 지원될 것으로 예측됩니다.

2022년에 유럽 각국의 여행 제한이 점차 완화됨에 따라 유럽 대륙 내 이동은 COVID-19의 유행시보다 훨씬 쉬워졌습니다. 봉쇄 기간 동안 여행할 수 없었던 여객은 국내에서 휴가를 받는 대신 다시 해외로 날아가고 싶었습니다. 그리고 2021년 대비 8%의 성장을 나타냈습니다. 영국, 독일, 스페인은 유럽 항공 여객 운송량 전체의 36%를 차지하고 있어 향후 몇 년간은 다른 유럽 국가에 비해 신형 항공기에 대한 더 많은 수요를 낳을 가능성이 있습니다.

2022년 1-6월기의 유럽 공항 이용자 수는 2021년 대비 247% 증가하여, 그 결과 유럽 대륙 전체에서 6억 6,000만 명의 여객이 증가했습니다. 항구를 옹호해 2022년 상반기 여객수는 대폭적인 성장세를 기록했습니다. 기타 유럽의 공항에서도 2022년 8월에 비슷한 항공 여객 수송량 증가가 보였습니다. 벨라루스와 러시아의 공항에서도 러시아 우크라이나 전쟁이 시작된 이래, 여객수의 감소가 기록되었습니다.

유럽 민간 항공기 객실 좌석 산업 개요

유럽의 민간 항공기 좌석 시장은 상당히 통합되어 있으며 상위 5개 기업에서 98.19%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 좌석

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

항공 여객 수송량

신규 항공기 납품 수

1인당 GDP(현행 가격)

항공기 제조업체의 매출액

항공기 수주 잔여

수주 총액

공항 건설 지출(계속 중)

항공사의 연료비

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

항공기 유형

협폭동체

광폭동체

국가명

프랑스

독일

스페인

튀르키예

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Adient Aerospace

Collins Aerospace

Expliseat

Jamco Corporation

Recaro Group

Safran

STELIA Aerospace(Airbus Atlantic Merginac)

Thompson Aero Seating

ZIM Aircraft Seating GmbH

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Europe Commercial Aircraft Cabin Seating Market size is estimated at 431.6 million USD in 2025, and is expected to reach 504.6 million USD by 2030, growing at a CAGR of 3.17% during the forecast period (2025-2030).

Europe is expected to experience a surge in demand for aircraft seats with improved technological features and enhanced passenger travel comfort

Modern-generation aircraft seats are made from lightweight, non-metallic materials and have lightweight designs to reduce fuel expenses and increase the aircraft's sustainability. The demand for seats with enhanced features and technologically based convenience is increasing, which will accelerate market expansion in the future.

An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to rising preferences for business-class travelers. Worldwide airline operators and OEMs are increasing their efforts to reduce weight and develop a sustainable way to manage the airline industry in consideration of the zero-emission 2050 goal.

During 2017-2022, narrowbody aircraft accounted for the majority of deliveries, with 82% of the total aircraft delivered. As domestic demand has grown, the narrowbody segment is expected to grow at a faster rate than the widebody segment. In 2022, the procurement of new aircraft in the region exceeded the pre-pandemic levels by 38% compared to 2019.

Factors such as the rising adoption of innovative cabin seats, the growing demand for luxury air travel, and the huge number of aircraft orders are expected to drive the market during the forecast period. On this note, as part of fleet expansion and the demand driven by new narrowbody aircraft with long range on major routes, airlines placed new orders, such as Rostec ordering 250 aircraft, Ryanair ordering 200 aircraft, and Wizz Air ordering 102 narrowbody aircraft. During 2023-2030, around 2,647 aircraft are to be delivered to the region, boosting the overall seating market in the region.

The surge in low cost carriers and demand for improved passenger seating experience is anticipated to aid the market growth in Europe

The importance of comfortable seating in aircraft has increased. The major reason for this is to provide a better passenger experience. The increased passenger traffic drives the demand for new aircraft procurements, creating the need for a larger cabin interior market. Airline companies in the European region are implementing fleet expansion plans to cater to the growing air passenger traffic across major countries. The United Kingdom, Germany, and Russia are expected to generate the maximum demand for new aircraft compared to other European countries.

Europe's three most prominent airline groups, Anglo-Spanish Multinational Airline IAG and Germany's Lufthansa & Air France have significantly improved their seating capacity in 2023, with healthy capacities across their route networks compared to 2022. Although these efforts have been stepped up, these carriers are still behind the levels they reached before the pandemic.

The commercial aircraft manufacturers, namely Boeing and Airbus, are expected to deliver many aircraft in the region. About 2,647 new jets are expected to be delivered across the region. Of these, 2354 jets are expected to be narrow-body aircraft. There is a high preference for smaller and more economical aircraft, along with the introduction of long-range narrow-body aircraft.

The success of LCCs is high in this region. Major airline companies in the region, such as Air France, British Airways, and Lufthansa, focus on improving the overall passenger experience in the aircraft market. This is expected to aid the region's demand for commercial aircraft cabin interior products.

Europe Commercial Aircraft Cabin Seating Market Trends

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Europe

Europe was the second-largest region with the highest air passenger traffic in 2022. Air passenger traffic in Europe reached 1.05 billion in 2022, up by 11% from 2017. Airlines are concentrating on growing their fleet sizes to meet the rising demand for air travel, which may result in a significant increase in the demand for new aircraft in Europe.

Between 2017 and 2022, a total of 1,206 new aircraft were delivered to Europe, and another 2,647 new jets are anticipated to be delivered between 2023 and 2030. During the historic period, new jet deliveries in Europe amounted to around 25% of global commercial aircraft deliveries. A number of factors may contribute to the increasing number of deliveries during the forecast period, such as LCC's business innovation to increase passenger load factors, reduce competitive costs, and create an organizational structure that satisfies the demand for travelers with a limited budget while creating distinctly affordable market opportunities. On this note, a total of 1,206 jets were delivered during this period, of which 990 were narrowbody aircraft.

As of June 2023, around 3,000+ Airbus aircraft were delivered in the region, with major deliveries by A320ceo, A320neo, A321ceo, and A321neo aircraft in the narrowbody segment, and A330-300 and A350-900 in the widebody segment. Several major airlines in Europe, such as Ryanair, Lufthansa, Wizz Air, Aeroflot Group, Air France-KLM, and EasyJet, have a backlog of over 1,600 aircraft, including a mix of narrowbody and widebody jets. Such factors are expected to aid the growth of the commercial aircraft cabin interior market in the future.

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

Europe Commercial Aircraft Cabin Seating Industry Overview

The Europe Commercial Aircraft Cabin Seating Market is fairly consolidated, with the top five companies occupying 98.19%. The major players in this market are Collins Aerospace, Jamco Corporation, Recaro Group, Safran and Thompson Aero Seating (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Air Passenger Traffic

4.2 New Aircraft Deliveries

4.3 GDP Per Capita (current Price)

4.4 Revenue Of Aircraft Manufacturers

4.5 Aircraft Backlog

4.6 Gross Orders

4.7 Expenditure On Airport Construction Projects (ongoing)

4.8 Expenditure Of Airlines On Fuel

4.9 Regulatory Framework

4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Aircraft Type

5.1.1 Narrowbody

5.1.2 Widebody

5.2 Country

5.2.1 France

5.2.2 Germany

5.2.3 Spain

5.2.4 Turkey

5.2.5 United Kingdom

5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Adient Aerospace

6.4.2 Collins Aerospace

6.4.3 Expliseat

6.4.4 Jamco Corporation

6.4.5 Recaro Group

6.4.6 Safran

6.4.7 STELIA Aerospace (Airbus Atlantic Merginac)

6.4.8 Thompson Aero Seating

6.4.9 ZIM Aircraft Seating GmbH

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS